Filed by Magenta Therapeutics, Inc. Pursuant to Rule 425 under the

Securities Act of 1933, as amended, and deemed filed pursuant to Rule 14a-12 of the Securities Exchange Act of 1934, as amended Subject Company: Magenta Therapeutics, Inc. (Commission File No. 333-271917) Corporate Presentation August

2023

DISCLAIMER Forward Looking Statements Certain statements in this

presentation (“Presentation”), other than purely historical information, may constitute “-florw ookard ing statements” within the meaning of the federal securities laws, including for purposes of the safe harbor provisions

under the United Stated Private Securities Litigation Reform Act of 1995, concerning Magenta Therapeutics, Inc. (“Magenta”), Dianthus Therapeutics, Inc. (“Dianthus”), a proposed concurrent financing and the proposed business

combination between Magenta and Dianthus (the “Proposed Trans an acd tion oth”)er matters. These forward-looking statements include, but are not limited to, express or implied statements regarding Magenta’s or Dianthus’

expectations, hopes, beliefs, intentions or s gies tr reg ate arding the future, including, without limitation, statements regarding: the Proposed Transaction and the expected effects, perceived benefits or opportunities and related timing with

respect thereto, expectations regarding or plans for discovery, preclinical studies, clinical trials and research and development programs, in particular with respect to DNTH103, and any developments or results in connection therewith, including the

target product profile of DNTH103; the anticipated timing of the results from those studies and trials; expectations regarding the use of proceeds and the time period over which the combined company’s capital resources will be sufficient to

fund its anticipated operations; expectations regarding the market and potential opportunities for complement therapies, in particular with respect to DNTH103; and the expected trading of the combined company’s common stock on Nasdaq under the

ticker symbol “DNTH.” In addition, any statements that refer to projections, forecasts, or other characteri of zfati utuon re sev ents or circumstances, including the projected initiation timing of Dianthus clinical trials, and any

underlying assumptions of any of the foregoing, are forward-looking statements. The words “opportuni”ty ,“potential,” “milestones,” “runway,” “will,” “anticipate,”

“achieve,” “ne -term ar ,” “catalysts,” “pursue,” “pipeline,” “believe,” “continue,” “could,” “estimate,” “expect,”

“intend,” “may,” “might,” “plos ans,”i “ ble,” p “predict,” “project,” “should,” “strategy,” “strive,” “would,”

“aim,” “target,” “commit,” and similar expressions (including the negatives of these terms or variations of them) generally identify forward-looking statements, but the absence of these words does not mean that

statement is not forward looking. Forward-looking statements are subject to risks, uncertainties and other factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements. These

forward-looking statements are based on current expectations and assumptions that, while considered reasonable by Magenta and its management, or Dianthus and its management, as the case may be, are inherently uncertain. New risks and uncertainties

may emerge from time to time, and it is not possible to predict or identify all risks and uncertainties. Factors that may cause actual results to differ materially from current expectations include, but are not limited to: the risk that the

conditions to the closing or consummation of the Proposed Transaction are not satisfied, including the failure to obtain stockholder approval for the Proposed Transaction; the risk that the concurrent financing is not completed in a timely manner or

at all; uncertainties as to the timing of the consummation of the Proposed Transaction and the ability of each of Magenta and Dianthus to consummate the transactions contemplated; risks related to Magenta’s continued listing on the Nasdaq

until closing of the Proposed Transaction and the combined company’s ability to remain listed following the Proposed Tranisskac s tiron elate ; rd to Magenta’s and Dianthus’ ability to correctly estimate their respective operating

expenses and expenses associated with the Proposed Transaction, as applicable, as well as uncertainties regarding the impact any delay in the closing would have on the anticipated cash resources of the resulting combined company upon closing and

other events and unanticipated spending and costs that could reduce the combined company’s cash resources; the occurrence of any event, change or other circumstance or condition that could give rise to the termination of the business

combination between Magenta and Dianthus; the effect of the announcement or pendency of the business combination on Magenta’s or Dianthus’ business relationships, operating results and business generally; costs related to the Proposed

ctiT on rans ; the a outcome of any legal proceedings that may be instituted against Magenta, Dianthus or any of their respective directors or officers related to the merger agreement or the transactions contemplated thereby; the ability of Magenta

or Dianthus to protect their respective intellectual property rights; competitive responses to the Proposed Transaction; unexpected costs, charges or expenses resulting from the Proposed Transaction; potential adverse reactions or changes to

business relationships resulting from the announcement or completion of the Proposed Transaction; legislative, regulatory, political and economic developments; and those uncertainties and factors set forth in the sections entitled “Risk

Factors,” “Risk Factor Summary” and “Forw-ard Looking Statements” in Magenta’s Annual Report on Form -K f10 iled with the Securities and Exchange Commission (“SEC”) on March 23, 2023, in other filings

by Magenta from time to time with the SEC and any risk factors related to Magenta or Dianthus made available to you in connection with the Proposed Transaction, as well as risk factors associated with companies, such as Dianthus, that operate in the

biopharma industry. Should one or more of these risks or uncertainties materialize, or should any of Magenta’s or Dianthus’ assumptions prove incorrect, actual results may vary in material respects from those projected in these

forward-looking statements. Nothing in this Presentation should be regarded as a representation by any person that the forward-looking statements set forth herein will be achieved or that any of the contemplated results of such forward-looking

statements will be achieved. You should not place undue reliance on forward-looking statements in this Presentation, which speak only as of the date they are made and are qualified in their entirety by reference to the cautionary statements herein.

Neither Magenta nor Dianthus undertakes or accepts any duty to release publicly any updates or revisions to any forward-looking statements. This Presentation does not purport to summarize all of the conditions, risks and other attributes of an

investment in Magenta or Dianthus. 2

DISCLAIMER (continued) No Offer or Solicitation This Presentation and the

information contained herein is not intended to and shall not constitute (i) a solicitation of a proxy, consent or approval with respect to any securities or in respect of the Proposed Transaction or (ii) an offer to buy or sell, or the solicitation

of an offer to buy or sell, any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such

jurisdiction. No offer of securities shall be made, except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended, or an exemption therefrom. NEITHER THE SEC NOR ANY STATE SECURITIES COMMISSION HAS

APPROVED OR DISAPPROVED OF THE SECURITIES OR DETERMINED IF THIS PRESENTATION IS TRUTHFUL OR COMPLETE. Important Additional Information About the Proposed Transaction and Where to Find It This Presentation is not a substitute for the registration

statement on Form S-4, as amended, or for any other document that Magenta filed or may file with the SEC in connection with the Proposed Transaction. In connection with the Proposed Transaction, Magenta filed with the SEC a registration statement on

Form S-4, as amended, which contains a definitive proxy statement/prospectus of Magenta. The registration on Form S-4 was declared effective by the SEC on August 1, 2023, and the special meeting of Magenta stockholders is scheduled to be held on

September 8, 2023. Magenta may also file other relevant documents regarding the Proposed Transaction with the SEC. MAGENTA URGES INVESTORS AND STOCKHOLDERS TO READ THE REGISTRATION STATEMENT ON FORM S-4, THE DEFINITIVE PROXY STATEMENT/PROSPECTUS AND

ANY OTHER RELEVANT DOCUMENTS THAT ARE OR MAY BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION ABOUT MAGENTA, DIANTHUS, THE

PROPOSED TRANSACTION AND RELATED MATTERS. Investors and stockholders are able to obtain free copies of the definitive proxy statement/prospectus and other documents filed with the SEC by Magenta through the website maintained by the SEC at

www.sec.gov. In addition, investors and stockholders should note that Magenta communicates with investors and the public using its website (www.magentatx.com) where anyone is able to obtain free copies of the definitive proxy statement/prospectus

and other documents filed by Magenta with the SEC, and stockholders are urged to read the definitive proxy statement/prospectus and the other relevant materials filed with the SEC before making any voting or investment decision with respect to the

Proposed Transaction. Participants in the Solicitation Magenta, Dianthus and their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from stockholders in connection with the Proposed

Transaction. Information about Magenta’s directors and executive officers is included in Magenta’s most recent Annual Report on -F Korm , inc lud 10ing any information incorporated therein by reference, as filed with the SEC. Information

about Magenta’s and Dianthus’ respective directors and executive officers and their interests in the Proposed Transiac ncti lud oned is i n the definitive proxy statement/prospectus relating to the Proposed Transaction filed with the

SEC. These documents can be obtained free of charge from the sources indicated above. Industry and Market Data Certain information contained in this Presentation relates to or is based on studies, publications, surveys and Dian thu internal s’

ow es n timates and research. In this Presentation, Magenta and Dianthus rely on, and refer to, publicly available information and statistics regarding market participants in the sector in which Dianthus competes and other industry data. Any

comparison of Dianthus to any other entity assumes the reliability of the information available to Dianthus. Dianthus obtained this information and statistics from third-party sources, including reports by market research firms and company filings.

In addition, all of the market data included in this Presentation involve a number of assumptions and limitations, and there can be no guarantee as to the accuracy or reliability of such assumptions. Finally, while Dianthus believes its internal

research is reliable, such research has not been verified by any independent source and neither Magenta nor Dianthus has independently verified the information. Trademarks Magenta and Dianthus own or have rights to various trademarks, service marks

and trade names that they use in connection with the operation of their respective businesses. This Presentation may also contain trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective

owners. The use or display of third parties’ trademarks, service marks, trade names or products in this Presentation is not intended to, and does not imply, a relationship with Magenta or Dianthus, or an endorsement or sponsorship by or of

Magenta or Dianthus. Solely for convenience, some of the 3 trademarks, service marks, trade names and copyrights referred to in this Presentation may be listed without the TM, SM, © or ® symbols, but such references are not intended to

indicate in any way that Magenta and Dianthus will not assert, to the fullest extent under applicable law, the rights of the applicable owners, if any, to these trademarks, service marks, trade names and copyrights.

Advancing next-generation complement therapies to improve the lives of

autoimmune disease patients Founded in 2019 to develop next-generation complement therapies to treat severe autoimmune diseases Lead program, DNTH103, is a potent investigational monoclonal antibody that targets the classical complement pathway by

selectively inhibiting active C1s protein DNTH103 intended to be the first subcutaneous, self-administered injection dosed as infrequently as once-every-two-weeks to treat generalized Myasthenia Gravis Top-line Ph. 1 data confirm a ~60-day

half-life, potent classical pathway inhibition, and a potentially differentiated safety profile Ph. 2 trials in multiple neuromuscular indications starting with generalized Myasthenia Gravis in Q1’24 targeting top-line results in 2H’25

Cash runway expected to fund operations into Q2’26 4

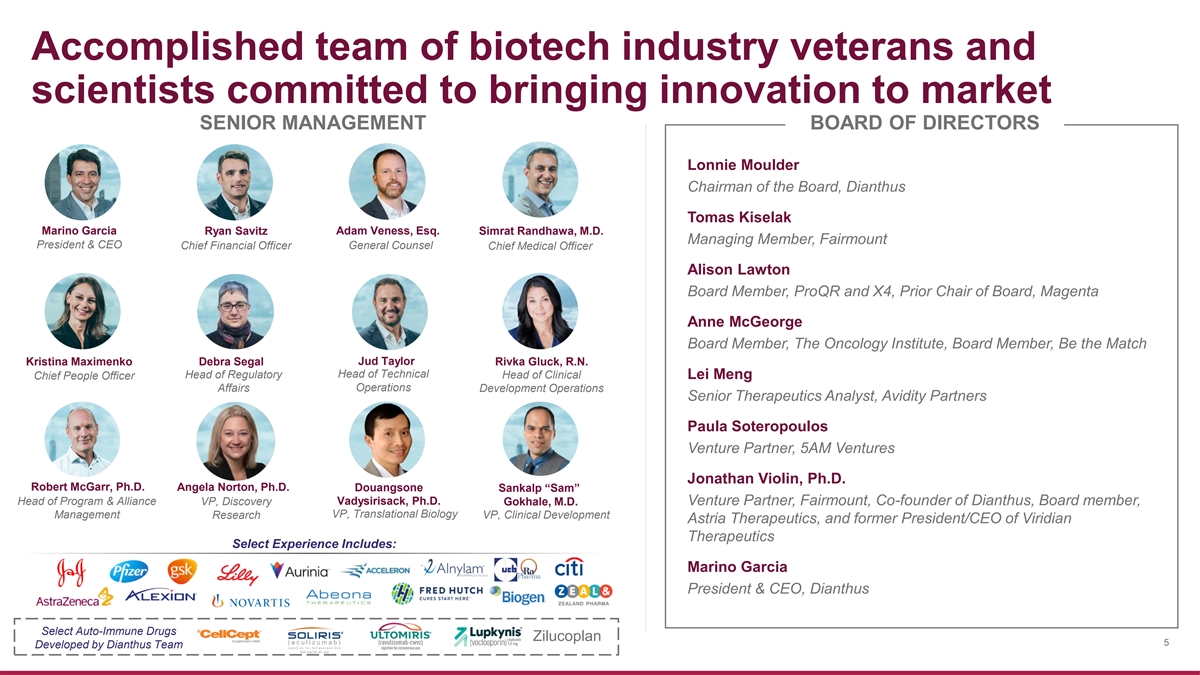

Accomplished team of biotech industry veterans and scientists committed to

bringing innovation to market SENIOR MANAGEMENT BOARD OF DIRECTORS Lonnie Moulder Chairman of the Board, Dianthus Tomas Kiselak Marino Garcia Ryan Savitz Adam Veness, Esq. Simrat Randhawa, M.D. Managing Member, Fairmount President & CEO General

Counsel Chief Financial Officer Chief Medical Officer Alison Lawton Board Member, ProQR and X4, Prior Chair of Board, Magenta Anne McGeorge Board Member, The Oncology Institute, Board Member, Be the Match Jud Taylor Kristina Maximenko Debra Segal

Rivka Gluck, R.N. Head of Technical Head of Regulatory Head of Clinical Lei Meng Chief People Officer Operations Affairs Development Operations Senior Therapeutics Analyst, Avidity Partners Paula Soteropoulos Venture Partner, 5AM Ventures Jonathan

Violin, Ph.D. Robert McGarr, Ph.D. Angela Norton, Ph.D. Douangsone Sankalp “Sam” Head of Program & Alliance VP, Discovery Vadysirisack, Ph.D. Venture Partner, Fairmount, Co-founder of Dianthus, Board member, Gokhale, M.D. VP,

Translational Biology Management Research VP, Clinical Development Astria Therapeutics, and former President/CEO of Viridian Therapeutics Select Experience Includes: Marino Garcia President & CEO, Dianthus Select Auto-Immune Drugs Zilucoplan 5

Developed by Dianthus Team

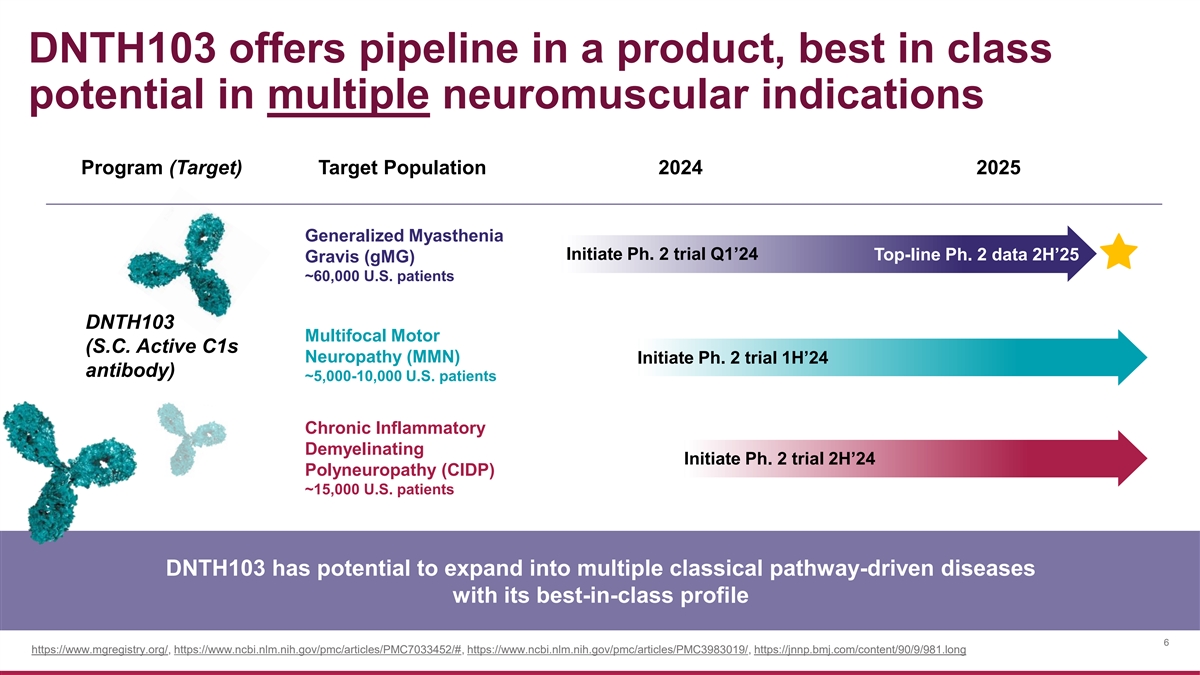

DNTH103 offers pipeline in a product, best in class potential in multiple

neuromuscular indications Program (Target) Target Population 2024 2025 Generalized Myasthenia Initiate Ph. 2 trial Q1’24 Top-line Ph. 2 data 2H’25 Gravis (gMG) ~60,000 U.S. patients DNTH103 Multifocal Motor (S.C. Active C1s Neuropathy

(MMN) Initiate Ph. 2 trial 1H’24 antibody) ~5,000-10,000 U.S. patients Chronic Inflammatory Demyelinating Initiate Ph. 2 trial 2H’24 Polyneuropathy (CIDP) ~15,000 U.S. patients DNTH103 has potential to expand into multiple classical

pathway-driven diseases with its best-in-class profile 6 https://www.mgregistry.org/, https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7033452/#, https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3983019/,

https://jnnp.bmj.com/content/90/9/981.long

DNTH103 Opportunity in Myasthenia Gravis

gMG represents a multi billion-dollar opportunity with only two approved

classes, each with room to improve Complement Class FcRn Class Soliris & Ultomiris U.S. gMG estimated Vyvgart sales >$5B in sales and in gMG showing rapid growth patient population: growing ~60,000 Approved in gMG, aHUS, Estimated gMG peak

sales >$3BN NMOSD, PNH $269.3 Ultomiris Soliris $5,727 $5,362 $5,141 $218.0 $1,965 $1,389 $1,077 $173.4 $131.3 $4,064 $3,973 $74.8 $3,762 $21.2 Q1'22 Q2'22 Q3'22 Q4'22 Q1'23 Q2'23 2020 2021 2022 $ in millions. Soliris & Ultomiris 2021 sales

account for 1/1 – 6/30 & 7/21 – 12/31. Evaluate Pharma 8 https://www.mgregistry.org/, https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7033452/#

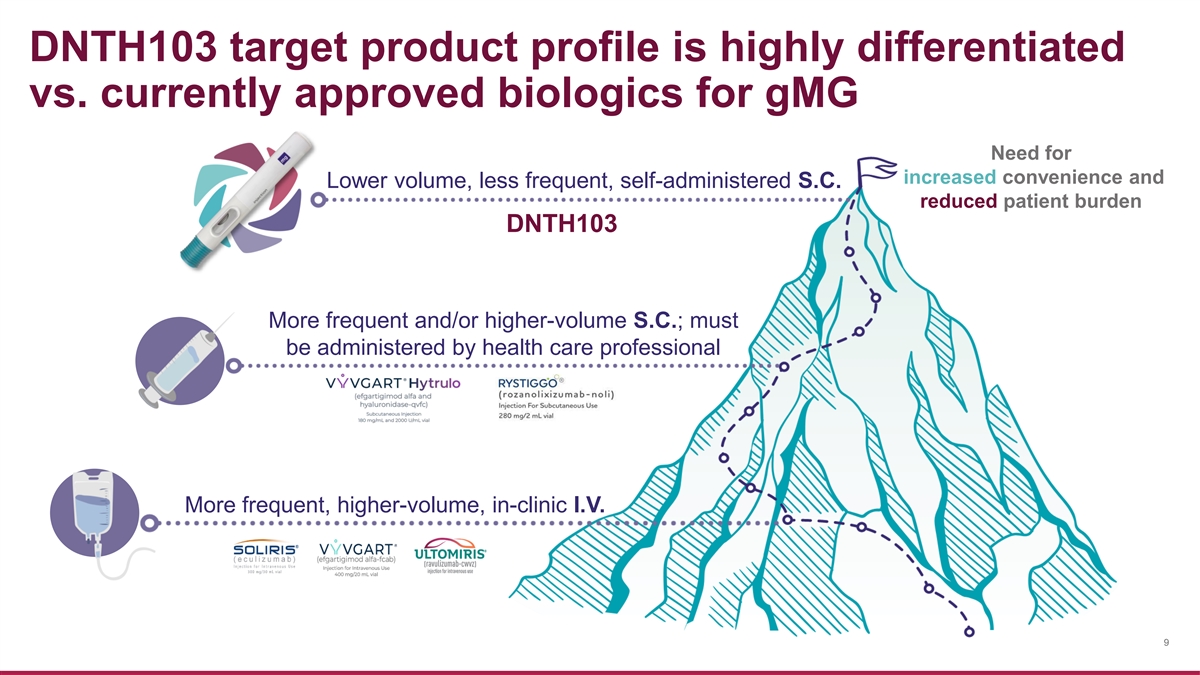

DNTH103 target product profile is highly differentiated vs. currently

approved biologics for gMG Need for increased convenience and Lower volume, less frequent, self-administered S.C. reduced patient burden DNTH103 More frequent and/or higher-volume S.C.; must be administered by health care professional More frequent,

higher-volume, in-clinic I.V. 9

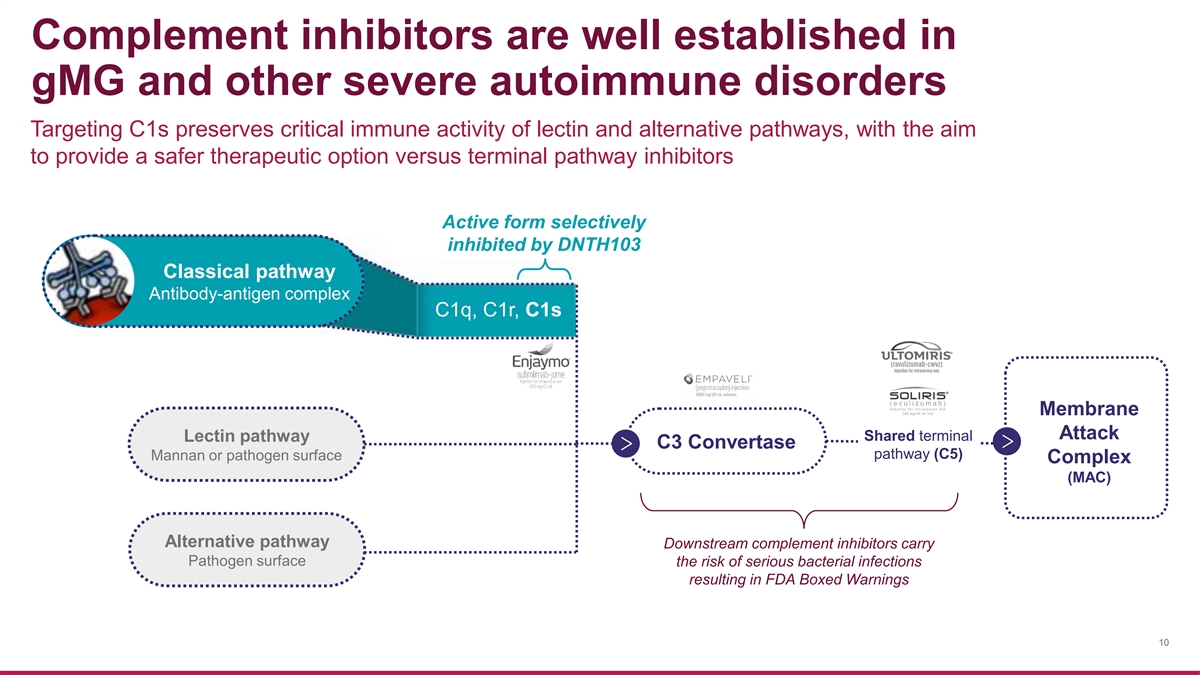

Complement inhibitors are well established in gMG and other severe

autoimmune disorders Targeting C1s preserves critical immune activity of lectin and alternative pathways, with the aim to provide a safer therapeutic option versus terminal pathway inhibitors Active form selectively inhibited by DNTH103 Classical

pathway Antibody-antigen complex C1q, C1r, C1s Membrane Attack Shared terminal Lectin pathway C3 Convertase pathway (C5) Mannan or pathogen surface Complex (MAC) Alternative pathway Downstream complement inhibitors carry Pathogen surface the risk of

serious bacterial infections resulting in FDA Boxed Warnings 10

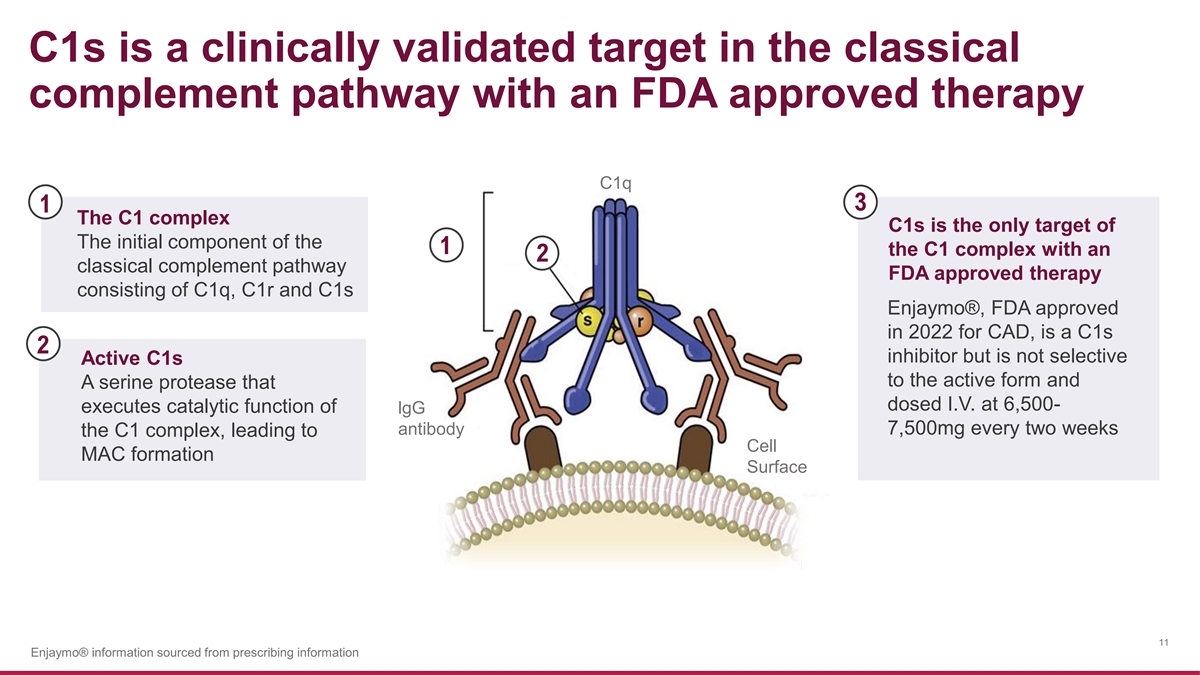

C1s is a clinically validated target in the classical complement pathway

with an FDA approved therapy C1q 3 1 The C1 complex C1s is the only target of The initial component of the 1 the C1 complex with an 2 classical complement pathway FDA approved therapy consisting of C1q, C1r and C1s Enjaymo®, FDA approved in

2022 for CAD, is a C1s 2 inhibitor but is not selective Active C1s to the active form and A serine protease that dosed I.V. at 6,500- executes catalytic function of lgG antibody 7,500mg every two weeks the C1 complex, leading to Cell MAC formation

Surface 11 Enjaymo® information sourced from prescribing information

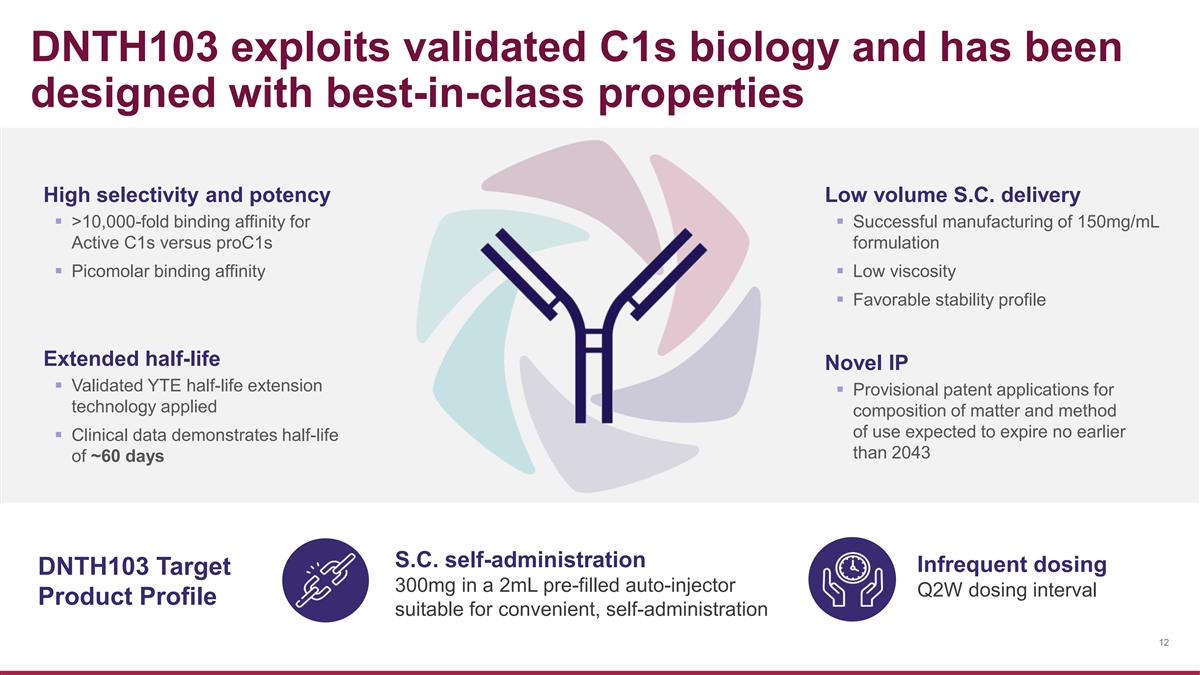

DNTH103 exploits validated C1s biology and has been designed with

best-in-class properties High selectivity and potency Low volume S.C. delivery ▪ >10,000-fold binding affinity for ▪ Successful manufacturing of 150mg/mL Active C1s versus proC1s formulation ▪ Picomolar binding affinity▪

Low viscosity ▪ Favorable stability profile Extended half-life Novel IP ▪ Validated YTE half-life extension ▪ Provisional patent applications for technology applied composition of matter and method of use expected to expire no

earlier ▪ Clinical data demonstrates half-life than 2043 of ~60 days S.C. self-administration Infrequent dosing DNTH103 Target 300mg in a 2mL pre-filled auto-injector Q2W dosing interval Product Profile suitable for convenient,

self-administration 12

DNTH103 Clinical Development

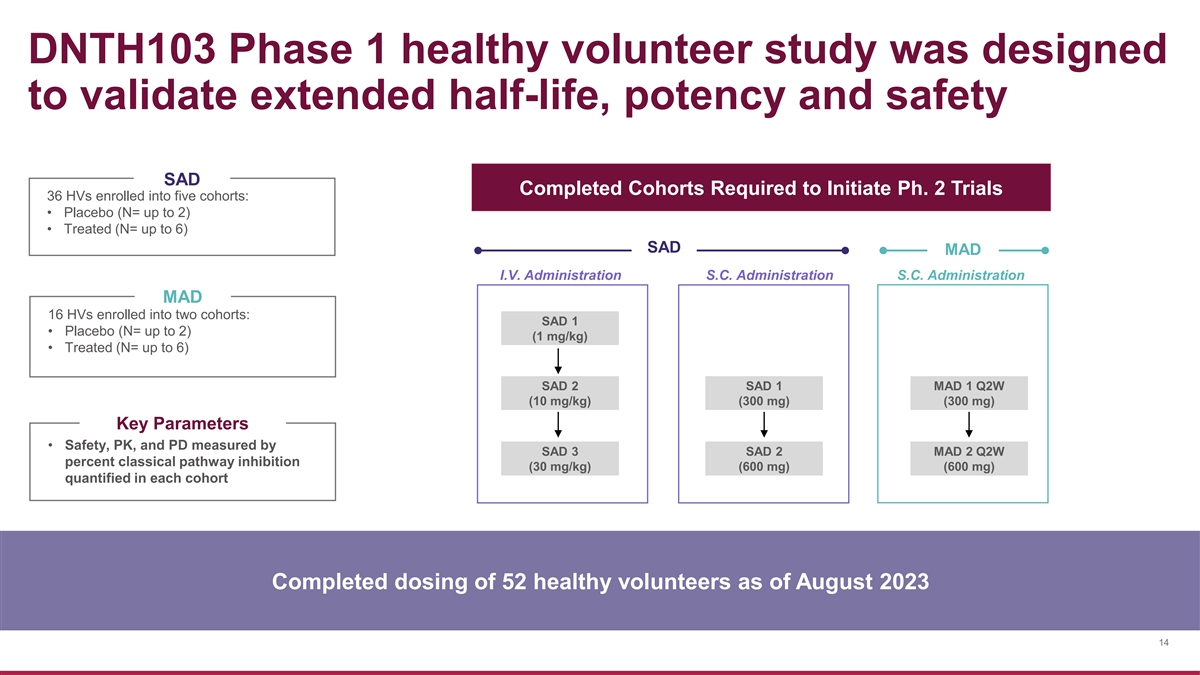

DNTH103 Phase 1 healthy volunteer study was designed to validate extended

half-life, potency and safety SAD Completed Cohorts Required to Initiate Ph. 2 Trials 36 HVs enrolled into five cohorts: • Placebo (N= up to 2) • Treated (N= up to 6) SAD MAD I.V. Administration S.C. Administration S.C. Administration

MAD 16 HVs enrolled into two cohorts: SAD 1 • Placebo (N= up to 2) (1 mg/kg) • Treated (N= up to 6) SAD 2 SAD 1 MAD 1 Q2W (10 mg/kg) (300 mg) (300 mg) Key Parameters • Safety, PK, and PD measured by SAD 3 SAD 2 MAD 2 Q2W percent

classical pathway inhibition (30 mg/kg) (600 mg) (600 mg) quantified in each cohort Completed dosing of 52 healthy volunteers as of August 2023 14

DNTH103 has demonstrated deep and sustained complement inhibition in

healthy volunteers I.V. SAD: S.C. MAD: PK/PD: Half-life Extended PK (~60-days) Strong Accumulation with Q2W Dosing Analysis Demonstrates IC90 of 83 µg/mL 150 600 100 500 80 400 100 60 300 40 200 50 20 100 0 0 0 0 7 14 21 28 0 7 14 21 28 35 -20

100 220 340 460 580 700 Time (Days) Time (Days) DNTH103 Concentration (µg/mL) 1 mg/kg IV SAD 10 mg/kg IV SAD 30 mg/kg IV SAD 300 mg SC SAD 1 mg/kg IV SAD 10 mg/kg IV SAD 30 mg/kg IV SAD 300 mg SC MAD 600 mg SC MAD Data comprised of 52 HVs from

7 cohorts 600 mg SC SAD 300 mg SC MAD 600 mg SC MAD DNTH103 was generally well tolerated No SAEs, no complement-related infections seen in healthy volunteers 15 DNTH103 Concentration (µg/mL) (Mean SE) DNTH103 Concentration (µg/mL) (Mean

SE) CH50 Inhibition (%)

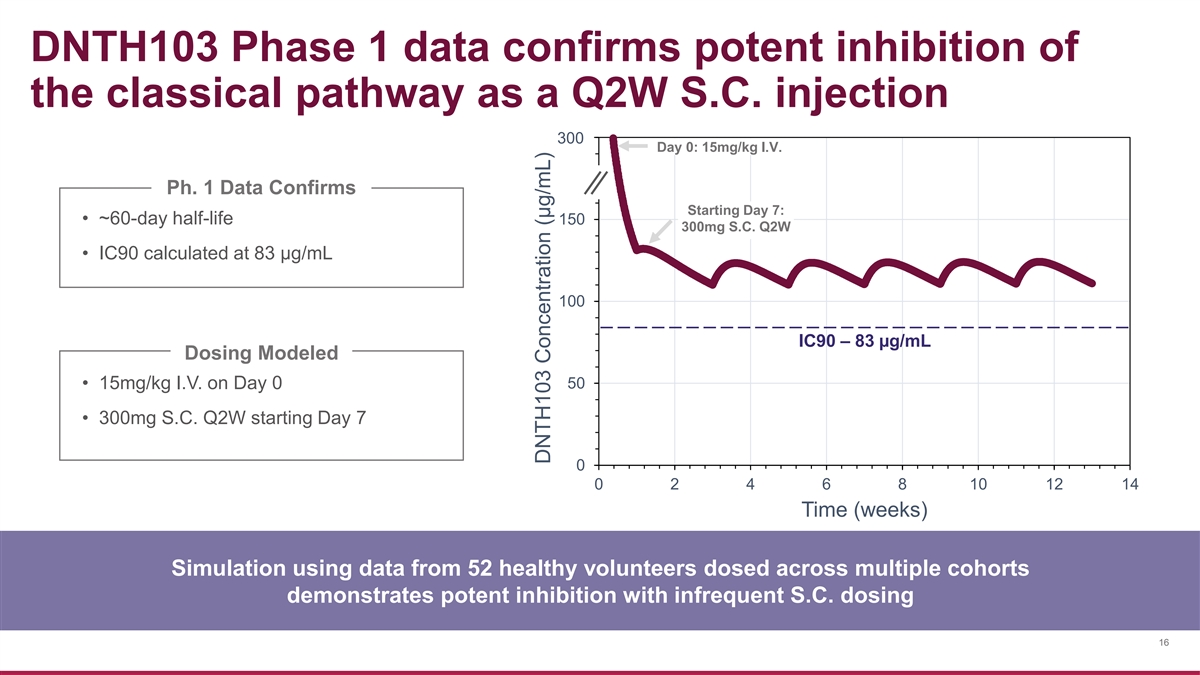

DNTH103 Phase 1 data confirms potent inhibition of the classical pathway

as a Q2W S.C. injection 200 300 Day 0: 15mg/kg I.V. Ph. 1 Data Confirms Starting Day 7: • ~60-day half-life 150 300mg S.C. Q2W • IC90 calculated at 83 µg/mL 100 IC90 – 83 µg/mL Dosing Modeled • 15mg/kg I.V. on Day 0

50 • 300mg S.C. Q2W starting Day 7 0 0 2 4 6 8 10 12 14 Time (weeks) Simulation using data from 52 healthy volunteers dosed across multiple cohorts demonstrates potent inhibition with infrequent S.C. dosing 16 DNTH103 Concentration

(µg/mL)

DNTH103 improves neurotransmission and muscle contraction in an AChR+ MG

model Ravulizumab* (1 μM) DNTH103 (0.1 μM) DNTH103 (1 μM) n=3 n=3 n=3 0 • Serum from MG patients used in a validated in vitro 1,2,3 MG model -10 -14.8% • Assessed improvement in neurotransmission and muscle contraction of

ravulizumab* and DNTH103, -20 as measured by decrease in muscle contraction fatigue -24.8% -27.8% • Results confirm DNTH03 improved -30 neurotransmission and muscle contraction AChR+ MG Patient Sera -40 Results provide further scientific

rationale for DNTH103 in gMG 17 1 https://pubmed.ncbi.nlm.nih.gov/34881241/, 2 - https://pubmed.ncbi.nlm.nih.gov/31846349/, 3 - https://pubmed.ncbi.nlm.nih.gov/30867827/ * Engineered using patent sequence Muscle Contraction Fatigue Index (% Change

to Baseline, Mean ± SEM)

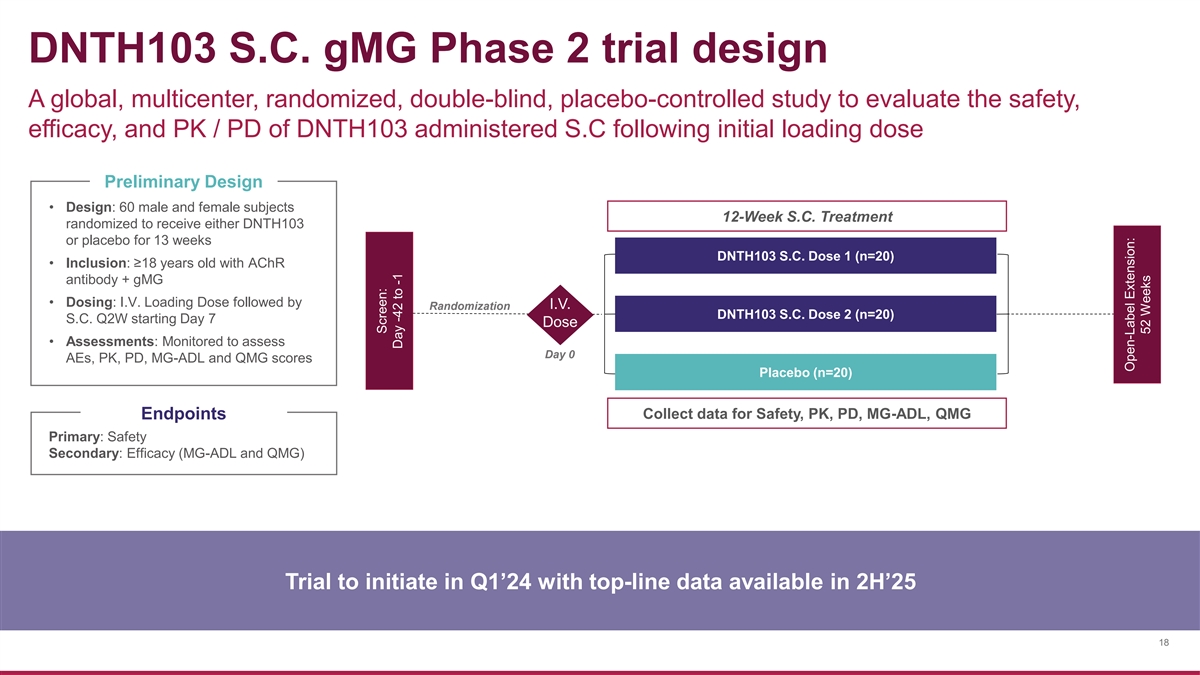

DNTH103 S.C. gMG Phase 2 trial design A global, multicenter, randomized,

double-blind, placebo-controlled study to evaluate the safety, efficacy, and PK / PD of DNTH103 administered S.C following initial loading dose Preliminary Design • Design: 60 male and female subjects 12-Week S.C. Treatment randomized to

receive either DNTH103 or placebo for 13 weeks DNTH103 S.C. Dose 1 (n=20) • Inclusion: ≥18 years old witAh ChR antibody + gMG • Dosing: I.V. Loading Dose followed by I.V. Randomization DNTH103 S.C. Dose 2 (n=20) S.C. Q2W starting

Day 7 Dose • Assessments: Monitored to assess Day 0 AEs, PK, PD, MG-ADL and QMG scores Placebo (n=20) Collect data for Safety, PK, PD, MG-ADL, QMG Endpoints Primary: Safety Secondary: Efficacy (MG-ADL and QMG) Trial to initiate in Q1’24

with top-line data available in 2H’25 18 Screen: Day -42 to -1 Open-Label Extension: 52 Weeks

MMN and CIDP offer clear biological and commercial rationale for next

DNTH103 indications Chronic Inflammatory Multifocal Motor Neuropathy (MMN) Demyelinating Polyneuropathy (CIDP) Neuromuscular indications with No approved targeted ~5,000 - 10,000 ~15,000 No approved targeted high unmet biologic therapies biologic

therapies patients in the U.S. patients in the U.S. medical need Evidence ~50% of patients have Complement deposition CIDP patient serum supports Classical MMN patient sera has anti-GM1 IgM activating has been observed activates complement

Complement role been confirmed to the classical complement and mimics CIDP features clinically on pertinent activate complement pathway nerves in pre-clinical models in Disease Phase 2 trials in MMN and CIDP planned for initiation in 1H’24 and

2H’24, respectively 19

Corporate

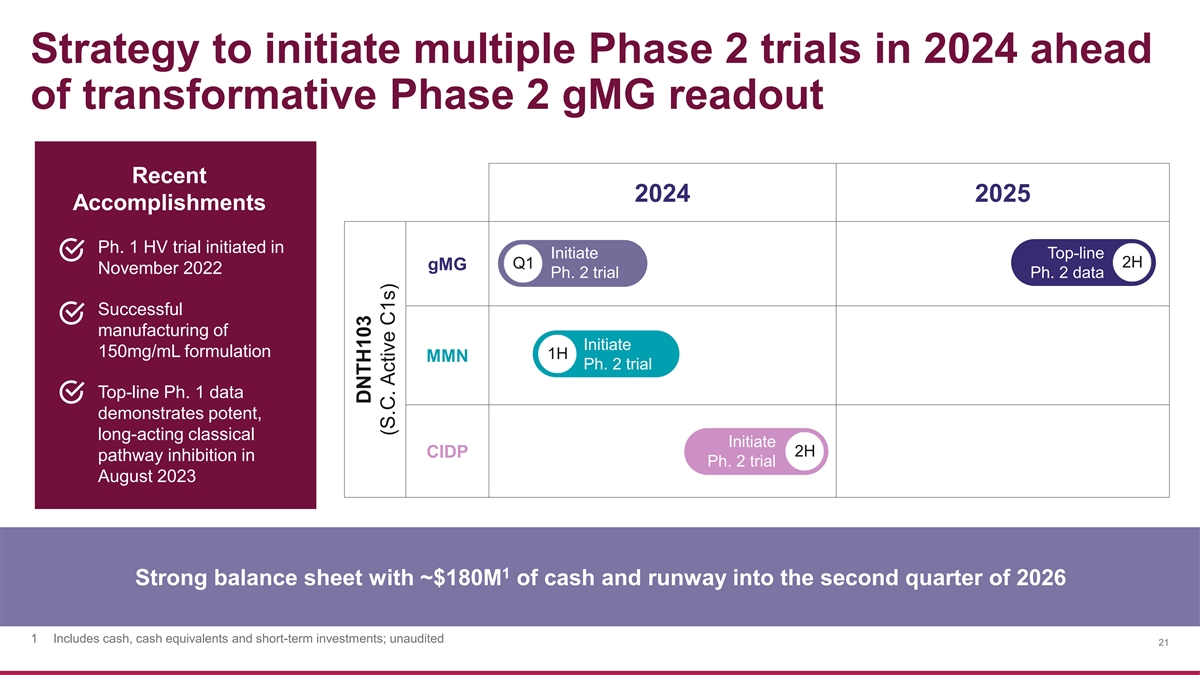

Strategy to initiate multiple Phase 2 trials in 2024 ahead of

transformative Phase 2 gMG readout Recent 2024 2025 Accomplishments Ph. 1 HV trial initiated in Initiate Top-line 2H Q1 gMG November 2022 Ph. 2 trial Ph. 2 data Successful manufacturing of Initiate 150mg/mL formulation 1H MMN Ph. 2 trial Top-line

Ph. 1 data demonstrates potent, long-acting classical Initiate 2H CIDP pathway inhibition in Ph. 2 trial August 2023 1 Strong balance sheet with ~$180M of cash and runway into the second quarter of 2026 1 Includes cash, cash equivalents and

short-term investments; unaudited 21 DNTH103 (S.C. Active C1s)

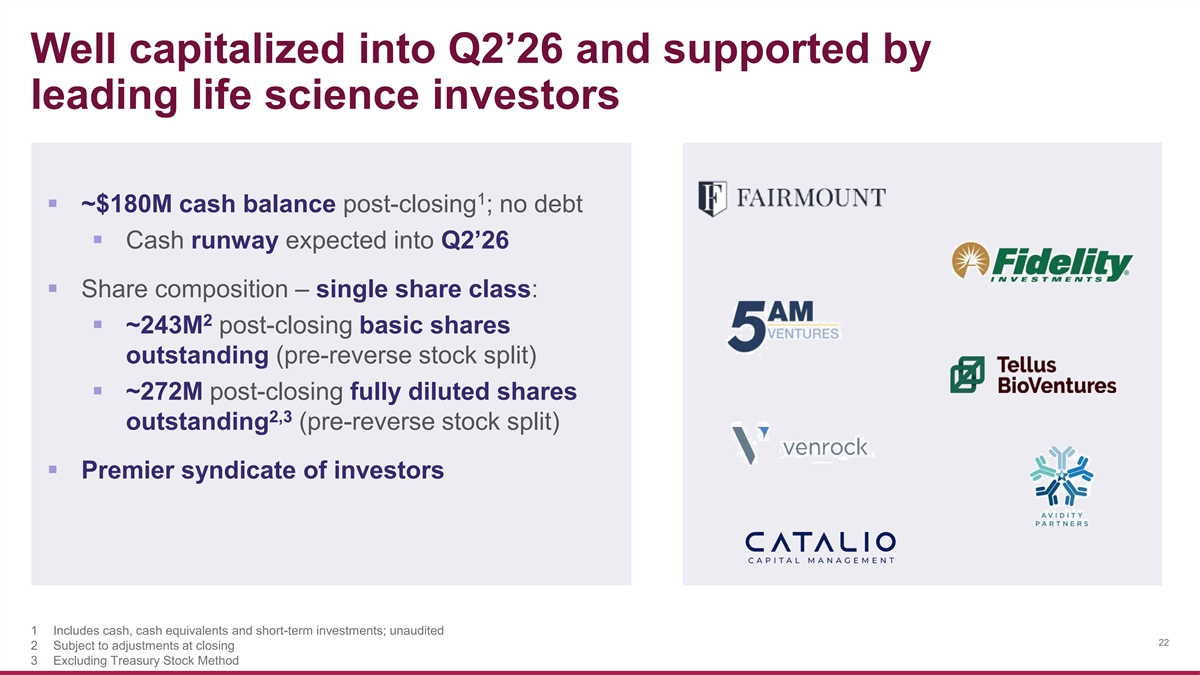

Well capitalized into Q2’26 and supported by leading life science

investors 1 ▪ ~$180M cash balance post-closing ; no debt ▪ Cash runway expected into Q2’26 ▪ Share composition – single share class: 2 ▪ ~243M post-closing basic shares outstanding (pre-reverse stock split)

▪ ~272M post-closing fully diluted shares 2,3 outstanding (pre-reverse stock split) ▪ Premier syndicate of investors 1 Includes cash, cash equivalents and short-term investments; unaudited 22 2 Subject to adjustments at closing 3

Excluding Treasury Stock Method

Magenta Therapeutics (NASDAQ:MGTA)

Graphique Historique de l'Action

De Avr 2024 à Mai 2024

Magenta Therapeutics (NASDAQ:MGTA)

Graphique Historique de l'Action

De Mai 2023 à Mai 2024