REINSURANCE GROUP OF AMERICA INC false 0000898174 0000898174 2024-06-13 2024-06-13 0000898174 rga:CommonStockOutstandingMember 2024-06-13 2024-06-13 0000898174 rga:M5.75FixedToFloatingRateSubordinatedDebenturesDue2056Member 2024-06-13 2024-06-13 0000898174 rga:M7.125FixedRateResetSubordinatedDebenturesDue2052Member 2024-06-13 2024-06-13

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of Earliest Event Reported): June 13, 2024

REINSURANCE GROUP OF AMERICA, INCORPORATED

(Exact Name of Registrant as Specified in its Charter)

|

|

|

|

|

| Missouri |

|

1-11848 |

|

43-1627032 |

| (State or Other Jurisdiction of Incorporation) |

|

(Commission File Number) |

|

(IRS Employer Identification No.) |

16600 Swingley Ridge Road, Chesterfield, Missouri 63017

(Address of Principal Executive Offices, and Zip Code)

Registrant’s telephone number, including area code: (636) 736-7000

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| |

☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| |

☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

| Title of each class |

|

Trading

Symbol(s) |

|

Name of each exchange on which registered |

| Common Stock, par value $0.01 |

|

RGA |

|

New York Stock Exchange |

| 5.75% Fixed-To-Floating Rate Subordinated Debentures due 2056 |

|

RZB |

|

New York Stock Exchange |

| 7.125% Fixed-Rate Reset Subordinated Debentures due 2052 |

|

RZC |

|

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter):

☐ Emerging growth company

☐ If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

| Item 7.01 |

Regulation FD Disclosure. |

As previously reported in a Current Report on Form 8-K furnished on May 16, 2024, Reinsurance Group of America, Incorporated (the “Company”) announced that it will host a conference for institutional investors and analysts in New York City on Thursday, June 13, 2024 from 8:30 a.m. to 11:00 a.m. Eastern time. A live audio webcast of the presentation will be accessible on the Company’s website at www.rgare.com under the Investors tab. Copies of the slides used in the presentation will be available on the Company’s website at www.rgare.com through the link on the Investors tab, and are attached hereto as Exhibit 99.1 and incorporated herein by reference. An audio recording of the presentation will be made available and posted to Company’s website after the event.

The information in this Item 7.01 and the exhibit attached hereto will not be deemed to be “filed” for the purposes of Section 18 of the Securities Exchange Act of 1934 (the “Exchange Act”), or otherwise subject to the liabilities of such section, nor will such information or exhibit be deemed incorporated by reference in any filing under the Securities Act of 1933 or the Exchange Act, except as may be expressly set forth by specific reference in such filing.

| Item 9.01 |

Financial Statements and Exhibits. |

(d) Exhibits.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

|

|

|

|

|

|

|

|

|

|

REINSURANCE GROUP OF AMERICA, INCORPORATED |

|

|

|

|

| Date: June 13, 2024 |

|

|

|

By: |

|

/s/ Todd C. Larson |

|

|

|

|

|

|

Todd C. Larson |

|

|

|

|

|

|

Senior Executive Vice President and Chief Financial Officer |

Exhibit 99.1 Trusted partner. Proven results. RGA Investor Day 2024 June

13, 2024

Recent Awards and Recognitions Fortune 500 Life Reinsurer of the Year

RGA listed at #223 on the 2024 Fortune RGA Middle East was honored as “Life 500 list, which ranks U.S.-based Reinsurer of the Year” by Middle East Insurance companies by total revenues. Review at the 10th Middle East Insurance Industry

Awards 2023. World’s Most Admired NACD DE&I AWARD Companies RGA’s Board was named winner of the 2023 RGA was named to the 2024 Fortune Diversity, Equity and Inclusion Award by the World’s Most Admired Companies list National

Association of Corporate Directors. based on criteria including the company’s value as a long-term investment, quality of management, innovativeness, community Bloomberg Gender Equality Index responsibility, and the ability to attract and

retain talent. RGA was recognized on the 2023 Bloomberg Gender Equality Index for the company’s commitment to diversity and inclusion. #1 in Global Business Capability In 2023, RGA was ranked #1 for the 13th Life Reinsurer of the Year

consecutive year on NMG Consulting’s RGA was recognized by Asia Insurance Review as Global All Respondents Business Capability “Life Reinsurer of the Year” at the 2023 Asia Index, based on feedback from life and Insurance Industry

Awards. health insurance companies worldwide. 2

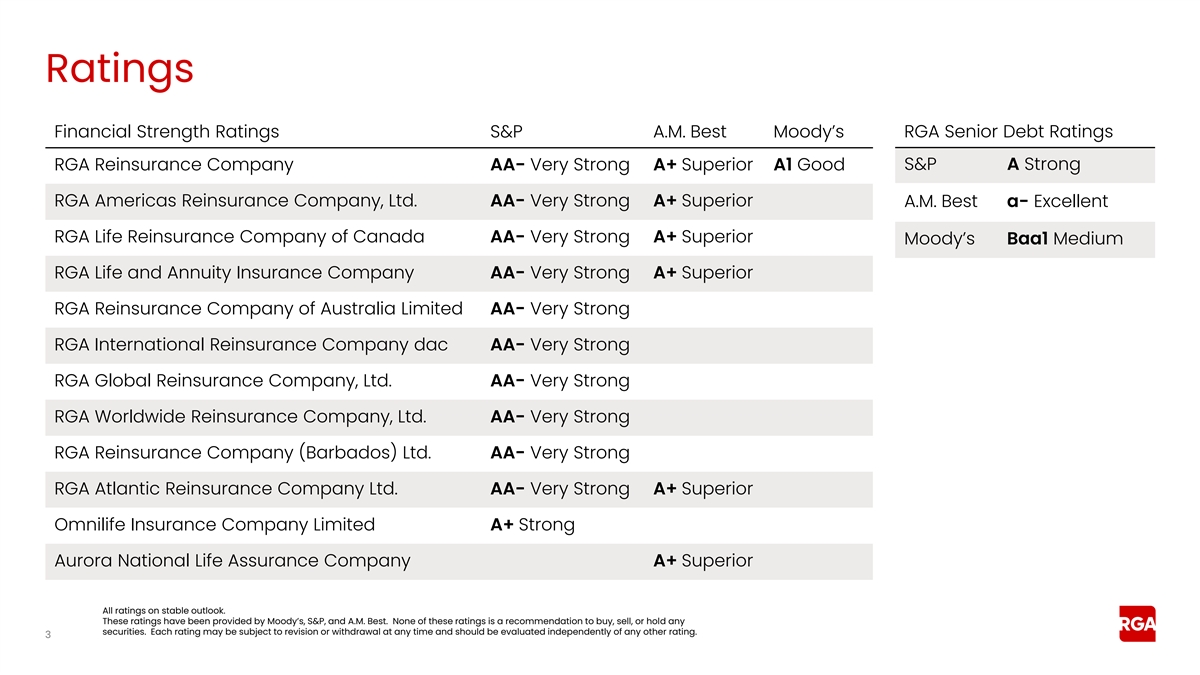

Ratings Financial Strength Ratings S&P A.M. Best Moody’s RGA

Senior Debt Ratings S&P A Strong RGA Reinsurance Company AA- Very Strong A+ Superior A1 Good RGA Americas Reinsurance Company, Ltd. AA- Very Strong A+ Superior A.M. Best a- Excellent RGA Life Reinsurance Company of Canada AA- Very Strong A+

Superior Moody’s Baa1 Medium RGA Life and Annuity Insurance Company AA- Very Strong A+ Superior RGA Reinsurance Company of Australia Limited AA- Very Strong RGA International Reinsurance Company dac AA- Very Strong RGA Global Reinsurance

Company, Ltd. AA- Very Strong RGA Worldwide Reinsurance Company, Ltd. AA- Very Strong RGA Reinsurance Company (Barbados) Ltd. AA- Very Strong RGA Atlantic Reinsurance Company Ltd. AA- Very Strong A+ Superior Omnilife Insurance Company Limited A+

Strong Aurora National Life Assurance Company A+ Superior All ratings on stable outlook. These ratings have been provided by Moody’s, S&P, and A.M. Best. None of these ratings is a recommendation to buy, sell, or hold any securities. Each

rating may be subject to revision or withdrawal at any time and should be evaluated independently of any other rating. 3

Responsibilities and Commitments Governance Social Impact Sustainability

1 Committed to providing Board and executive Targeting net-zero GHG oversight of sustainability a diverse and inclusive by 2026 workplace that respects strategy and embraces all Targeting a 20% Annual sustainability reduction in the carbon Expanded

programs to reporting aligned with Sustainable intensity of public 3 support employee TCFD and SASB corporate bond portfolio principles are 2 volunteerism and by the end of 2026 essential to our targeted workforce Board diversity with 75% engagement

of 50% by female or ethnically/ Increased investments in long-term 2026 racially diverse renewable energy, success and are health, education, and Increased philanthropic sustainable development embedded in support through the RGA our culture and

Foundation and Longer Life Foundation business strategy 1 Operational Greenhouse Gas Emissions, Scope 1 and 2. 2 From YE 2021 baseline; Scope 1 and Scope 2 intensity where information is available. 3 Task Force on Climate-Related Financial

Disclosures, Sustainability Accounting Standards Board. 4

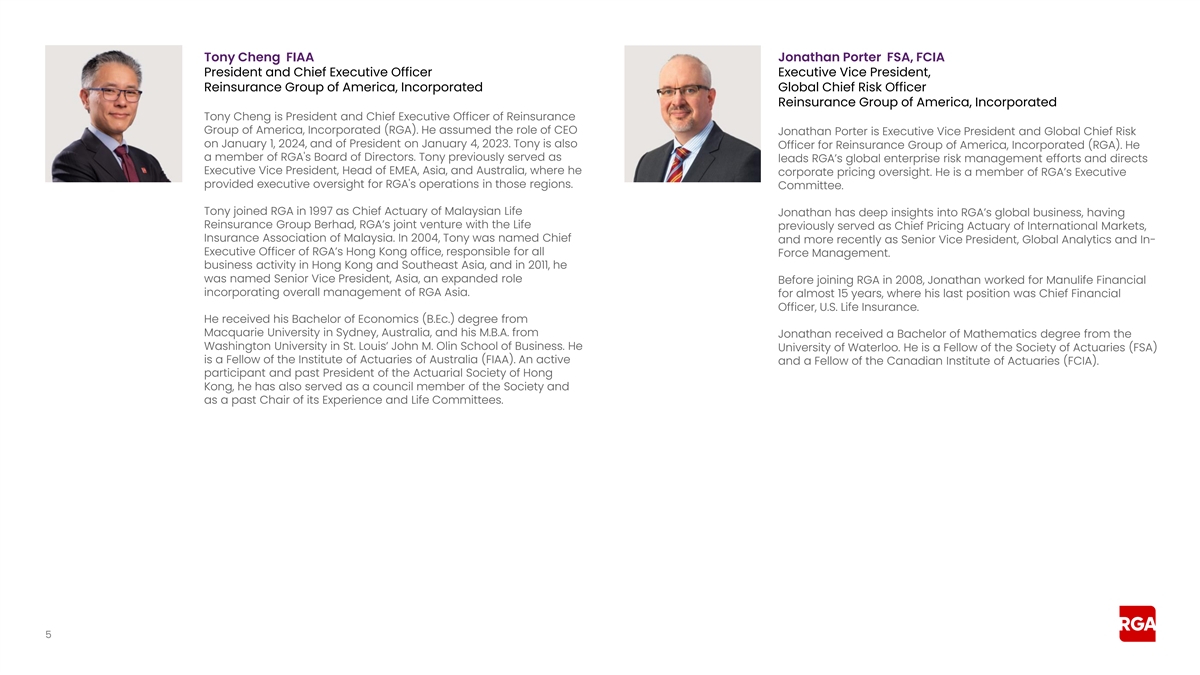

Tony Cheng FIAA Jonathan Porter FSA, FCIA President and Chief Executive

Officer Executive Vice President, Reinsurance Group of America, Incorporated Global Chief Risk Officer Reinsurance Group of America, Incorporated Tony Cheng is President and Chief Executive Officer of Reinsurance Group of America, Incorporated

(RGA). He assumed the role of CEO Jonathan Porter is Executive Vice President and Global Chief Risk on January 1, 2024, and of President on January 4, 2023. Tony is also Officer for Reinsurance Group of America, Incorporated (RGA). He a member of

RGA's Board of Directors. Tony previously served as leads RGA’s global enterprise risk management efforts and directs Executive Vice President, Head of EMEA, Asia, and Australia, where he corporate pricing oversight. He is a member of

RGA’s Executive provided executive oversight for RGA's operations in those regions. Committee. Tony joined RGA in 1997 as Chief Actuary of Malaysian Life Jonathan has deep insights into RGA’s global business, having Reinsurance Group

Berhad, RGA’s joint venture with the Life previously served as Chief Pricing Actuary of International Markets, Insurance Association of Malaysia. In 2004, Tony was named Chief and more recently as Senior Vice President, Global Analytics and

In- Executive Officer of RGA’s Hong Kong office, responsible for all Force Management. business activity in Hong Kong and Southeast Asia, and in 2011, he was named Senior Vice President, Asia, an expanded role Before joining RGA in 2008,

Jonathan worked for Manulife Financial incorporating overall management of RGA Asia. for almost 15 years, where his last position was Chief Financial Officer, U.S. Life Insurance. He received his Bachelor of Economics (B.Ec.) degree from Macquarie

University in Sydney, Australia, and his M.B.A. from Jonathan received a Bachelor of Mathematics degree from the Washington University in St. Louis’ John M. Olin School of Business. He University of Waterloo. He is a Fellow of the Society of

Actuaries (FSA) is a Fellow of the Institute of Actuaries of Australia (FIAA). An active and a Fellow of the Canadian Institute of Actuaries (FCIA). participant and past President of the Actuarial Society of Hong Kong, he has also served as a

council member of the Society and as a past Chair of its Experience and Life Committees. 5

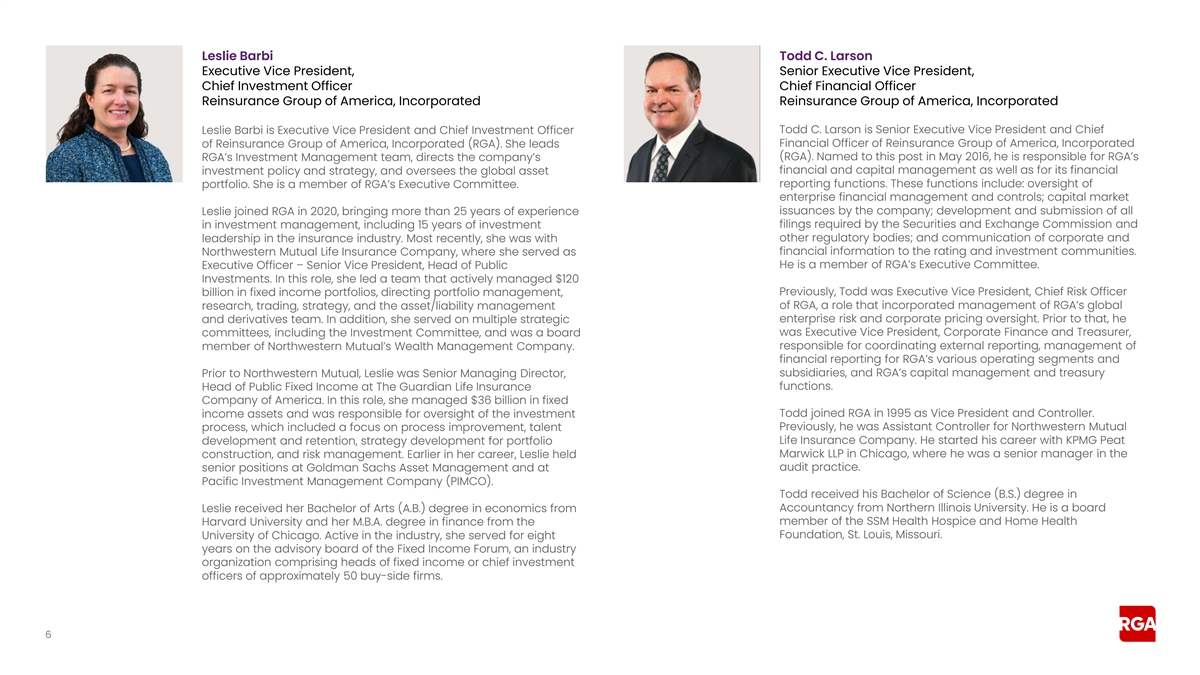

Leslie Barbi Todd C. Larson Executive Vice President, Senior Executive

Vice President, Chief Investment Officer Chief Financial Officer Reinsurance Group of America, Incorporated Reinsurance Group of America, Incorporated Leslie Barbi is Executive Vice President and Chief Investment Officer Todd C. Larson is Senior

Executive Vice President and Chief of Reinsurance Group of America, Incorporated (RGA). She leads Financial Officer of Reinsurance Group of America, Incorporated (RGA). Named to this post in May 2016, he is responsible for RGA’s RGA’s

Investment Management team, directs the company’s financial and capital management as well as for its financial investment policy and strategy, and oversees the global asset reporting functions. These functions include: oversight of portfolio.

She is a member of RGA’s Executive Committee. enterprise financial management and controls; capital market Leslie joined RGA in 2020, bringing more than 25 years of experience issuances by the company; development and submission of all filings

required by the Securities and Exchange Commission and in investment management, including 15 years of investment other regulatory bodies; and communication of corporate and leadership in the insurance industry. Most recently, she was with financial

information to the rating and investment communities. Northwestern Mutual Life Insurance Company, where she served as Executive Officer – Senior Vice President, Head of Public He is a member of RGA’s Executive Committee. Investments. In

this role, she led a team that actively managed $120 Previously, Todd was Executive Vice President, Chief Risk Officer billion in fixed income portfolios, directing portfolio management, of RGA, a role that incorporated management of RGA’s

global research, trading, strategy, and the asset/liability management enterprise risk and corporate pricing oversight. Prior to that, he and derivatives team. In addition, she served on multiple strategic committees, including the Investment

Committee, and was a board was Executive Vice President, Corporate Finance and Treasurer, member of Northwestern Mutual’s Wealth Management Company. responsible for coordinating external reporting, management of financial reporting for

RGA’s various operating segments and subsidiaries, and RGA’s capital management and treasury Prior to Northwestern Mutual, Leslie was Senior Managing Director, functions. Head of Public Fixed Income at The Guardian Life Insurance Company

of America. In this role, she managed $36 billion in fixed income assets and was responsible for oversight of the investment Todd joined RGA in 1995 as Vice President and Controller. Previously, he was Assistant Controller for Northwestern Mutual

process, which included a focus on process improvement, talent Life Insurance Company. He started his career with KPMG Peat development and retention, strategy development for portfolio Marwick LLP in Chicago, where he was a senior manager in the

construction, and risk management. Earlier in her career, Leslie held senior positions at Goldman Sachs Asset Management and at audit practice. Pacific Investment Management Company (PIMCO). Todd received his Bachelor of Science (B.S.) degree in

Accountancy from Northern Illinois University. He is a board Leslie received her Bachelor of Arts (A.B.) degree in economics from member of the SSM Health Hospice and Home Health Harvard University and her M.B.A. degree in finance from the

University of Chicago. Active in the industry, she served for eight Foundation, St. Louis, Missouri. years on the advisory board of the Fixed Income Forum, an industry organization comprising heads of fixed income or chief investment officers of

approximately 50 buy-side firms. 6

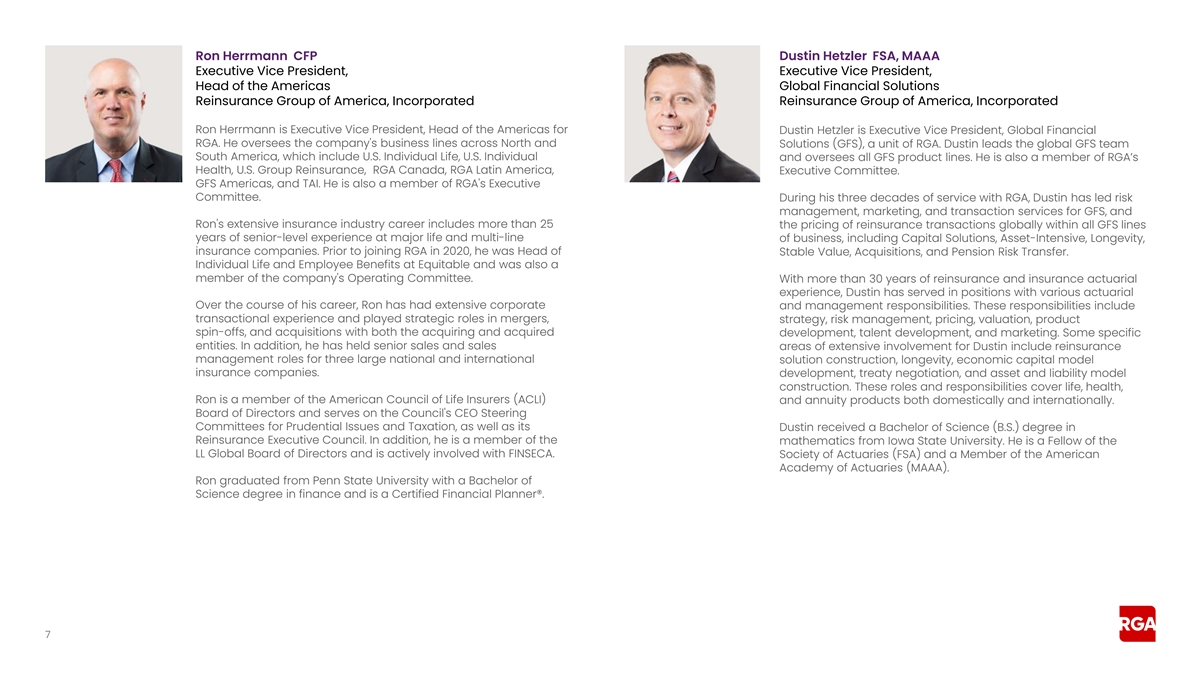

Ron Herrmann CFP Dustin Hetzler FSA, MAAA Executive Vice President,

Executive Vice President, Head of the Americas Global Financial Solutions Reinsurance Group of America, Incorporated Reinsurance Group of America, Incorporated Ron Herrmann is Executive Vice President, Head of the Americas for Dustin Hetzler is

Executive Vice President, Global Financial RGA. He oversees the company's business lines across North and Solutions (GFS), a unit of RGA. Dustin leads the global GFS team South America, which include U.S. Individual Life, U.S. Individual and

oversees all GFS product lines. He is also a member of RGA’s Health, U.S. Group Reinsurance, RGA Canada, RGA Latin America, Executive Committee. GFS Americas, and TAI. He is also a member of RGA's Executive Committee. During his three decades

of service with RGA, Dustin has led risk management, marketing, and transaction services for GFS, and Ron's extensive insurance industry career includes more than 25 the pricing of reinsurance transactions globally within all GFS lines years of

senior-level experience at major life and multi-line of business, including Capital Solutions, Asset-Intensive, Longevity, insurance companies. Prior to joining RGA in 2020, he was Head of Stable Value, Acquisitions, and Pension Risk Transfer.

Individual Life and Employee Benefits at Equitable and was also a member of the company's Operating Committee. With more than 30 years of reinsurance and insurance actuarial experience, Dustin has served in positions with various actuarial Over the

course of his career, Ron has had extensive corporate and management responsibilities. These responsibilities include transactional experience and played strategic roles in mergers, strategy, risk management, pricing, valuation, product spin-offs,

and acquisitions with both the acquiring and acquired development, talent development, and marketing. Some specific entities. In addition, he has held senior sales and sales areas of extensive involvement for Dustin include reinsurance management

roles for three large national and international solution construction, longevity, economic capital model insurance companies. development, treaty negotiation, and asset and liability model construction. These roles and responsibilities cover life,

health, Ron is a member of the American Council of Life Insurers (ACLI) and annuity products both domestically and internationally. Board of Directors and serves on the Council's CEO Steering Committees for Prudential Issues and Taxation, as well as

its Dustin received a Bachelor of Science (B.S.) degree in Reinsurance Executive Council. In addition, he is a member of the mathematics from Iowa State University. He is a Fellow of the LL Global Board of Directors and is actively involved with

FINSECA. Society of Actuaries (FSA) and a Member of the American Academy of Actuaries (MAAA). Ron graduated from Penn State University with a Bachelor of Science degree in finance and is a Certified Financial Planner®. 7

Arthur Ozeki Simon Wainwright FCIB Executive Vice President, Executive

Vice President, Head of Asia Pacific Head of EMEA Reinsurance Group of America, Incorporated Reinsurance Group of America, Incorporated Arthur Ozeki is Executive Vice President, Head of Asia Pacific, based in Simon Wainwright is Executive Vice

President, Head of EMEA. Simon is Hong Kong. Prior to his current role, he served as Senior Vice President, responsible for leading the management and growth of RGA’s China and Japan Markets. Since joining RGA in 2016 as Chief Executive

businesses and operations in the U.K. and Ireland, Continental Officer for RGA Reinsurance Company Japan Branch, Arthur has Europe, the Middle East, and Africa. He is a member of RGA’s played a pivotal role in strengthening RGA’s

presence and market Executive Committee. capabilities to serve the growing customer demand for innovative solutions in the Japan market. He is a member of RGA’s Executive Simon has more than 30 years of strategic and global leadership

Committee. experience in financial services. Prior to joining RGA in 2012 he worked for HSBC for 15 years in roles as varied as CEO HSBC Bank Arthur has more than 30 years of experience in international financial Ireland during the GFC, COO, Global

Commercial & Corporate services, and he has led mergers and acquisitions (M&A) and banking Banking, and Managing Director Insurance, EMEA. He has also held teams for global investment banks in Japan and Singapore for more executive

leadership roles with Lloyds Banking Group and than 20 of those years. He has advised many leading Japanese and Nationwide Building Society. multinational institutions on highly strategic and transformational transactions, particularly in the

automotive, industrial, healthcare, and He holds several directorships with both RGA and external financial services sectors. organizations. Simon is a graduate of The University of Reading and received a Diploma in Management Studies (DMS) from

Oxford, as Prior to joining RGA, Arthur was with the Macquarie Group in Japan well as an M.B.A. from Henley Management School. In addition, he is and Singapore, as Country Head, Branch Manager, and Chairman for a Fellow of the Chartered Institute of

Bankers (now The Institute of Japan. During this period, he oversaw the development of Macquarie’s Financial Services), and a Chartered Company Director and Fellow business in Japan across multiple areas, including investment of the Institute

of Directors. banking, capital-raising, and principal investments. In addition, Arthur has held senior leadership positions at UBS Securities and Lazard Frères in Japan, and with J.P. Morgan in both Japan and the United States. Arthur received

a Bachelor of Science (B.S.) in Computer Science and Engineering from the Massachusetts Institute of Technology and an MBA from the University of Chicago’s Graduate School of Business. 8

J. Jeffrey Hopson CFA Senior Vice President, Investor Relations

Reinsurance Group of America, Incorporated J. Jeffrey (Jeff) Hopson is Senior Vice President, Investor Relations for RGA. He is responsible for managing RGA’s financial communications with the investment community. Jeff, who came to RGA in

September 2013, has several decades of experience in the field of investment analysis, following a wide range of life and property-casualty insurance and asset management firms. A ten-time All-Star Analyst in The Wall Street Journal’s annual

Best of the Street poll, Jeff is also a member of the Journal’s Analysts Hall of Fame. Prior to joining RGA, Jeff was a Managing Director and Senior Analyst with the St. Louis-based brokerage and investment firm of Stifel, Nicolaus &

Company. Previously, he served in a variety of roles with the St. Louis-based regional brokerage firm of A.G. Edwards & Sons, Inc., culminating as Vice President, Senior Analyst and Group Leader, Financial Services. Jeff’s Bachelor of Arts

(B.A.) and M.B.A. degrees in Finance are from Saint Louis University. He is a Chartered Financial Analyst (CFA). 9

Welcome Jeff Hopson Senior Vice President, Investor Relations

10

Safe Harbor This document contains forward-looking statements within

the meaning of the Private Securities Litigation Reform Act of 1995 and federal securities laws including, among others, statements relating to projections of the future operations, strategies, earnings, revenues, income or loss, ratios, financial

performance and growth potential of Reinsurance Group of America, Incorporated (the “Company”). Forward-looking statements often contain words and phrases such as “anticipate,” “assume,” “believe,”

“continue,” “could,” “estimate,” “expect,” “if,” “intend,” “likely,” “may,” “plan,” “potential,” “pro forma,”

“project,” “should,” “will,” “would,” and other words and terms of similar meaning or that are otherwise tied to future periods or future performance, in each case in all derivative forms.

Forward-looking statements are based on management’s current expectations and beliefs concerning future developments and their potential effects on the Company. Forward-looking statements are not a guarantee of future performance and are

subject to risks and uncertainties, some of which cannot be predicted or quantified. Future events and actual results, performance, and achievements could differ materially from those set forth in, contemplated by or underlying the forward-looking

statements. Factors that could also cause results or events to differ, possibly materially, from those expressed or implied by forward-looking statements, include, among others: (1) adverse changes in mortality, morbidity, lapsation or claims

experience, (2) inadequate risk analysis and underwriting, (3) adverse capital and credit market conditions and their impact on the Company’s liquidity, access to capital and cost of capital, (4) changes in the Company’s financial

strength and credit ratings and the effect of such changes on the Company’s future results of operations and financial condition, (5) the availability and cost of collateral necessary for regulatory reserves and capital, (6) requirements to

post collateral or make payments due to declines in the market value of assets subject to the Company’s collateral arrangements, (7) action by regulators who have authority over the Company’s reinsurance operations in the jurisdictions

in which it operates, (8) the effect of the Company parent’s status as an insurance holding company and regulatory restrictions on its ability to pay principal of and interest on its debt obligations, (9) general economic conditions or a

prolonged economic downturn affecting the demand for insurance and reinsurance in the Company’s current and planned markets, (10) the impairment of other financial institutions and its effect on the Company’s business, (11) fluctuations

in U.S. or foreign currency exchange rates, interest rates, or securities and real estate markets, (12) market or economic conditions that adversely affect the value of the Company’s investment securities or result in the impairment of all or

a portion of the value of certain of the Company’s investment securities that in turn could affect regulatory capital, (13) market or economic conditions that adversely affect the Company’s ability to make timely sales of investment

securities, (14) risks inherent in the Company’s risk management and investment strategy, including changes in investment portfolio yields due to interest rate or credit quality changes, (15) the fact that the determination of allowances and

impairments taken on the Company’s investments is highly subjective, (16) the stability of and actions by governments and economies in the markets in which the Company operates, including ongoing uncertainties regarding the amount of U.S.

sovereign debt and the credit ratings thereof, (17) the Company’s dependence on third parties, including those insurance companies and reinsurers to which the Company cedes some reinsurance, third-party investment managers and others, (18)

financial performance of the Company’s clients, (19) the threat of natural disasters, catastrophes, terrorist attacks, pandemics, epidemics or other major public health issues anywhere in the world where the Company or its clients do business,

(20) competitive factors and competitors’ responses to the Company’s initiatives, (21) development and introduction of new products and distribution opportunities, (22) execution of the Company’s entry into new markets, (23)

integration of acquired blocks of business and entities, (24) interruption or failure of the Company’s telecommunication, information technology or other operational systems, or the Company’s failure to maintain adequate security to

protect the confidentiality or privacy of personal or sensitive data and intellectual property stored on such systems, (25) adverse developments with respect to litigation, arbitration or regulatory investigations or actions, (26) the adequacy of

reserves, resources and accurate information relating to settlements, awards and terminated and discontinued lines of business, (27) changes in laws, regulations, and accounting standards applicable to the Company or its business, including

Long-Duration Targeted Improvement accounting changes and (28) other risks and uncertainties described in this document and in the Company’s filings with the Securities and Exchange Commission (“SEC”). Forward-looking statements

should be evaluated together with the many risks and uncertainties that affect the Company’s business, including those mentioned in this document and described in the periodic reports the Company files with the SEC. These forward-looking

statements speak only as of the date on which they are made. The Company does not undertake any obligation to update these forward-looking statements, even though the Company’s situation may change in the future, except as required under

applicable securities law. For a discussion of the risks and uncertainties that could cause actual results to differ materially from those contained in the forward-looking statements, you are advised to see Item 1A – “Risk Factors”

in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023, as may be supplemented by Item 1A - “Risk Factors” in the Company’s subsequent Quarterly Reports on Form 10-Q and in our other periodic and

current reports filed with the SEC. 11

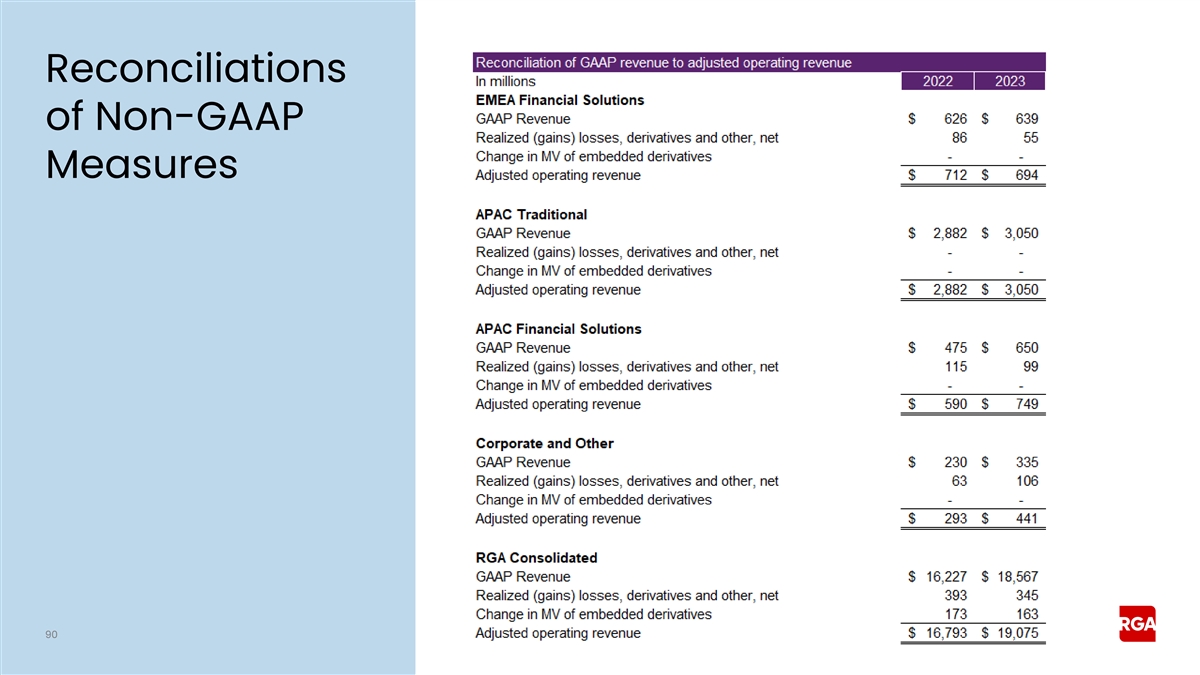

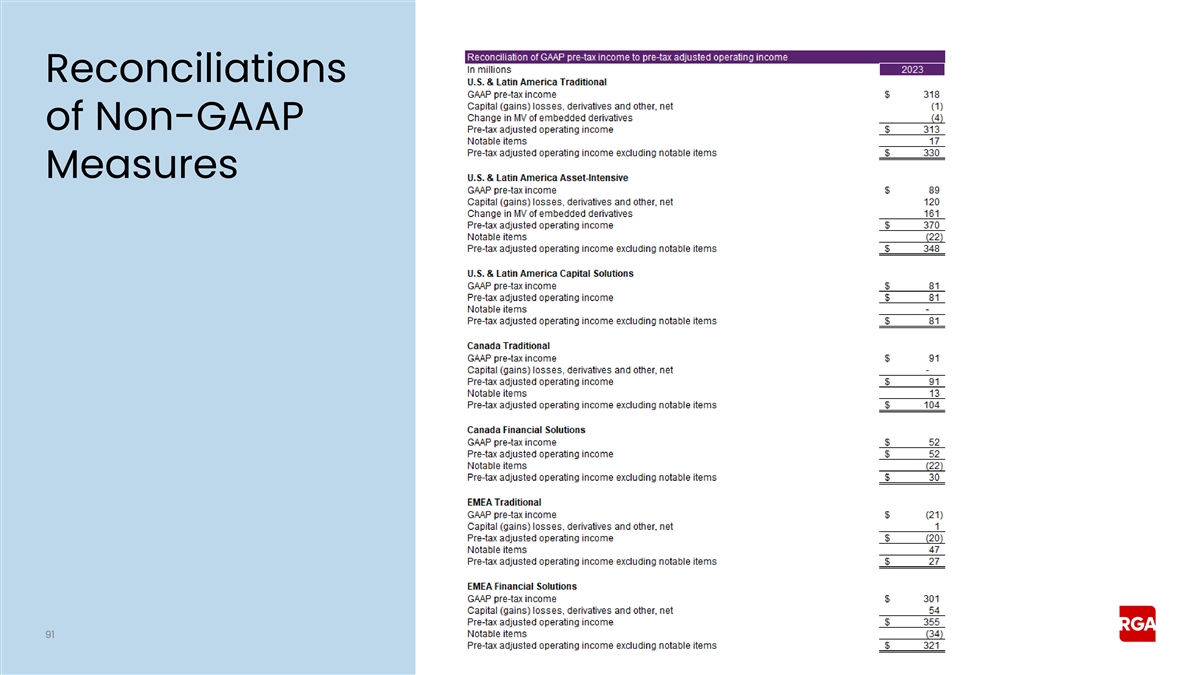

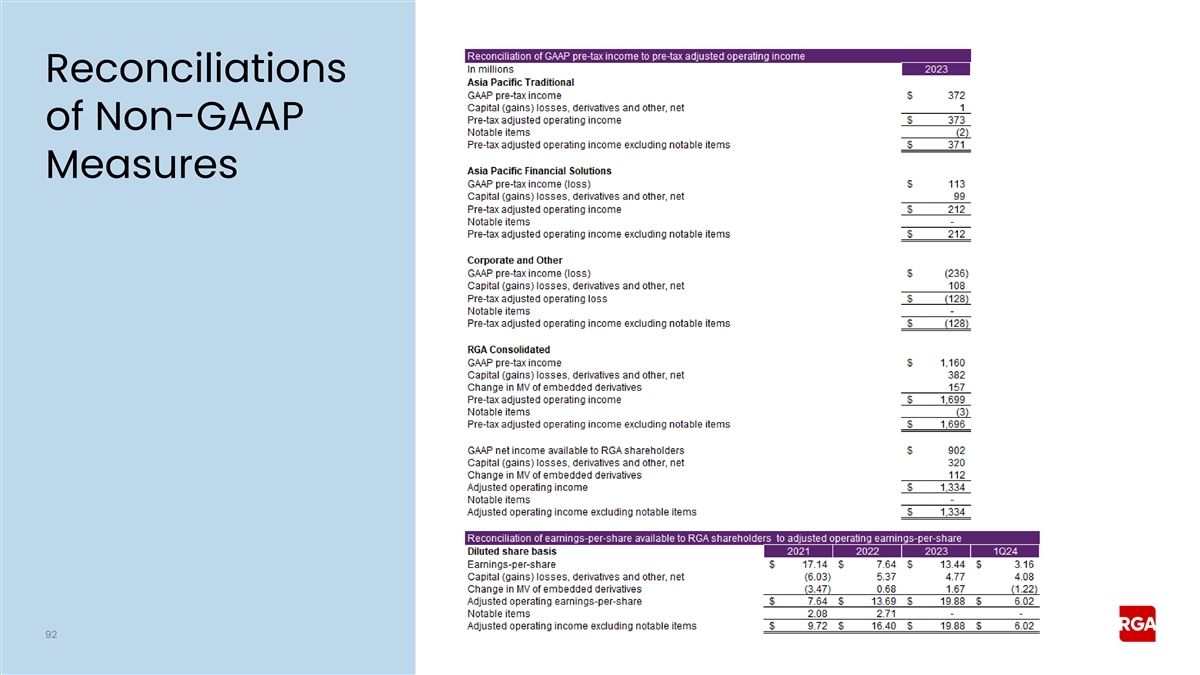

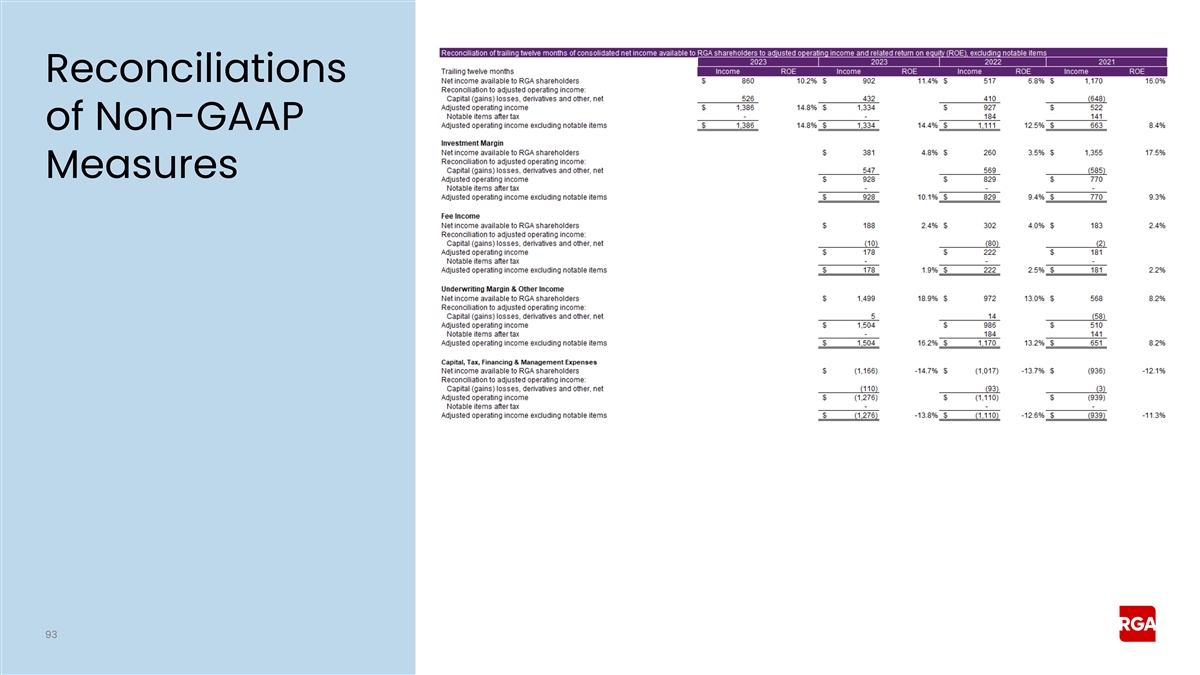

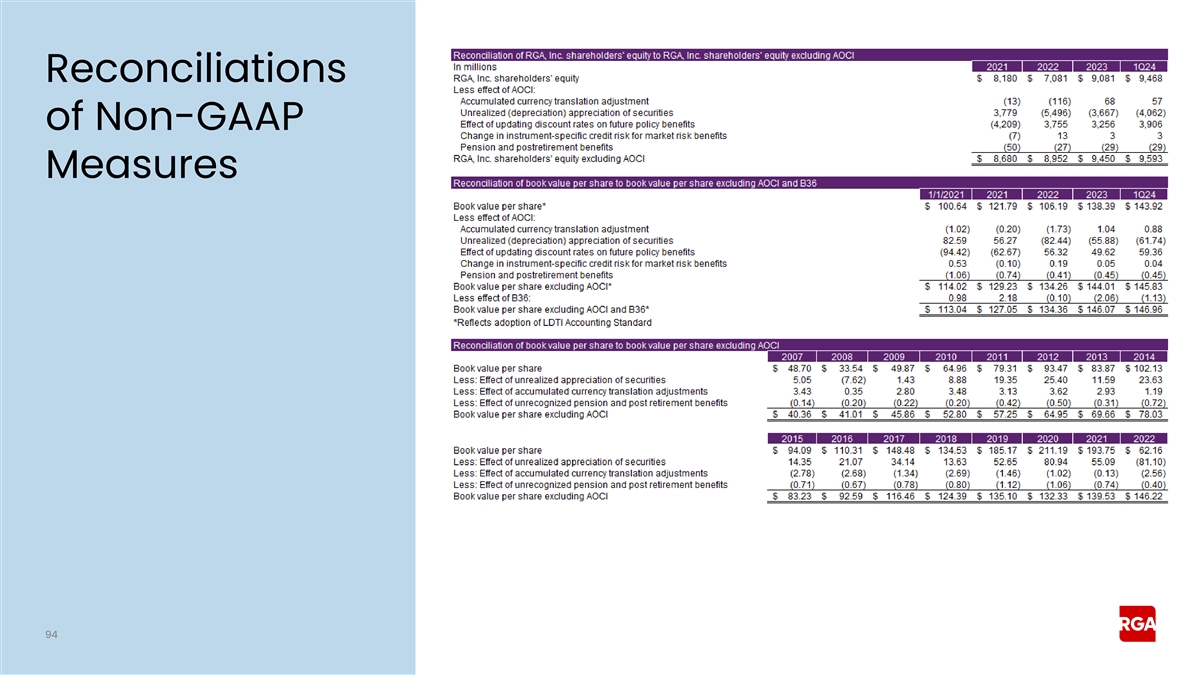

Use of Non-GAAP Financial Measures Non-GAAP Financial Measures

Reinsurance Group of America, Incorporated (the “Company”) discloses certain financial measures that are not determined in accordance with U.S. GAAP. The Company principally uses such non-GAAP financial measures in evaluating performance

because the Company believes that such measures, when reviewed in conjunction with relevant U.S. GAAP measures, present a clearer picture of our operating performance and assist the Company in the allocation of its resources. The Company believes

that these non-GAAP financial measures provide investors and other third parties with a better understanding of the Company’s results of operations, financial statements and the underlying profitability drivers and trends of the

Company’s businesses by excluding specified items which may not be indicative of the Company’s ongoing operating performance and may fluctuate significantly from period to period. These measures should be considered supplementary to the

Company’s financial results that are presented in accordance with U.S. GAAP and should not be viewed as a substitute for U.S. GAAP measures. Other companies may use similarly titled non-GAAP financial measures that are calculated differently

from the way the Company calculates such measures. Consequently, the Company’s non-GAAP financial measures may not be comparable to similar measures used by other companies. The following non-GAAP financial measures are used in this document

or in other public disclosures made by the Company from time to time: 1. Adjusted operating income, on a pre-tax and after-tax basis, and adjusted operating income per diluted share. The Company uses these measures as a basis for analyzing financial

results because the Company believes that such measures better reflect the ongoing profitability and underlying trends of the Company’s continuing operations. Adjusted operating income is calculated as net income available to the

Company’s shareholders (or, in the case of pre-tax adjusted operating income, income before income taxes) excluding, as applicable: • substantially all of the effect of net investment related gains and losses; • changes in the fair

value of certain embedded derivatives; • changes in the fair value of contracts that provide market risk benefits; • non-economic losses at contract inception for direct pension risk transfer single premium business (which are amortized

into adjusted operating income within claims and other policy benefits over the estimated lives of the contracts); • any net gain or loss from discontinued operations; • the cumulative effect of any accounting changes; • the impact

of certain tax-related items; and • any other items that the Company believes are not indicative of the Company’s ongoing operations as such items can be volatile and may not reflect the underlying performance of the Company’s

business. In addition, adjusted operating income per diluted share is calculated as adjusted operating income divided by weighted average diluted shares outstanding. These measures also serve as a basis for establishing target levels and awards

under the Company’s management incentive programs. 2. Adjusted operating income (on a pre-tax and after-tax basis), excluding notable items. Notable items are items the Company believes may not be indicative of its ongoing operating

performance which are excluded from adjusted operating income to provide investors and other third parties with a better understanding of the Company’s results. Such items may be unexpected, unknown when the Company prepares its business plan

or otherwise. Notable items presented may include the financial impact of the Company’s assumption reviews on business subject to the Financial Accounting Standards Board’s Accounting Standards Update No. 2018-12, “Targeted

Improvements to the Accounting for Long-Duration Contracts” and related amendments, reflected in future policy benefits remeasurement gains or losses. 3. Adjusted operating revenue. This measure excludes the effects of net realized capital

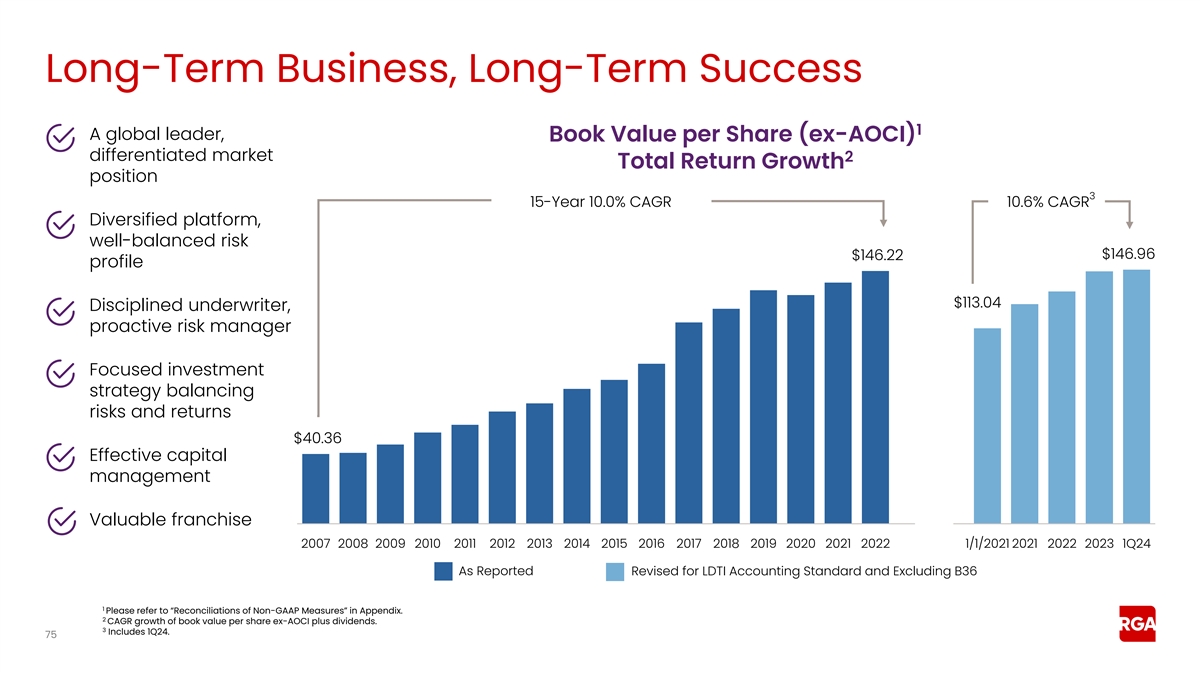

gains and losses, and changes in the fair value of certain embedded derivatives. 4. Shareholders’ equity position excluding the impact of accumulated other comprehensive income (loss) (“AOCI”), shareholders’ average equity

position excluding AOCI, and book value per share excluding the impact of AOCI. The Company believes that these measures provide useful information since such measures exclude AOCI-related items that are not permanent and can fluctuate significantly

from period to period, and may not reflect the impact of the underlying performance of the Company’s businesses on shareholders’ equity and book value per share. AOCI primarily relates to changes in interest rates, credit spreads on its

investment securities, future policy benefits discount rate measurement gains (losses), market risk benefits instrument-specific credit risk remeasurement gains (losses) and foreign currency fluctuations. The Company also discloses the following

non-GAAP financial measures: • Shareholders’ average equity position excluding AOCI and B36, where B36 refers to the cumulative change in fair value of funds withheld embedded derivatives; • Shareholders’ average equity

position excluding AOCI and notable items; and • Shareholders’ average equity position excluding AOCI, B36 and notable items. 5. Adjusted operating return on equity. This measure is calculated as adjusted operating income divided by

average shareholders’ equity excluding AOCI. Adjusted operating return on equity also serves as a basis for establishing target levels and awards under the Company’s management incentive programs. The Company also discloses the following

non-GAAP financial measures: • Adjusted operating return on equity excluding AOCI and B36; • Adjusted operating return on equity excluding AOCI and notable items, which is calculated as adjusted operating income excluding notable items

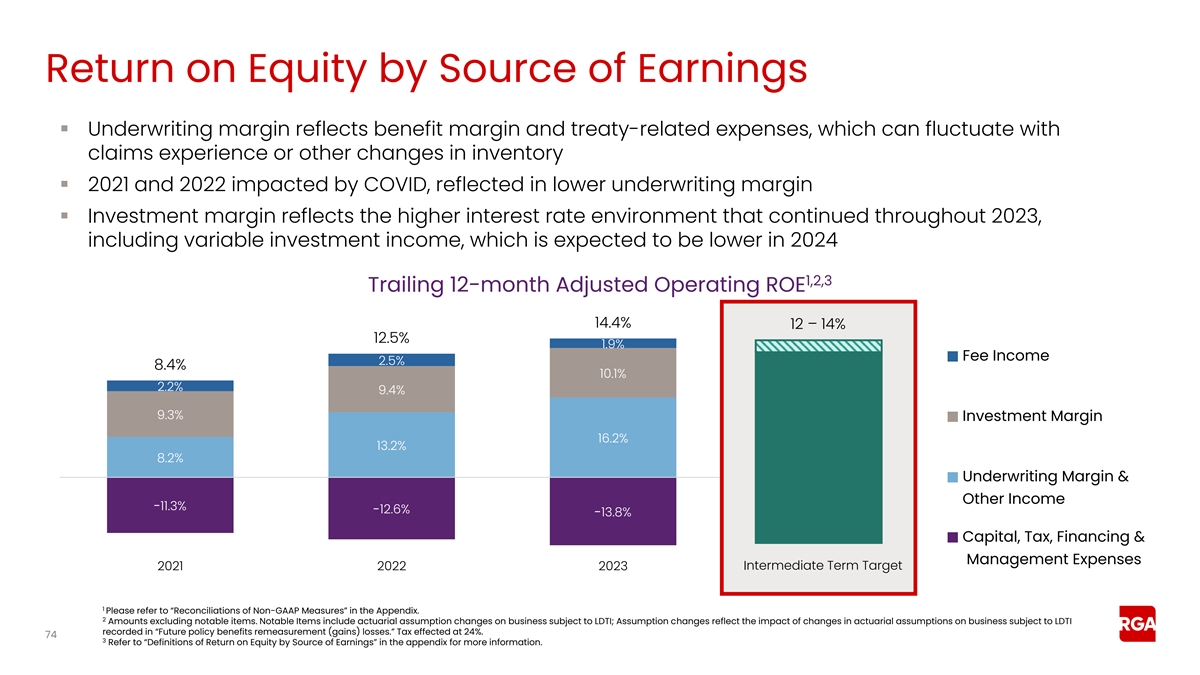

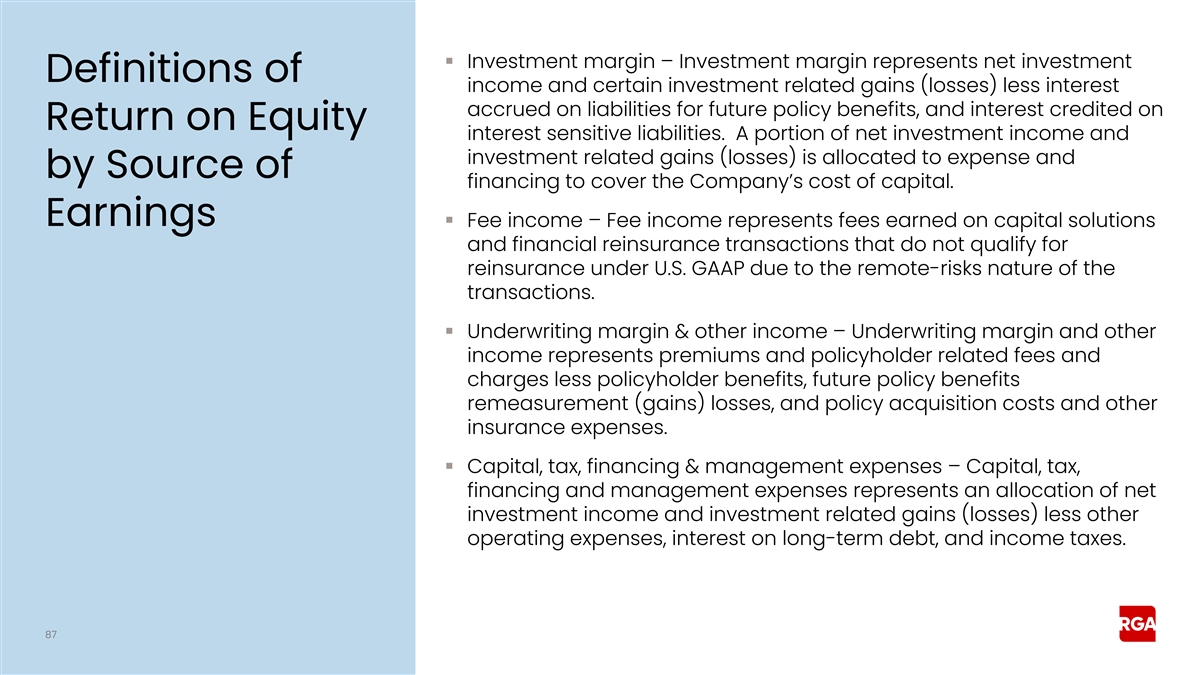

divided by average shareholders’ equity excluding notable items and AOCI; and • Adjusted operating return on equity excluding AOCI, B36 and notable items. 6. Adjusted operating return on equity by sources of earnings . These measure are

calculated utilizing adjusted operating income for each source of earnings divided by average shareholders’ equity excluding AOCI. The Company discloses the return on equity for the following earnings categories: • Investment margin

– Investment margin represents net investment income and certain investment related gains (losses) less interest accrued on liabilities for future policy benefits, and interest credited on interest sensitive liabilities. A portion of net

investment income and investment related gains (losses) is allocated to expense and financing to cover the Company’s cost of capital. • Fee income – Fee income represents fees earned on capital solutions and financial reinsurance

transactions that do not qualify for reinsurance under U.S. GAAP due to the remote-risks nature of the transactions. • Underwriting margin & other income – Underwriting margin and other income represents premiums and policyholder

related fees and charges less policyholder benefits, future policy benefits remeasurement (gains) losses, and policy acquisition costs and other insurance expenses. • Capital, tax, financing & management expenses – Capital, tax,

financing and management expenses represents an allocation of net investment income and investment related gains (losses) less other operating expenses, interest on long-term debt, and income taxes. Reconciliations of the foregoing non-GAAP

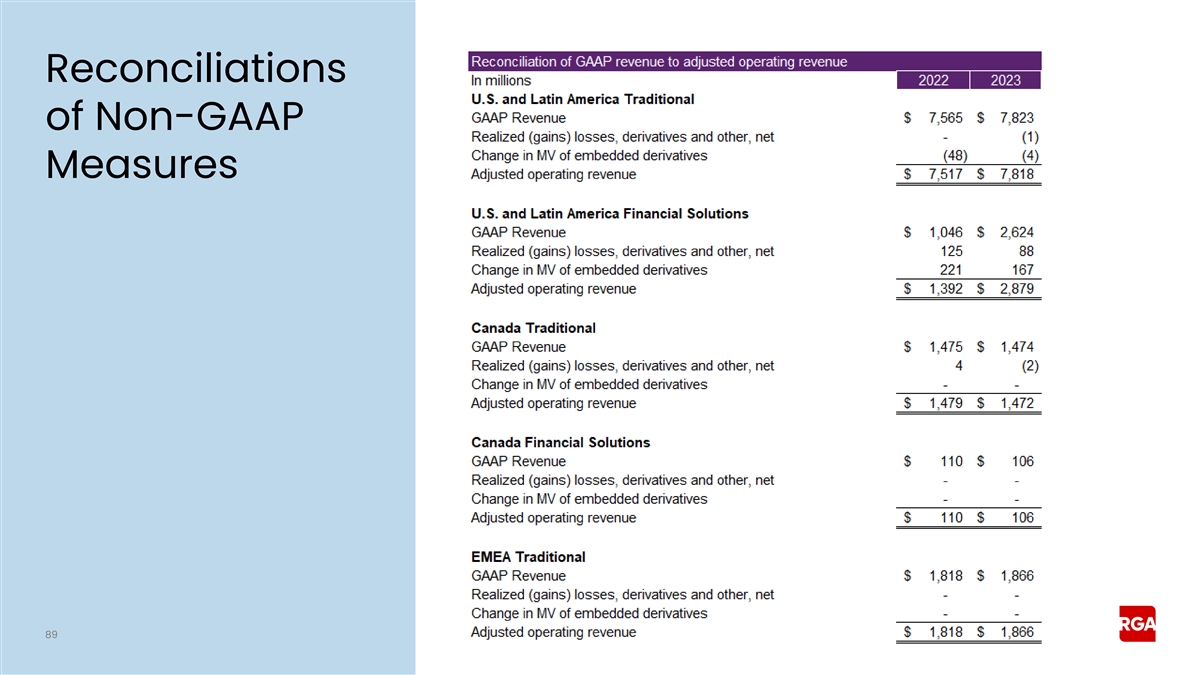

financial measures (to the extent disclosed in this document) to the most comparable GAAP financial measures are provided in the Appendix at the end of this document. 12

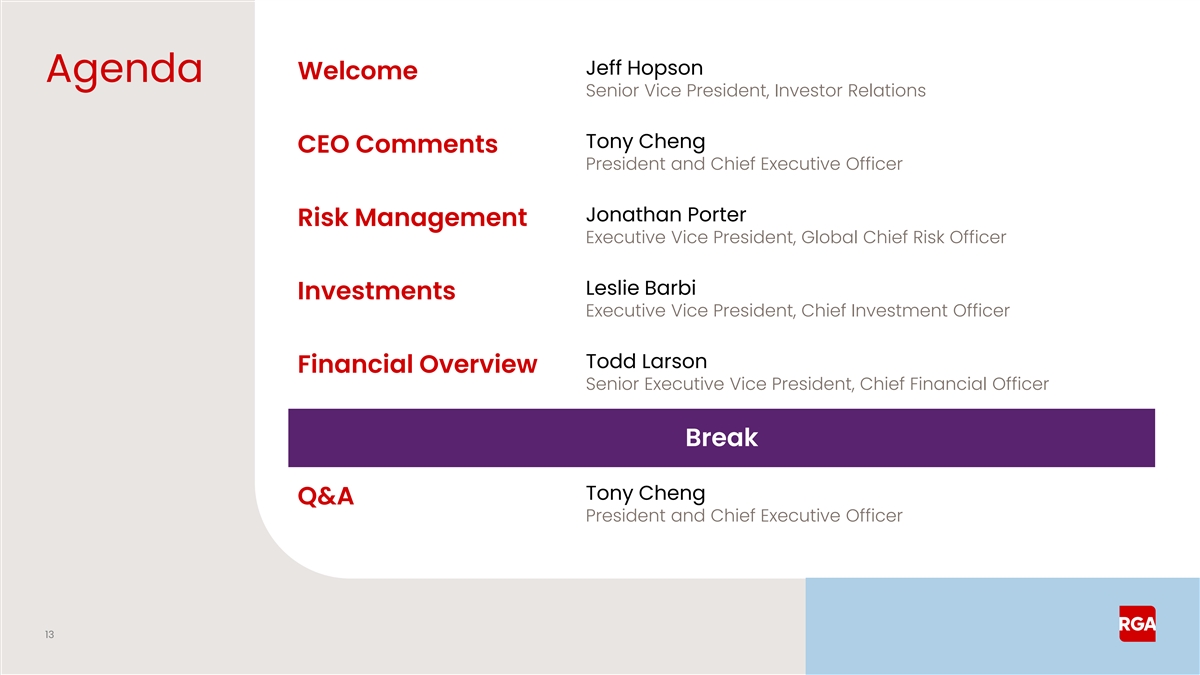

Jeff Hopson Welcome Agenda Senior Vice President, Investor Relations

Tony Cheng CEO Comments President and Chief Executive Officer Jonathan Porter Risk Management Executive Vice President, Global Chief Risk Officer Leslie Barbi Investments Executive Vice President, Chief Investment Officer Todd Larson Financial

Overview Senior Executive Vice President, Chief Financial Officer Break Tony Cheng Q&A President and Chief Executive Officer 13

CEO Comments Tony Cheng President and Chief Executive Officer

14

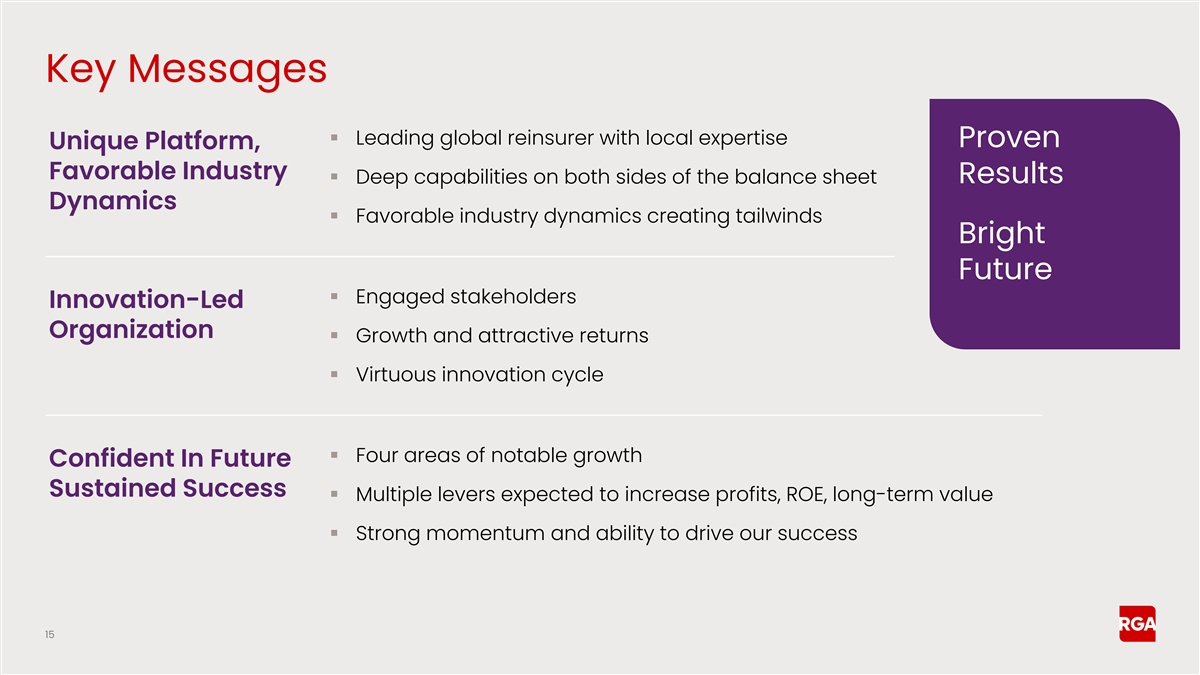

Key Messages ▪ Leading global reinsurer with local expertise

Proven Unique Platform, Favorable Industry ▪ Deep capabilities on both sides of the balance sheet Results Dynamics ▪ Favorable industry dynamics creating tailwinds Bright Future ▪ Engaged stakeholders Innovation-Led Organization

▪ Growth and attractive returns ▪ Virtuous innovation cycle ▪ Four areas of notable growth Confident In Future Sustained Success ▪ Multiple levers expected to increase profits, ROE, long-term value ▪ Strong momentum and

ability to drive our success 15

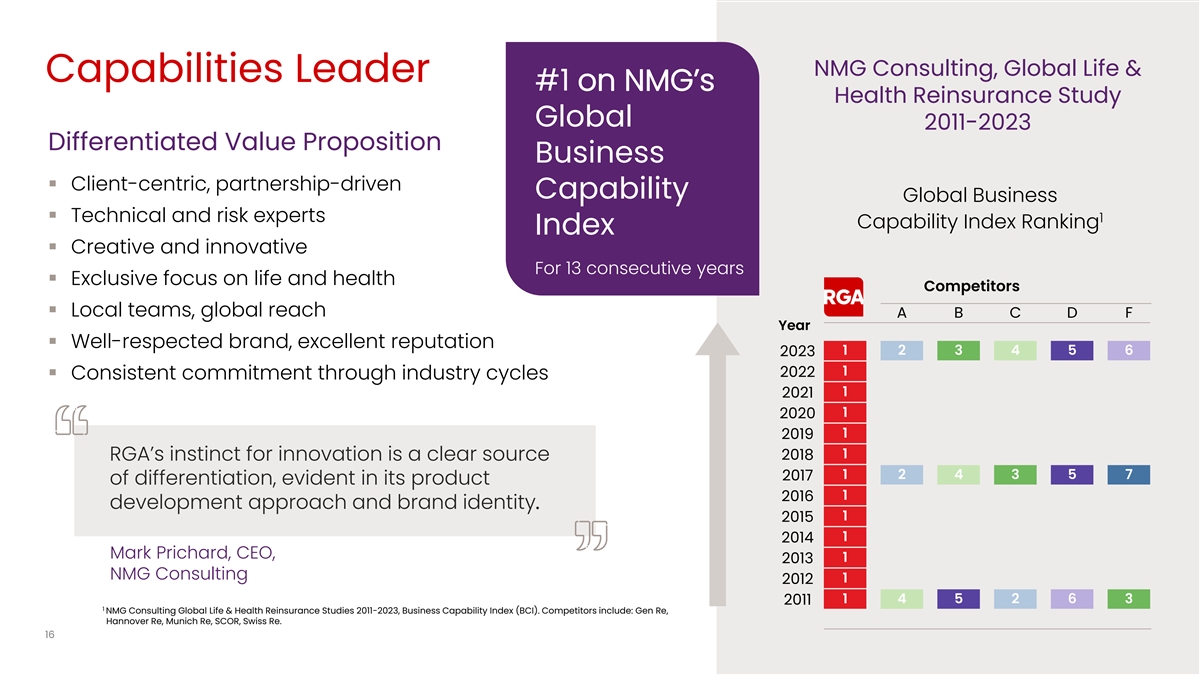

NMG Consulting, Global Life & Capabilities Leader #1 on NMG’s

Health Reinsurance Study Global 2011-2023 Differentiated Value Proposition Business ▪ Client-centric, partnership-driven Capability Global Business ▪ Technical and risk experts 1 Capability Index Ranking Index ▪ Creative and

innovative For 13 consecutive years ▪ Exclusive focus on life and health Competitors ▪ Local teams, global reach A B C D F Year ▪ Well-respected brand, excellent reputation 1 2 3 4 5 6 2023 1 2022 ▪ Consistent commitment

through industry cycles 1 2021 1 2020 1 2019 1 2018 RGA’s instinct for innovation is a clear source 1 2 4 3 5 7 2017 of differentiation, evident in its product 1 2016 development approach and brand identity. 1 2015 1 2014 Mark Prichard, CEO, 1

2013 NMG Consulting 1 2012 1 4 5 2 6 3 2011 1 NMG Consulting Global Life & Health Reinsurance Studies 2011-2023, Business Capability Index (BCI). Competitors include: Gen Re, Hannover Re, Munich Re, SCOR, Swiss Re. 16

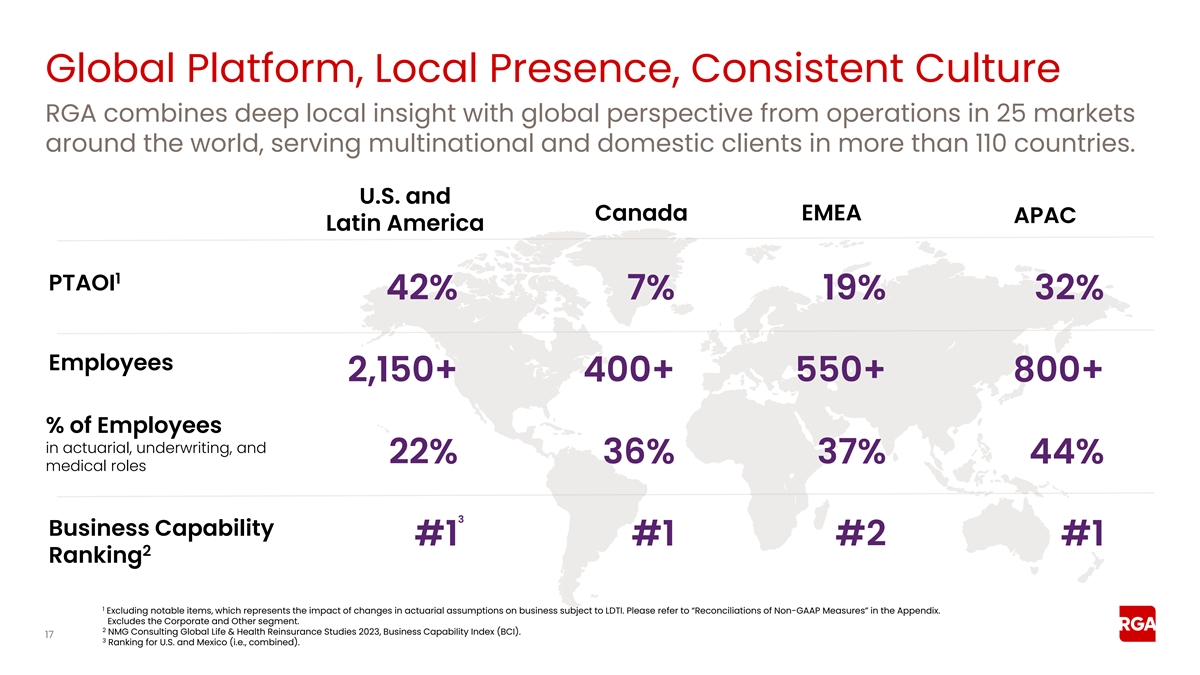

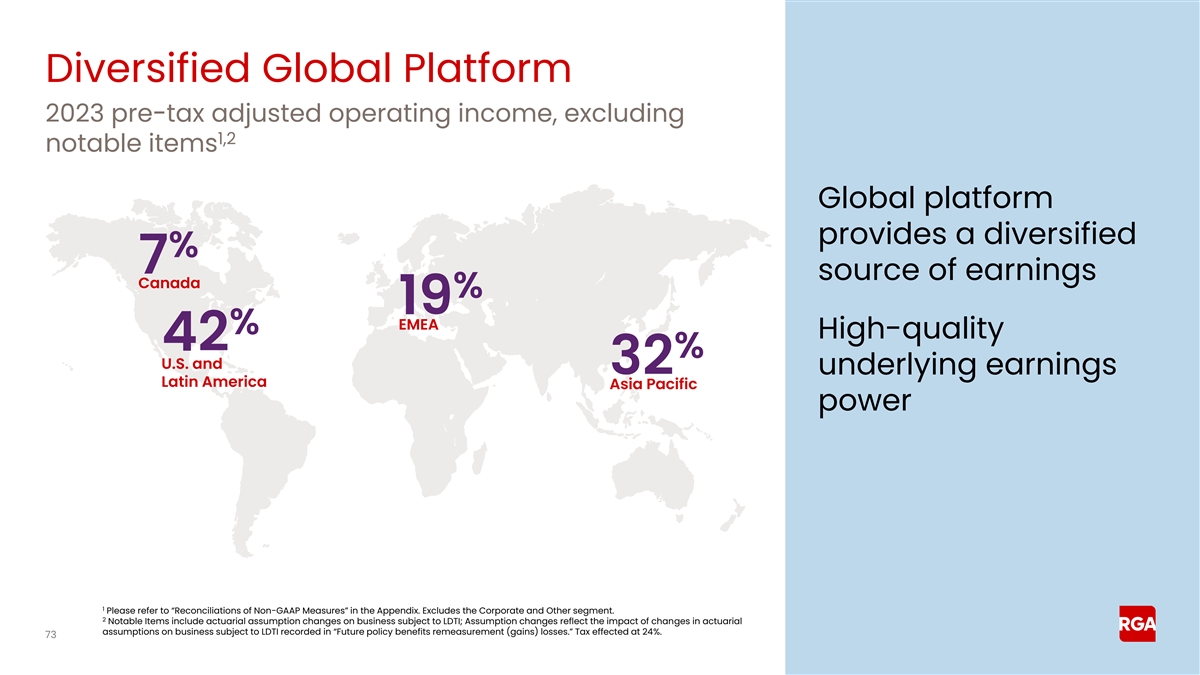

Global Platform, Local Presence, Consistent Culture RGA combines deep

local insight with global perspective from operations in 25 markets around the world, serving multinational and domestic clients in more than 110 countries. U.S. and EMEA Canada APAC Latin America 1 PTAOI 42% 7% 19% 32% Employees 2,150+ 400+ 550+

800+ % of Employees in actuarial, underwriting, and 22% 36% 37% 44% medical roles 3 Business Capability #1 #1 #2 #1 2 Ranking 1 Excluding notable items, which represents the impact of changes in actuarial assumptions on business subject to LDTI.

Please refer to “Reconciliations of Non-GAAP Measures” in the Appendix. Excludes the Corporate and Other segment. 2 NMG Consulting Global Life & Health Reinsurance Studies 2023, Business Capability Index (BCI). 17 3 Ranking for U.S.

and Mexico (i.e., combined).

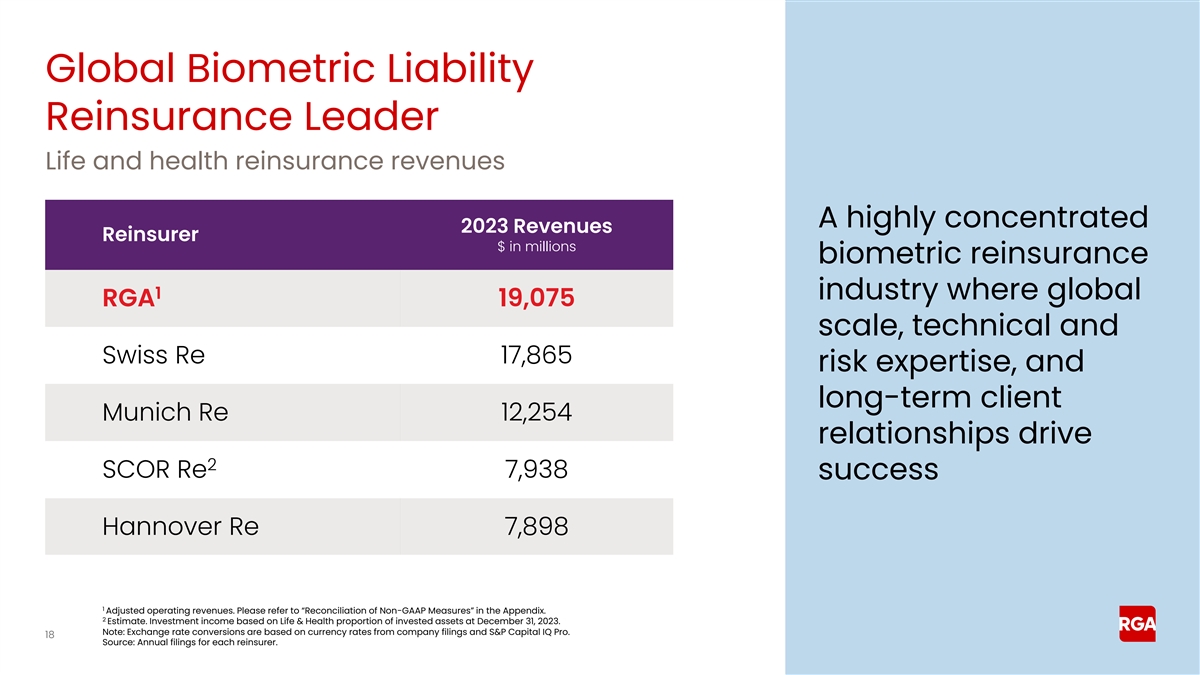

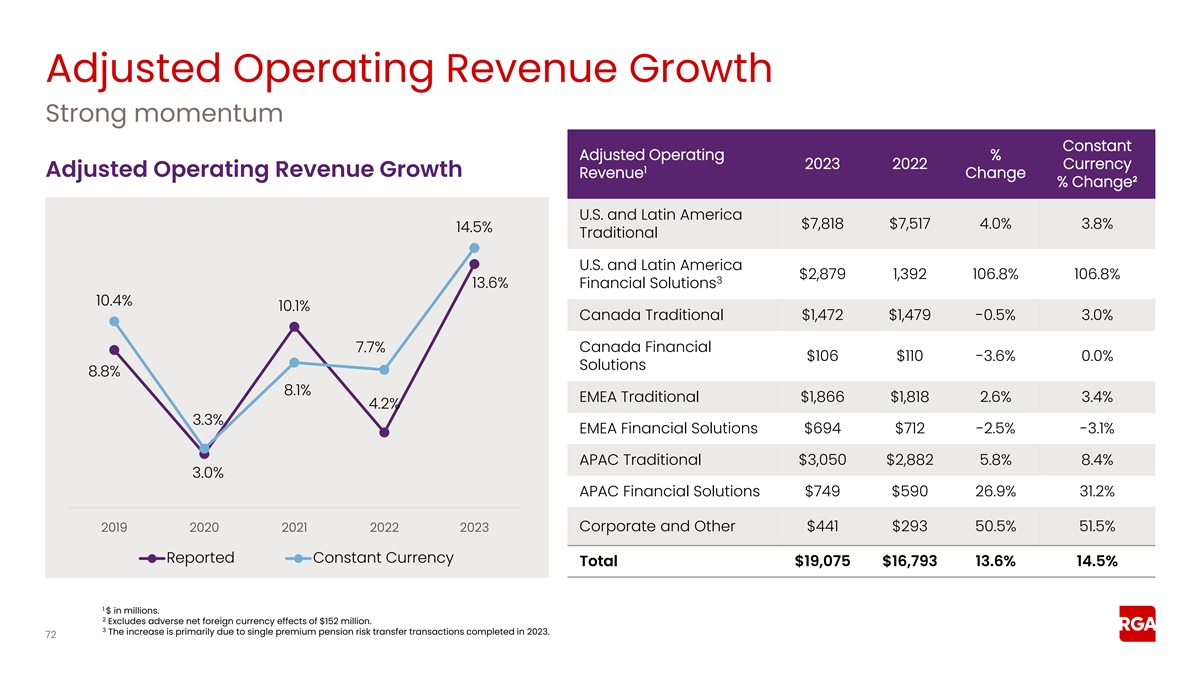

Global Biometric Liability Reinsurance Leader Life and health

reinsurance revenues A highly concentrated 2023 Revenues Reinsurer $ in millions biometric reinsurance 1 industry where global RGA 19,075 scale, technical and Swiss Re 17,865 risk expertise, and long-term client Munich Re 12,254 relationships drive

2 SCOR Re 7,938 success Hannover Re 7,898 1 Adjusted operating revenues. Please refer to “Reconciliation of Non-GAAP Measures” in the Appendix. 2 Estimate. Investment income based on Life & Health proportion of invested assets at

December 31, 2023. Note: Exchange rate conversions are based on currency rates from company filings and S&P Capital IQ Pro. 18 Source: Annual filings for each reinsurer.

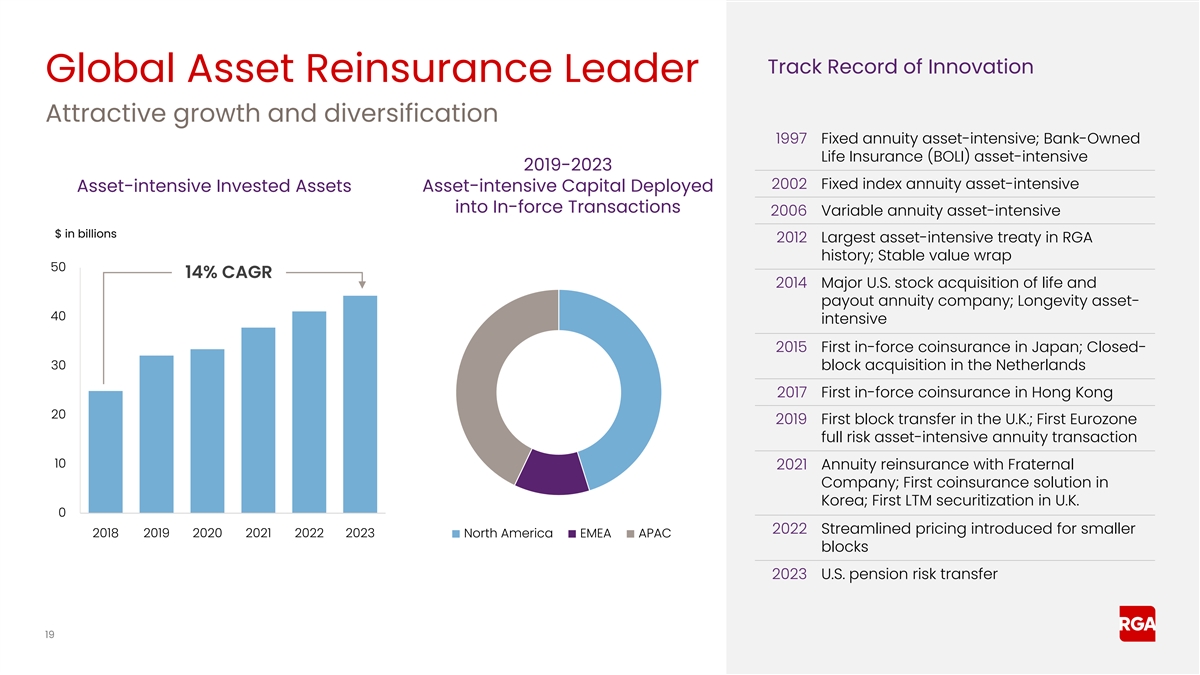

Track Record of Innovation Global Asset Reinsurance Leader Attractive

growth and diversification 1997 Fixed annuity asset-intensive; Bank-Owned Life Insurance (BOLI) asset-intensive 2019-2023 2002 Fixed index annuity asset-intensive Asset-intensive Invested Assets Asset-intensive Capital Deployed into In-force

Transactions 2006 Variable annuity asset-intensive $ in billions 2012 Largest asset-intensive treaty in RGA history; Stable value wrap 50 14% CAGR 2014 Major U.S. stock acquisition of life and payout annuity company; Longevity asset- 40 intensive

2015 First in-force coinsurance in Japan; Closed- 30 block acquisition in the Netherlands 2017 First in-force coinsurance in Hong Kong 20 2019 First block transfer in the U.K.; First Eurozone full risk asset-intensive annuity transaction 10 2021

Annuity reinsurance with Fraternal Company; First coinsurance solution in Korea; First LTM securitization in U.K. 0 2022 Streamlined pricing introduced for smaller 2018 2019 2020 2021 2022 2023 North America EMEA APAC blocks 2023 U.S. pension risk

transfer 19

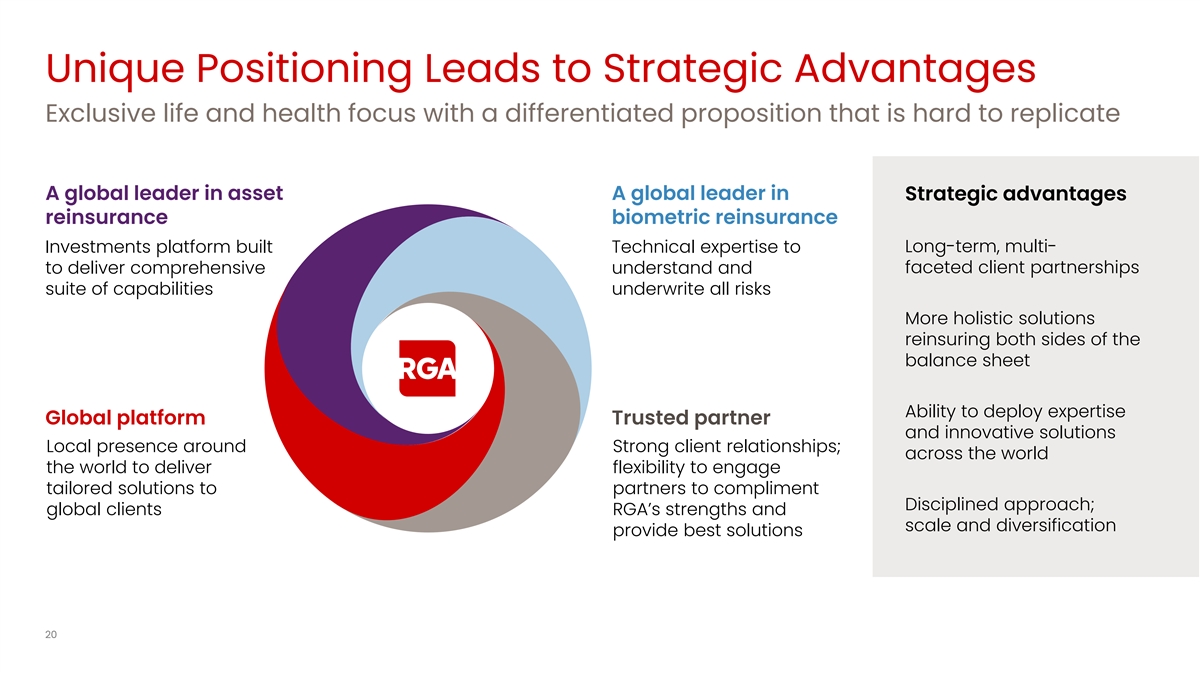

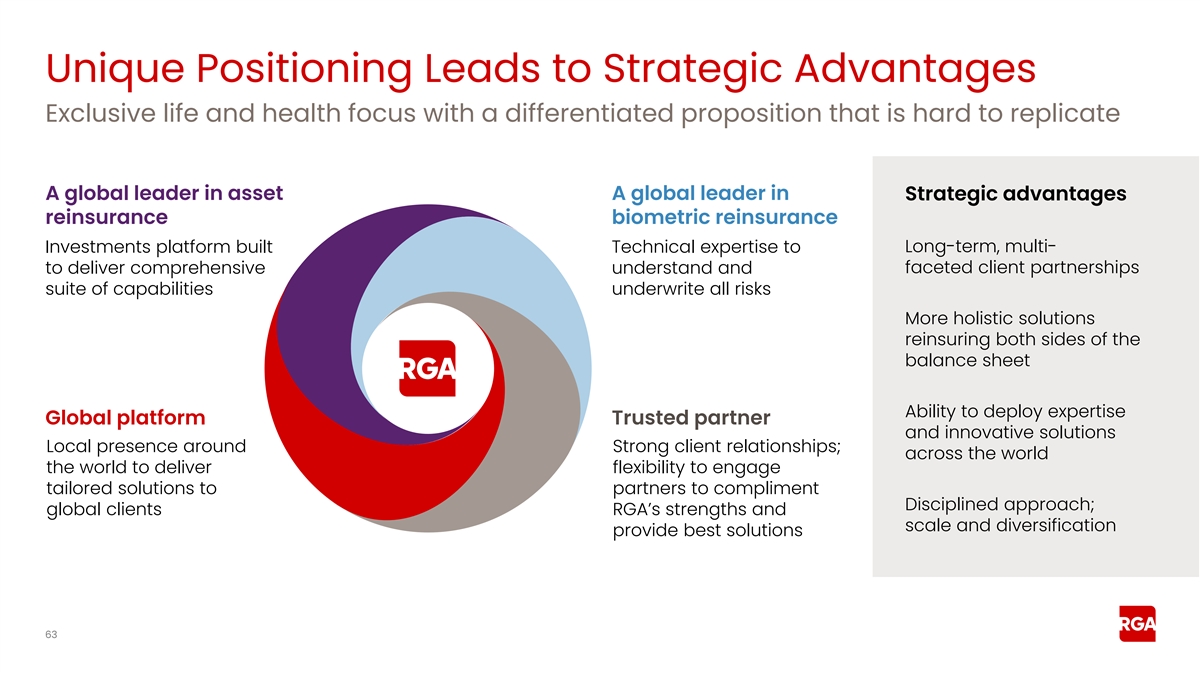

Unique Positioning Leads to Strategic Advantages Exclusive life and

health focus with a differentiated proposition that is hard to replicate A global leader in asset A global leader in Strategic advantages reinsurance biometric reinsurance Investments platform built Technical expertise to Long-term, multi- to

deliver comprehensive understand and faceted client partnerships suite of capabilities underwrite all risks More holistic solutions reinsuring both sides of the balance sheet Ability to deploy expertise Global platform Trusted partner and innovative

solutions Local presence around Strong client relationships; across the world the world to deliver flexibility to engage tailored solutions to partners to compliment Disciplined approach; global clients RGA’s strengths and scale and

diversification provide best solutions 20

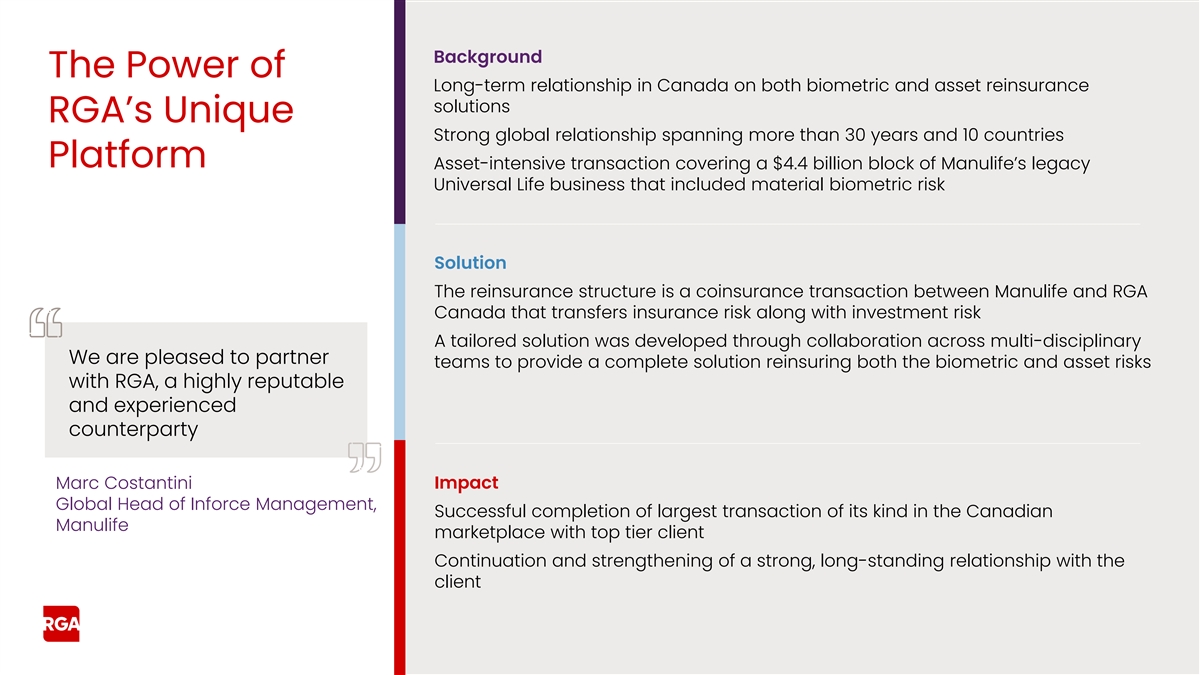

Background The Power of Long-term relationship in Canada on both

biometric and asset reinsurance solutions RGA’s Unique Strong global relationship spanning more than 30 years and 10 countries Platform Asset-intensive transaction covering a $4.4 billion block of Manulife’s legacy Universal Life

business that included material biometric risk Solution The reinsurance structure is a coinsurance transaction between Manulife and RGA Canada that transfers insurance risk along with investment risk A tailored solution was developed through

collaboration across multi-disciplinary We are pleased to partner teams to provide a complete solution reinsuring both the biometric and asset risks with RGA, a highly reputable and experienced counterparty Marc Costantini Impact Global Head of

Inforce Management, Successful completion of largest transaction of its kind in the Canadian Manulife marketplace with top tier client Continuation and strengthening of a strong, long-standing relationship with the client

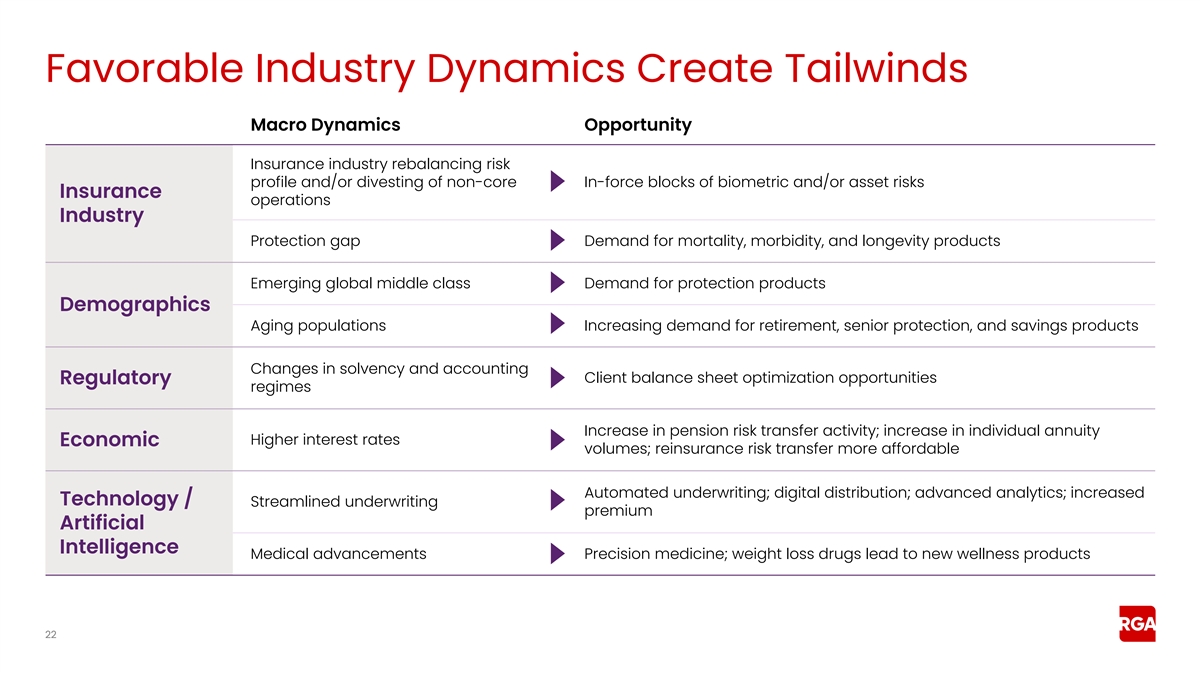

Favorable Industry Dynamics Create Tailwinds Macro Dynamics Opportunity

Insurance industry rebalancing risk profile and/or divesting of non-core In-force blocks of biometric and/or asset risks Insurance operations Industry Protection gap Demand for mortality, morbidity, and longevity products Emerging global middle

class Demand for protection products Demographics Aging populations Increasing demand for retirement, senior protection, and savings products Changes in solvency and accounting Client balance sheet optimization opportunities Regulatory regimes

Increase in pension risk transfer activity; increase in individual annuity Higher interest rates Economic volumes; reinsurance risk transfer more affordable Automated underwriting; digital distribution; advanced analytics; increased Technology /

Streamlined underwriting premium Artificial Intelligence Medical advancements Precision medicine; weight loss drugs lead to new wellness products 22

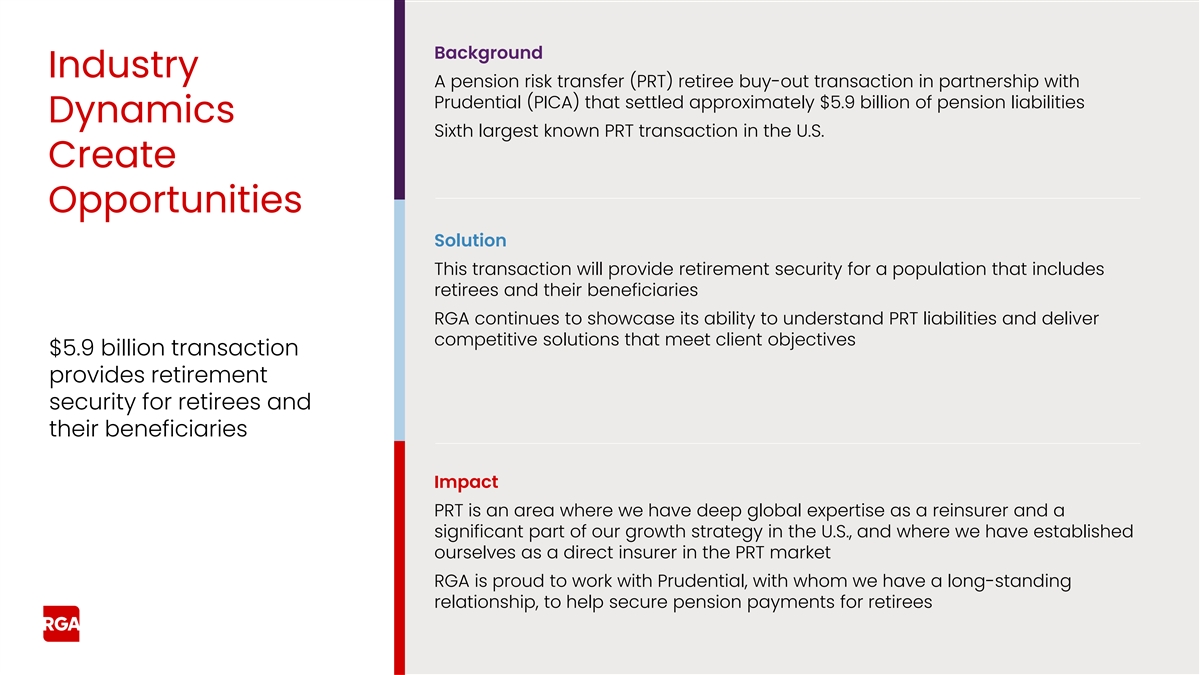

Background Industry A pension risk transfer (PRT) retiree buy-out

transaction in partnership with Prudential (PICA) that settled approximately $5.9 billion of pension liabilities Dynamics Sixth largest known PRT transaction in the U.S. Create Opportunities Solution This transaction will provide retirement security

for a population that includes retirees and their beneficiaries RGA continues to showcase its ability to understand PRT liabilities and deliver competitive solutions that meet client objectives $5.9 billion transaction provides retirement security

for retirees and their beneficiaries Impact PRT is an area where we have deep global expertise as a reinsurer and a significant part of our growth strategy in the U.S., and where we have established ourselves as a direct insurer in the PRT market

RGA is proud to work with Prudential, with whom we have a long-standing relationship, to help secure pension payments for retirees

Innovation-Led Organization Capability-driven, market-first products

and innovations 2010-2014 2015-2019 2020-2024 ▪ Rx scoring tool in the U.S.▪ First longevity transaction including an ▪ Award-winning CI product for seniors in Spain underlying pension ▪ First in-force longevity transaction

in Canada▪ Cancer survivor coverage in Singapore plan in Canada ▪ Comprehensive early critical illness (CI) in ▪ ASAP Infinity, an expansion of our first-in-class instant ▪ Just-in-time capital solution in Asia Singapore

decision facultative tool in the U.S. ▪ Diabetic-focused wellness program in ▪ Early CI product in Indonesia▪ Guaranteed issue funeral cover in South Africa Hong Kong ▪ Scaled simplified issue (SI) product in Korea▪

First coinsurance solution in Korea ▪ First-in-class accelerated underwriting ▪ Cancer reimbursement product in Hong Kong▪ Plan V Care, a protection product for female program in the U.S. millennials in the U.K. ▪ First

longevity shock absorber in the ▪ Dynamic risk scoring model in India Netherlands▪ First SI CI in China ▪ Insurance product for rapid test of ▪ First cancer product targeted to the senior market in HIV/cholesterol in South

Africa Taiwan ▪ Premium waiver product in Asia ▪ FAC Exchange, an industry-wide solution providing a ▪ Tiered CI product in Asia conduit and integration platform for facultative ▪ First SI dementia product offering a family

reinsurance submission in the U.S. care feature in Korea ▪ First asset-intensive transaction in Continental Europe X for RGA ` ▪ First-in-market major SI medical reimbursement product in China ▪ First mass lapse reinsurance

transaction in France 24

Engaged Local and Global Teams An engaged workforce drives

World’s Most Admired Companies collaboration RGA was named to the 2024 Fortune World’s Most Admired and Companies list based on criteria including the company’s innovation value as a long-term investment, quality of management,

innovativeness, community responsibility, and the ability to attract and retain talent. 2023 2023 engagement voluntary 5.2% 86% score turnover rate Outperformed industry Low voluntary turnover rate; benchmarks for the top 25% of favorable to

industry norms high-performing companies, regardless of industry 25

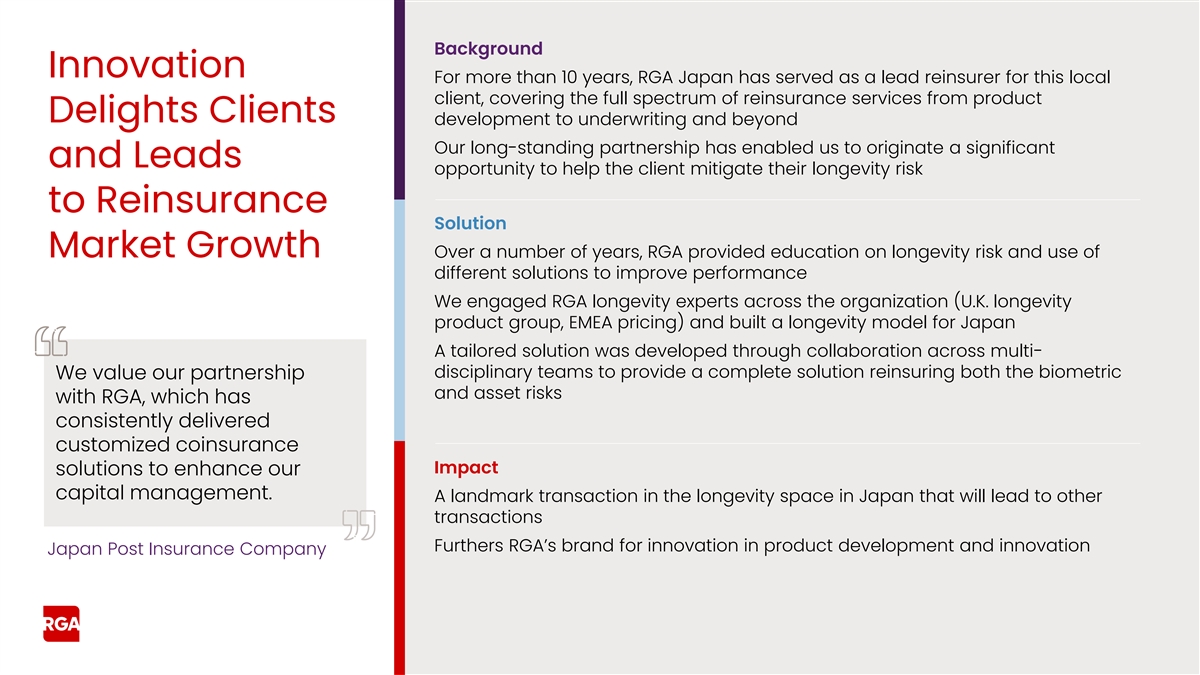

Background Innovation For more than 10 years, RGA Japan has served as a

lead reinsurer for this local client, covering the full spectrum of reinsurance services from product Delights Clients development to underwriting and beyond Our long-standing partnership has enabled us to originate a significant and Leads

opportunity to help the client mitigate their longevity risk to Reinsurance Solution Market Growth Over a number of years, RGA provided education on longevity risk and use of different solutions to improve performance We engaged RGA longevity

experts across the organization (U.K. longevity product group, EMEA pricing) and built a longevity model for Japan A tailored solution was developed through collaboration across multi- disciplinary teams to provide a complete solution reinsuring

both the biometric We value our partnership and asset risks with RGA, which has consistently delivered customized coinsurance Impact solutions to enhance our capital management. A landmark transaction in the longevity space in Japan that will lead

to other transactions Furthers RGA’s brand for innovation in product development and innovation Japan Post Insurance Company

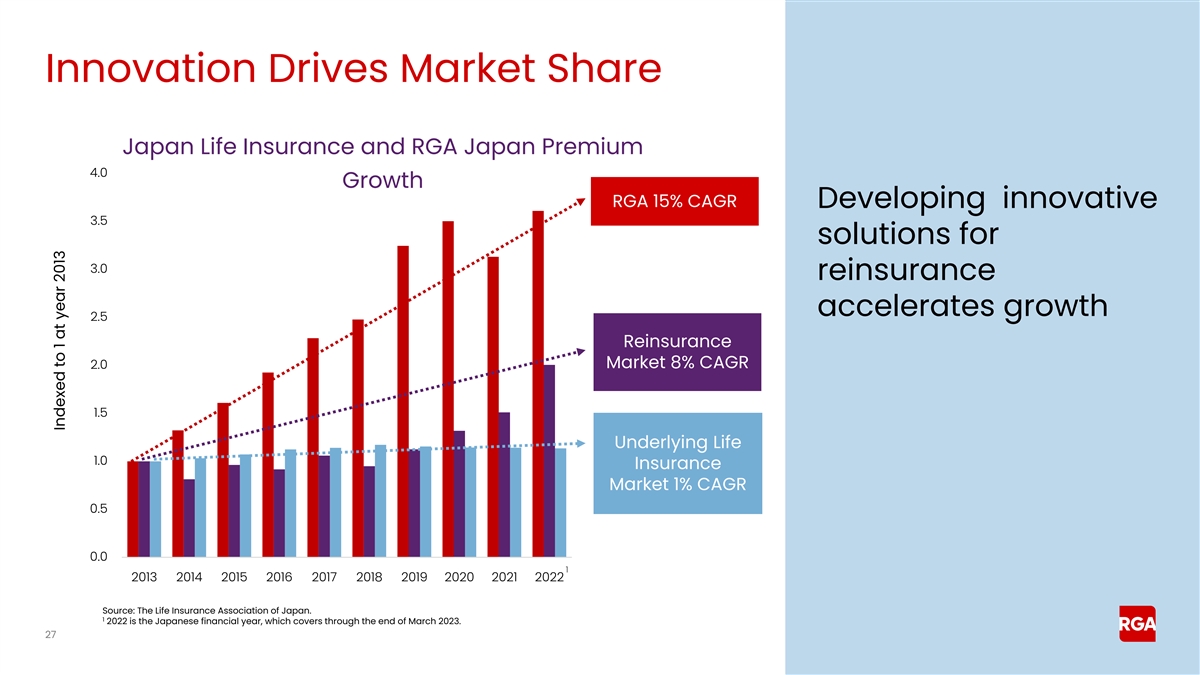

Innovation Drives Market Share Japan Life Insurance and RGA Japan

Premium 4.0 Growth RGA 15% CAGR Developing innovative 3.5 solutions for 3.0 reinsurance accelerates growth 2.5 Reinsurance 2.0 Market 8% CAGR 1.5 Underlying Life 1.0 Insurance Market 1% CAGR 0.5 0.0 1 2013 2014 2015 2016 2017 2018 2019 2020 2021

2022 Source: The Life Insurance Association of Japan. 1 2022 is the Japanese financial year, which covers through the end of March 2023. 27 Indexed to 1 at year 2013

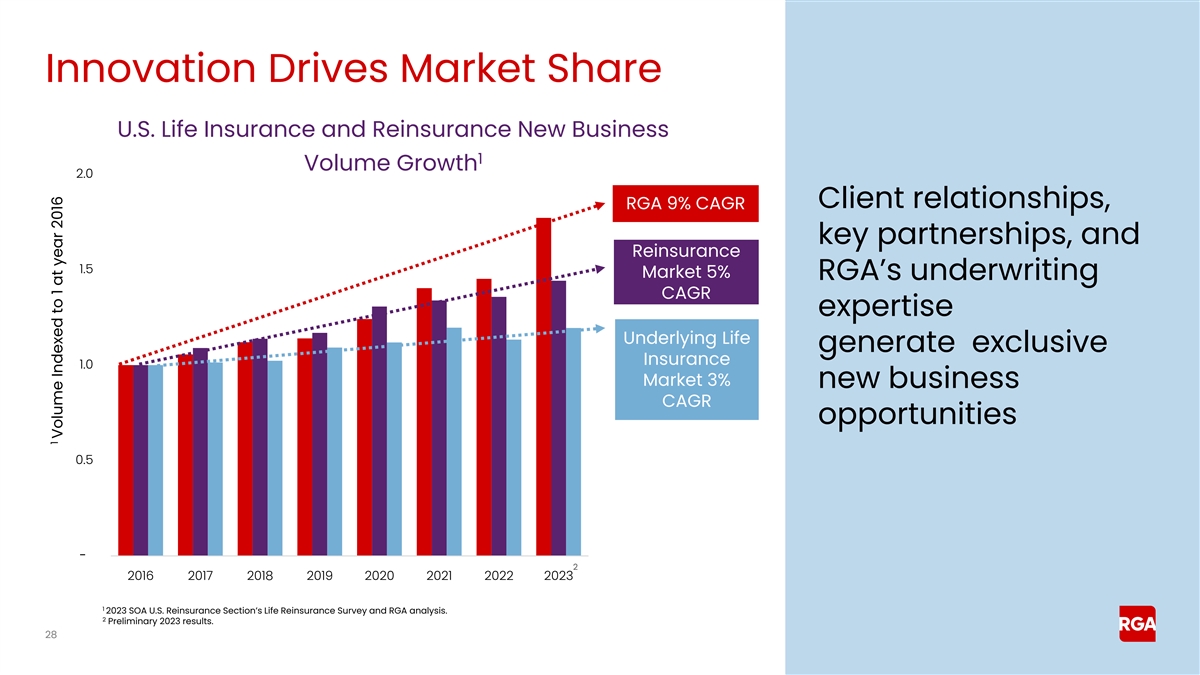

Innovation Drives Market Share U.S. Life Insurance and Reinsurance New

Business 1 Volume Growth 2.0 Client relationships, RGA 9% CAGR key partnerships, and Reinsurance 1.5 Market 5% RGA’s underwriting CAGR expertise Underlying Life generate exclusive Insurance 1.0 Market 3% new business CAGR opportunities 0.5 - 2

2016 2017 2018 2019 2020 2021 2022 2023 1 2023 SOA U.S. Reinsurance Section’s Life Reinsurance Survey and RGA analysis. 2 Preliminary 2023 results. 28 1 Volume Indexed to 1 at year 2016

Background Virtuous Previously launched a simplified critical illness

(CI) product in China in late 2022 Innovation Leveraged off data, knowledge, and a product developed in response to the aging population in South Korea five years ago Cycle Solution Conducted an industry seminar sharing practical knowledge and

experience on the underwriting and claims aspects of this product Broadly replicated this product with 11 other Chinese clients Impact Launched a simplified issue medical product in supplement to the original CI product in December 2023 Advanced our

goal of creating an impaired-life business line, rather than just a niche product Strengthened RGA’s team engagement Enhanced RGA’s brand in China and reputation for innovation in product development

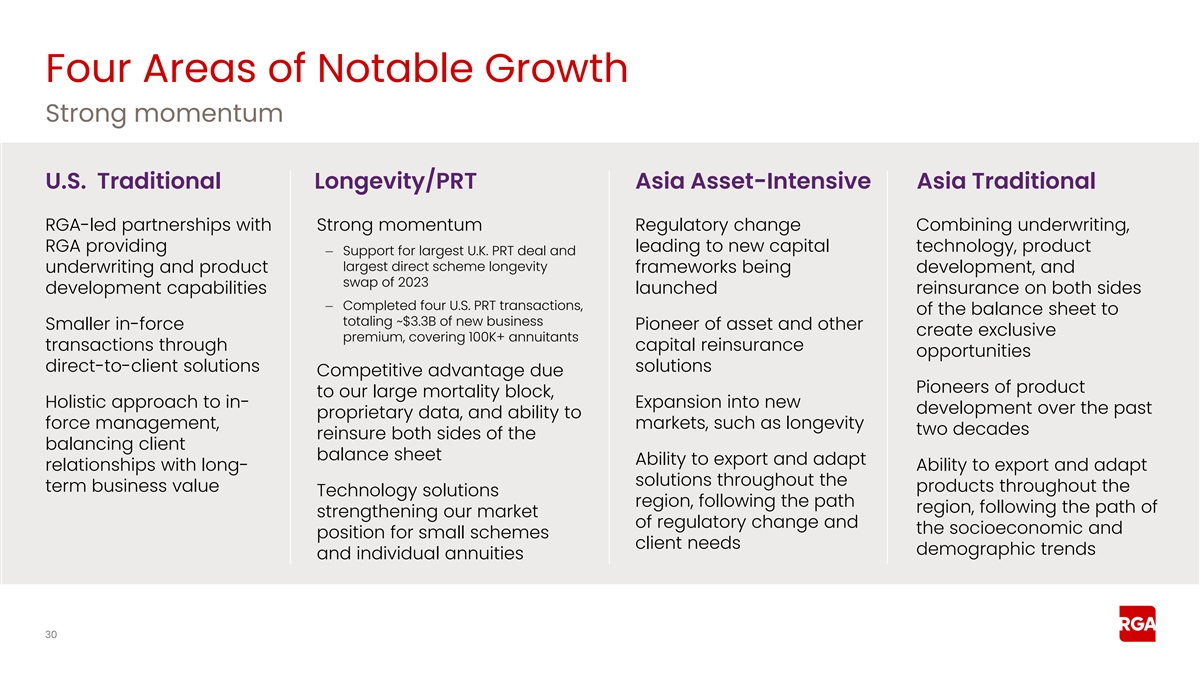

Four Areas of Notable Growth Strong momentum U.S. Traditional

Longevity/PRT Asia Asset-Intensive Asia Traditional RGA-led partnerships with Strong momentum Regulatory change Combining underwriting, RGA providing leading to new capital technology, product – Support for largest U.K. PRT deal and largest

direct scheme longevity underwriting and product frameworks being development, and swap of 2023 development capabilities launched reinsurance on both sides – Completed four U.S. PRT transactions, of the balance sheet to totaling ~$3.3B of new

business Smaller in-force Pioneer of asset and other create exclusive premium, covering 100K+ annuitants transactions through capital reinsurance opportunities direct-to-client solutions solutions Competitive advantage due Pioneers of product to our

large mortality block, Holistic approach to in- Expansion into new development over the past proprietary data, and ability to force management, markets, such as longevity two decades reinsure both sides of the balancing client balance sheet Ability

to export and adapt relationships with long- Ability to export and adapt solutions throughout the term business value products throughout the Technology solutions region, following the path region, following the path of strengthening our market of

regulatory change and the socioeconomic and position for small schemes client needs demographic trends and individual annuities 30

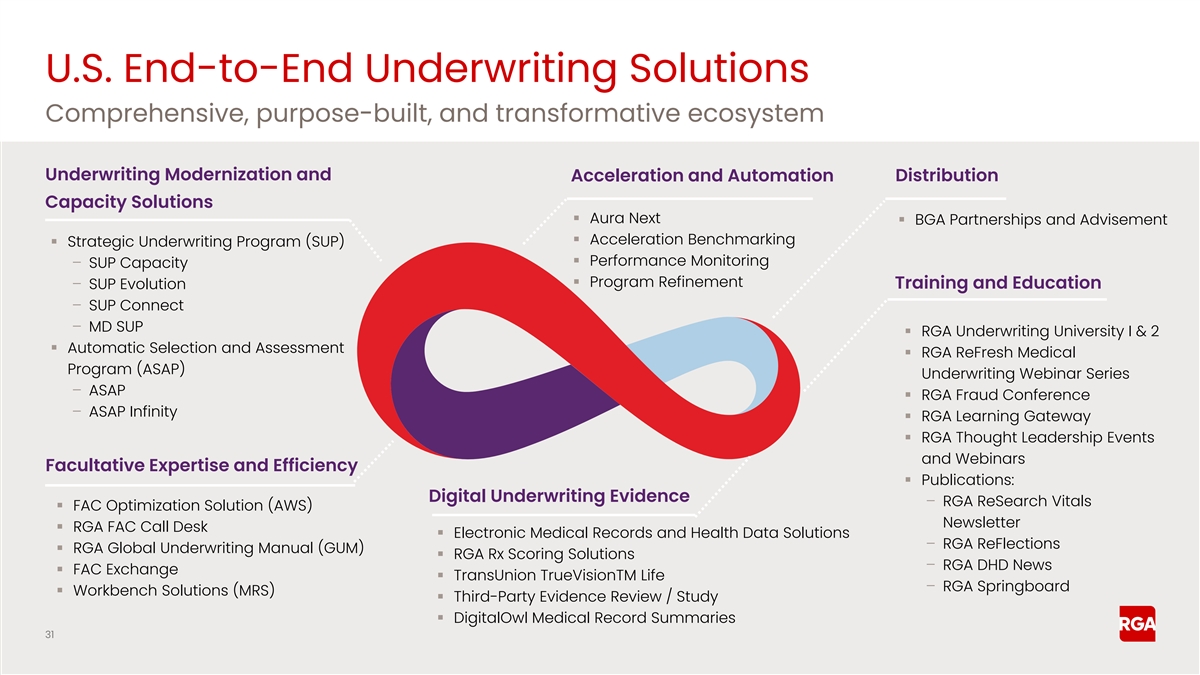

U.S. End-to-End Underwriting Solutions Comprehensive, purpose-built,

and transformative ecosystem Underwriting Modernization and Acceleration and Automation Distribution Capacity Solutions ▪ Aura Next ▪ BGA Partnerships and Advisement ▪ Acceleration Benchmarking ▪ Strategic Underwriting

Program (SUP) ▪ Performance Monitoring – SUP Capacity ▪ Program Refinement – SUP Evolution Training and Education – SUP Connect – MD SUP ▪ RGA Underwriting University I & 2 ▪ Automatic Selection

and Assessment ▪ RGA ReFresh Medical Program (ASAP) Underwriting Webinar Series – ASAP ▪ RGA Fraud Conference – ASAP Infinity ▪ RGA Learning Gateway ▪ RGA Thought Leadership Events and Webinars Facultative

Expertise and Efficiency ▪ Publications: Digital Underwriting Evidence – RGA ReSearch Vitals ▪ FAC Optimization Solution (AWS) Newsletter ▪ RGA FAC Call Desk ▪ Electronic Medical Records and Health Data Solutions

– RGA ReFlections ▪ RGA Global Underwriting Manual (GUM) ▪ RGA Rx Scoring Solutions – RGA DHD News ▪ FAC Exchange ▪ TransUnion TrueVisionTM Life – RGA Springboard ▪ Workbench Solutions (MRS) ▪

Third-Party Evidence Review / Study ▪ DigitalOwl Medical Record Summaries 31

Background RGA-Led A leading distribution insurtech partner and a life

insurance carrier needed a creative solution to help meet the capital requirements of new business on a Partnerships final expense product offering The life insurance carrier slowed their sales of new business due to capital Drive Exclusive

constraints Successes Solution RGA rapidly developed a solution, leveraging our end-to-end underwriting and product development capabilities with a first dollar quota share, coinsurance structure on their new business, and an in-force reinsurance

transaction that provides new business strain for past sales that had not been securitized to fund the distribution partner's growth goals RGA demonstrated strength of underwriting and product Impact development The solution delivered by RGA allowed

the life insurance carrier to regain market capabilities, industry leadership, and the distribution partner to meet their growth goals leading position, and RGA established a new relationship with the life insurance carrier and was able culture of

innovation to generate meaningful annual premiums on an exclusive basis RGA’s ability to move swiftly deepened both relationships and multiple new opportunities have emerged with both the life insurance carrier and the distributor to develop

new underwriting and product capabilities going forward

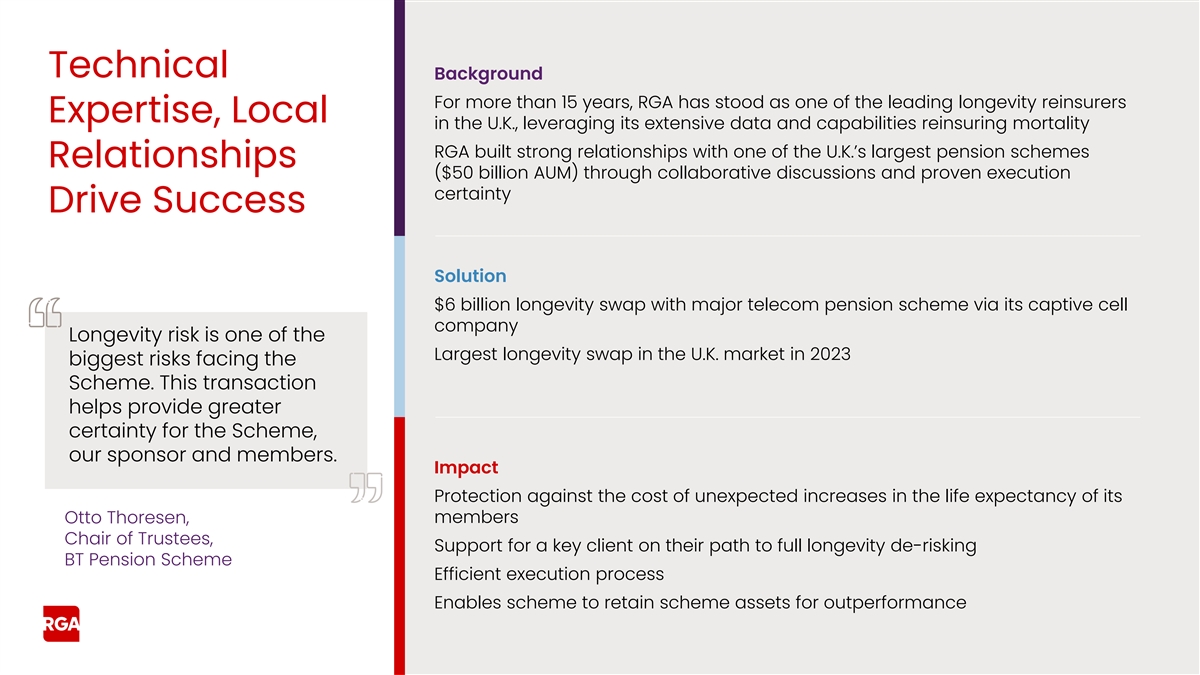

Technical Background For more than 15 years, RGA has stood as one of

the leading longevity reinsurers Expertise, Local in the U.K., leveraging its extensive data and capabilities reinsuring mortality RGA built strong relationships with one of the U.K.’s largest pension schemes Relationships ($50 billion AUM)

through collaborative discussions and proven execution certainty Drive Success Solution $6 billion longevity swap with major telecom pension scheme via its captive cell company Longevity risk is one of the Largest longevity swap in the U.K. market

in 2023 biggest risks facing the Scheme. This transaction helps provide greater certainty for the Scheme, our sponsor and members. Impact Protection against the cost of unexpected increases in the life expectancy of its Otto Thoresen, members Chair

of Trustees, Support for a key client on their path to full longevity de-risking BT Pension Scheme Efficient execution process Enables scheme to retain scheme assets for outperformance

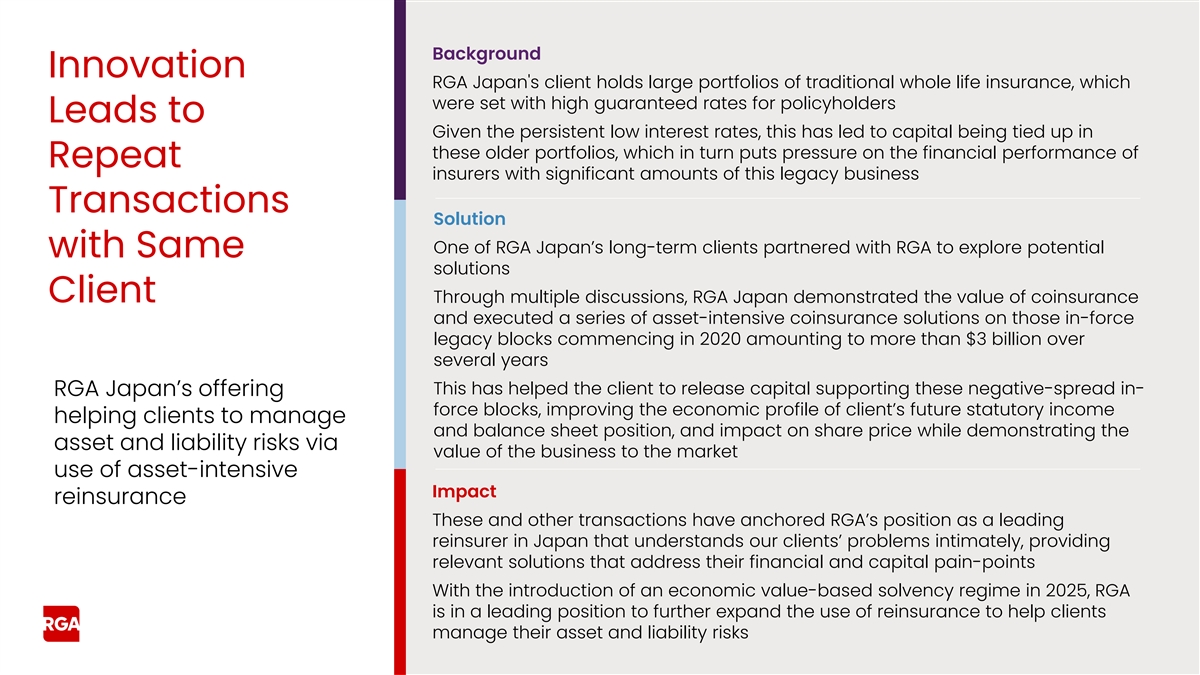

Background Innovation RGA Japan's client holds large portfolios of

traditional whole life insurance, which were set with high guaranteed rates for policyholders Leads to Given the persistent low interest rates, this has led to capital being tied up in these older portfolios, which in turn puts pressure on the

financial performance of Repeat insurers with significant amounts of this legacy business Transactions Solution One of RGA Japan’s long-term clients partnered with RGA to explore potential with Same solutions Client Through multiple

discussions, RGA Japan demonstrated the value of coinsurance and executed a series of asset-intensive coinsurance solutions on those in-force legacy blocks commencing in 2020 amounting to more than $3 billion over several years This has helped the

client to release capital supporting these negative-spread in- RGA Japan’s offering force blocks, improving the economic profile of client’s future statutory income helping clients to manage and balance sheet position, and impact on

share price while demonstrating the asset and liability risks via value of the business to the market use of asset-intensive Impact reinsurance These and other transactions have anchored RGA’s position as a leading reinsurer in Japan that

understands our clients’ problems intimately, providing relevant solutions that address their financial and capital pain-points With the introduction of an economic value-based solvency regime in 2025, RGA is in a leading position to further

expand the use of reinsurance to help clients manage their asset and liability risks

Background RGA Hong Kong has been partnering with this market-leading

client for more Winning than 10 years The client came to us to look for solutions to take advantage of the new business Exclusives by opportunities from Mainland Chinese visitors following the re-opening of borders, and to address capital

constraints under the new risk-based capital (HK RBC) Applying our Full regime Suite of Solution Capabilities Combining our strengths across the value chain, RGA provided: ▪ Product development: new product features leveraging our

understanding of customers and distribution needs ▪ Product and pricing expertise, helping our client enhance the range of RGA combines its protection propositions to customers product development, ▪ A combined asset and biometric

solution to optimize capital requirements underwriting and under HK RBC, coupled with an underwriting and claims technology solution technology solutions, to improve the customer journey of Mainland Chinese visitors and asset and biometric

reinsurance capabilities Impact to extend its strong market leadership Successfully launched a new version of their leading critical illness product with an innovative customer journey Opportunity to replicate this packaged solution to other Hong

Kong carriers and in other RGA markets

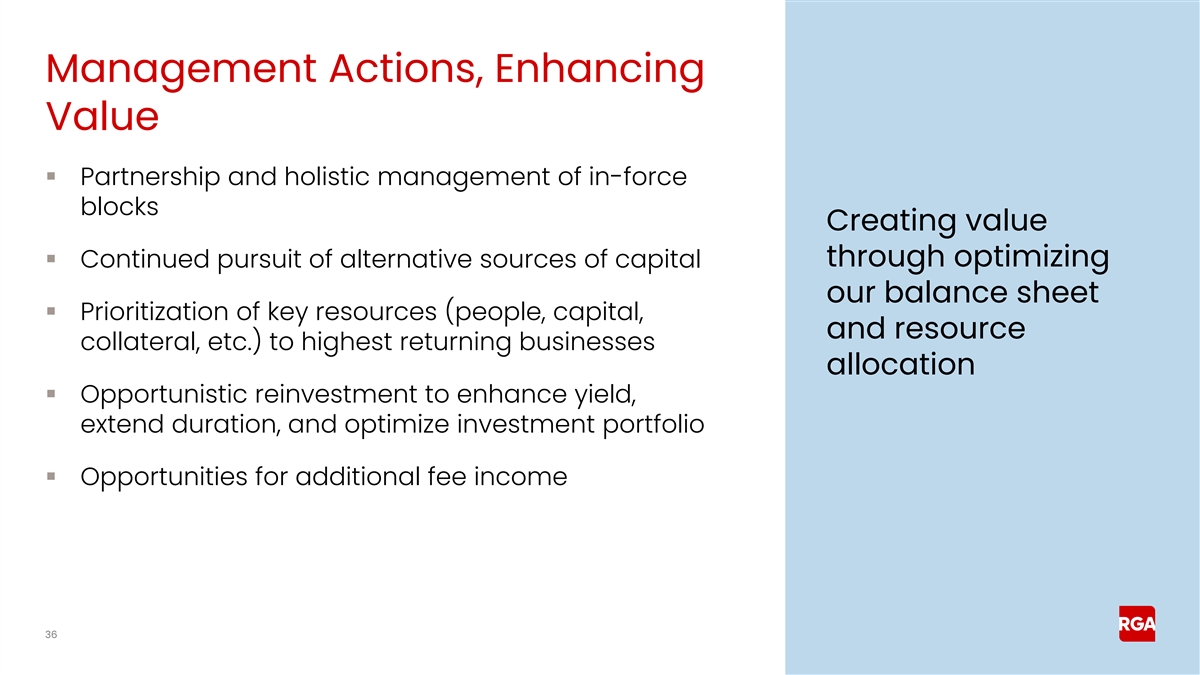

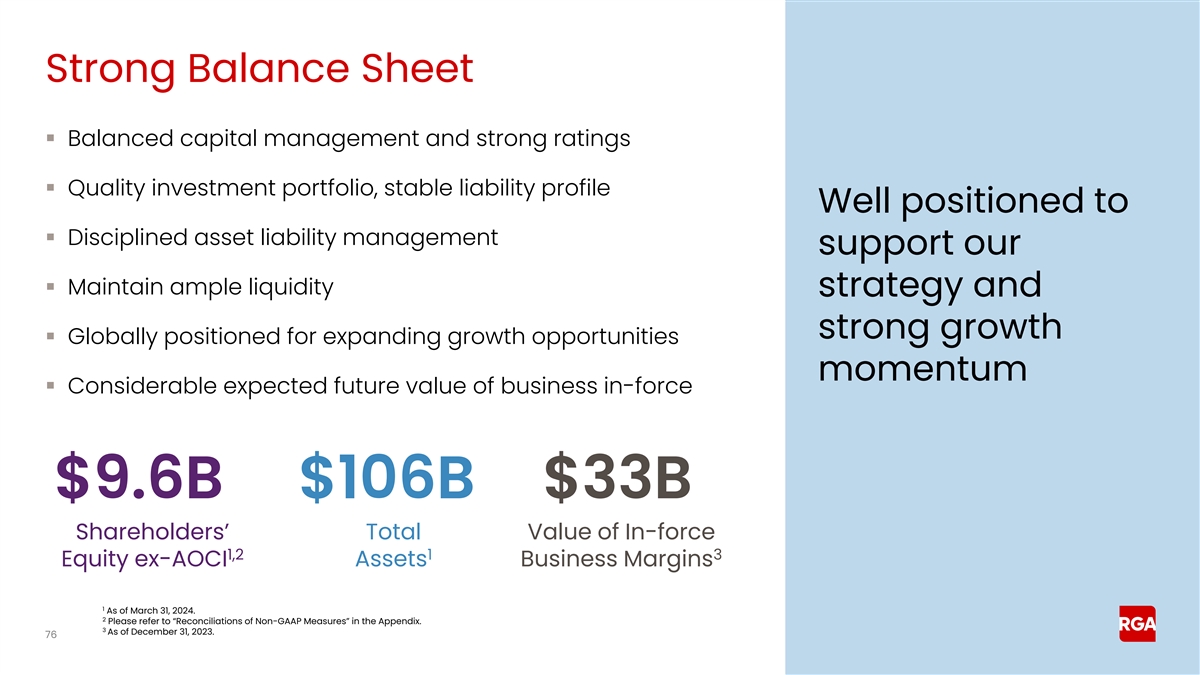

Management Actions, Enhancing Value ▪ Partnership and holistic

management of in-force blocks Creating value through optimizing ▪ Continued pursuit of alternative sources of capital our balance sheet ▪ Prioritization of key resources (people, capital, and resource collateral, etc.) to highest

returning businesses allocation ▪ Opportunistic reinvestment to enhance yield, extend duration, and optimize investment portfolio ▪ Opportunities for additional fee income 36

Multiple Levers Expected to Grow Profit and Increase ROE New Percentage

of Increased Management business new business focus on actions value value from growth areas exclusives Higher earnings Higher ROE Higher earnings Higher earnings power power power and higher ROE 37

Strong Momentum, Sustained Success Unique Favorable Culture of Notable

Multiple levers platform industry innovation growth areas for value dynamics creation Confidence in bright future 38

Our Success is Our People Management Management team's team’s

average average years 24 13 industry with RGA years years experience Recognized for excellence 39

Risk Management Jonathan Porter Executive Vice President, Global Chief

Risk Officer 40

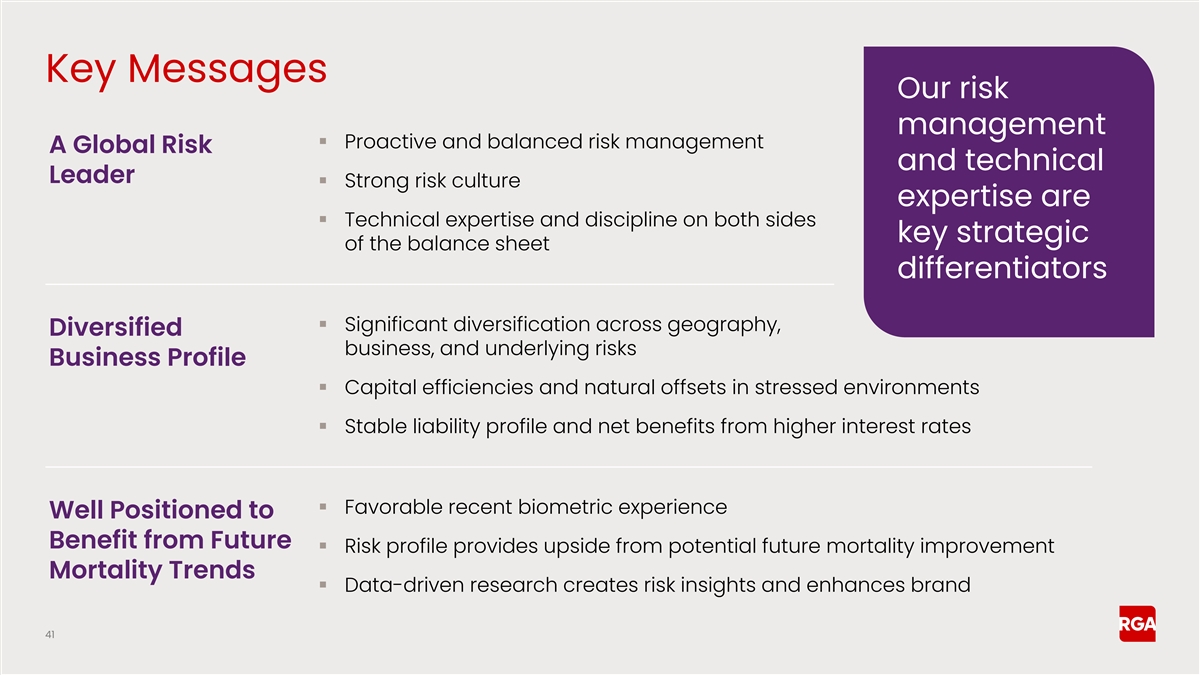

Key Messages Our risk management ▪ Proactive and balanced risk

management A Global Risk and technical Leader ▪ Strong risk culture expertise are ▪ Technical expertise and discipline on both sides key strategic of the balance sheet differentiators ▪ Significant diversification across geography,

Diversified business, and underlying risks Business Profile ▪ Capital efficiencies and natural offsets in stressed environments ▪ Stable liability profile and net benefits from higher interest rates ▪ Favorable recent biometric

experience Well Positioned to Benefit from Future ▪ Risk profile provides upside from potential future mortality improvement Mortality Trends ▪ Data-driven research creates risk insights and enhances brand 41

Proactive and Effective Risk Management ▪ A strong risk culture

underpins everything we do Governance and Risk ▪ Well-established governance practices integrated Framework into disciplined decision making Access to Risk Contingent Appetite ▪ Alignment of risk appetites and limits with Facilities and

Limits business strategy ▪ Prudent capital and liquidity management Strong ▪ Active pursuit of diversified risk profile Risk Scenario Capital and Testing Liquidity Culture ▪ Deep technical expertise ▪ Regular stress testing

to identify emerging strategic and tactical threats Active Monitoring Diversified ▪ Prepared to navigate through a wide range of and Risk Profile future scenarios Mitigation Technical Expertise 42

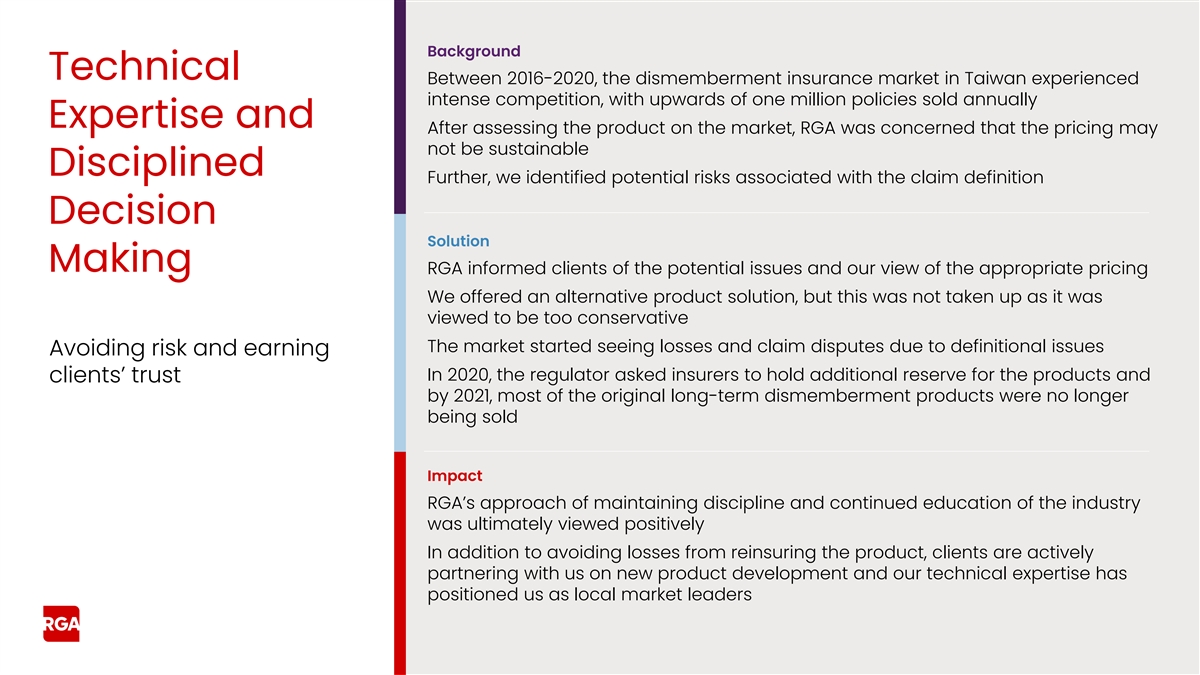

Background Technical Between 2016-2020, the dismemberment insurance

market in Taiwan experienced intense competition, with upwards of one million policies sold annually Expertise and After assessing the product on the market, RGA was concerned that the pricing may not be sustainable Disciplined Further, we

identified potential risks associated with the claim definition Decision Solution Making RGA informed clients of the potential issues and our view of the appropriate pricing We offered an alternative product solution, but this was not taken up as it

was viewed to be too conservative The market started seeing losses and claim disputes due to definitional issues Avoiding risk and earning In 2020, the regulator asked insurers to hold additional reserve for the products and clients’ trust by

2021, most of the original long-term dismemberment products were no longer being sold Impact RGA’s approach of maintaining discipline and continued education of the industry was ultimately viewed positively In addition to avoiding losses from

reinsuring the product, clients are actively partnering with us on new product development and our technical expertise has positioned us as local market leaders

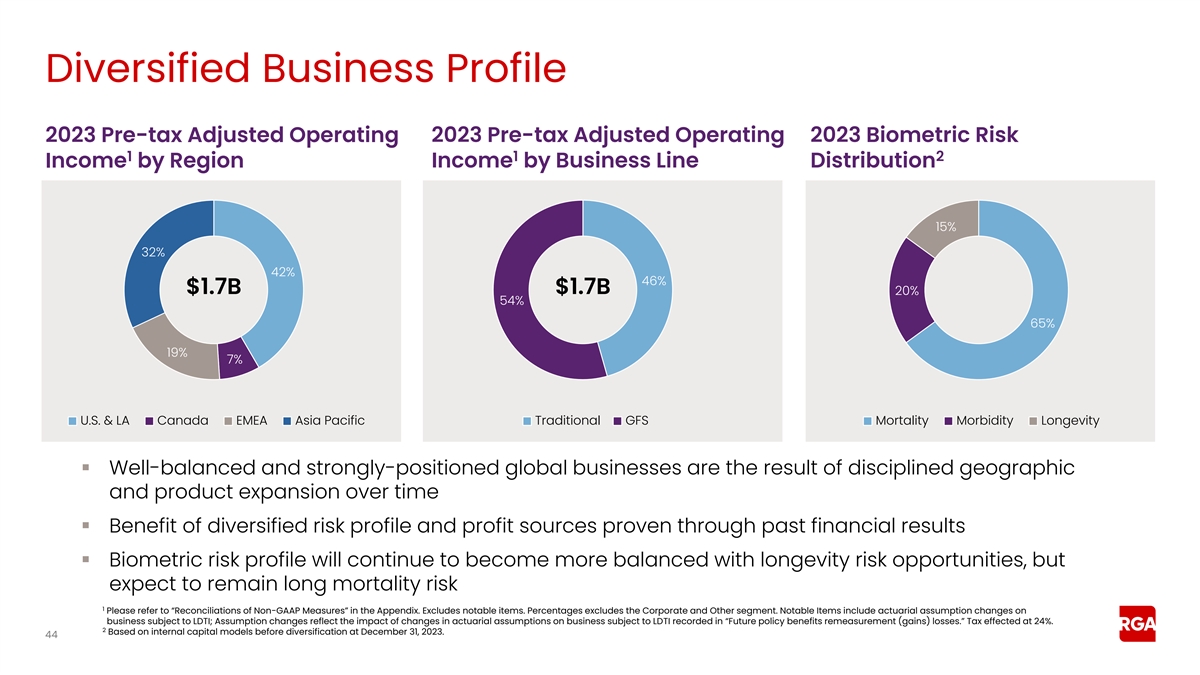

Diversified Business Profile 2023 Pre-tax Adjusted Operating 2023

Pre-tax Adjusted Operating 2023 Biometric Risk 1 1 2 Income by Region Income by Business Line Distribution 15% 32% 42% 46% $1.7B $1.7B 20% 54% 65% 19% 7% U.S. & LA Canada EMEA Asia Pacific Traditional GFS Mortality Morbidity Longevity ▪

Well-balanced and strongly-positioned global businesses are the result of disciplined geographic and product expansion over time ▪ Benefit of diversified risk profile and profit sources proven through past financial results ▪ Biometric

risk profile will continue to become more balanced with longevity risk opportunities, but expect to remain long mortality risk 1 Please refer to “Reconciliations of Non-GAAP Measures” in the Appendix. Excludes notable items. Percentages

excludes the Corporate and Other segment. Notable Items include actuarial assumption changes on business subject to LDTI; Assumption changes reflect the impact of changes in actuarial assumptions on business subject to LDTI recorded in “Future

policy benefits remeasurement (gains) losses.” Tax effected at 24%. 2 Based on internal capital models before diversification at December 31, 2023. 44

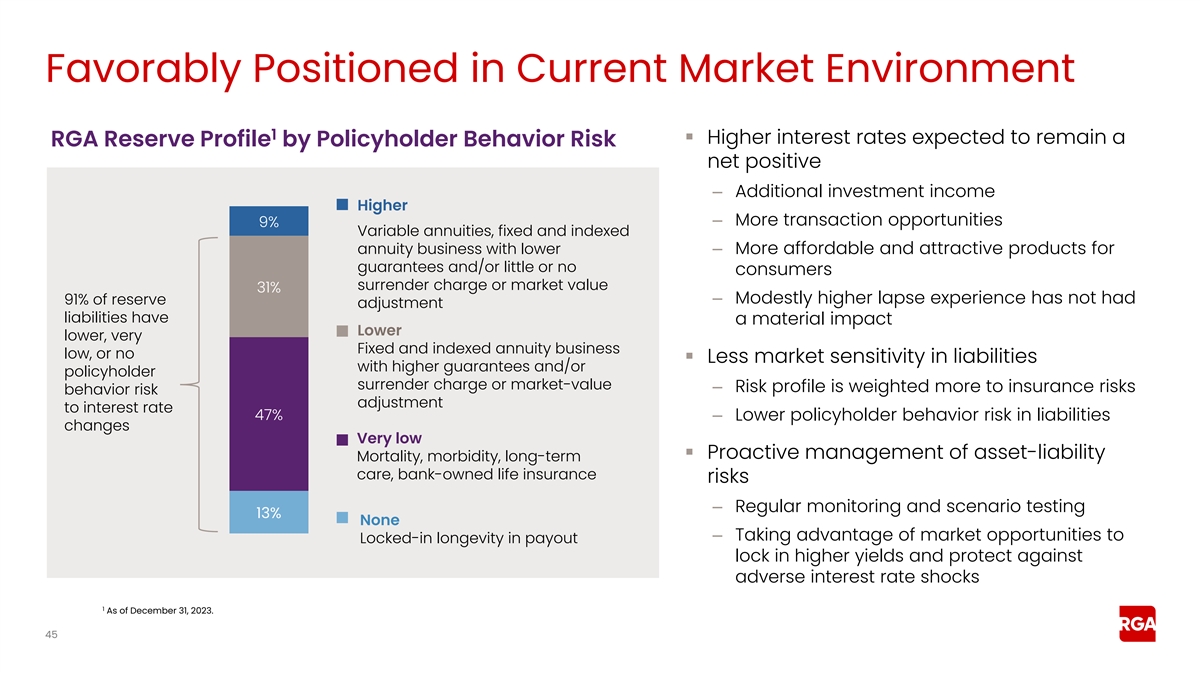

Favorably Positioned in Current Market Environment 1 ▪ Higher

interest rates expected to remain a RGA Reserve Profile by Policyholder Behavior Risk net positive – Additional investment income Higher – More transaction opportunities 9% Variable annuities, fixed and indexed annuity business with

lower – More affordable and attractive products for guarantees and/or little or no consumers surrender charge or market value 31% – Modestly higher lapse experience has not had 91% of reserve adjustment liabilities have a material impact

Lower lower, very Fixed and indexed annuity business low, or no ▪ Less market sensitivity in liabilities with higher guarantees and/or policyholder surrender charge or market-value – Risk profile is weighted more to insurance risks

behavior risk adjustment to interest rate 47% – Lower policyholder behavior risk in liabilities changes Very low ▪ Proactive management of asset-liability Mortality, morbidity, long-term care, bank-owned life insurance risks –

Regular monitoring and scenario testing 13% None – Taking advantage of market opportunities to Locked-in longevity in payout lock in higher yields and protect against adverse interest rate shocks 1 As of December 31, 2023. 45

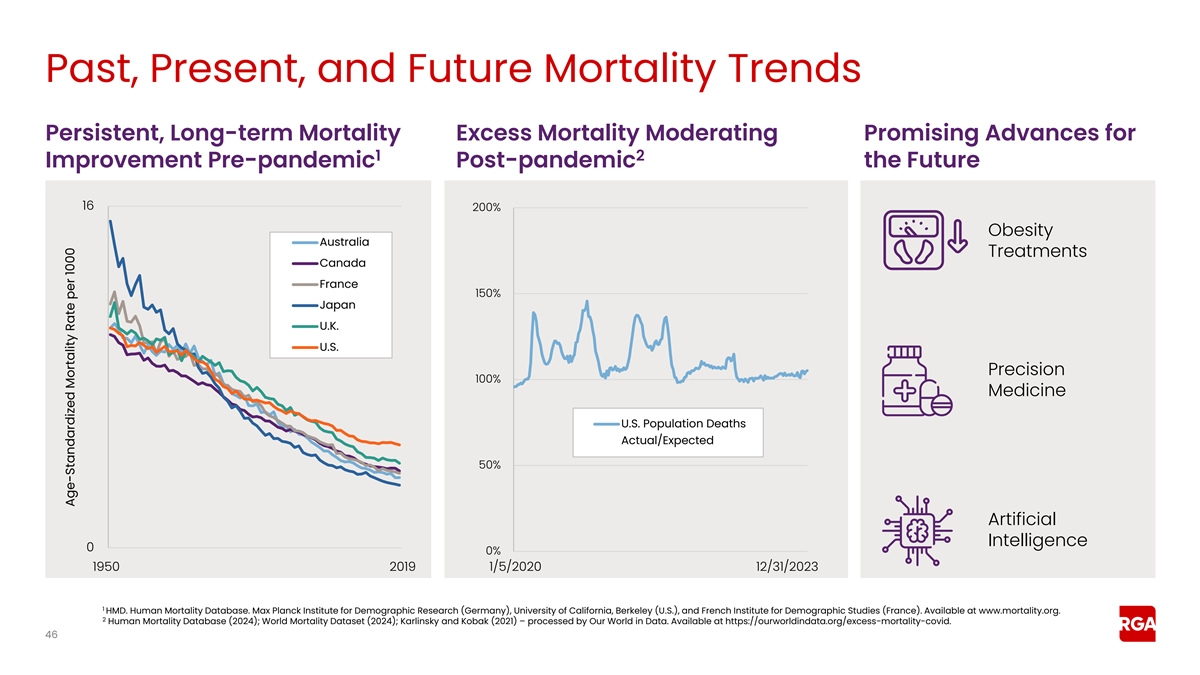

Past, Present, and Future Mortality Trends Persistent, Long-term

Mortality Excess Mortality Moderating Promising Advances for 1 2 Improvement Pre-pandemic Post-pandemic the Future 16 200% Obesity Australia Treatments Canada France 150% Japan U.K. U.S. Precision 100% Medicine U.S. Population Deaths Actual/Expected

50% Artificial Intelligence 0 0% 1950 2019 1/5/2020 12/31/2023 1 HMD. Human Mortality Database. Max Planck Institute for Demographic Research (Germany), University of California, Berkeley (U.S.), and French Institute for Demographic Studies

(France). Available at www.mortality.org. 2 Human Mortality Database (2024); World Mortality Dataset (2024); Karlinsky and Kobak (2021) – processed by Our World in Data. Available at https://ourworldindata.org/excess-mortality-covid. 46

Age-Standardized Mortality Rate per 1000

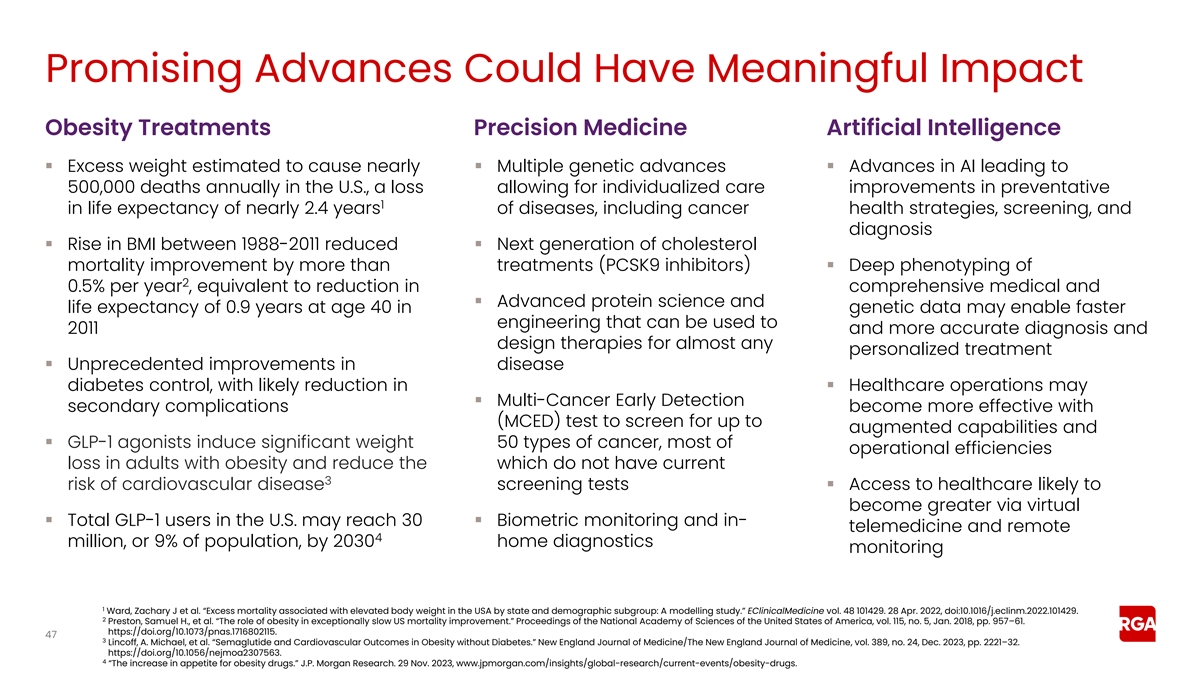

Promising Advances Could Have Meaningful Impact Obesity Treatments

Precision Medicine Artificial Intelligence ▪ Excess weight estimated to cause nearly ▪ Multiple genetic advances ▪ Advances in AI leading to 500,000 deaths annually in the U.S., a loss allowing for individualized care improvements

in preventative 1 in life expectancy of nearly 2.4 years of diseases, including cancer health strategies, screening, and diagnosis ▪ Rise in BMI between 1988-2011 reduced ▪ Next generation of cholesterol mortality improvement by more

than treatments (PCSK9 inhibitors)▪ Deep phenotyping of 2 0.5% per year , equivalent to reduction in comprehensive medical and ▪ Advanced protein science and life expectancy of 0.9 years at age 40 in genetic data may enable faster

engineering that can be used to 2011 and more accurate diagnosis and design therapies for almost any personalized treatment ▪ Unprecedented improvements in disease diabetes control, with likely reduction in ▪ Healthcare operations may

▪ Multi-Cancer Early Detection secondary complications become more effective with (MCED) test to screen for up to augmented capabilities and ▪ GLP-1 agonists induce significant weight 50 types of cancer, most of operational efficiencies

loss in adults with obesity and reduce the which do not have current 3 risk of cardiovascular disease screening tests▪ Access to healthcare likely to become greater via virtual ▪ Total GLP-1 users in the U.S. may reach 30 ▪

Biometric monitoring and in- telemedicine and remote 4 million, or 9% of population, by 2030 home diagnostics monitoring 1 Ward, Zachary J et al. “Excess mortality associated with elevated body weight in the USA by state and demographic

subgroup: A modelling study.” EClinicalMedicine vol. 48 101429. 28 Apr. 2022, doi:10.1016/j.eclinm.2022.101429. 2 Preston, Samuel H., et al. “The role of obesity in exceptionally slow US mortality improvement.” Proceedings of the

National Academy of Sciences of the United States of America, vol. 115, no. 5, Jan. 2018, pp. 957–61. https://doi.org/10.1073/pnas.1716802115. 47 3 Lincoff, A. Michael, et al. “Semaglutide and Cardiovascular Outcomes in Obesity without

Diabetes.” New England Journal of Medicine/The New England Journal of Medicine, vol. 389, no. 24, Dec. 2023, pp. 2221–32. https://doi.org/10.1056/nejmoa2307563. 4 “The increase in appetite for obesity drugs.” J.P. Morgan

Research. 29 Nov. 2023, www.jpmorgan.com/insights/global-research/current-events/obesity-drugs.

Data-Driven Research Creates Risk Insights and Enhances Brand ▪

Differentiated, multi-disciplinary expertise enables exclusive and forward-looking insights for both risks and opportunities ▪ Thought leadership initiates and supports client engagement and reinforces RGA’s brand as an innovation leader

in the life and health insurance industry ▪ RGA has ranked #1 in thought leadership and knowledge for seven consecutive years on NMG Consulting's Global Life & Health Reinsurance Study 48

Managing Risk for Sustained Success Strong risk Technical Diversified

Favorable Research and culture, expertise set of macro thought proactive risk and global risks trends leadership management discipline Confidence in bright future 49

Investments Leslie Barbi Executive Vice President, Chief Investment

Officer 50

Key Messages Integrated, ▪ Flexible asset platform delivering a

Completion Platform aligned, and comprehensive suite of capabilities and Provides Integrated customized to asset solutions Strategic Advantages deliver creative ▪ Integrated solutions, tailored to our new business and in-force liabilities

client solutions ▪ Positioned for growth opportunities and asset-liability risk management ▪ Experienced team balances return and risk to weather cycles Experience, Proven Strategy, Execution ▪ Disciplined investment underwriting

and ongoing management drive long-term success ▪ Well-established investment and enterprise risk management ▪ Expanding our integrated asset platform Long Track Record of Performance Integral ▪ Supporting financial strength to

Success ▪ Delivering results targeted for integrated business success 51

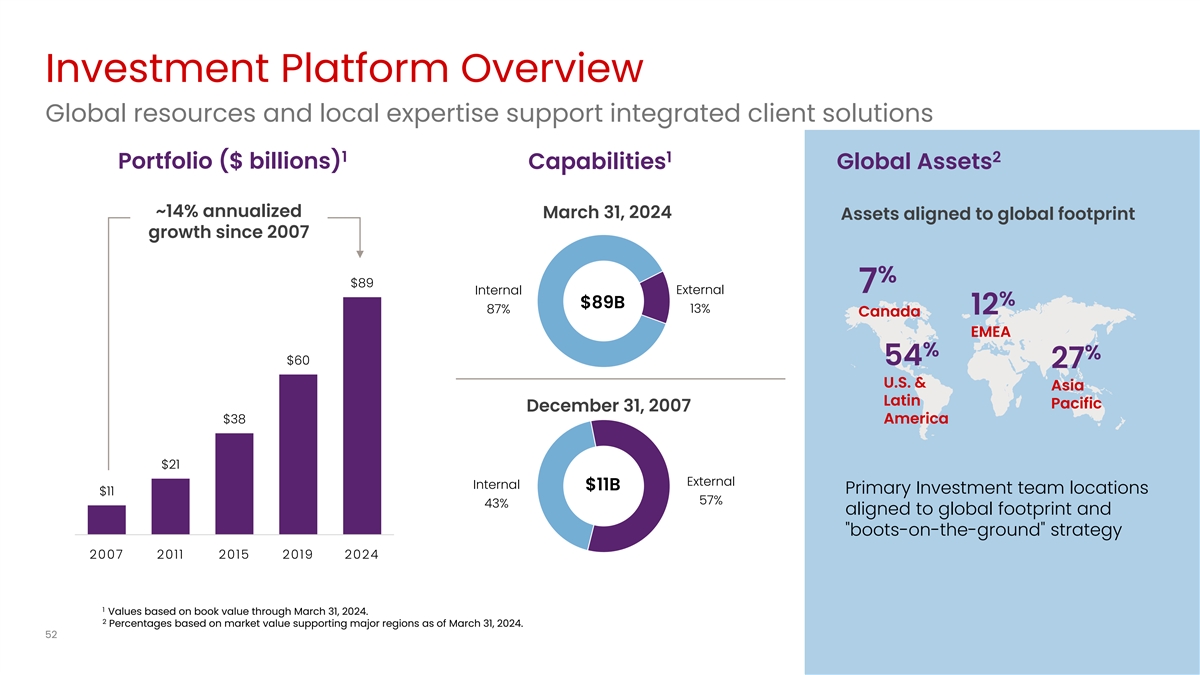

Investment Platform Overview Global resources and local expertise

support integrated client solutions 1 1 2 Portfolio ($ billions) Capabilities Global Assets ~14% annualized March 31, 2024 Assets aligned to global footprint growth since 2007 % $89 External 7 Internal % $89B 13% 87% 12 Canada EMEA % % $60 54 27

U.S. & Asia Latin Pacific December 31, 2007 $38 America $21 External Internal $11B Primary Investment team locations $11 57% 43% aligned to global footprint and boots-on-the-ground strategy 2007 2011 2015 2019 2024 1 Values based on book value

through March 31, 2024. 2 Percentages based on market value supporting major regions as of March 31, 2024. 52

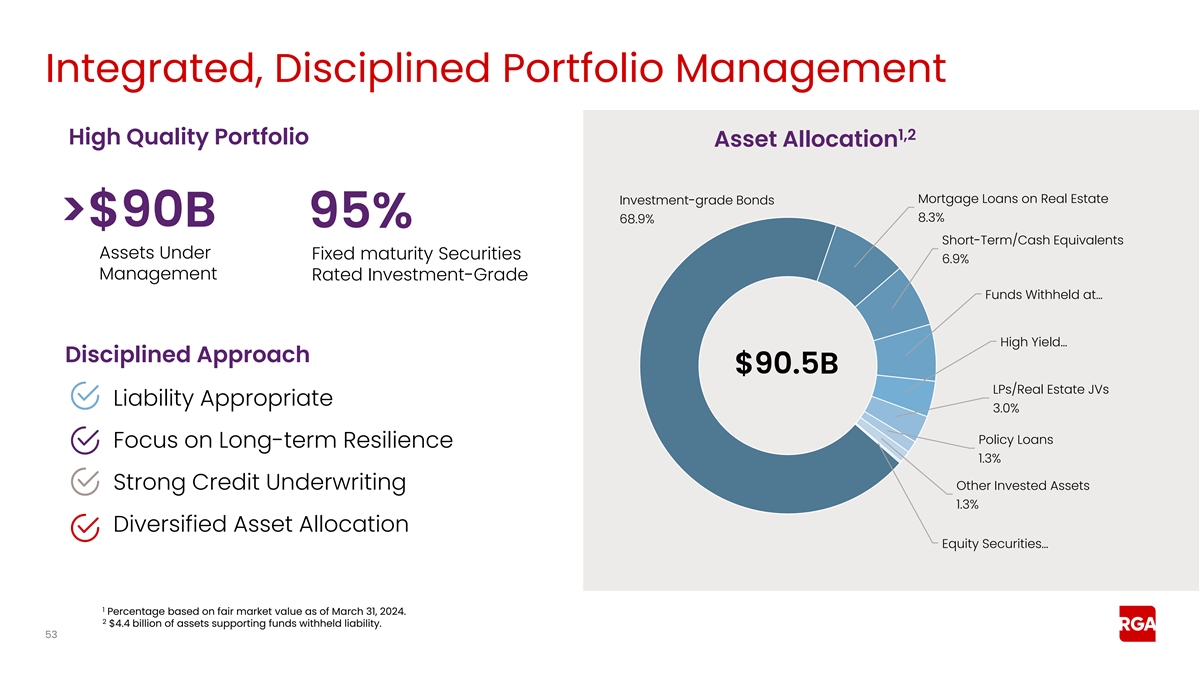

Integrated, Disciplined Portfolio Management 1,2 High Quality Portfolio

Asset Allocation Mortgage Loans on Real Estate Investment-grade Bonds 8.3% 68.9% >$90B 95% Short-Term/Cash Equivalents Assets Under Fixed maturity Securities 6.9% Management Rated Investment-Grade Funds Withheld at … High Yield …

Disciplined Approach $90.5B LPs/Real Estate JVs Liability Appropriate 3.0% Policy Loans Focus on Long-term Resilience 1.3% Strong Credit Underwriting Other Invested Assets 1.3% Diversified Asset Allocation Equity Securities… 1 Percentage based

on fair market value as of March 31, 2024. 2 $4.4 billion of assets supporting funds withheld liability. 53

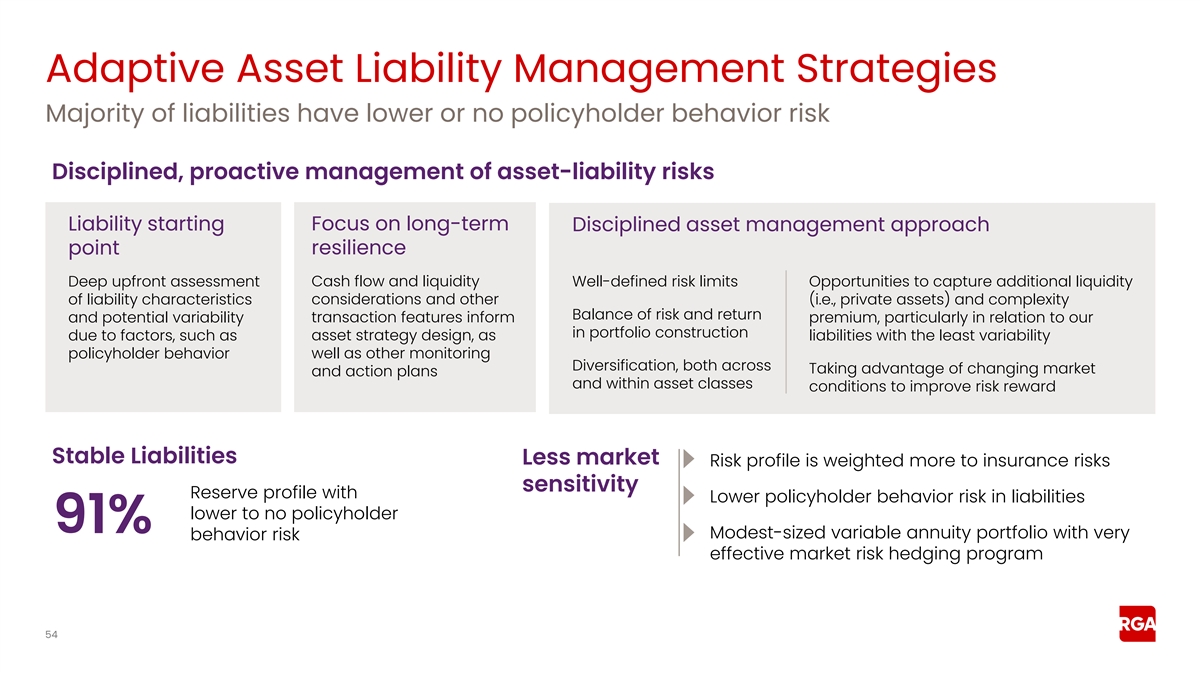

Adaptive Asset Liability Management Strategies Majority of liabilities

have lower or no policyholder behavior risk Disciplined, proactive management of asset-liability risks Focus on long-term Liability starting Disciplined asset management approach point resilience Deep upfront assessment Cash flow and liquidity

Well-defined risk limits Opportunities to capture additional liquidity of liability characteristics considerations and other (i.e., private assets) and complexity Balance of risk and return and potential variability transaction features inform

premium, particularly in relation to our in portfolio construction asset strategy design, as due to factors, such as liabilities with the least variability policyholder behavior well as other monitoring Diversification, both across Taking advantage

of changing market and action plans and within asset classes conditions to improve risk reward Stable Liabilities Less market Risk profile is weighted more to insurance risks sensitivity Reserve profile with Lower policyholder behavior risk in

liabilities lower to no policyholder 91% Modest-sized variable annuity portfolio with very behavior risk effective market risk hedging program 54

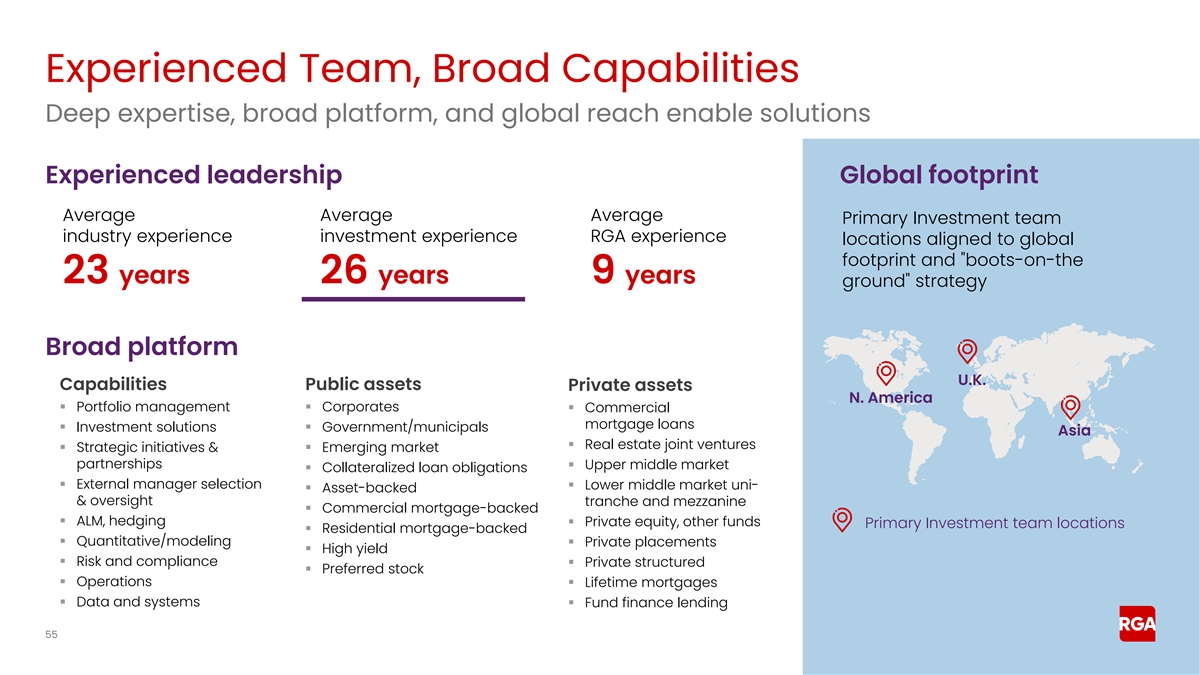

Experienced Team, Broad Capabilities Deep expertise, broad platform,

and global reach enable solutions Experienced leadership Global footprint Average Average Average Primary Investment team industry experience investment experience RGA experience locations aligned to global footprint and boots-on-the 23 years 26

years 9 years ground strategy Broad platform U.K. Capabilities Public assets Private assets N. America ▪ Portfolio management▪ Corporates ▪ Commercial mortgage loans ▪ Investment solutions▪ Government/municipals Asia

▪ Real estate joint ventures ▪ Strategic initiatives & ▪ Emerging market partnerships ▪ Upper middle market ▪ Collateralized loan obligations ▪ External manager selection ▪ Lower middle market uni-

▪ Asset-backed & oversight tranche and mezzanine ▪ Commercial mortgage-backed ▪ ALM, hedging▪ Private equity, other funds Primary Investment team locations ▪ Residential mortgage-backed ▪

Quantitative/modeling▪ Private placements ▪ High yield ▪ Risk and compliance ▪ Private structured ▪ Preferred stock ▪ Operations ▪ Lifetime mortgages ▪ Data and systems ▪ Fund finance lending

55

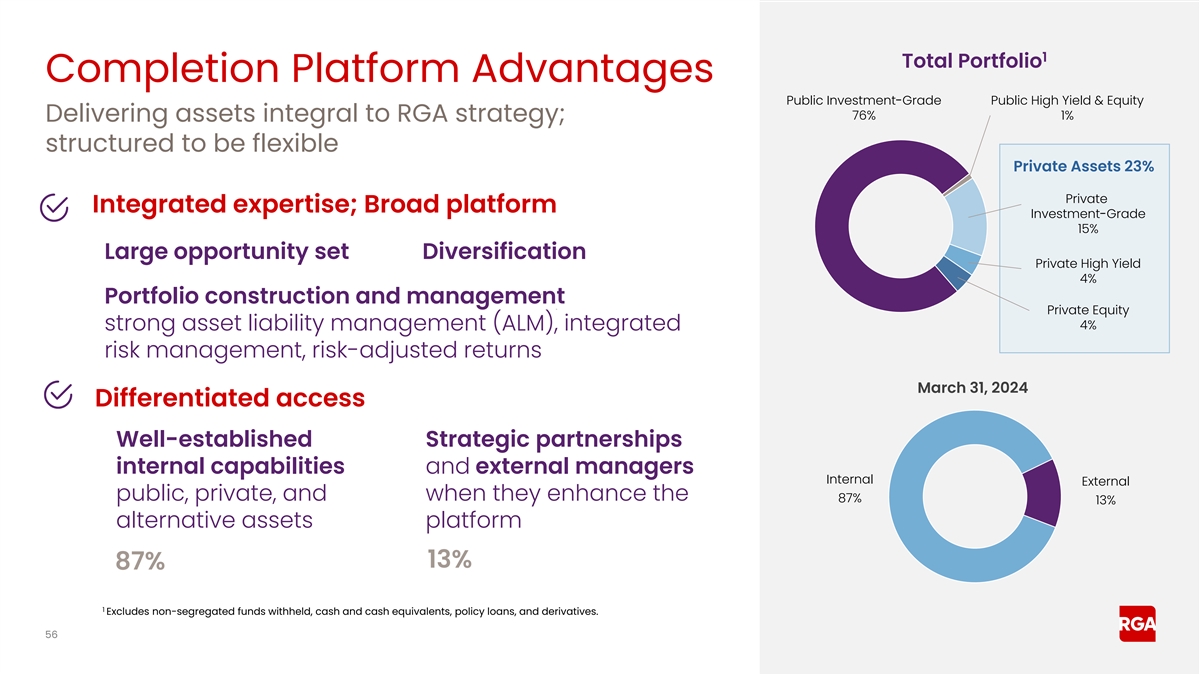

1 Total Portfolio Completion Platform Advantages Public

Investment-Grade Public High Yield & Equity 76% 1% Delivering assets integral to RGA strategy; structured to be flexible Private Assets 23% Private Integrated expertise; Broad platform Investment-Grade 15% Large opportunity set Diversification

Private High Yield 4% Portfolio construction and management Private Equity 4% strong asset liability management (ALM), integrated risk management, risk-adjusted returns March 31, 2024 Differentiated access Well-established Strategic partnerships

internal capabilities and external managers Internal External public, private, and when they enhance the 87% 13% alternative assets platform 13% 87% 1 Excludes non-segregated funds withheld, cash and cash equivalents, policy loans, and derivatives.

56

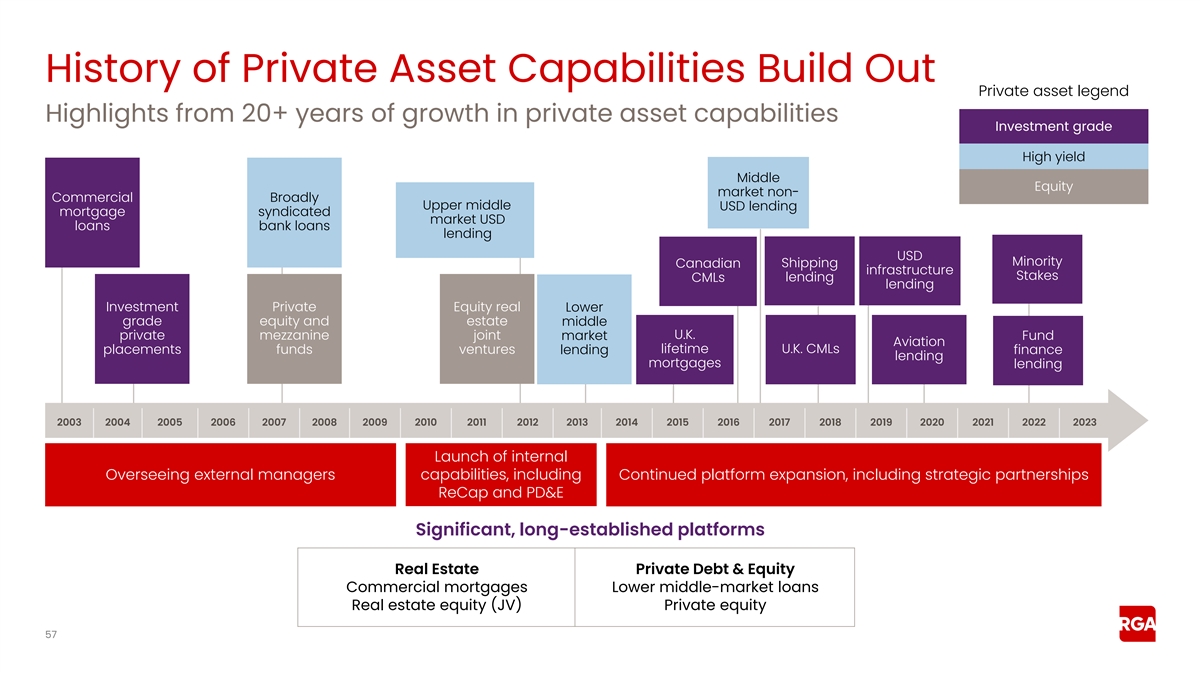

History of Private Asset Capabilities Build Out Private asset legend

Highlights from 20+ years of growth in private asset capabilities Investment grade High yield Middle Equity market non- Commercial Broadly Upper middle USD lending mortgage syndicated market USD loans bank loans lending USD Minority Canadian

Shipping infrastructure Stakes lending CMLs lending Investment Private Equity real Lower grade equity and estate middle U.K. private mezzanine joint market Fund Aviation placements funds ventures lending lifetime U.K. CMLs finance lending mortgages

lending 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 Launch of internal Overseeing external managers capabilities, including Continued platform expansion, including strategic partnerships

ReCap and PD&E Significant, long-established platforms Real Estate Private Debt & Equity Commercial mortgages Lower middle-market loans Real estate equity (JV) Private equity 57

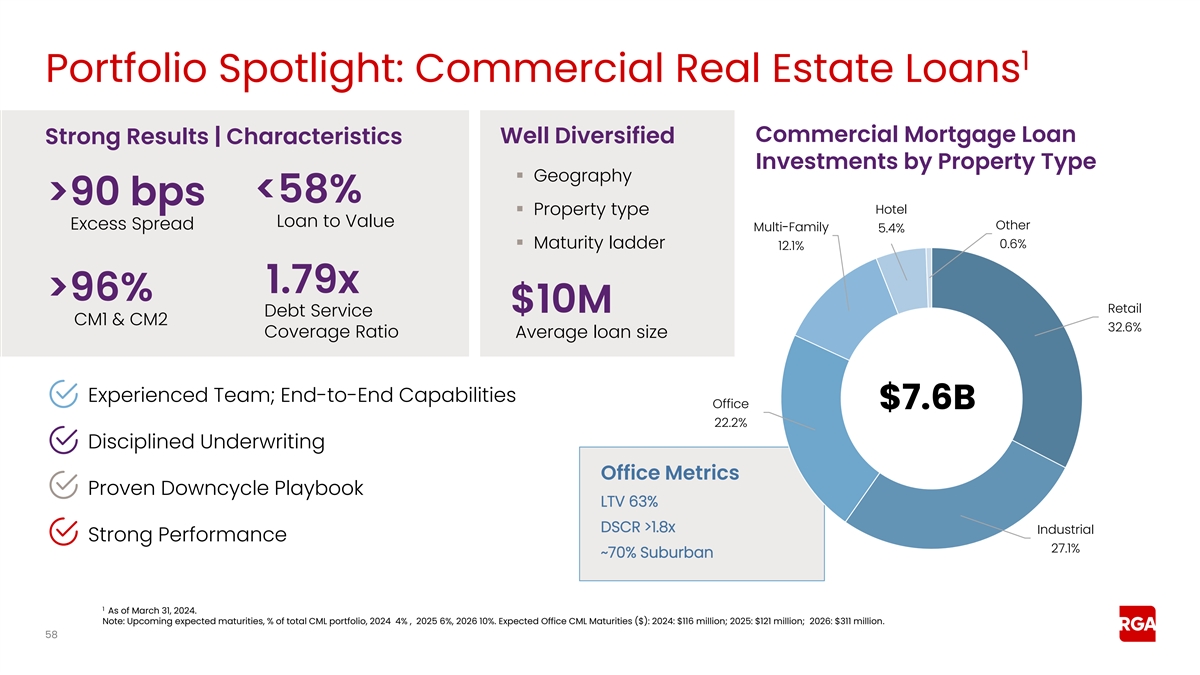

1 Portfolio Spotlight: Commercial Real Estate Loans Commercial Mortgage

Loan Strong Results | Characteristics Well Diversified Investments by Property Type ▪ Geography <58% >90 bps Hotel ▪ Property type Loan to Value Excess Spread Other Multi-Family 5.4% ▪ Maturity ladder 0.6% 12.1% 1.79x >96%

$10M Retail Debt Service CM1 & CM2 32.6% Coverage Ratio Average loan size Experienced Team; End-to-End Capabilities Office $7.6B 22.2% Disciplined Underwriting Office Metrics Proven Downcycle Playbook LTV 63% DSCR >1.8x Industrial Strong

Performance 27.1% ~70% Suburban 1 As of March 31, 2024. Note: Upcoming expected maturities, % of total CML portfolio, 2024 4% , 2025 6%, 2026 10%. Expected Office CML Maturities ($): 2024: $116 million; 2025: $121 million; 2026: $311 million.

58

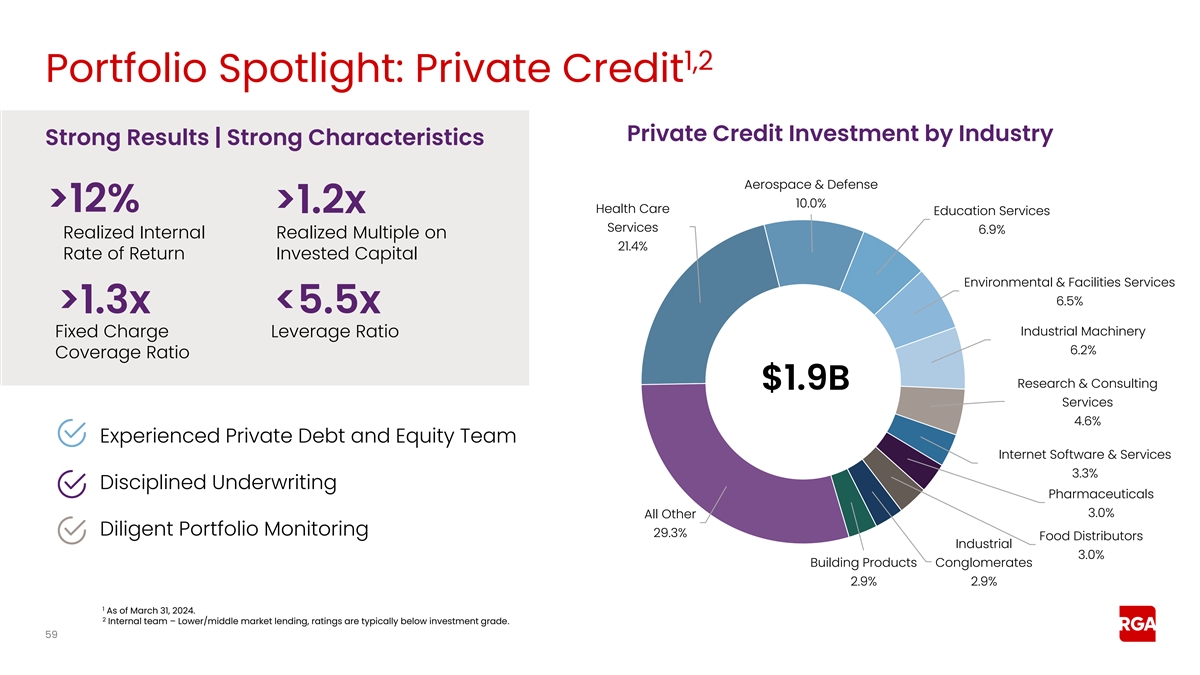

1,2 Portfolio Spotlight: Private Credit Private Credit Investment by

Industry Strong Results | Strong Characteristics Aerospace & Defense 10.0% >12% >1.2x Health Care Education Services Services 6.9% Realized Internal Realized Multiple on 21.4% Rate of Return Invested Capital Environmental & Facilities

Services 6.5% >1.3x <5.5x Industrial Machinery Fixed Charge Leverage Ratio 6.2% Coverage Ratio Research & Consulting $1.9B Services 4.6% Experienced Private Debt and Equity Team Internet Software & Services 3.3% Disciplined

Underwriting Pharmaceuticals 3.0% All Other Diligent Portfolio Monitoring 29.3% Food Distributors Industrial 3.0% Building Products Conglomerates 2.9% 2.9% 1 As of March 31, 2024. 2 Internal team – Lower/middle market lending, ratings are

typically below investment grade. 59

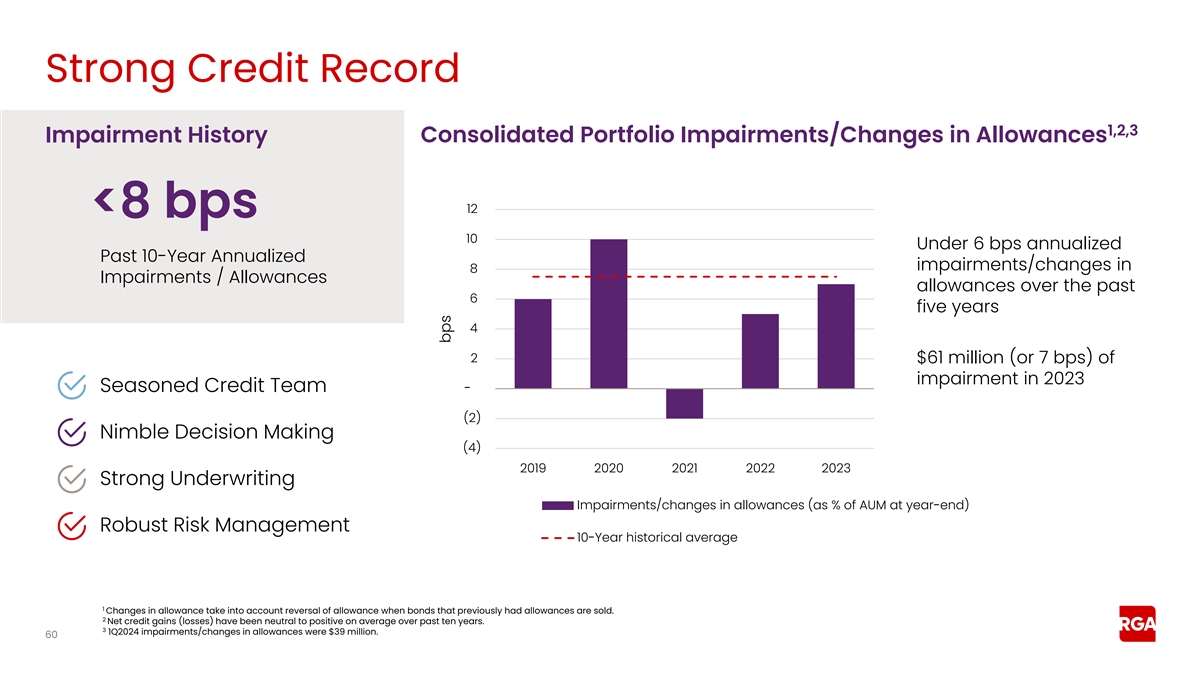

Strong Credit Record 1,2,3 Impairment History Consolidated Portfolio

Impairments/Changes in Allowances 12 <8 bps 10 Under 6 bps annualized Past 10-Year Annualized impairments/changes in 8 Impairments / Allowances allowances over the past 6 five years 4 2 $61 million (or 7 bps) of impairment in 2023 Seasoned Credit

Team - (2) Nimble Decision Making (4) 2019 2020 2021 2022 2023 Strong Underwriting Impairments/changes in allowances (as % of AUM at year-end) Robust Risk Management 10-Year historical average 1 Changes in allowance take into account reversal of

allowance when bonds that previously had allowances are sold. 2 Net credit gains (losses) have been neutral to positive on average over past ten years. 3 1Q2024 impairments/changes in allowances were $39 million. 60 bps

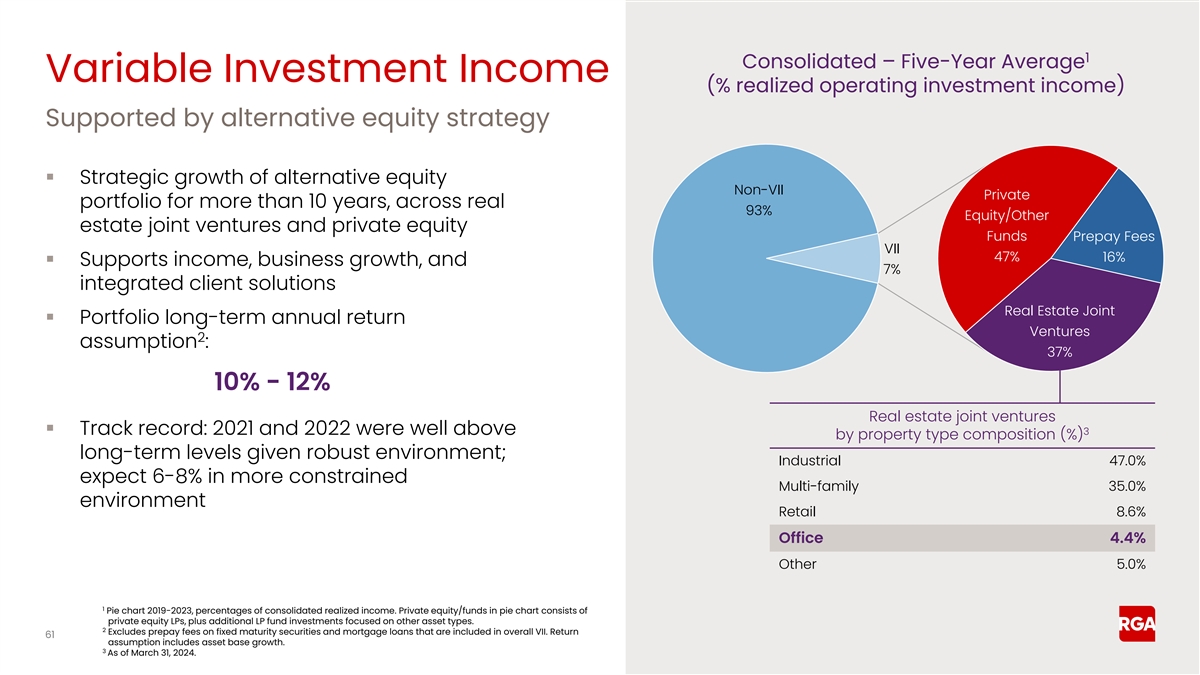

1 Consolidated – Five-Year Average Variable Investment Income (%

realized operating investment income) Supported by alternative equity strategy ▪ Strategic growth of alternative equity Non-VII Private portfolio for more than 10 years, across real 93% Equity/Other estate joint ventures and private equity

Funds Prepay Fees VII 47% 16% ▪ Supports income, business growth, and 7% integrated client solutions Real Estate Joint ▪ Portfolio long-term annual return Ventures 2 assumption : 37% 10% - 12% Real estate joint ventures ▪ Track

record: 2021 and 2022 were well above 3 by property type composition (%) long-term levels given robust environment; Industrial 47.0% expect 6-8% in more constrained Multi-family 35.0% environment Retail 8.6% Office 4.4% Other 5.0% 1 Pie chart

2019-2023, percentages of consolidated realized income. Private equity/funds in pie chart consists of private equity LPs, plus additional LP fund investments focused on other asset types. 2 Excludes prepay fees on fixed maturity securities and

mortgage loans that are included in overall VII. Return 61 assumption includes asset base growth. 3 As of March 31, 2024.

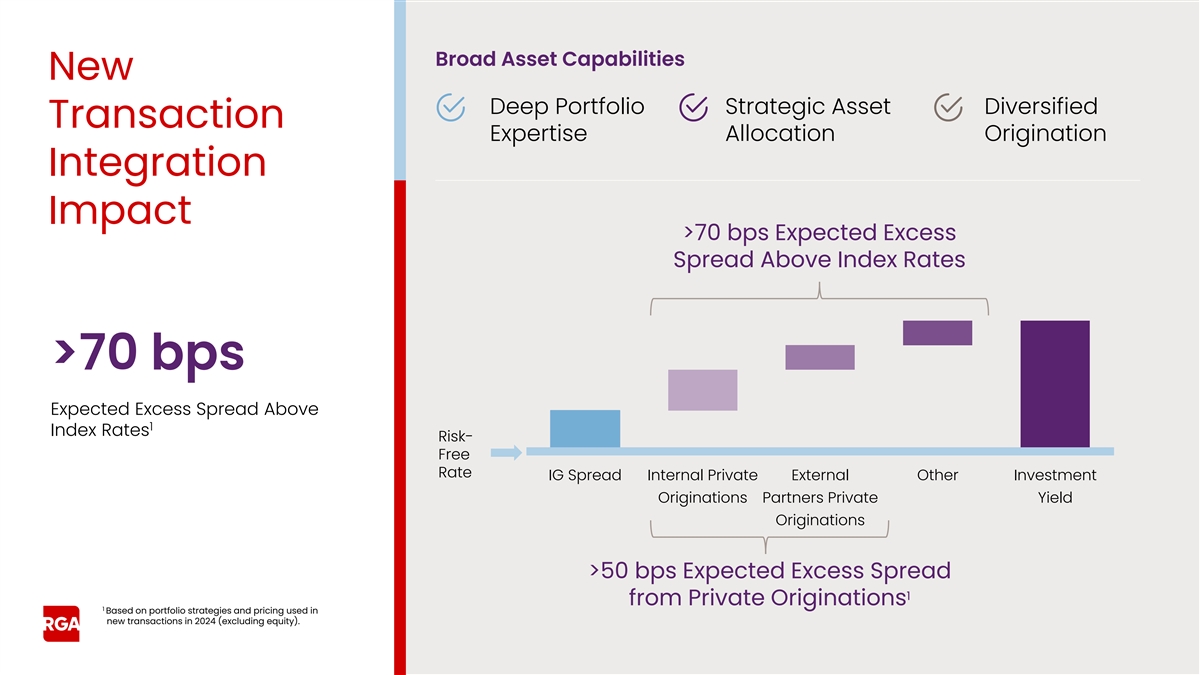

Broad Asset Capabilities New Deep Portfolio Strategic Asset Diversified

Transaction Expertise Allocation Origination Integration Impact >70 bps Expected Excess Spread Above Index Rates >70 bps Expected Excess Spread Above 1 Index Rates Risk- Free Rate IG Spread Internal Private External Other Investment