Royal Dutch Shell

-

28/10/2015 10:53

0

0

Grupo GuitarLumber

Messages postés: 1716 -

Membre depuis: 24/6/2003

(CercleFinance.com) - Après avoir renoncé, le mois dernier, à un projet offshore au nord de l'Alaska, la major pétro-gazière Royal Dutch Shell continue de sabrer ses actifs d'Amérique du Nord. C'est cette fois le projet de Carmon Creek, situé dans l'Etat canadien de l'Alberta réputé pour ses sables bitumineux et dont le potentiel était chiffré à 80.000 barils/jour, qui passe à la trappe. Ce qui occasionnera une charge pour dépréciation de l'ordre de deux milliards de dollars sur les comptes du 3e trimestre, attendus le 29 octobre.

Le projet était sur la sellette depuis mars 2015. Hier, Shell a annoncé qu'après avoir passé en revue le projet d'un point de vue technique et avoir mis à jour ses hypothèses de coûts, il ne considérait plus, en l'état actuel des choses, que Carmon Creek pouvait figurer au sein de son portefeuille d'actifs.

Le directeur général, Ben van Beurden, a déclaré que cette décision s'était imposée au groupe en raison notamment de la faiblesse actuelle des cours du pétrole.

L'un de problèmes dénoncés le plus clairement : l'absence d'infrastructure permettant de transporter le brut qui aurait été extrait de ce projet vers les marchés pétroliers globaux.

Les travaux de développement du gisement seront gelés et jusqu'à ce qu'une décision soit prise, une maintenance minimale des infrastructures actuelles sera de rigueur.

De ce fait, les comptes du 3e trimestre seront grevés par une provision pour dépréciation de l'ordre de deux milliards de dollars (1,8 milliard d'euros environ).

|

|

Réponses

245 Réponses

... ...

|

141 de 245

-

13/5/2017 11:16

0

Ariane

Messages postés: 1317 -

Membre depuis: 29/9/2002

Ex-dividend date RDS A ADSs and RDS B ADSs May 17, 2017 Ex-dividend date RDS A and RDS B shares May 18, 2017 Record date May 19, 2017 Scrip reference share price announcement date May 25, 2017 Closing of scrip election and currency election (See Note) June 5, 2017 Pounds sterling and euro equivalents announcement date June 12, 2017 Payment date June 26, 2017

|

142 de 245

-

24/5/2017 08:46

0

waldron

Messages postés: 9812 -

Membre depuis: 17/9/2002

Royal Dutch Shell : nouvelle grosse cession en vue au Canada

Jean-Baptiste André,

publié le 24/05/2017 à 08h24

Crédit photo © Reuters

(Boursier.com) — Royal Dutch Shell

s'apprête à réaliser une nouvelle grosse cession au Canada. Le géant

pétrolier anglo-néerlandais serait en train de choisir la banque conseil

chargée de vendre sa participation de 8,8% dans Canadian Natural

Resources, croit savoir Reuters. L'agence, qui cite des personnes

proches du dossier, précise qu'au cours de clôture du titre du groupe

canadien à Toronto, la participation Shell représente un peu plus de

quatre milliards de dollars canadiens (2,65 milliards d'euros). Dans

le cadre de la cession de la plus grande partie de ses actifs dans les

sables bitumineux au Canada pour 8,5 Mds$, Royal Dutch Shell avait

acheté cette part de 8,8% dans Canadian Natural. Le géant

pétrolier prévoit d'affecter le produit de la vente de ces titres à son

programme de cessions d'actifs de quelque 30 milliards de dollars, mis

en oeuvre pour réduire son endettement depuis l'acquisition de BG l'an

dernier pour 54 milliards de dollars.

|

143 de 245

-

30/5/2017 07:32

0

waldron

Messages postés: 9812 -

Membre depuis: 17/9/2002

Total, Chevron et Shell préqualifiés pour des blocs pétroliers au Mexique Shell B (LSE:RDSB)

Graphique Intraday de l'Action Aujourd'hui : Mardi 30 Mai 2017

MEXICO (Agefi-Dow Jones)--Cinq consortiums et 20 sociétés

individuelles - parmi lesquelles des géants comme Chevron (CVX), Shell

(RDSA.LN) et Total (FP.FR) - se sont préqualifiés pour la prochaine mise

aux enchères de blocs pétroliers par le Mexique. Les candidats à ces

contrats de partage de la production portant sur 15 blocs en eaux peu

profondes dans le golfe du Mexique ont jusqu'au 19 juin pour remettre

leurs offres. Ces blocs ont une taille moyenne de 594 kilomètres carrés

et représentent des réserves potentielles totales de 1,6 milliard de

barils équivalent pétrole. La production devrait démarrer dans quatre

ans.

|

144 de 245

-

08/6/2017 13:20

0

grupo

Messages postés: 1061 -

Membre depuis: 11/5/2004

Le géant pétrolier anglo-néerlandais Shell a annoncé jeudi avoir

repris ses activités sur le terminal de Forcados, dans le sud-est du

Nigeria, après plusieurs mois de fermeture, dus à des attaques répétées

par des groupes armés.

"Nous avons repris la production

à Forcados le 6 juin, après avoir levé l'état de force majeure, que

nous avions mis en place l'année dernière", a déclaré à l'AFP, Precious

Okolobo, porte-parole de Shell.

Après l'explosion de

plusieurs lignes d'approvisionnement du terminal revendiquée par les

Vengeurs du Delta du Niger (NDA), Shell avait dû déclarer la "force

majeure" sur les exportations de brut de ce terminal en février 2016:

une mesure légale exceptionnelle pour interrompre une partie de la

production.

L'oléoduc sous-marin qui mène à Forcados,

point stratégique pour cette immense puissance pétrolière en Afrique, a

été constamment attaqué au cours de l'année 2016. Mais M. Okolobo a

affirmé que "toutes les réparations nécessaires ont abouti".

Des groupes armés indépendantistes, les NDA en tête, avaient promis de

mettre l'économie du Nigeria à genoux, réclamant une meilleure

redistribution des richesses du pétrole.

Le géant de

l'Afrique de l'Ouest, qui était jusque l'année dernière la première

économie du continent africain, est entré en récession au deuxième

trimestre 2016, sa production d'or noir ayant chuté à 1,2 millions de

barils, contre plus de 2 millions auparavant.

Des

négociations ont été engagées entre les rebelles et le gouvernement,

apaisant pour l'instant la situation dans la région du Delta.

(END) Dow Jones Newswires

June 08, 2017 06:11 ET (10:11 GMT)

|

145 de 245

-

13/6/2017 22:22

0

waldron

Messages postés: 9812 -

Membre depuis: 17/9/2002

Oil Prices Suffer First 'Death Cross' Since 2014 Collapse

by Tyler Durden

Jun 13, 2017 3:00 PM

12

SHARES Twitter Facebook Reddit For the first time since September 2014, after which oil prices collapsed almost 75%, Brent and WTI Crude futures both just flashed a 'death cross' signal as the 50-day moving-average crossed below the 200-day moving-average. The crossover is typically seen a loss of short-term

momentum and last occurred in the second half of 2014, when prices

collapsed due to oversupply amid surging U.S. shale oil production.

As Bloomberg notes, OPEC and its partners will be hoping

their efforts to curb output will be enough to support prices and

counteract any fears of growing downside risk.

However, this morning's news of "real" OPEC production may raise more doubts about the cartel's commitment (and going forward, the Qatar debacle won't help).

|

146 de 245

-

23/6/2017 16:21

0

waldron

Messages postés: 9812 -

Membre depuis: 17/9/2002

Shell : devient l'une des valeurs favorites de Credit suisse. 23/06/2017 | 11:42 Bien que le cours du

pétrole soit à la peine, Credit suisse confirme ce matin son conseil

acheteur de 'surperformance' sur l'action Royal Dutch Shell. Mieux : les

analystes ont intégré le titre à leur liste des valeurs préférées en

Europe. L'objectif de cours est fixé à 2.500 pence.

Selon une

note de recherche, le point mort de la 'major' pétrolière

anglo-néerlandaise devrait s'améliorer d'environ dix dollars par baril

par rapport aux objectifs à horizon 20119/2021 fixés par la direction.

'Au lieu se de préparer à un Brent à environ 50 dollars, Shell pourrait

bien, selon nous, s'adapter à un prix d'une quarantaine de dollars',

indique en substance une note de recherche.

En effet, avec

l'acquisition de BG Group, Shell s'est repositionné - vers le bas - sur

la courbe des coûts des gisements. Le 'nouveau Shell' est également

moins intensif en capital, juge Credit suisse. Ce qui lui permet de

'prioriser' ses investissements et de réduire le risque associé au

dividende.

|

147 de 245

-

26/6/2017 14:28

0

maywillow

Messages postés: 1324 -

Membre depuis: 27/1/2002

Total Eur2.5 (EU:FP)

Graphique Intraday de l'Action Aujourd'hui : Lundi 26 Juin 2017

LONDRES (Agefi-Dow Jones)--Les investisseurs privilégient Royal

Dutch Shell (RDSA.LN) parmi les majors pétrolières européennes, ce qui

constitue peut-être une erreur, estime HSBC. Selon la banque, la prime

offerte par Shell par rapport à BP (BP.LN) et Total (FP.FR) ne se

justifie pas. Shell présente les risques les plus élevés sur le plan de

la distribution de dividendes et, à moyen terme, son activité

d'exploration et de production paraît la moins attractive, en

particulier si les cours du pétrole baissent, explique HSBC. "D'après

nos estimations, BP et Total profiteront d'une meilleure croissance des

volumes à court terme ainsi que de la stabilité de leurs activités amont

à long terme (2020-2025), et la stratégie de leurs équipes dirigeantes

est au moins aussi offensive en matière d'objectifs d'amélioration des

rendements et de performances

financières", précise HSBC. Shell, BP et Total s'octroient chacun 0,5%,

soutenus par un léger rebond des cours du brut, après leur récente

chute.

-Sarah Kent, Dow Jones Newswires (Version française Aurélie Henri) ed: VLV

(END) Dow Jones Newswires

June 26, 2017 06:04 ET (10:04 GMT)

|

148 de 245

-

29/6/2017 18:45

0

Ariane

Messages postés: 1317 -

Membre depuis: 29/9/2002

Shell : toujours la 'super-major' préférée de Credit Suisse. 29/06/2017 | 11:36 Dans le cadre d'une

note sectorielle consacrée aux pétrolières, Credit suisse a confirmé sa

préférence, parmi les 'super-majors', pour Royal Dutch Shell. Le conseil

acheteur ('surperformance') sur le titre 'A' est donc maintenu, ainsi

que l'objectif de cours de 2.500 pence et le statut de valeur préférée

('focus list stock').

Les analystes relèvent que Shell a aligné

trois robustes trimestres consécutifs, dépassant autant les attentes du

consensus que la performance de la principale valeur comparable,

l'américaine ExxonMobil. 'Il sera intéressant de voir si la société

parvient à maintenir la cadence au 2e trimestre 2017', indique une note

de recherche en vue des semestriels.

Credit suisse ajoute que le

rapprochement avec BG Group a 'repositionné Shell vers le bas de la

courbe des coûts' des gisements. Le nouveau groupe est aussi exposé à

des actifs plus diversifiés, tant du point de vue du calendrier que de

leur rentabilité. Du côté du gaz naturel liquéfié (GNL) enfin, la

position que Shell s'est bâtie est jugée 'supérieure à celle des valeurs

comparables'.

Crédit suisse indique enfin que dans le pire des

scénarii possibles, son objectif de cours sur la valeur se situe à 2.040

pence, soit pratiquement le cours actuel. Dans le meilleur des cas, la

cible serait de 3.065 pence.

|

149 de 245

-

14/7/2017 10:10

0

La Forge

Messages postés: 1339 -

Membre depuis: 03/8/2000

The 2017 interim dividend timetable is also available on www.shell.com/dividend 2nd quarter 2017 Event Date Announcement date July 27, 2017 Ex-dividend date RDS A ADSs and RDS B ADSs August 9, 2017 Ex-dividend date RDS A and RDS B shares August 10, 2017 Record date August 11, 2017 Scrip reference share price announcement date August 17, 2017 Closing of scrip election and currency election (See Note) August 25, 2017 Pounds sterling and euro equivalents announcement date September 4, 2017 Payment date September 18, 2017

|

150 de 245

-

21/7/2017 20:59

0

La Forge

Messages postés: 1339 -

Membre depuis: 03/8/2000

Les cours de l'action Royal Dutch Shell oscille horizontalement. Cette phase de distribution doit théoriquement laisser place à un retour de la volatilité.

On pourra se positionner à l'achat pour viser les 24.31 €.

|

151 de 245

-

21/7/2017 21:02

0

La Forge

Messages postés: 1339 -

Membre depuis: 03/8/2000

Points forts - La proximité du support moyen terme des 23.08 EUR offre un bon timing pour l'achat du titre.

- La

société bénéficie de niveaux de valorisation attractifs avec un ratio

VE/CA relativement faible comparé aux autres sociétés cotées dans le

monde. - Les investisseurs qui recherchent du rendement pourront trouver dans cette action un intérêt majeur.

- L'objectif

de cours moyen des analystes suivant la valeur est relativement éloigné

et suppose un potentiel d'appréciation important.

Points faibles - Les

estimations des analystes concernant l'évolution de l'activité de la

société diffèrent de manière relativement importante les unes aux

autres. La visibilité liée à l'activité de la société apparaît

relativement faible. - Dans le passé, le groupe a souvent déçu les analystes en publiant des chiffres d'activité inférieurs à leurs attentes.

- Les

prévisions de chiffre d'affaires des analystes couvrant la société ont

été récemment revues à la baisse. Un tassement de l'activité est

nouvellement anticipé. - Les analystes ont révisé à la baisse leurs anticipations de résultats ces derniers mois.

- Au cours des 12 derniers mois, les analystes ont revu régulièrement à la baisse leurs anticipations de bénéfices.

|

152 de 245

-

25/7/2017 18:36

0

Grupo GuitarLumber

Messages postés: 1716 -

Membre depuis: 24/6/2003

LONDRES (Agefi-Dow Jones)--Les groupes

pétroliers européens ayant des activités de raffinage profitent d'une

augmentation des marges dans ce secteur, liée à la hausse saisonnière de

la demande d'essence et aux opérations de maintenance des raffineries.

Cette progression des marges ne devrait toutefois pas durer, prévient

Barclays. Les marges de raffinage ont atteint en moyenne 5,5 dollars le

baril la semaine dernière, ce qui représente le plus haut niveau depuis

septembre 2015 et une augmentation de 4 dollars le baril sur un an.

Barclays attribue cette progression à un marché du carburant

exceptionnellement tendu, à la croissance saisonnière de la demande

d'essence et à une remontée du diesel portée par des ruptures

d'approvisionnement. Barclays ne pense pas que la hausse durera plus de

quelques semaines, mais continue de priviléger les groupes présents dans

le raffinage en raison de leur flux de trésorerie, qui soutient les

dividendes. La banque a une recommandation "surpondérer" pour BP avec un

objectif de cours de 675 pence, Royal Dutch Shell (2.750 pence), Total

(60 euros), OMV (54 euros) et Repsol (20 euros).

-Philip Waller, Dow Jones Newswires (Version française Adeline Raynal) ed: LBO

(END) Dow Jones Newswires

July 25, 2017 12:11 ET (16:11 GMT)

|

153 de 245

-

31/7/2017 12:53

0

Grupo GuitarLumber

Messages postés: 1716 -

Membre depuis: 24/6/2003

Royal

Dutch Shell prévoit de supprimer environ 400 postes aux Pays-Bas,

principalement au sein de sa division "grands projets et technologies de

l'énergie" dans le cadre de son adaptation à un environnement de cours

du pétrole plus bas, montre un document interne consulté par Reuters. La deuxième compagnie pétrolière mondiale en termes de

capitalisation boursière a dit dans un communiqué en réponse à des

questions de Reuters qu'"environ 400 (salariés) étaient exposés à un

risque de licenciement au quatrième trimestre 2017/premier semestre

2018." Ce chiffre représente environ un quart des effectifs de

cette division, selon le document soumis aux instances représentatives

des salariés du groupe consulté par Reuters. Shell emploie au total

92.000 personnes dans le monde. (Tom Bergin, Marc Joanny pour le service français, édité par Véronique Tison)

|

154 de 245

-

31/7/2017 23:00

0

maywillow

Messages postés: 1324 -

Membre depuis: 27/1/2002

Shell's Downstream Operations Continue To Drive Its Profitability

July 31, 2017, 03:37:36 PM EDT

By Trefis Team, Trefis

Shutterstock photo

Royal Dutch Shell

(NYSE:RDS.A), the European integrated energy company, posted a notable

improvement in its June quarter 2017 earnings on 27th July 2017(( Royal Dutch Shell Announces June Quarter 2017 Results

, 27th July 2017, www.shell.com)), despite the slowdown in the

recovery of commodity prices during the quarter. While the oil and gas

company has witnessed a remarkable recovery in its upstream operations

on a year-on-year basis, its downstream business, particularly refining

and chemicals, continued to account for a majority of its profits.

Strong results from its downstream operations, coupled with its

consistent efforts to bring down its operating costs and capital

spending, enabled the company to report adjusted earnings of 86 cents,

beating the market expectations by a huge margin. Going forward, Shell

will continue to work towards reshaping itself by focusing on improving

its capital efficiency, reducing its costs, delivering on new projects,

and completing its divestment program. See Our Complete Analysis On Royal Dutch Shell Here  Key Operational Highlights - Shell

has seen notable growth in its deep-water and integrated gas business

since its acquisition of the BG Group. Assuming the exchange rates at

the time of BG acquisition, the company expects to achieve $4.5

billion in synergies by the end of 2017. - Shell's

integrated gas adjusted earnings for the June quarter stood at $1.2

billion, 35% higher compared to the same quarter of last year. This

growth in earnings was largely driven by higher realized oil, gas, and

LNG prices, higher LNG volumes, and lower operating expenses,

partially offset by the impact of lower production volumes. - The

company's upstream division reported adjusted earnings of $339

million in 2Q'17, as opposed to a loss of $1.3 billion in 2Q'16. This

was backed by higher price realization, increased production, and

lower depreciation (due to divestments). - Shell's downstream

operations continued to dominate its profitability in this quarter as

well. Its downstream operations, particularly refining and chemicals,

witnessed positive industry trends during the quarter, resulting in

earnings of $2.5 billion in 2Q'17 versus $1.8 billion in the year ago

quarter.

Pulling Levers To Survive The Downturn As

mentioned earlier, Shell has been focused at maneuvering four main

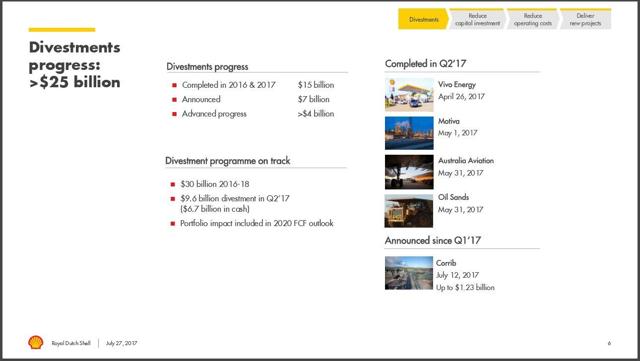

levers (described below) to weather the ongoing commodity slowdown. - Divestment

- So far, Shell has completed asset sales worth $15 billion in the

2016-2017 time frame, and has received a sum of $11.5 billion in cash

for these deals. It has further announced sales of $7 billion, which

are likely to be closed by the end of the year, taking the total of

its divestment program to $25 billion. The company indicates that it

has another $4 billion worth of deals in the pipeline, implying that

it is on track to achieve its divestment target of $30 billion by the

end of 2018. - Capital Investment

- Given the slump in the commodity prices, Shell has reduced its

capital spending (including BG Group) by $20 billion between 2014 and

2016. Since the outlook for the markets is still uncertain, the

company plans to restrict its capital investment to $25 billion in

2017, and in the range of $25 to $30 billion between 2018 and 2020.

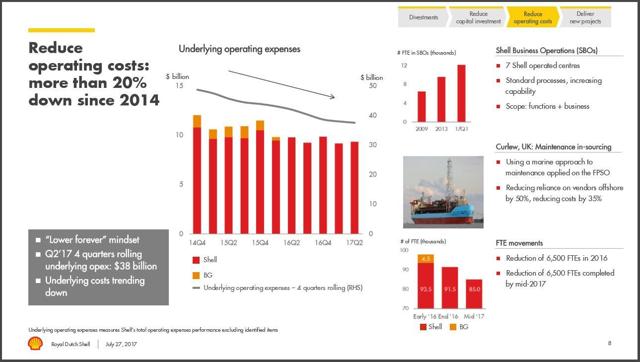

- Operating Costs

- Since 2014, Shell has managed to reduce its operating costs by

roughly $11 billion, or more than 20%. This has enabled the company to

sustain its margins in this slowdown. For the current year, the

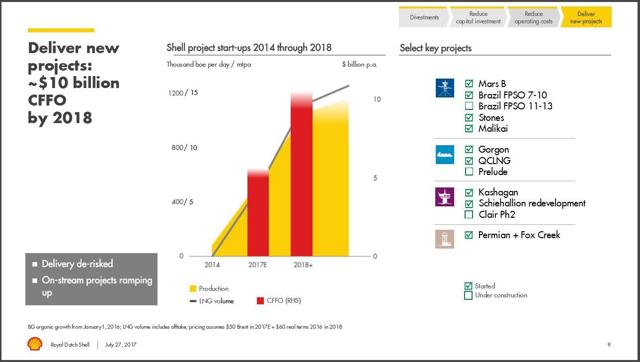

company expects to keep its operating costs below $40 billion. - Delivery of New Projects

- Shell has a robust portfolio of projects that have either become

operational or are expected to come on-stream soon. Some of the

projects that are now producing include Stones deep-water oil and gas

project in the Gulf of Mexico (GOM), the Kashagan field in Kazakhstan,

and Queensland Curtis Liquefied Natural Gas (QCLNG) plant in

Australia. The company is on track to deliver on these ongoing

projects, which are expected to produce more than 1 million barrels of

oil equivalent per day, and contribute $10 billion in cash flows by

2018.

Overall,

we believe that Shell's focus on the pulling of its four main levers

will enable it to reshape its operations and emerge out of the ongoing

commodity slump. View Interactive Institutional Research (Powered by Trefis): Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap More Trefis Research

The views and opinions expressed

herein are the views and opinions of the author and do not necessarily

reflect those of Nasdaq, Inc.

|

155 de 245

-

01/8/2017 20:40

0

maywillow

Messages postés: 1324 -

Membre depuis: 27/1/2002

Le géant pétrolier anglo-néerlandais Shell espère relancer "au plus

tôt dans la deuxième moitié d'août" sa raffinerie de Rotterdam aux

Pays-Bas, la plus grande d'Europe, à l'arrêt suite à deux incidents

survenus sur le site, a-t-il indiqué mardi.

Le site

Shell Pernis de Rotterdam a mis hors service depuis lundi midi la

plupart de ses usines "par mesures de sécurité" suite à une panne de

courant provoquée par un incendie, a rapporté le groupe dans un

communiqué.

Le feu avait pris samedi dans une centrale

électrique à haute tension de la raffinerie Shell Pernis qui est, avec

environ 60 usines, la plus grande raffinerie d'Europe et l'une des plus

grandes au monde.

L'incendie a été maîtrisé dimanche au petit matin.

Un second incident est survenu lundi lors du nettoyage d'une de ces

usines: une fuite de fluorure d'hydrogène, un gaz incolore très réactif.

"La source de la fuite a été identifiée et la fuite colmatée", a ajouté

l'entreprise.

Les deux incidents font l'objet d'une enquête.

"Nous nous attendons à relancer nos opérations au plus tôt dans la seconde moitié d'août", a déclaré un porte-parole à l'AFP.

La centrale électrique doit désormais être réparée avant que la raffinerie ne puisse être à nouveau en service.

"Nous regrettons l'impact que cela pourrait causer à nos clients et

nous faisons tout notre possible pour (le) minimiser", a-t-il ajouté, se

refusant toutefois à tout commentaire quant aux éventuelles

conséquences de cet arrêt sur le marché.

La raffinerie,

qui produit 404.000 barils de pétrole par jour, couvre une surface

équivalente à 800 terrains de football, faisant de la maintenance une

opération massive et permanente. Les produits y sont traités au travers

de pipelines dont la longueur serait équivalente à environ quatre fois

le tour de la terre.

(END) Dow Jones Newswires

August 01, 2017 12:35 ET (16:35 GMT)

|

156 de 245

-

11/8/2017 16:35

0

maywillow

Messages postés: 1324 -

Membre depuis: 27/1/2002

Royal Dutch Shell: If I Could Buy Just One Energy Stock Aug. 11, 2017 9:55 AM ET|14 comments| About: Royal Dutch Shell plc (RDS.A), RDS.B

Ray Merola Value, dividend investing, growth at reasonable price, contrarian

(6,696 followers)

Summary In 2017, most energy stocks have under performed. Amidst the castaways, there's a Super Major gem hiding in plain sight. It's a turnaround story wrapped in a 6.7% dividend yield. Of

all the companies I follow, one 2Q 2017 earnings release stood out. The

company blew out Street estimates. Management continued to fulfill

promises to investors. Remarkably, the stock resides in 2017's most

downtrodden neighborhood: Energy. The company is Royal Dutch Shell (RDS.A) (RDS.B).

For those that follow my work here on

Seeking Alpha, I've been constructive on RDS shares for a long time.

I've advocated CEO Ben van Beurden is the real deal. He's a no-nonsense

Dutchman with an eye for business simplification and efficiency;

precisely what Shell needed. In 2014, Mr. van Beurden was elevated to

the CEO role after an outstanding run at Shell Chemical. Over three-a-half years into his new role, he's not disappointed. Looking

back to 1Q 2016, Shell had just completed its BG Group acquisition. Ben

van Beurden touted it. He owned the deal. The transaction was roundly

criticized by many. Detractors declared, "The timing is terrible,"

"Shell paid far too much," and of course, "The dividend is unsustainable. It must be cut!" Some 6 quarters later, RDS stock is up 28%. The cash dividend remains at $0.94 per

ADR. In mid-2015, management made a highly unusual move for a global

corporation in the midst of a commodity collapse: CEO van Beurden and

CFO Simon Henry promised the payout would be maintained through at least

the end of 2016, despite the industry struggling with an energy

commodity collapse. Indeed, it was not

reduced, and has been maintained for an additional two quarters. In

August 2017, none withstanding the robust capital appreciation, Shell

shares still yield about 6.7%. Meanwhile, Royal Dutch Shell

began the process of concurrently re-imagining itself and absorbing the

BG Group; a company about one-quarter the size of the old Shell itself. Let's briefly walk through where we've been, and look forward to where I believe we're heading. From the Depths By

mid-2015, oil prices began to roll over, hitting rock bottom in 1Q

2016. In January and February 2016, Brent and WTI fell to the mid $20s.

Shell closed on the BG deal around the same time. The

company borrowed big to fund the $53 billion cash-and-stock

acquisition. The rock-solid balance sheet took a hit. Gearing (i.e.,

debt-to-capital) nearly doubled to 26% from just 14% at the end of 2015. Shortly after the transaction closed, van Beurden made some promises: First, he said operating costs and capital expenditures were coming down; and fast.

source for this section's slides: Shell 1Q 2016 earnings release

Second, he pointed out BG production was going up.

In late 2015, I once again advocated a position for the shares. January

2016 marked investors' point of maximum pain. RDS.A shares traded for

under $40 each, and offered nearly a 10% dividend yield. Fortitude was

required for those scaling in on the long trip down. The underlying business hit bedrock in 1Q 2016. Shell generated only $661 million operating cash flow, or an annualized $2.6 billion.

It was a pale comparison versus over $40 billion a year OCF reported in

the YE 2012-2014. In 2016, cash dividends were costing the company ~$2.5 billion per quarter. Fast-Forward to 2017 Since the close of the BG acquisition, Royal Dutch Shell has COMPLETELY absorbed the operation's capex and opex, while reducing its own legacy costs dramatically. Spending Capital spending has been reduced to $25 billion from over $40 billion a year.

source for this section's slides: Shell 2Q 2017 earnings release

The

go-forward capex run-rate is $25 billion to $30 billion a year. The

reduction is not simply a "cut." Shell now utilizes far more commercial

discipline. The company can stretch a buck farther than years' past. Opex is down 20% since 2014.

For years, Shell management emphasized span. Cost containment

was not a prime mover. No more. Under Ben van Beurden operating costs

are down, and these are staying down. It's a template he used

successfully when heading up Shell Chemical. The energy business is

notoriously cyclical; within the energy business, chemicals are cyclical

on steroids.

Divestiture Program An

announced $30 billion divestiture program remains on track. About $26

billion has been closed, is pending closure, or in advanced discussions.

Between 2016 and 2018, management promised $30 billion in cash from

divestitures. Proceeds are earmarked to reduce debt. Concerns about

Shell being forced to settle for "fire sale" prices, or an inability to

close deals fast enough failed to materialize.

As outlined initially by Van

Beurden, the 3-year divestment strategy is about simplification, not

mortgaging the future or shrinking to pay the dividend. Concurrent Production Increases At

the end of 2015 (prior to BG), Shell produced 2.95 million BoE/d. Given

more than half the divestitures complete, 2Q 2017 total production

climbed to 3.62 million BoE/d. In other words, while operating expenses

declined by 20%, energy production increased 23%. In

addition, long-lead, major capital projects are coming online. These

projects are scheduled to deliver $5 billion incremental cash flow this

year. By 2018, Shell management expects $10 billion incremental cash

flow from these projects.

Capital Returns and Debt Reduction Are In Focus CEO

Van Beurden anticipates near-term Return-on-Average-Capital-Employed

(RoACE) to reach 10%; far eclipsing the ~7% returns the company's

experienced during the 2012 to 2014 boom cycle. The mark is now 4%; up

from negative returns in 2016. As the major capital projects come

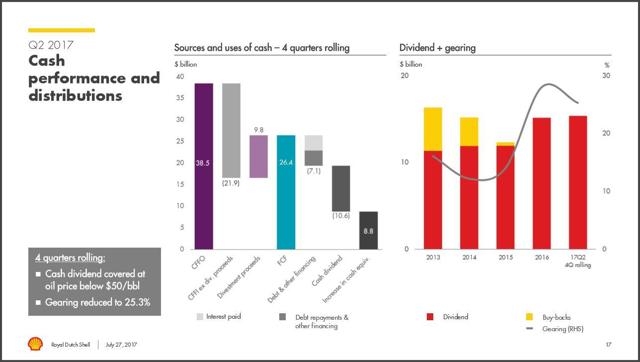

online, "dead" capital comes to life and RoACE will rise. Net debt and gearing are on the way down. Gearing is 25.3% now, on its ways towards a 20% target. Cash Flow and the Dividend Most

importantly to income investors, the trailing 4 quarters' operating

cash flow covered the dividend easily. Over these quarters, Shell

generated $38.45 billion operating cash flow. Capital expenditures were

$22.10 billion. Dividend payments totaled $10.58 billion.

The arithmetic and the chart is compelling. Indeed,

Shell is NOT borrowing to pay the dividend. Notably, the ongoing script

program continues to dilute current stockholders; however, the past

year has seen the total number of shares outstanding rise by only 2.3%.

On the 2Q 2017 conference call, management is well-aware of the script

program's dilutive effect, and desires to end it as quickly as possible.

Nonetheless, corporate financial priorities remain unchanged: - Reduce debt

- Fund the dividend

- Reinvest for growth initiatives

Shell CFO Jessica Uhl reinforced management's view of the script program during the 2Q 2017 conference call: And

I do want it to be very clear, our commitment to taking the scrip off

as soon as it's appropriate to do so. So, the - if I've used different

language, I would not want that to leave any other impression than that

one. It is about getting our gearing down to 20%, getting our debt to

the right levels and taking the scrip off as soon as possible. We're

absolutely committed to doing that.

Again, we're focusing on the

fundamentals of the company and driving our cash flow to a different

level, driving our profitability to a different level. This will make us

a healthier company, a resilient company that ultimately can pay our

dividends by cash year in year out and that's really what we're driving

our company to be and again to get the scrip off as soon as we possibly

can.

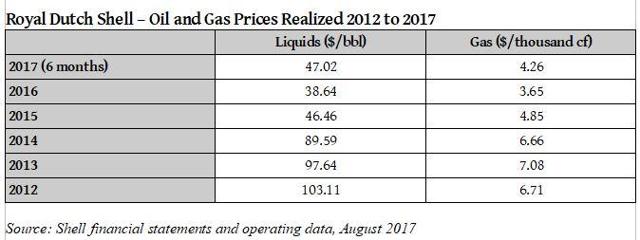

All This While Prices Realized Plummeted In order to appreciate the magnitude of these achievements, here's a table summary of Shell's 2012 to 2017 prices realized:

Crude oil prices have been slashed in

half. Gas is down my more than 40 percent. Shell managed to completely

integrate and absorb another major corporation, grind down costs,

increase total production, and generate nearly as much cash flow as it

did in 2013. I find the picture pretty clear, don't you? Looking Forward Under

CEO Ben van Beurden and his staff, Royal Dutch Shell is positioned to

manage itself in a sub-$50/bbl oil world. Shell does not need $60 or $70

oil to sustain positive net cash flow. Tight

controls on opex and capex are not about to slip under the current

regime. Heading into 2018, a bevy of high-profile, cash-rich projects

are poised to generate incremental cash flow. Shell is running for cash,

capital returns, and intent upon making a long-term, sustainable

investment case for its stockholders. I maintain the

dividend is secure. I've stated this position previously; and continue

to do so. Shell has not cut its dividend since 1945. It is highly

unlikely to happen now: not on Ben van Beurden's watch. I

contend RDS shares are arguably the best deal in the oil patch: a sound

and improving balance sheet, an indisputably outstanding franchise, the

company is very well-managed, generates enormous cash flow, and is

exceedingly shareholder-friendly. Additional disclosure: very long RDS.A

|

157 de 245

-

12/8/2017 12:42

0

Ariane

Messages postés: 1317 -

Membre depuis: 29/9/2002

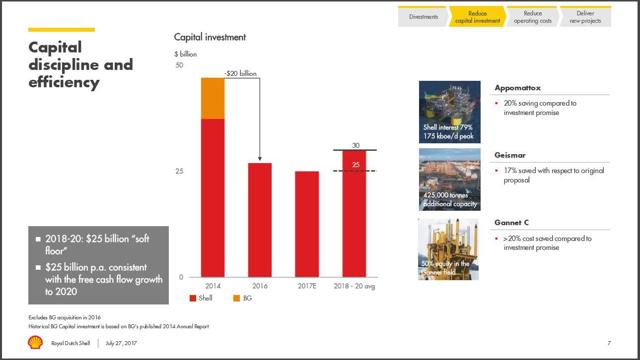

Appomattox We

have taken the final investment decision to move ahead with the

Appomattox deep-water project in the Gulf of Mexico, the latest of our

deep-water developments. Key facts Location: Gulf of Mexico, 130 kilometres (80 miles) off Louisiana Depth: 2,195 metres (7,200 feet) Interests: Shell (79% operator), Nexen Petroleum Offshore USA Inc. (21%) Fields: Appomattox, Vicksburg Average peak annual production: 175,000 barrels of oil equivalent Project development On July 1, 2015, Shell announced the final investment decision

to advance the Appomattox deep-water development in the Gulf of Mexico.

This decision authorises construction and installation of what will be

our eighth and largest floating platform in the Gulf. The

Appomattox development will initially produce from the Appomattox and

Vicksburg fields, with average peak production estimated to reach

approximately 175,000 barrels of oil equivalent per day (boe/d). Currently,

we are the only operator in the Gulf of Mexico with commercial

deep-water discoveries in this formation, called Norphlet, which dates

back 150-200 million years to the Jurassic period. Technology During

design work for Appomattox, we reduced the total project cost by 20%

thanks in part to design improvements. These include advancements from

previous four-column production hosts, such as the Olympus tension leg platform. Shell

Pipeline Company LP also made a final investment decision on the Mattox

Pipeline, a 24-inch corridor pipeline that will transport crude oil

from the Appomattox host to an existing offshore structure in the South

Pass area and then connect onshore through an existing pipeline. Deep-water milestones  A long history of deep-water development

|

158 de 245

-

06/9/2017 22:06

0

maywillow

Messages postés: 1324 -

Membre depuis: 27/1/2002

Le géant pétrolier Royal Dutch Shell a annoncé qu'il investirait un

milliard de dollars au Mexique durant la prochaine décennie, après y

avoir ouvert mardi sa première station-essence.

Cet

investissement se réalisera si les conditions du marché se maintiennent,

a précisé l'entreprise dans un communiqué, qui consacrera cette somme à

"l'expansion et l'amélioration du réseau de succursales".

La major pétrolière anglo-néerlandaise a ouvert mardi sa première

station-service dans le pays, à Tlalnepantla, dans la banlieue de

Mexico, premier jalon de son futur réseau.

Il s'agit

d'"un jalon pour Shell, cela montre notre engagement envers le Mexique,

le cinquième plus important consommateur d'essence au monde. C'est un

marché important et en croissance", a souligné Istvan Kapitany,

vice-président des stations Shell.

Shell est la

première compagnie au monde pour la vente d'essence au détail, avec

43.000 stations dans 80 pays, fournissant près de 30 millions de clients

chaque jour.

Outre le Mexique, Shell investit dans

plusieurs autres marchés en développement, comme le Brésil, l'Inde, la

Chine et l'Indonésie.

Le Mexique a adopté en 2014 une

réforme historique de son secteur énergétique mettant fin au monopole de

l'entreprise d'Etat Pemex, en vigueur depuis 1938. Elle a permis

l'entrée sur le marché mexicain d'investisseurs étrangers et privés,

notamment pour la commercialisation de carburant.

(END) Dow Jones Newswires

September 06, 2017 11:47 ET (15:47 GMT)

|

159 de 245

-

07/9/2017 17:21

0

waldron

Messages postés: 9812 -

Membre depuis: 17/9/2002

Shell International Finance B.V. and Royal Dutch Shell plc: Publication of Prospectus Supplement 07/09/2017 3:53pm PR Newswire (US)

Royal Dutch Shell (NYSE:RDS.B)

Intraday Stock Chart Today : Thursday 7 September 2017

LONDON, September 7, 2017 /PRNewswire/ -- The following documents (the "Documents") are available for viewing: Prospectus Supplement dated 4 September 2017 Shell International Finance B.V. unaudited interim financial statements for the six month period ended 30 June 2017 The Documents must be read in conjunction with the Information Memorandum dated 8 August 2017

relating to the Programme. The Information Memorandum constitutes a

base prospectus for the purposes of Article 5.4 of Directive 2003/71/EC

as amended. Full information on Shell International Finance B.V. and Royal Dutch Shell plc(NYSE: RDS.A) (NYSE: RDS.B) is only available on the basis of the Information Memorandum. The Documents are available for viewing at the 'Financial

Publications' section of Shell's website. To view the Documents, please

paste the following URLs into the address bar of your browser. Shell International Finance B.V. unaudited interim financial statements for the six month period ended 30 June 2017 http://www.shell.com/investors/financial-reporting... Prospectus Supplement dated 4 September 2017 http://www.shell.com/investors/financial-reporting... Other content available on Shell's website and the content of any

other website accessible from hyperlinks on Shell's website is not

incorporated into, and does not forms part of, this announcement. The Documents have also been submitted to the National Storage

Mechanism and will shortly be available for inspection at

http://www.morningstar.co.uk/uk/nsm. DISCLAIMER - INTENDED ADDRESSEES Please note that the information contained in the Information

Memorandum may be addressed to and/or targeted at persons who are

residents of particular countries (specified in the Information

Memorandum) only and is not intended for use and should not be relied

upon by any person outside these countries and/or to whom the offer

contained in the Information Memorandum is not addressed. Prior to

relying on the information contained in the Information Memorandum, you

must ascertain from the Information Memorandum whether or not you are

part of the intended addressees of the information contained therein. This publication does not constitute an offering of the securities

described in the Information Memorandum for sale in the United States.

This is not for distribution in the United States. The securities have

not been, and will not be, registered under the United States Securities

Act of 1933, as amended (the "Securities Act") or under any relevant

securities laws of any state of the United States and are subject to U.S. tax law requirements. Subject to certain exceptions, the securities may not be offered or sold within the United States

or to or for the account or benefit of U.S. persons, as such terms are

defined in Regulation S under the Securities Act. There will be no

public offering of the securities in the United States. Your right to access this service is conditional upon complying with the above requirement. Enquiries:

Shell Media Relations

International, UK, European Press: +44 (0)207-934-5550

Shell Investor Relations

Europe: + 31(0)70-377-3996

SOURCE Shell International Finance BV and Royal Dutch Shell plc.

|

160 de 245

-

02/10/2017 15:38

0

grupo

Messages postés: 1061 -

Membre depuis: 11/5/2004

LONDRES (Agefi-Dow Jones)--La performance

en Bourse des grands groupes pétroliers européens laisse à désirer

cette année, mais ceux-ci sont en train de prouver leur capacité à

surmonter le contexte actuel de faiblesse des cours de l'or noir.

Barclays estime que les bénéfices de ces groupes au troisième trimestre

devraient s'inscrire en hausse de 60% en moyenne par rapport à l'année

dernière, grâce à leurs mesures d'adaptation à un environnement marqué

par un prix du baril à 50 dollars et aux bons résultats des activités

raffinage et commercialisation. Les groupes pétroliers se rapprochent

également de leur objectif de couvrir leurs dividendes avec les

liquidités générées par leurs activités. Selon Barclays, le cours moyen

nécessaire pour que ces groupes couvrent leurs dépenses d'investissement

et leurs dividendes grâce à la trésorerie au troisième trimestre se

situe à 52 dollars le baril, soit une baisse de 4 dollars le baril par

rapport au deuxième trimestre.

-Sarah Kent, Dow Jones Newswires (Version française Maylis Jouaret) ed : LBO

(END) Dow Jones Newswires

October 02, 2017 08:36 ET (12:36 GMT)

|

|

245 Réponses

... ...

|

|

Messages à suivre: (245)

Dernier Message: 05/Mai/2022 07h24

|

|

Hot Features

Hot Features

Afficher tous les Messages

Afficher tous les Messages Retourner à la liste

Retourner à la liste Rafraîchir

Rafraîchir

Ex-dividend date RDS A ADSs and RDS B ADSs May 17, 2017 Ex-dividend date RDS A and RDS B shares May 18, 2017 Record date May 19, 2017 Scrip reference share price announcement date May 25, 2017 Closing of scrip election and currency election (See Note) June 5, 2017 Pounds sterling and euro equivalents announcement date June 12, 2017 Payment date June 26, 2017