Form 8-K - Current report

14 Février 2024 - 11:23PM

Edgar (US Regulatory)

false

0001324404

0001324404

2024-02-14

2024-02-14

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

UNITED STATES

SECURITIES AND

EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section

13 OR 15(d) of The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported):

February 14, 2024

CF

Industries Holdings, Inc.

(Exact name of registrant as specified in its

charter)

| Delaware |

|

001-32597 |

|

20-2697511 |

(State

or other jurisdiction

of incorporation) |

|

(Commission

File Number) |

|

(IRS

Employer

Identification No.) |

2375

Waterview Drive

Northbrook,

Illinois |

|

|

|

60062 |

(Address

of principal

executive offices) |

|

|

|

(Zip

Code) |

Registrant’s telephone number, including

area code (847) 405-2400

(Former name or former address,

if changed since last report.)

Check the appropriate box below if the Form 8-K

filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General

Instruction A.2. below):

| ¨ | Written

communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting

material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement

communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement

communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

|

Trading symbol(s) |

|

Name of each exchange on which registered |

| common

stock, par value $0.01 per share |

|

CF |

|

New

York Stock Exchange |

Indicate by check mark whether the registrant is

an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2

of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging

growth company ¨

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

| Item 2.02. | Results

of Operations and Financial Condition. |

On February 15, 2024, CF Industries Holdings, Inc. will

host a conference call discussing its results for the quarter and year ended December 31, 2023, at which the presentation attached

hereto as Exhibit 99.1 will be used.

The information set forth herein, including the exhibit attached hereto,

shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, nor shall

it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, except as shall be expressly set forth

by specific reference in any such filing.

| Item 9.01. | Financial

Statements and Exhibits. |

(d) Exhibits.

SIGNATURES

Pursuant to the requirements of the Securities

Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Date: |

February 14,

2024 |

CF

INDUSTRIES HOLDINGS, INC. |

| |

|

|

|

| |

|

|

|

| |

|

By: |

/s/ Christopher

D. Bohn |

| |

|

Name: |

Christopher

D. Bohn |

| |

|

Title: |

Executive

Vice President and Chief Operating Officer |

Exhibit 99.1

| 2023 Fourth Quarter

and Full Year

Financial Results

February 14, 2024

NYSE: CF |

| Safe harbor statement

All statements in this presentation by CF Industries Holdings, Inc. (together with its subsidiaries, the “Company”), other than those relating to historical facts, are

forward-looking statements. Forward-looking statements can generally be identified by their use of terms such as “anticipate,” “believe,” “could,” “estimate,”

“expect,” “intend,” “may,” “plan,” “predict,” “project,” “will” or “would” and similar terms and phrases, including references to assumptions. Forward-looking

statements are not guarantees of future performance and are subject to a number of assumptions, risks and uncertainties, many of which are beyond the

Company’s control, which could cause actual results to differ materially from such statements. These statements may include, but are not limited to, statements

about the synergies and other benefits, and other aspects of the transactions with Incitec Pivot Limited (“IPL”), strategic plans and management’s expectations

with respect to the production of green and blue (low-carbon) ammonia, the development of carbon capture and sequestration projects, the transition to and

growth of a hydrogen economy, greenhouse gas reduction targets, projected capital expenditures, statements about future financial and operating results, and

other items described in this presentation. Important factors that could cause actual results to differ materially from those in the forward-looking statements

include, among others, the risk of obstacles to realization of the benefits of the transactions with IPL; the risk that the synergies from the transactions with IPL may

not be fully realized or may take longer to realize than expected; the risk that the completion of the transactions with IPL, including integration of the Waggaman

ammonia production complex into the Company’s operations, disrupt current operations or harm relationships with customers, employees and suppliers; the risk

that integration of the Waggaman ammonia production complex with the Company’s current operations will be more costly or difficult than expected or may

otherwise be unsuccessful; diversion of management time and attention to issues relating to the transactions with IPL; unanticipated costs or liabilities associated

with the IPL transactions; the cyclical nature of the Company’s business and the impact of global supply and demand on the Company’s selling prices; the global

commodity nature of the Company’s nitrogen products, the conditions in the international market for nitrogen products, and the intense global competition from

other producers; conditions in the United States, Europe and other agricultural areas, including the influence of governmental policies and technological

developments on the demand for our fertilizer products; the volatility of natural gas prices in North America and the United Kingdom; weather conditions and the

impact of adverse weather events; the seasonality of the fertilizer business; the impact of changing market conditions on the Company’s forward sales programs;

difficulties in securing the supply and delivery of raw materials, increases in their costs or delays or interruptions in their delivery; reliance on third party providers

of transportation services and equipment; the Company’s reliance on a limited number of key facilities; risks associated with cybersecurity; acts of terrorism and

regulations to combat terrorism; risks associated with international operations; the significant risks and hazards involved in producing and handling the Company’s

products against which the Company may not be fully insured; the Company’s ability to manage its indebtedness and any additional indebtedness that may be

incurred; the Company’s ability to maintain compliance with covenants under its revolving credit agreement and the agreements governing its indebtedness;

downgrades of the Company’s credit ratings; risks associated with changes in tax laws and disagreements with taxing authorities; risks involving derivatives and

the effectiveness of the Company’s risk management and hedging activities; potential liabilities and expenditures related to environmental, health and safety laws

and regulations and permitting requirements; regulatory restrictions and requirements related to greenhouse gas emissions; the development and growth of the

market for green and blue (low-carbon) ammonia and the risks and uncertainties relating to the development and implementation of the Company’s green and blue

(low-carbon) ammonia projects; risks associated with expansions of the Company’s business, including unanticipated adverse consequences and the significant

resources that could be required; and risks associated with the operation or management of the strategic venture with CHS (the “CHS Strategic Venture”), risks

and uncertainties relating to the market prices of the fertilizer products that are the subject of the supply agreement with CHS over the life of the supply agreement,

and the risk that any challenges related to the CHS Strategic Venture will harm the Company’s other business relationships. More detailed information about

factors that may affect the Company’s performance and could cause actual results to differ materially from those in any forward-looking statements may be found

in CF Industries Holdings, Inc.’s filings with the Securities and Exchange Commission, including CF Industries Holdings, Inc.’s most recent annual and quarterly

reports on Form 10-K and Form 10-Q, which are available in the Investor Relations section of the Company’s web site. It is not possible to predict or identify all

risks and uncertainties that might affect the accuracy of our forward-looking statements and, consequently, our descriptions of such risks and uncertainties should

not be considered exhaustive. There is no guarantee that any of the events, plans or goals anticipated by these forward-looking statements will occur, and if any of

the events do occur, there is no guarantee what effect they will have on our business, results of operations, cash flows, financial condition and future prospects.

Forward-looking statements are given only as of the date of this presentation and the Company disclaims any obligation to update or revise the forward-looking

statements, whether as a result of new information, future events or otherwise, except as required by law. |

| Note regarding non-GAAP financial measures

The Company reports its financial results in accordance with U.S. generally accepted accounting principles (GAAP). Management

believes that EBITDA, adjusted EBITDA, free cash flow, free cash flow to adjusted EBITDA conversion and free cash flow yield,

which are non-GAAP financial measures, provide additional meaningful information regarding the Company's performance and

financial strength. Non-GAAP financial measures should be viewed in addition to, and not as an alternative for, the Company's

reported results prepared in accordance with GAAP. In addition, because not all companies use identical calculations, EBITDA,

adjusted EBITDA, free cash flow, free cash flow to adjusted EBITDA conversion and free cash flow yield included in this presentation

may not be comparable to similarly titled measures of other companies. Reconciliations of EBITDA, adjusted EBITDA, free cash flow,

and free cash flow yield to the most directly comparable GAAP measures are provided in the tables accompanying this presentation.

EBITDA is defined as net earnings attributable to common stockholders plus interest expense - net, income taxes, and depreciation

and amortization. Other adjustments include the elimination of loan fee amortization that is included in both interest and amortization,

and the portion of depreciation that is included in noncontrolling interest. The Company has presented EBITDA because

management uses the measure to track performance and believes that it is frequently used by securities analysts, investors and

other interested parties in the evaluation of companies in the industry.

Adjusted EBITDA is defined as EBITDA adjusted with the selected items as summarized in the tables accompanying this

presentation. The Company has presented adjusted EBITDA because management uses adjusted EBITDA, and believes it is useful

to investors, as a supplemental financial measure in the comparison of year-over-year performance.

Free cash flow is defined as net cash provided by operating activities, as stated in the consolidated statements of cash flows,

reduced by capital expenditures and distributions to noncontrolling interests. Free cash flow to adjusted EBITDA conversion is

defined as free cash flow divided by adjusted EBITDA. Free cash flow yield is defined as free cash flow divided by market value of

equity (market cap). For full year 2022, the Company has also presented cash provided by operating activities, free cash flow, free

cash flow to adjusted EBITDA conversion and free cash flow yield, in each case excluding certain tax and interest payments made to

Canadian tax authorities in relation to an arbitration decision covering tax years 2006 through 2011 and to our transfer pricing

positions between Canada and the United States for open years 2012 and after. The Company has presented these financial

measures, as well as the financial measures free cash flow, free cash flow to adjusted EBITDA conversion and free cash flow yield,

because management uses these measures and believes they are useful to investors, as an indication of the strength of the

Company and its ability to generate cash and to evaluate the Company’s cash generation ability relative to its industry competitors. It

should not be inferred that the entire free cash flow amount is available for discretionary expenditures. |

| 4

Strong global demand and favorable energy spreads

underpin solid results

(1) See appendix for reconciliations of EBITDA and adjusted EBITDA to the most directly comparable GAAP measures

(2) Free cash flow represents cash provided by operating activities (cash from operations) less capital expenditures less distributions to noncontrolling interest; see

appendix for reconciliation of free cash flow

EBITDA(1)

Net earnings Net earnings per

diluted share

Adjusted EBITDA(1)

$2.76 B

FY 2023

$5.88 B

FY 2022

$7.87

FY 2023

$16.38

FY 2022

2023 Cash from

operations(2)

2023 Free cash flow(2)

Strong cash generation enabled significant return of

capital since the beginning of 2021:

- Invested $1.4 billion in growth projects

- Deployed $2.5 billion to repurchase 31.3 million

shares, ~15% of the shares outstanding

- $2.6 billion remaining in $3 billion share

repurchase authorization

- Returned approximately $900 million to

shareholders through dividends

- Latest dividend 67% higher

Acquisition of Waggaman ammonia facility complete

Advanced our clean energy initiatives

- Progressed low-carbon and green ammonia

projects

• Initial FEED study with Mitsui completed; FID

targeted 2H 2024

• Autothermal reforming (ATR) and flue gas FEED

studies in progress to evaluate optimal carbon

reduction alternatives

• Donaldsonville green ammonia project:

electrolyzer installed, mechanically complete and

commissioning activities underway

- Entered into agreement with bp to purchase

4.4 billion cubic feet of certified natural gas, double

the amount purchased in 2023

$2.76 B

$2.71 B

FY 2023

$5.54 B

FY 2022

$1.53 B

FY 2023

$3.35 B

FY 2022

$1.80 B |

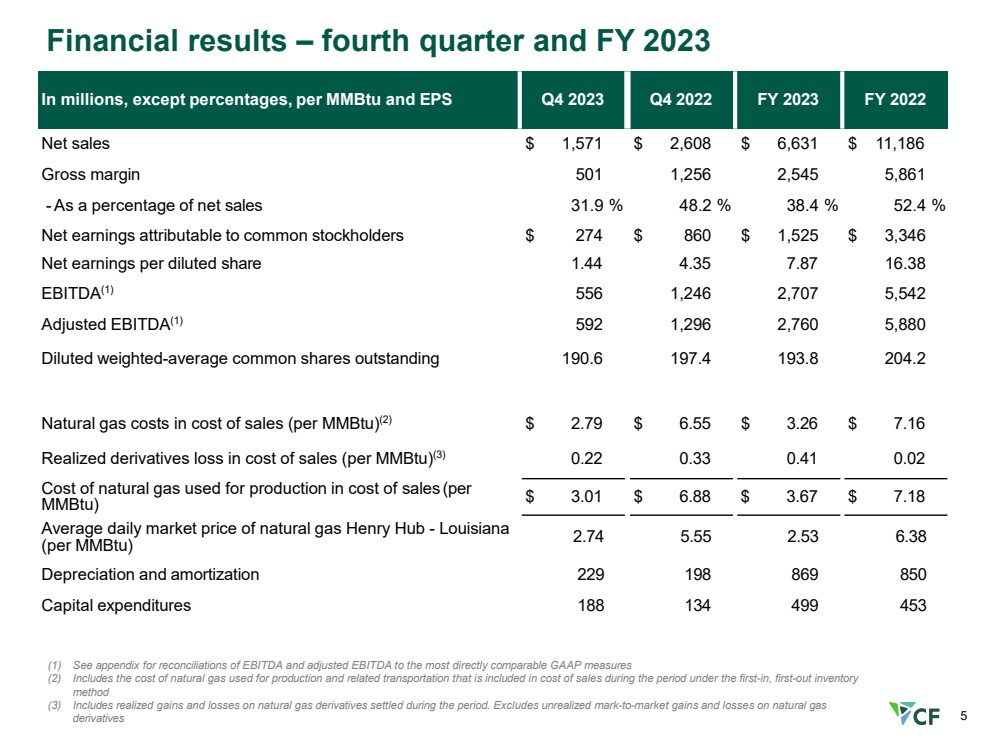

| 5

Financial results – fourth quarter and FY 2023

In millions, except percentages, per MMBtu and EPS Q4 2023 Q4 2022 FY 2023 FY 2022

Net sales $ 1,571 $ 2,608 $ 6,631 $ 11,186

Gross margin 501 1,256 2,545 5,861

-As a percentage of net sales 31.9 % 48.2 % 38.4 % 52.4 %

Net earnings attributable to common stockholders $ 274 $ 860 $ 1,525 $ 3,346

Net earnings per diluted share 1.44 4.35 7.87 16.38

EBITDA(1) 556 1,246 2,707 5,542

Adjusted EBITDA(1) 592 1,296 2,760 5,880

Diluted weighted-average common shares outstanding 190.6 197.4 193.8 204.2

Natural gas costs in cost of sales (per MMBtu)(2) $ 2.79 $ 6.55 $ 3.26 $ 7.16

Realized derivatives loss in cost of sales (per MMBtu)(3) 0.22 0.33 0.41 0.02

Cost of natural gas used for production in cost of sales (per

MMBtu) $ 3.01 $ 6.88 $ 3.67 $ 7.18

Average daily market price of natural gas Henry Hub - Louisiana

(per MMBtu) 2.74 5.55 2.53 6.38

Depreciation and amortization 229 198 869 850

Capital expenditures 188 134 499 453

(1) See appendix for reconciliations of EBITDA and adjusted EBITDA to the most directly comparable GAAP measures

(2) Includes the cost of natural gas used for production and related transportation that is included in cost of sales during the period under the first-in, first-out inventory

method

(3) Includes realized gains and losses on natural gas derivatives settled during the period. Excludes unrealized mark-to-market gains and losses on natural gas

derivatives |

| 6

(1) Source of data: December 19, 2023 CRU Ammonia Database

(2) Represents CF Industries’ historical North American production and CRU’s capacity estimates for CF Industries

(3) Calculated by removing CF Industries’ annual reported production and capacity from the CRU data for all North American ammonia production peer group, Waggaman production/capacity

included for one month only

(4) ~0.9 million tons represents the difference between CF Industries’ actual trailing 5-year average ammonia production of 9.3 million tons at 97% of capacity utilization and the 8.4 million tons CF

Industries would have produced if operated at the 87% CRU North American benchmark excluding CF Industries

Note: CRU North American peer group includes AdvanSix, Austin Powder (US Nitrogen), Carbonair, CF Industries, Chevron, CVR Partners, Dakota Gasification Co, Dyno Nobel, Fortigen, Incitec

Pivot (11 months production/capacity), Koch Industries, LSB Industries, LSB Industries/Cherokee Nitrogen, Mississippi Power, Mosaic, Nutrien, OCI N.V., RenTech Nitrogen, Sherritt International

Corp, Shoreline Chemical, Simplot, Yara International

North American Ammonia Percent of

Capacity Utilization (1)

5-Year Rolling Avg. Percent of Capacity

CF’s 10% greater capacity utilization yields an additional

~0.9 million tons of ammonia annually(4)

Outstanding safety performance drives industry leading

production capacity utilization

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2011 2014 2017 2020 2023

Total injuries per 200,000 work hours

Total Recordable Incident Rate

BLS Fertilizer

Manufacturing

CF

Industries

As of December 31, 2023, the 12-month rolling average

recordable incident rate was 0.36 per 200,000 work hours

CF North

America (2)

North

America

Excl. CF (3)

96% 96%

97%

84%

86%

87%

80%

82%

84%

86%

88%

90%

92%

94%

96%

98%

100%

5 years ending 2021 5 years ending 2022 5 years ending 2023 |

| 7

Consistently strong free cash flow metrics show undervalued

equity

Attractive free cash flow yield and free cash flow to adjusted EBITDA conversion rate suggest

undervalued equity, supporting robust share repurchase program

9.7% 8.9% 9.0%

14.7%

16.7%

12.0%

2018 2019 2020 2021 2022 2023

2018-2023 average yield

Free Cash Flow Yield(1)

FCF/Adj EBITDA

conversion(2) %

67% 57% 55% 79% 47% 65%

56%(3)

19.6%(3)

(1) Represents annual free cash flow divided by market value of equity (market cap) as of December 31st of each year; see appendix for reconciliation of free cash flow to

the most directly comparable GAAP measure and calculation of market cap

(2) Represents annual free cash flow divided by annual adjusted EBITDA; see appendix for reconciliations of free cash flow and adjusted EBITDA to the most directly

comparable GAAP measures

(3) Excluding the impact of $491M of tax and interest payments related to a dispute between Canadian and U.S. tax authorities dating back to the early 2000s; the

Company has filed amended tax returns in the U.S. seeking refunds of related taxes paid

Canada/US

tax matter (3) |

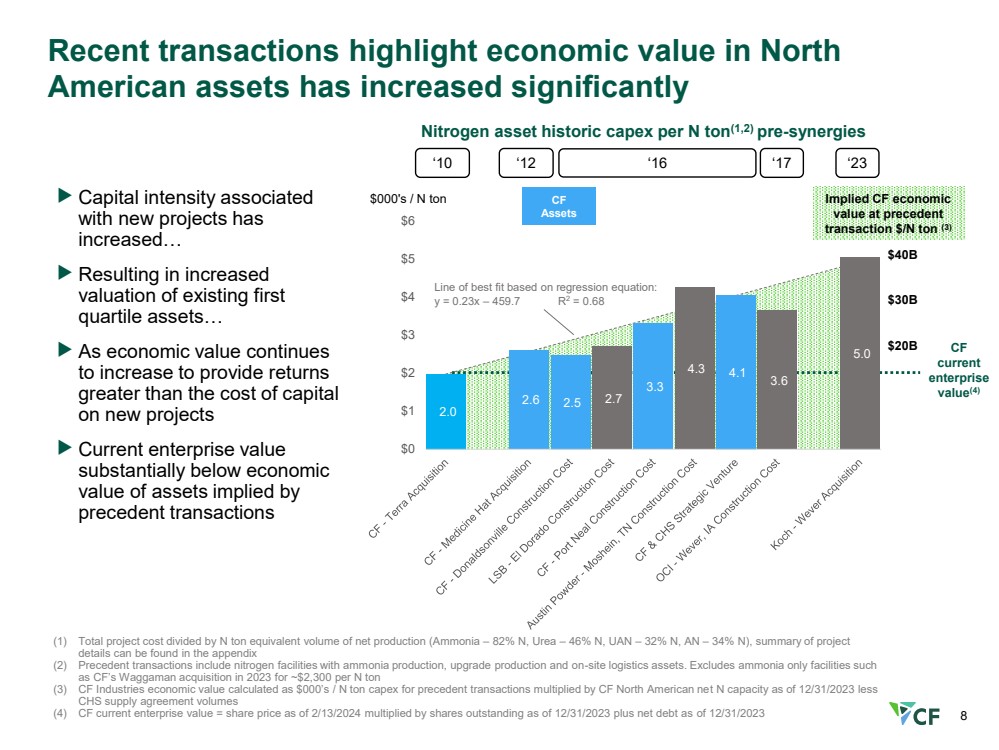

| 8

Recent transactions highlight economic value in North

American assets has increased significantly

Nitrogen asset historic capex per N ton(1,2) pre-synergies

$000's / N ton

‘10 ‘16 ‘17 ‘23

Capital intensity associated

with new projects has

increased…

Resulting in increased

valuation of existing first

quartile assets…

As economic value continues

to increase to provide returns

greater than the cost of capital

on new projects

Current enterprise value

substantially below economic

value of assets implied by

precedent transactions

$40B

$20B

(1) Total project cost divided by N ton equivalent volume of net production (Ammonia – 82% N, Urea – 46% N, UAN – 32% N, AN – 34% N), summary of project

details can be found in the appendix

(2) Precedent transactions include nitrogen facilities with ammonia production, upgrade production and on-site logistics assets. Excludes ammonia only facilities such

as CF’s Waggaman acquisition in 2023 for ~$2,300 per N ton

(3) CF Industries economic value calculated as $000’s / N ton capex for precedent transactions multiplied by CF North American net N capacity as of 12/31/2023 less

CHS supply agreement volumes

(4) CF current enterprise value = share price as of 2/13/2024 multiplied by shares outstanding as of 12/31/2023 plus net debt as of 12/31/2023

$30B

CF

current

enterprise

value(4)

‘12

Line of best fit based on regression equation:

y = 0.23x – 459.7 R2 = 0.68

Implied CF economic

value at precedent

transaction $/N ton (3)

CF

Assets

2.0

2.6 2.5 2.7

3.3

4.3 4.1 3.6

5.0

$0

$1

$2

$3

$4

$5

$6 |

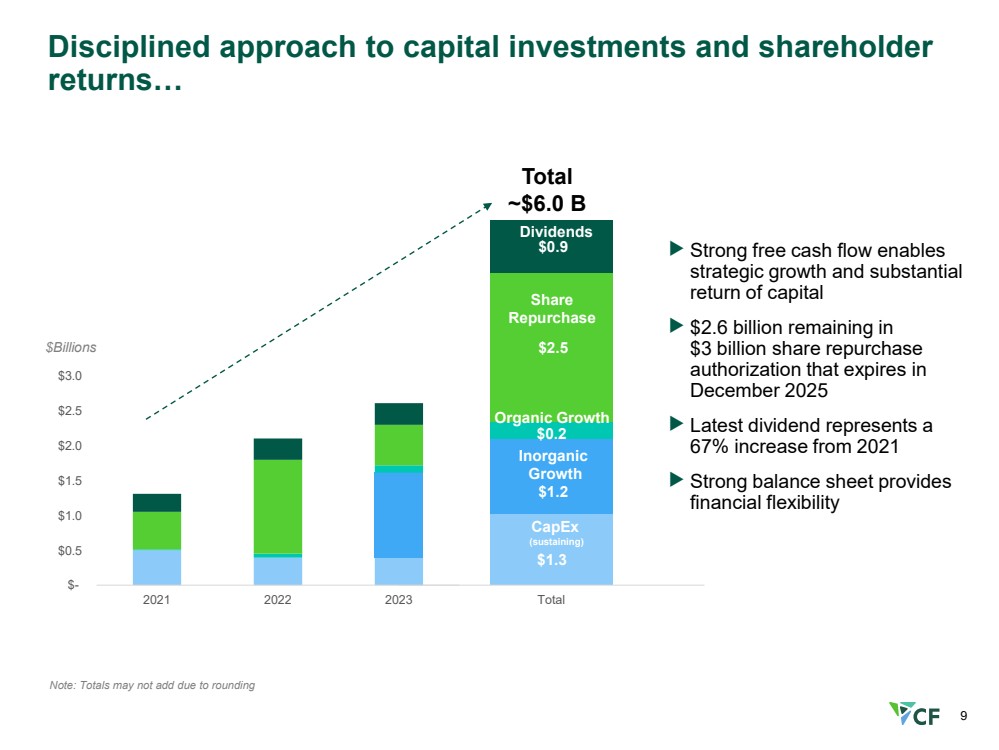

| 9

$1.2

$2.5

$0.9

Total

Disciplined approach to capital investments and shareholder

returns…

$Billions

Share

Repurchase

Dividends

Inorganic

Growth

Total

~$6.0 B

CapEx

(sustaining)

Strong free cash flow enables

strategic growth and substantial

return of capital

$2.6 billion remaining in

$3 billion share repurchase

authorization that expires in

December 2025

Latest dividend represents a

67% increase from 2021

Strong balance sheet provides

financial flexibility

Note: Totals may not add due to rounding

Organic Growth

$0.2

$1.3

$-

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

2021 2022 2023 |

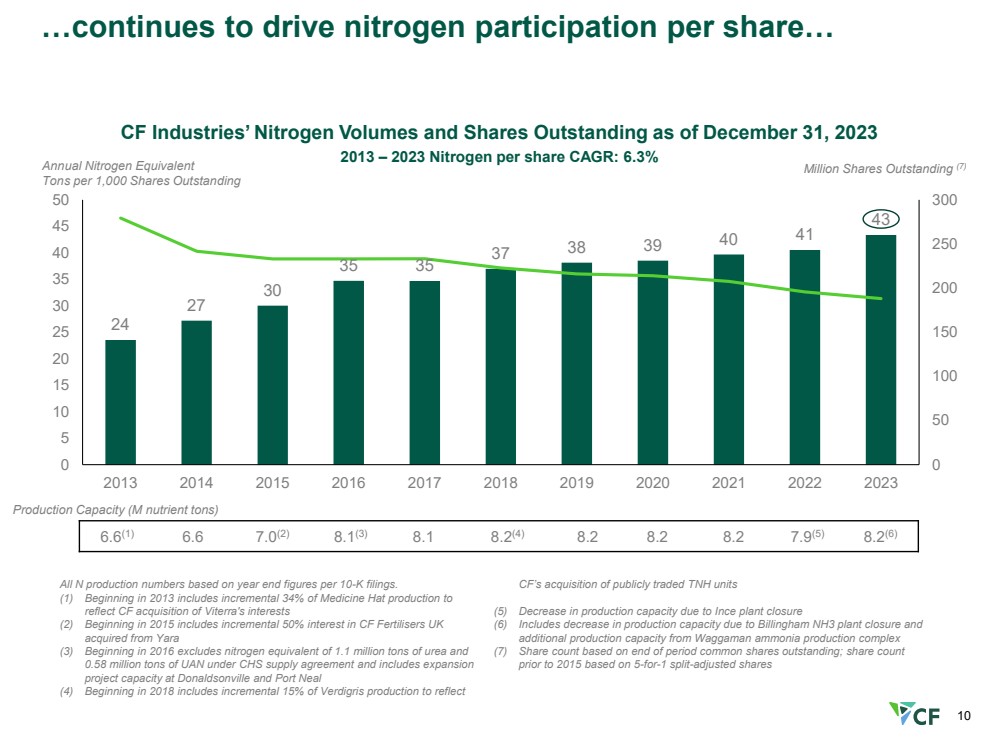

| 10

6.6(1) 6.6 7.0(2) 8.1(3) 8.1 8.2(4) 8.2 8.2 8.2 7.9(5) 8.2(6)

All N production numbers based on year end figures per 10-K filings.

(1) Beginning in 2013 includes incremental 34% of Medicine Hat production to

reflect CF acquisition of Viterra's interests

(2) Beginning in 2015 includes incremental 50% interest in CF Fertilisers UK

acquired from Yara

(3) Beginning in 2016 excludes nitrogen equivalent of 1.1 million tons of urea and

0.58 million tons of UAN under CHS supply agreement and includes expansion

project capacity at Donaldsonville and Port Neal

(4) Beginning in 2018 includes incremental 15% of Verdigris production to reflect

CF’s acquisition of publicly traded TNH units

(5) Decrease in production capacity due to Ince plant closure

(6) Includes decrease in production capacity due to Billingham NH3 plant closure and

additional production capacity from Waggaman ammonia production complex

(7) Share count based on end of period common shares outstanding; share count

prior to 2015 based on 5-for-1 split-adjusted shares

Production Capacity (M nutrient tons)

Annual Nitrogen Equivalent

Tons per 1,000 Shares Outstanding

CF Industries’ Nitrogen Volumes and Shares Outstanding as of December 31, 2023

Million Shares Outstanding (7)

2013 – 2023 Nitrogen per share CAGR: 6.3%

24

27

30

35 35

37 38 39 40 41

43

0

50

100

150

200

250

300

0

5

10

15

20

25

30

35

40

45

50

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

…continues to drive nitrogen participation per share… |

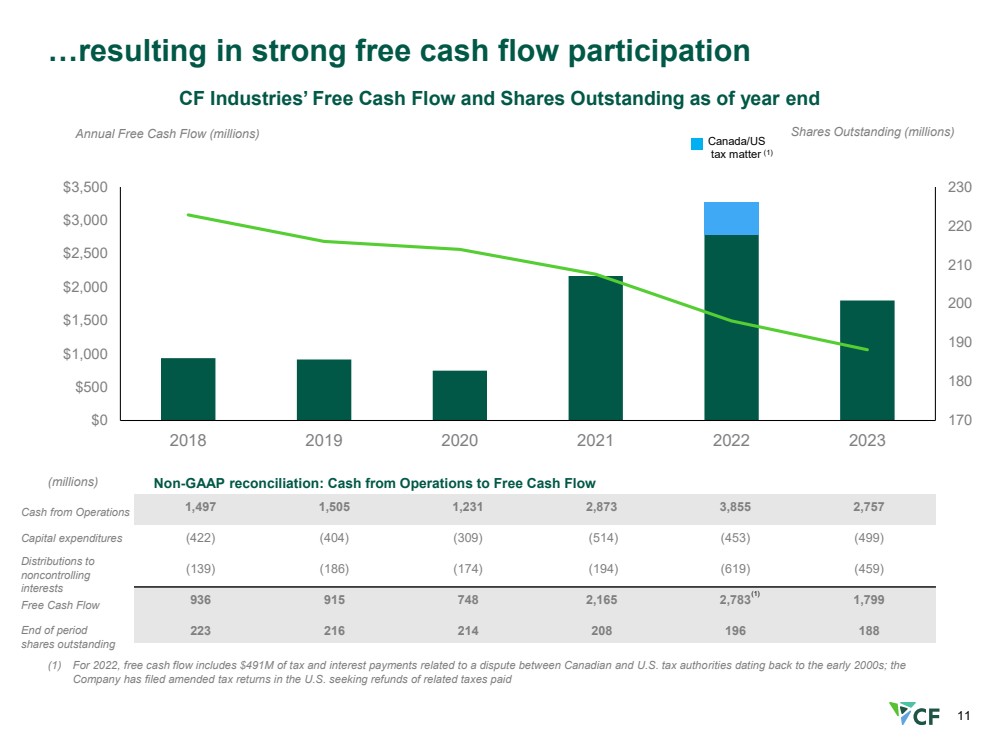

| 11

1,497 1,505 1,231 2,873 3,855 2,757

(422) (404) (309) (514) (453) (499)

(139) (186) (174) (194) (619) (459)

936 915 748 2,165 2,783 1,799

223 216 214 208 196 188

Annual Free Cash Flow (millions)

CF Industries’ Free Cash Flow and Shares Outstanding as of year end

Shares Outstanding (millions)

170

180

190

200

210

220

230

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2018 2019 2020 2021 2022 2023

…resulting in strong free cash flow participation

End of period

shares outstanding

Cash from Operations

Capital expenditures

Distributions to

noncontrolling

interests

Free Cash Flow

(millions) Non-GAAP reconciliation: Cash from Operations to Free Cash Flow

(1)

(1) For 2022, free cash flow includes $491M of tax and interest payments related to a dispute between Canadian and U.S. tax authorities dating back to the early 2000s; the

Company has filed amended tax returns in the U.S. seeking refunds of related taxes paid

Canada/US

tax matter (1) |

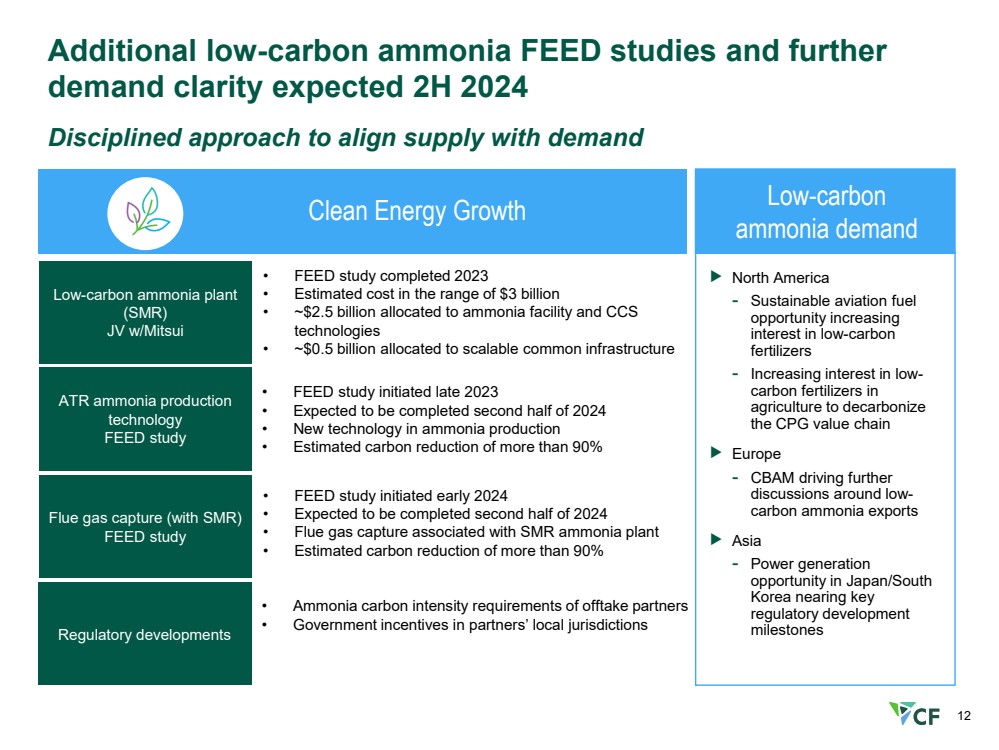

| 12

Additional low-carbon ammonia FEED studies and further

demand clarity expected 2H 2024

Disciplined approach to align supply with demand

Clean Energy Growth

Low-carbon ammonia plant

(SMR)

JV w/Mitsui

ATR ammonia production

technology

FEED study

Flue gas capture (with SMR)

FEED study

• FEED study completed 2023

• Estimated cost in the range of $3 billion

• ~$2.5 billion allocated to ammonia facility and CCS

technologies

• ~$0.5 billion allocated to scalable common infrastructure

• FEED study initiated late 2023

• Expected to be completed second half of 2024

• New technology in ammonia production

• Estimated carbon reduction of more than 90%

• FEED study initiated early 2024

• Expected to be completed second half of 2024

• Flue gas capture associated with SMR ammonia plant

• Estimated carbon reduction of more than 90%

Low-carbon

ammonia demand

Regulatory developments

• Ammonia carbon intensity requirements of offtake partners

• Government incentives in partners’ local jurisdictions

North America

- Sustainable aviation fuel

opportunity increasing

interest in low-carbon

fertilizers

- Increasing interest in low-carbon fertilizers in

agriculture to decarbonize

the CPG value chain

Europe

- CBAM driving further

discussions around low-carbon ammonia exports

Asia

- Power generation

opportunity in Japan/South

Korea nearing key

regulatory development

milestones |

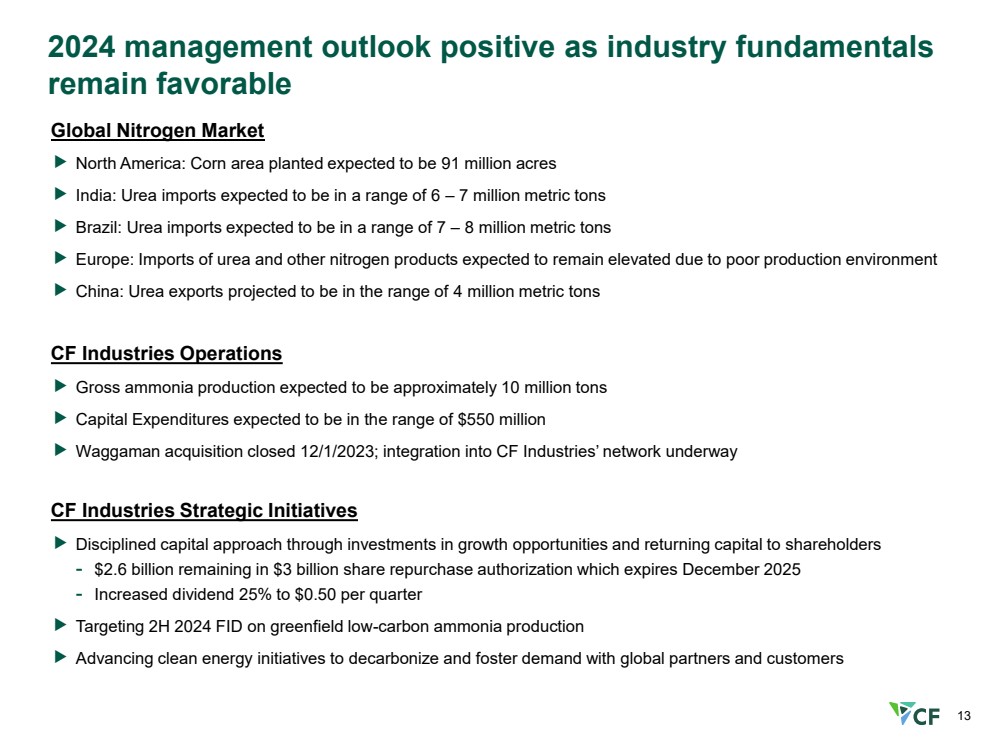

| 13

2024 management outlook positive as industry fundamentals

remain favorable

Global Nitrogen Market

North America: Corn area planted expected to be 91 million acres

India: Urea imports expected to be in a range of 6 – 7 million metric tons

Brazil: Urea imports expected to be in a range of 7 – 8 million metric tons

Europe: Imports of urea and other nitrogen products expected to remain elevated due to poor production environment

China: Urea exports projected to be in the range of 4 million metric tons

CF Industries Operations

Gross ammonia production expected to be approximately 10 million tons

Capital Expenditures expected to be in the range of $550 million

Waggaman acquisition closed 12/1/2023; integration into CF Industries’ network underway

CF Industries Strategic Initiatives

Disciplined capital approach through investments in growth opportunities and returning capital to shareholders

- $2.6 billion remaining in $3 billion share repurchase authorization which expires December 2025

- Increased dividend 25% to $0.50 per quarter

Targeting 2H 2024 FID on greenfield low-carbon ammonia production

Advancing clean energy initiatives to decarbonize and foster demand with global partners and customers |

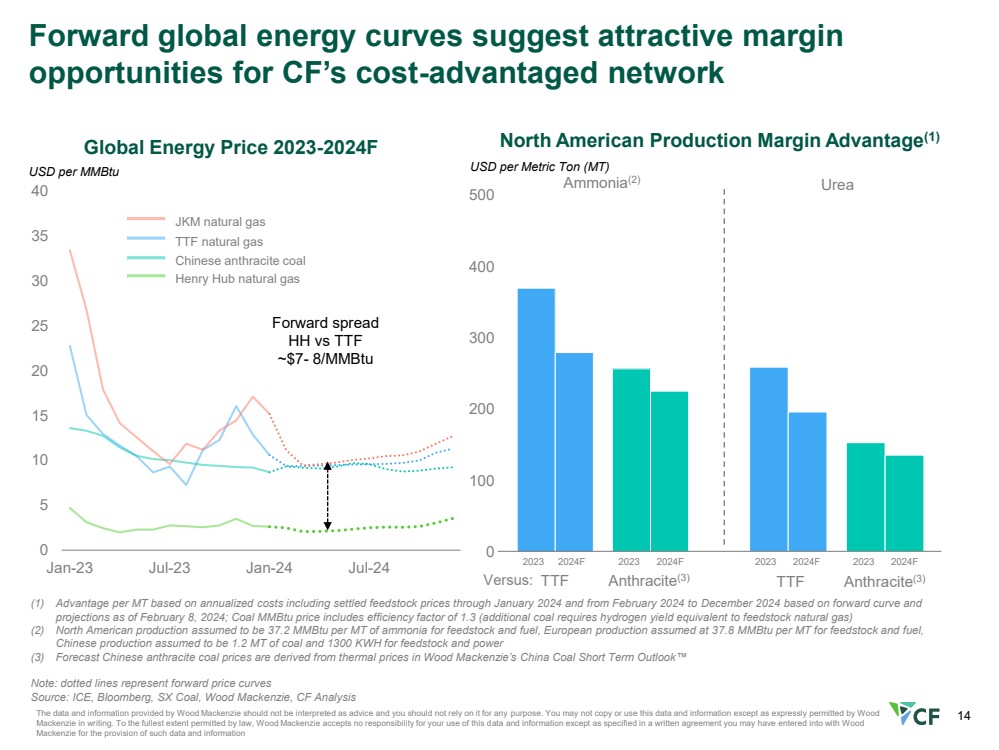

| 14

0

5

10

15

20

25

30

35

40

Jan-23 Jul-23 Jan-24 Jul-24

The data and information provided by Wood Mackenzie should not be interpreted as advice and you should not rely on it for any purpose. You may not copy or use this data and information except as expressly permitted by Wood

Mackenzie in writing. To the fullest extent permitted by law, Wood Mackenzie accepts no responsibility for your use of this data and information except as specified in a written agreement you may have entered into with Wood

Mackenzie for the provision of such data and information

Global Energy Price 2023-2024F

Henry Hub natural gas

TTF natural gas

Chinese anthracite coal

JKM natural gas

USD per MMBtu

0

100

200

300

400

500

USD per Metric Ton (MT)

North American Production Margin Advantage(1)

Ammonia(2) Urea

TTF Anthracite(3)

2023 2024F

Versus: TTF Anthracite(3)

(1) Advantage per MT based on annualized costs including settled feedstock prices through January 2024 and from February 2024 to December 2024 based on forward curve and

projections as of February 8, 2024; Coal MMBtu price includes efficiency factor of 1.3 (additional coal requires hydrogen yield equivalent to feedstock natural gas)

(2) North American production assumed to be 37.2 MMBtu per MT of ammonia for feedstock and fuel, European production assumed at 37.8 MMBtu per MT for feedstock and fuel,

Chinese production assumed to be 1.2 MT of coal and 1300 KWH for feedstock and power

(3) Forecast Chinese anthracite coal prices are derived from thermal prices in Wood Mackenzie’s China Coal Short Term Outlook™

Note: dotted lines represent forward price curves

Source: ICE, Bloomberg, SX Coal, Wood Mackenzie, CF Analysis

2023 2024F 2023 2024F 2023 2024F

Forward global energy curves suggest attractive margin

opportunities for CF’s cost-advantaged network

Forward spread

HH vs TTF

~$7- 8/MMBtu |

| 15

2024 global delivered U.S. Gulf urea cost curve suggests

prices near historic averages

2024 Monthly Delivered U.S. Gulf Urea Cost Curve

2024 Shipments:

17.5M Tons Avg.

Appx. Monthly

Range

Energy (N.G.)

Other Cash

Freight

Estimated 2024 Cost Range: $320-$375

5 10 15 20

Energy

(Coal)

5

Y-axis: USD/st

X-axis: Monthly Production Capacity at 95% Operating Rate, 85% Operating Rate in China, million short tons

Illustrative of seasonal highs

Illustrative of seasonal lows

Source: Industry Publications, CF Analysis

Energy (N.G.)

Other Cash

Freight

Energy

(Coal) |

| Appendix |

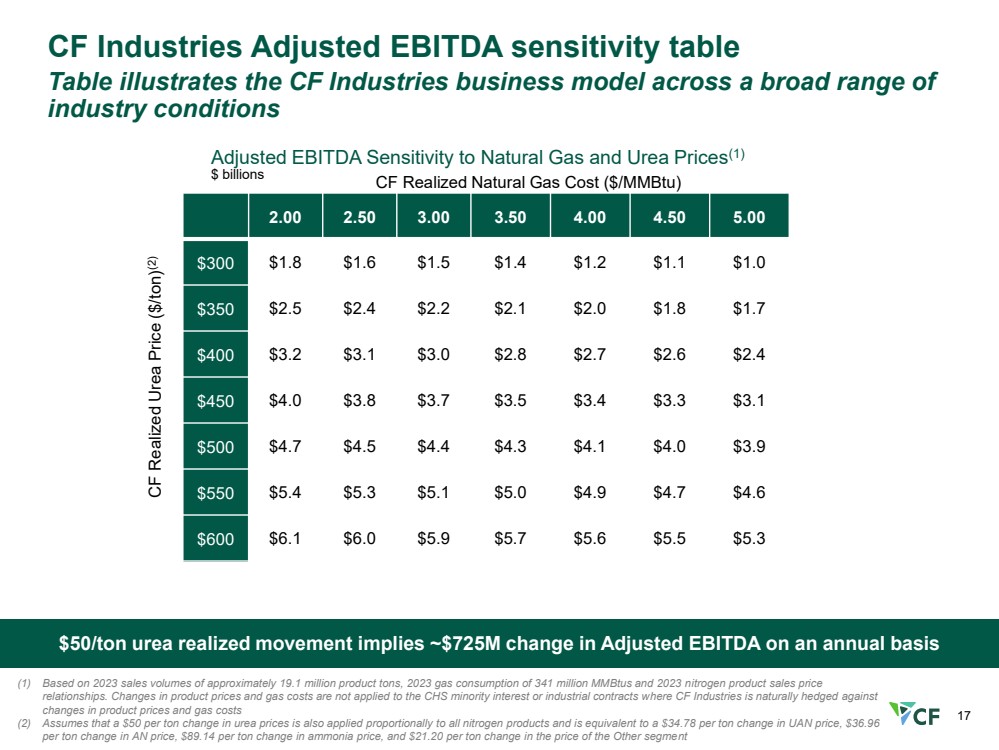

| 17

2.00 2.50 3.00 3.50 4.00 4.50 5.00

$300 $1.8 $1.6 $1.5 $1.4 $1.2 $1.1 $1.0

$350 $2.5 $2.4 $2.2 $2.1 $2.0 $1.8 $1.7

$400 $3.2 $3.1 $3.0 $2.8 $2.7 $2.6 $2.4

$450 $4.0 $3.8 $3.7 $3.5 $3.4 $3.3 $3.1

$500 $4.7 $4.5 $4.4 $4.3 $4.1 $4.0 $3.9

$550 $5.4 $5.3 $5.1 $5.0 $4.9 $4.7 $4.6

$600 $6.1 $6.0 $5.9 $5.7 $5.6 $5.5 $5.3

CF Industries Adjusted EBITDA sensitivity table

Table illustrates the CF Industries business model across a broad range of

industry conditions

$50/ton urea realized movement implies ~$725M change in Adjusted EBITDA on an annual basis

(1) Based on 2023 sales volumes of approximately 19.1 million product tons, 2023 gas consumption of 341 million MMBtus and 2023 nitrogen product sales price

relationships. Changes in product prices and gas costs are not applied to the CHS minority interest or industrial contracts where CF Industries is naturally hedged against

changes in product prices and gas costs

(2) Assumes that a $50 per ton change in urea prices is also applied proportionally to all nitrogen products and is equivalent to a $34.78 per ton change in UAN price, $36.96

per ton change in AN price, $89.14 per ton change in ammonia price, and $21.20 per ton change in the price of the Other segment

Adjusted EBITDA Sensitivity to Natural Gas and Urea Prices(1)

$ billions CF Realized Natural Gas Cost ($/MMBtu)

CF Realized Urea Price ($/ton)(2) |

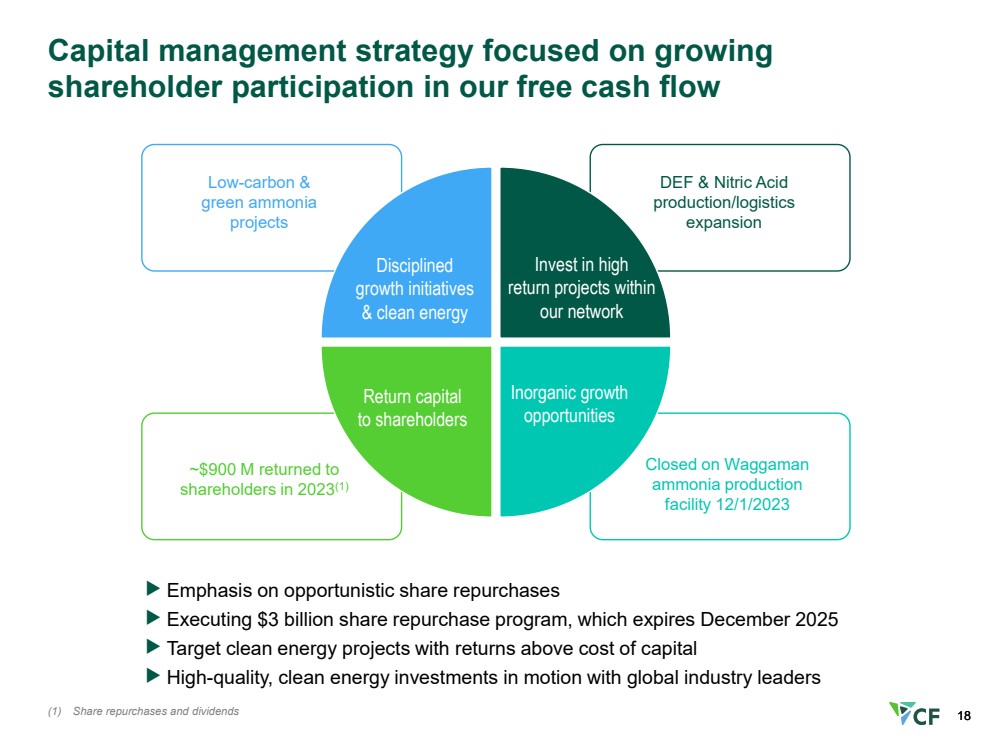

| 18

Capital management strategy focused on growing

shareholder participation in our free cash flow

Emphasis on opportunistic share repurchases

Executing $3 billion share repurchase program, which expires December 2025

Target clean energy projects with returns above cost of capital

High-quality, clean energy investments in motion with global industry leaders

~$900 M returned to

shareholders in 2023(1)

Closed on Waggaman

ammonia production

facility 12/1/2023

Low-carbon &

green ammonia

projects

DEF & Nitric Acid

production/logistics

expansion

Return capital

to shareholders

Inorganic growth

opportunities

Invest in high

return projects within

our network

Disciplined

growth initiatives

& clean energy

18 (1) Share repurchases and dividends |

| 19

Advancing decarbonization through significant progress on

strategic initiatives

Clean Energy

Growth

Purchased natural

gas certified by MiQ

Donaldsonville

green ammonia

Donaldsonville

CCS low-carbon ammonia

Engineering

activities ongoing

Low-carbon ammonia plant

(SMR w/CCS)

FEED study

FID targeted

2H 2024

Flue gas capture

FEED study

Clean ammonia industry

demand milestones

Potential supply of

low-carbon

ammonia into Asia

PROJECTS

ATR ammonia

production technology

FEED study

Decarbonization

Inorganic Growth

Closed 12/1/2023

Waggaman ammonia

production facility

Expected

completion

2H 2024

2025 project

start-up

Purchased 2.2 BCF Purchased 4.4 BCF

• European CBAM

• NH3 marine engine

commercialization

JERA: first commercial

co-fire test at Hekinan

coal fired power plant

Initial FEED study

completed

Estimated completion of

greenfield low-carbon

ammonia facility

(~4 years from FID)

Commissioning

activities underway

MOUs signed between

CF, JERA, POSCO &

LOTTE |

| 20

Global grain stocks-to-use expected to approach five-year

average by end of the 2024 growing season

(1) Crop futures prices represent Marketing Year (September – August) average daily settlement of the front month future contracts for 2011/12 through 2022/23. 2023/24F

represents actual futures settlements through January 16, 2024, and the forward curve through August 2024.

Source: USDA, CME, CF Analysis

Global Coarse Grains Stocks-to-Use Ratio

vs Corn Futures Prices(1)

Percent

$0

$1

$2

$3

$4

$5

$6

$7

0%

2%

4%

6%

8%

10%

12%

14%

16%

World ex-China

Crop Futures Price (RHS)

USD per Bushel

Global Oilseeds Stocks-to-Use Ratio vs

Soybean Futures Prices

Percent

$0

$2

$4

$6

$8

$10

$12

$14

$16

0%

5%

10%

15%

20%

25%

30%

World ex-China

Crop Futures Price (RHS)

USD per Bushel |

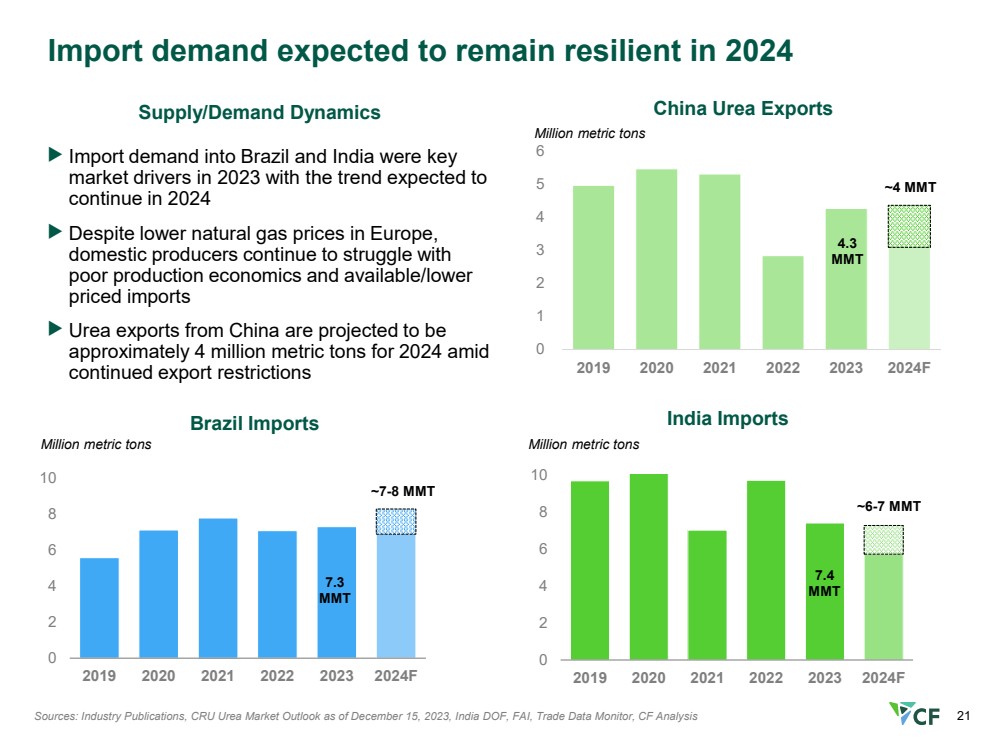

| 21

0

2

4

6

8

10

2019 2020 2021 2022 2023 2024F

0

2

4

6

8

10

2019 2020 2021 2022 2023 2024F

Import demand expected to remain resilient in 2024

Sources: Industry Publications, CRU Urea Market Outlook as of December 15, 2023, India DOF, FAI, Trade Data Monitor, CF Analysis

India Imports

Million metric tons

Brazil Imports

Million metric tons

Supply/Demand Dynamics

7.3

MMT

0

1

2

3

4

5

6

2019 2020 2021 2022 2023 2024F

China Urea Exports

Million metric tons

7.4

MMT

4.3

MMT

Import demand into Brazil and India were key

market drivers in 2023 with the trend expected to

continue in 2024

Despite lower natural gas prices in Europe,

domestic producers continue to struggle with

poor production economics and available/lower

priced imports

Urea exports from China are projected to be

approximately 4 million metric tons for 2024 amid

continued export restrictions

~6-7 MMT

~4 MMT

~7-8 MMT |

| 22

North American Nitrogen Precedent Transactions

Project FID

Year

Completion

Year

Total Cost

$M

Net N Volume

000's $000's / N

North American Nitrogen Assets

CF - Terra Acquisition 2010 2010 4,800 2,414 2.0

CF - Medicine Hat Acquisition 2012 2012 900 346 2.6

CF - Donaldsonville Construction Cost 2012 2016 2,643 1,067 2.5

LSB - El Dorado Construction Cost 2012 2016 830 308 2.7

CF - Port Neal Construction Cost 2012 2016 2,557 772 3.3

OCI - Wever, IA Construction Cost 2017 2017 2,600 713 3.6

Austin Powder - Mosheim, TN Construction Cost 2016 2016 225 53 4.3

CF & CHS Strategic Venture 2016 2016 2,800 689 4.1

Koch - Wever Acquisition 2023 2024 3,600 713 5.0 |

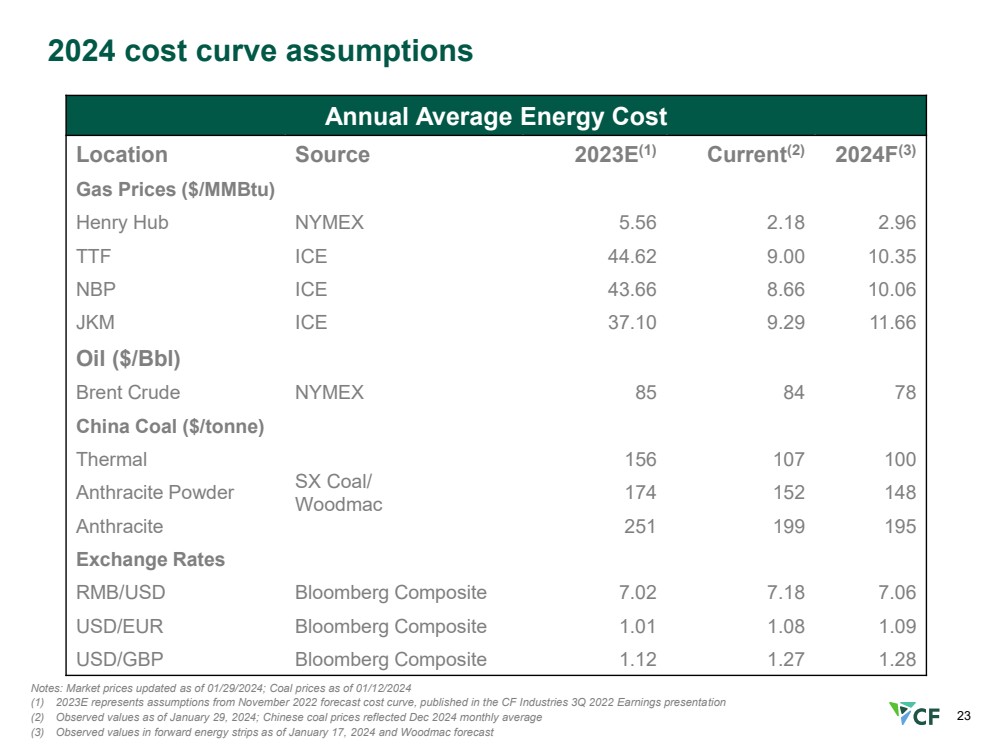

| 23

Annual Average Energy Cost

Location Source 2023E(1) Current(2) 2024F(3)

Gas Prices ($/MMBtu)

Henry Hub NYMEX 5.56 2.18 2.96

TTF ICE 44.62 9.00 10.35

NBP ICE 43.66 8.66 10.06

JKM ICE 37.10 9.29 11.66

Oil ($/Bbl)

Brent Crude NYMEX 85 84 78

China Coal ($/tonne)

Thermal

SX Coal/

Woodmac

156 107 100

Anthracite Powder 174 152 148

Anthracite 251 199 195

Exchange Rates

RMB/USD Bloomberg Composite 7.02 7.18 7.06

USD/EUR Bloomberg Composite 1.01 1.08 1.09

USD/GBP Bloomberg Composite 1.12 1.27 1.28

Notes: Market prices updated as of 01/29/2024; Coal prices as of 01/12/2024

(1) 2023E represents assumptions from November 2022 forecast cost curve, published in the CF Industries 3Q 2022 Earnings presentation

(2) Observed values as of January 29, 2024; Chinese coal prices reflected Dec 2024 monthly average

(3) Observed values in forward energy strips as of January 17, 2024 and Woodmac forecast

2024 cost curve assumptions |

| 24

Non-GAAP: reconciliation of net earnings to EBITDA and

adjusted EBITDA

In millions Q4 2023 Q4 2022 FY 2023 FY 2022

Net earnings $ 352 $ 1,009 $ 1,838 $ 3,937

Less: Net earnings attributable to noncontrolling interest (78) (149) (313) (591)

Net earnings attributable to common stockholders 274 860 1,525 3,346

Interest (income) expense – net (8) (34) (8) 279

Income tax provision 84 245 410 1,158

Depreciation and amortization 229 198 869 850

Less other adjustments:

Depreciation and amortization in noncontrolling interest (22) (22) (85) (87)

Loan fee amortization(1) (1) (1) (4) (4)

EBITDA $ 556 $ 1,246 $ 2,707 $ 5,542

Unrealized net mark-to-market loss (gain) on natural gas

derivatives

(Gain) loss on foreign currency transactions, including

intercompany loans

U.K. long-lived and intangible asset impairment

U.K. operations restructuring

Acquisition and integration costs

Impairment of equity method investment in PLNL

26 80 (39) 41

(5) (10) — 28

— — — 239

3 1 10 19

12 — 39 —

— — 43 —

Unrealized gain on embedded derivative liability — (14) — (14)

Pension settlement loss and curtailments gains—net — (7) — 17

Loss on debt extinguishment — — — 8

Total adjustments 36 50 53 338

Adjusted EBITDA $ 592 $ 1,296 $ 2,760 $ 5,880

(1) Loan fee amortization is included in both interest expense – net and depreciation and amortization |

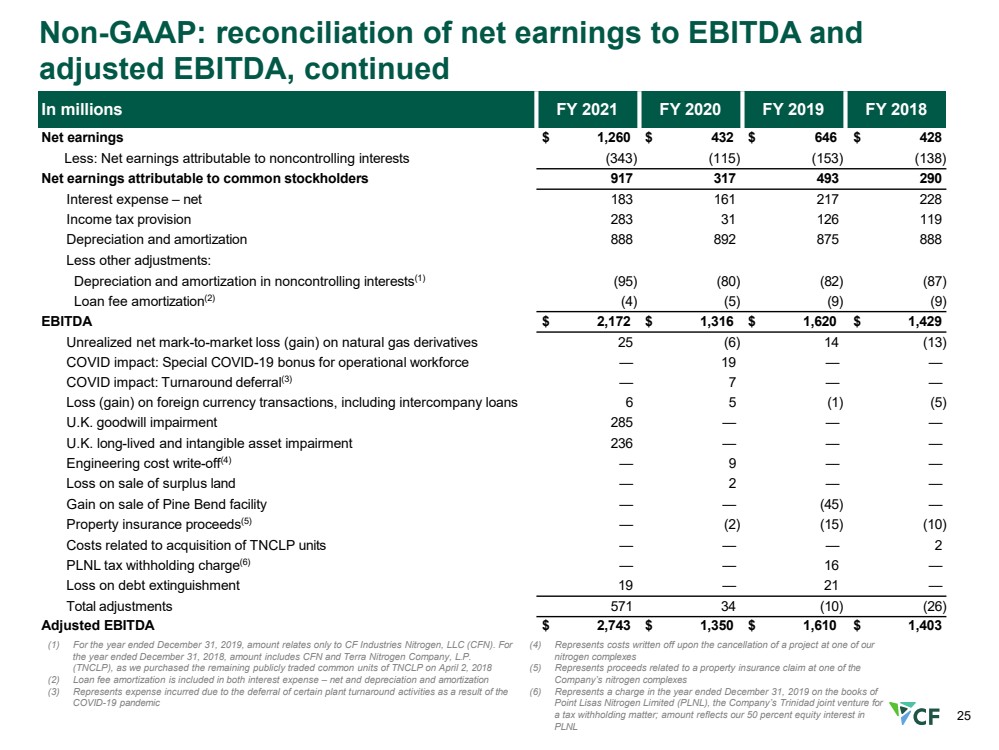

| 25

Non-GAAP: reconciliation of net earnings to EBITDA and

adjusted EBITDA, continued

In millions FY 2021 FY 2020 FY 2019 FY 2018

Net earnings $ 1,260 $ 432 $ 646 $ 428

Less: Net earnings attributable to noncontrolling interests (343) (115) (153) (138)

Net earnings attributable to common stockholders 917 317 493 290

Interest expense – net 183 161 217 228

Income tax provision 283 31 126 119

Depreciation and amortization 888 892 875 888

Less other adjustments:

Depreciation and amortization in noncontrolling interests(1) (95) (80) (82) (87)

Loan fee amortization(2) (4) (5) (9) (9)

EBITDA $ 2,172 $ 1,316 $ 1,620 $ 1,429

Unrealized net mark-to-market loss (gain) on natural gas derivatives 25 (6) 14 (13)

COVID impact: Special COVID-19 bonus for operational workforce — 19 — —

COVID impact: Turnaround deferral(3) — 7 — —

Loss (gain) on foreign currency transactions, including intercompany loans 6 5 (1) (5)

U.K. goodwill impairment 285 — — —

U.K. long-lived and intangible asset impairment 236 — — —

Engineering cost write-off(4) — 9 — —

Loss on sale of surplus land — 2 — —

Gain on sale of Pine Bend facility — — (45) —

Property insurance proceeds(5) — (2) (15) (10)

Costs related to acquisition of TNCLP units — — — 2

PLNL tax withholding charge(6) — — 16 —

Loss on debt extinguishment 19 — 21 —

Total adjustments 571 34 (10) (26)

Adjusted EBITDA $ 2,743 $ 1,350 $ 1,610 $ 1,403

(1) For the year ended December 31, 2019, amount relates only to CF Industries Nitrogen, LLC (CFN). For

the year ended December 31, 2018, amount includes CFN and Terra Nitrogen Company, L.P.

(TNCLP), as we purchased the remaining publicly traded common units of TNCLP on April 2, 2018

(2) Loan fee amortization is included in both interest expense – net and depreciation and amortization

(3) Represents expense incurred due to the deferral of certain plant turnaround activities as a result of the

COVID-19 pandemic

(4) Represents costs written off upon the cancellation of a project at one of our

nitrogen complexes

(5) Represents proceeds related to a property insurance claim at one of the

Company’s nitrogen complexes

(6) Represents a charge in the year ended December 31, 2019 on the books of

Point Lisas Nitrogen Limited (PLNL), the Company’s Trinidad joint venture for

a tax withholding matter; amount reflects our 50 percent equity interest in

PLNL |

| 26

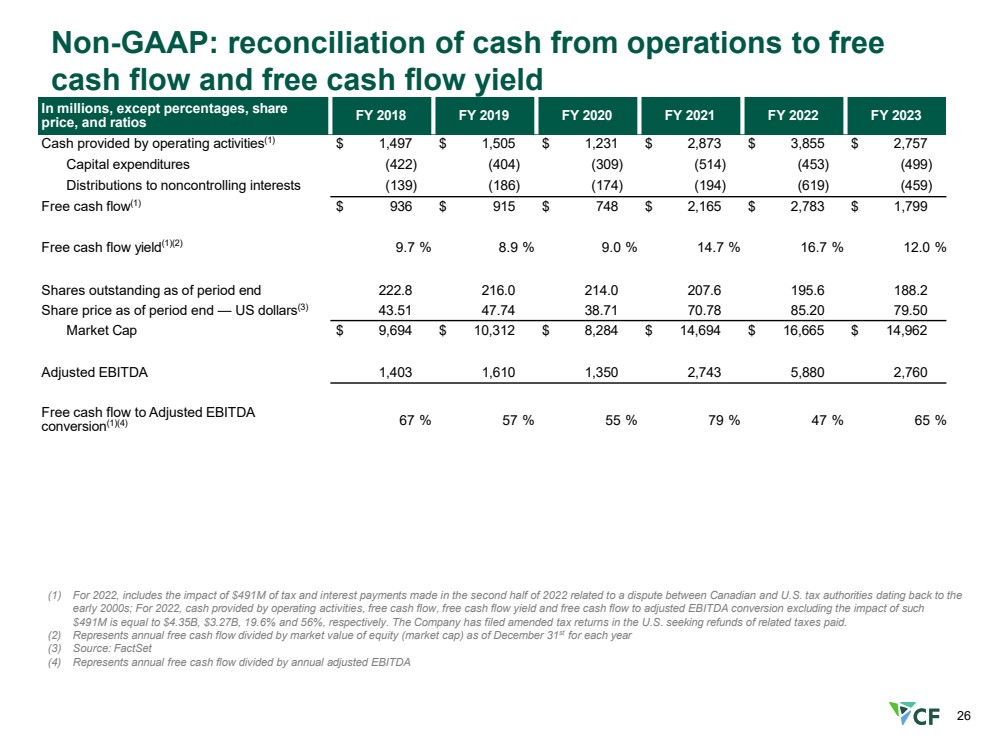

Non-GAAP: reconciliation of cash from operations to free

cash flow and free cash flow yield

In millions, except percentages, share

price, and ratios FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023

Cash provided by operating activities(1) $ 1,497 $ 1,505 $ 1,231 $ 2,873 $ 3,855 $ 2,757

Capital expenditures (422) (404) (309) (514) (453) (499)

Distributions to noncontrolling interests (139) (186) (174) (194) (619) (459)

Free cash flow(1) $ 936 $ 915 $ 748 $ 2,165 $ 2,783 $ 1,799

Free cash flow yield(1)(2) 9.7 % 8.9 % 9.0 % 14.7 % 16.7 % 12.0 %

Shares outstanding as of period end 222.8 216.0 214.0 207.6 195.6 188.2

Share price as of period end — US dollars(3) 43.51 47.74 38.71 70.78 85.20 79.50

Market Cap $ 9,694 $ 10,312 $ 8,284 $ 14,694 $ 16,665 $ 14,962

Adjusted EBITDA 1,403 1,610 1,350 2,743 5,880 2,760

Free cash flow to Adjusted EBITDA

conversion(1)(4) 67 % 57 % 55 % 79 % 47 % 65 %

(1) For 2022, includes the impact of $491M of tax and interest payments made in the second half of 2022 related to a dispute between Canadian and U.S. tax authorities dating back to the

early 2000s; For 2022, cash provided by operating activities, free cash flow, free cash flow yield and free cash flow to adjusted EBITDA conversion excluding the impact of such

$491M is equal to $4.35B, $3.27B, 19.6% and 56%, respectively. The Company has filed amended tax returns in the U.S. seeking refunds of related taxes paid.

(2) Represents annual free cash flow divided by market value of equity (market cap) as of December 31st for each year

(3) Source: FactSet

(4) Represents annual free cash flow divided by annual adjusted EBITDA |

| X |

- DefinitionBoolean flag that is true when the XBRL content amends previously-filed or accepted submission.

| Name: |

dei_AmendmentFlag |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionFor the EDGAR submission types of Form 8-K: the date of the report, the date of the earliest event reported; for the EDGAR submission types of Form N-1A: the filing date; for all other submission types: the end of the reporting or transition period. The format of the date is YYYY-MM-DD.

| Name: |

dei_DocumentPeriodEndDate |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:dateItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe type of document being provided (such as 10-K, 10-Q, 485BPOS, etc). The document type is limited to the same value as the supporting SEC submission type, or the word 'Other'.

| Name: |

dei_DocumentType |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:submissionTypeItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionAddress Line 1 such as Attn, Building Name, Street Name

| Name: |

dei_EntityAddressAddressLine1 |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- Definition

+ References

+ Details

| Name: |

dei_EntityAddressCityOrTown |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionCode for the postal or zip code

| Name: |

dei_EntityAddressPostalZipCode |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionName of the state or province.

| Name: |

dei_EntityAddressStateOrProvince |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:stateOrProvinceItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionA unique 10-digit SEC-issued value to identify entities that have filed disclosures with the SEC. It is commonly abbreviated as CIK. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityCentralIndexKey |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:centralIndexKeyItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionIndicate if registrant meets the emerging growth company criteria. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityEmergingGrowthCompany |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionCommission file number. The field allows up to 17 characters. The prefix may contain 1-3 digits, the sequence number may contain 1-8 digits, the optional suffix may contain 1-4 characters, and the fields are separated with a hyphen.

| Name: |

dei_EntityFileNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:fileNumberItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTwo-character EDGAR code representing the state or country of incorporation.

| Name: |

dei_EntityIncorporationStateCountryCode |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:edgarStateCountryItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe exact name of the entity filing the report as specified in its charter, which is required by forms filed with the SEC. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityRegistrantName |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe Tax Identification Number (TIN), also known as an Employer Identification Number (EIN), is a unique 9-digit value assigned by the IRS. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityTaxIdentificationNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:employerIdItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionLocal phone number for entity.

| Name: |

dei_LocalPhoneNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 13e

-Subsection 4c

| Name: |

dei_PreCommencementIssuerTenderOffer |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 14d

-Subsection 2b

| Name: |

dei_PreCommencementTenderOffer |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTitle of a 12(b) registered security. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b

| Name: |

dei_Security12bTitle |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:securityTitleItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionName of the Exchange on which a security is registered. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection d1-1

| Name: |

dei_SecurityExchangeName |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:edgarExchangeCodeItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as soliciting material pursuant to Rule 14a-12 under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Section 14a

-Number 240

-Subsection 12

| Name: |

dei_SolicitingMaterial |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTrading symbol of an instrument as listed on an exchange.

| Name: |

dei_TradingSymbol |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:tradingSymbolItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as written communications pursuant to Rule 425 under the Securities Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Securities Act

-Number 230

-Section 425

| Name: |

dei_WrittenCommunications |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

CF Industries (NYSE:CF)

Graphique Historique de l'Action

De Avr 2024 à Mai 2024

CF Industries (NYSE:CF)

Graphique Historique de l'Action

De Mai 2023 à Mai 2024