UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-01731

Source Capital, Inc.

(Exact name of registrant as specified in charter)

235 W. Galena Street

Milwaukee, WI 53212

(Address of principal executive offices) (Zip code)

Diane J. Drake

Mutual Fund Administration, LLC

2220 E. Route 66, Suite 226

Glendora, CA 91740

(Name and address of agent for service)

(626) 385-5777

Registrant's telephone number, including area code

Date of fiscal year end: December 31

Date of reporting period: June 30, 2024

Item 1. Report to Stockholders.

(a) The registrant’s semi-annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

SOURCE CAPITAL, INC.

2024

SEMIANNUAL REPORT

for the six months ended June 30, 2024

(This page has been left blank intentionally.)

SOURCE CAPITAL, INC.

LETTER TO SHAREHOLDERS

DEAR SHAREHOLDER:

Performance Overview

Source Capital Inc.'s ("Source" or "Fund") net asset value (NAV) gained 2.45% for the quarter and 14.85% for the trailing twelve months, which is in line with the illustrative balanced indices shown below.

Performance versus Illustrative Indices1

| | | Q2 2024 | | Trailing 12-month | |

Source Capital (NAV) | | | 2.45 | % | | | 14.85 | % | |

Balanced Indices | | | | | |

60% MSCI ACWI/40% Bloomberg US Agg | | | 1.75 | % | | | 12.49 | % | |

60% S&P 500/40% Bloomberg US Agg | | | 2.60 | % | | | 15.42 | % | |

Equity Index | |

MSCI ACWI | | | 2.87 | % | | | 19.38 | % | |

We include the Fund's underlying exposure by asset class in the following table:

Portfolio Exposure2

| | | Q2 2024 | |

Equity | | | |

Common Stocks | | | 39.8 | % | |

Total Equity | | | 39.8 | % | |

Credit | | | |

Public | | | 25.1 | % | |

Private (Invested assets only) | | | 16.0 | % | |

Total Credit | | | 41.1 | % | |

Other | | | 0.2 | % | |

Cash | | | 18.9 | % | |

Total | | | 100.0 | % | |

Portfolio & Market Discussion3

Equity

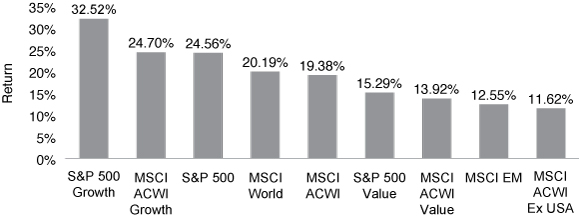

The stock market has been a tale of the haves and have-nots with returns lifted by just four contributors (Nvidia, Microsoft, Alphabet, and Amazon.com) that represented 43% and 53% of the MSCI ACWI and S&P 500 YTD returns, respectively.4

Though Value outperformed Growth in 2022's market rout, Growth is again leading the charge. In the last year, the S&P 500 Growth battered Value by more than seventeen percentage points while the MSCI ACWI Growth beat the Value component by almost eleven percentage points.

1 Comparison to the indices is for illustrative purposes only. An investor cannot invest directly in an index. Fund shareholders may only invest or redeem their shares at market value (NYSE: SOR), which may be higher or lower than the Fund's net asset value (NAV).

2 Source: FPA, as of June 30, 2024. Portfolio composition will change due to ongoing management of the Fund. Cash includes the non-invested portion of private credit investments. Totals may not add up to 100% due to rounding.

3 References to individual securities are for informational purposes only, are subject to change, and should not be construed as recommendation or a solicitation to buy or sell a particular security. Portfolio composition will change due to ongoing management of the Fund. Portfolio holdings for the Fund can be found at fpa.com.

4 Source: Factset. As of June 30, 2024. "YTD" stands for year-to-date.

Past results are no guarantee, nor are they indicative, of future results.

1

Trailing Twelve-Month Index Performance5

Value managers have not had an easy time of it. In the past decade, Value has underperformed Growth by such a significant margin that it threatens its existence as an investment philosophy.6 Many investors have capitulated and fired their Value managers, pushing some Value managers into early retirement. Others have converted to the Temple of Growth.

With respect to the recent performance of the Fund, in the previous twelve months, Source's top five performers contributed 7.18% to its return while its bottom five detracted 1.38%.7

We list the top equity contributors to and detractors from the Fund's trailing twelve-month returns below.

Trailing Twelve-Month Contributors and Detractors as of June 30, 20248

Contributors | | Perf.

Cont. | | Avg. %

of Port. | | Detractors | | Perf.

Cont. | | Avg. %

of Port. | |

Alphabet | | | 0.99 | % | | | 2.1 | % | | JDE Peet's | | | -0.34 | % | | | 0.9 | % | |

Holcim | | | 0.88 | % | | | 2.6 | % | | Aon | | | -0.24 | % | | | 1.4 | % | |

Citigroup | | | 0.82 | % | | | 1.8 | % | | Charter Communications | | | -0.12 | % | | | 0.6 | % | |

Meta Platforms | | | 0.71 | % | | | 1.2 | % | | Entain | | | -0.11 | % | | | 0.2 | % | |

Broadcom | | | 0.70 | % | | | 1.0 | % | | LG Corp | | | -0.08 | % | | | 0.8 | % | |

| | | | 4.10 | % | | | 8.7 | % | | | | | -0.90 | % | | | 3.9 | % | |

The following investments were meaningful to the Fund's trailing twelve-month return and have not been recently discussed.9

Building materials (largely concrete, cement, and aggregates) company Holcim has performed well over the past year. In addition to strong operating performance, management has taken several steps to return value to shareholders and improve awareness of the company's underlying business strength, including repurchasing shares, increasing the dividend, and announcing plans to separate the company's North American business.

5 Source: Morningstar. As of June 30, 2024.

6 Source: Morningstar. Over the past ten years through June 30, 2024, the cumulative return of the S&P 500 Value Index was 157% vs 303% for the S&P 500 Growth Index, and the cumulative return of the MSCI ACWI Value Index was 69% vs 188% of the MSCI ACWI Growth Index.

7 "Top five performers" and "bottom five" refers to the full portfolio of securities. Contribution is presented gross of investment management fees, transactions costs, and Fund operating expenses, which if included, would reduce the returns presented.

8 Reflects the top five contributors and detractors to the Fund's performance based on contribution to return for the trailing twelve months ("TTM"). Contribution is presented gross of investment management fees, transactions costs, and Fund operating expenses, which if included, would reduce the returns presented. The information provided does not reflect all positions purchased, sold or recommended by FPA during the quarter. A copy of the methodology used and a list of every holding's contribution to the overall Fund's performance during the TTM is available by contacting FPA Client Service at crm@fpa.com. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities listed.

9 The company data and statistics referenced in this section, including competitor data, are sourced from company press releases, investor presentations, financial disclosures, SEC filings, or company websites, unless otherwise noted. You can find the Fund's other positions addressed previously in our archived commentaries.

Past results are no guarantee, nor are they indicative, of future results.

2

Citigroup's shares have appreciated (along with other bank stocks) from a profoundly depressed level of less than 50% of tangible book value to a modestly depressed level of 70%. We expect the company to deliver significantly improved results and sizable capital returns over the next few years.

Charter has faced challenging operating conditions that have led to its share price weakness. Competitors have been overbuilding with fiber assets and fixed wireless has proven to be meaningful. There has been concern regarding the sustainability of business derived from subsidized customers. And, the company's near-term capital spending budget has exceeded expectations. Compounding matters, its relatively high leverage ratio adds volatility to its stock price. We look forward to the company demonstrating the competitive strength of its converged (fixed and wireless) connectivity offering, ramping down capital spending, and reaccelerating share repurchases.

We remain mindful of seeking to deliver a good return while assuming reasonable risk in the hopes of avoiding permanent capital impairments. While there are many ways to mitigate portfolio risk, Source offers various types that consider company valuations, risk exposure, business quality, and diversification.

It would be difficult to argue that the market has stocks on sale. While the stock market continues to migrate higher, earnings haven't kept pace at the same rate, making the market more expensive.

S&P 500 and MSCI ACWI Earnings Growth and Index Return since Year-End 202210

| | | S&P 500 | | MSCI ACWI | |

| | | Cumulative

Earnings Growth | | Cumulative

Return | | Cumulative

Earnings Growth | | Cumulative

Return | |

12/31/2022 - 6/30/2024 | | | 1.84 | % | | | 42.22 | % | | | 0.40 | % | | | 32.48 | % | |

Exposure is nuanced. It's not just a number. It is also a function of many squishy considerations that define business quality. Investing in higher quality businesses (e.g., those with a protective moat, good returns on capital, opportunities to attractively reinvest that capital, and an exemplary management team at its helm), should serve investors well over time. There was a time when it was easier to make money from lower quality businesses, but that is less the case today, thanks to the many disruptive businesses and new technologies that challenge them. The Fund, therefore, has focused on businesses of higher quality. What used to be price first and quality second has now reversed, with a business's quality being the first line of defense.

Fixed Income

Traditional

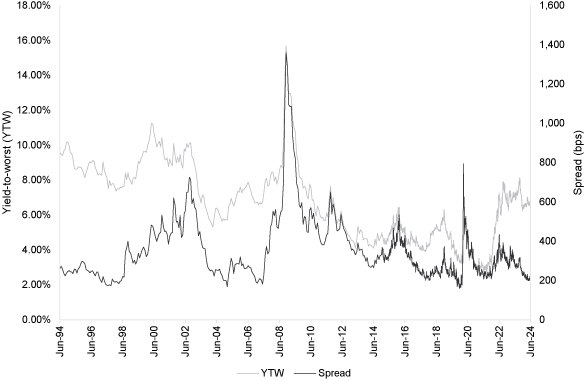

We do not generally see attractive investment opportunities in lower-rated debt. Yields on BBB-rated bonds remain near 15-year highs, but spreads are at the eighth percentile, as measured by the Bloomberg U.S. Aggregate BBB Index. Similarly, in the high yield market, yields also remain near 15-year highs, but spreads have retreated to the sixth percentile, as measured by the BB component of the Bloomberg U.S. Corporate High Yield index excluding Energy, an index we believe provides a more consistent view of high yield market prices over time with fewer distortions caused by changes in the composition of the overall high yield index.

10 Source: Factset. As of June 30, 2024.

Past results are no guarantee, nor are they indicative, of future results.

3

Bloomberg US Corporate High-Yield BB excluding Energy Yield-To-Worst (YTW) and Spread11

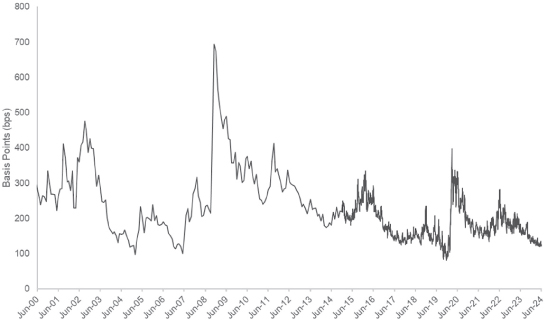

Further, the extra spread offered by high-yield bonds in comparison to investment grade bonds has also compressed. For example, the spread on the BB-rated high yield index, excluding energy, less the spread on investment grade corporate bonds, has decreased to the fourth percentile.

Bloomberg US Corporate High-Yield BB excluding Energy spread

less Bloomberg Investment Grade Corporate spread12

11 Source: Bloomberg. As of June 28, 2024. YTW is Yield-to-Worst. Spread reflects the quoted spread of a bond that is relative to the security off which it is priced, typically an on the-run Treasury. Please see Important Disclosures for definitions of key terms.

12 Source: Bloomberg. As of June 28, 2024. Please see Important Disclosures for definitions of key terms.

Past performance is no guarantee, nor is it indicative, of future results.

4

Importantly, measures of the high yield market such as yield and spread do not account for the underlying quality of bonds in the market at any given point in time. It is our opinion that, on a comparable ratings basis, there has been a degradation in the quality of high yield bonds over the past few years (most notably because of weaker structural protections for bondholders) which, all things being equal, makes high yield debt more expensive than the charts above would suggest. Nevertheless, we continue to search and will opportunistically invest in lower-rated debt when we believe prices adequately compensate for the risk of permanent impairment of capital.

Private Credit

Private credit has performed well, delivering a 6.86% return year-to-date. Source currently has committed 23.4% to private credit (including called and uncalled capital). We continue to look for opportunities to increase that exposure.

Closing

On July 25, 2024, the Fund's Board approved maintaining the Fund's regular monthly distribution of the current rate of 0.2083 cents per share through November 2024.13 This equates to an annualized 5.65% unlevered distribution rate based on the Fund's closing market price on June 28, 2024.

We sincerely appreciate our investors' continued support. We commit to working as hard as ever, and hopefully more intelligently than before, as we incorporate the many new lessons gleaned from our constant reading (and listening to podcasts), our peers, the markets, and our successes and failures. We hope to guide the successful extension of our long track record by keeping front of mind the British Army's 7 P's maxim: Proper Planning and Preparation Prevents Piss Poor Performance.

Respectfully submitted,

Source Capital Portfolio Managers

August 15, 2024

13 For more information related to the Fund's distribution rate, please see the press releases dated July 25, 2024 at: https://fpa.com/news-special-commentaries/fund-announcements. Dividends and other distributions are not guaranteed.

5

Important Disclosures

This Commentary is for informational and discussion purposes only and does not constitute, and should not be construed as, an offer or solicitation for the purchase or sale with respect to any securities, products or services discussed, and neither does it provide investment advice. This Commentary does not constitute an investment management agreement or offering circular.

Current performance information is updated monthly and is available by calling 1-800-982-4372 or by visiting fpa.com. Performance data quoted represents past performance, which is no guarantee of future results. Current performance may vary from the performance quoted. The returns shown for Source Capital are calculated at net asset value per share, including reinvestment of all distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions, which would lower these figures. Since Source Capital is a closed-end investment company and its shares are bought and sold on the New York Stock Exchange, your performance may also vary based upon the market price of the common stock.

The Fund is managed according to its investment strategy which may differ significantly in terms of security holdings, industry weightings, and asset allocation from those of the comparative indices. Overall Fund performance, characteristics and volatility may differ from the comparative indices shown.

There is no guarantee the Fund's investment objectives will be achieved. You should consider the Fund's investment objectives, risks, and charges and expenses carefully before you invest. You can obtain additional information by visiting the website at fpa.com, by email at crm@fpa.com, toll free by calling 1-800-982-4372 or by contacting the Fund in writing.

The views expressed herein and any forward-looking statements are as of the date of this publication and are those of the portfolio management team. Future events or results may vary significantly from those expressed and are subject to change at any time in response to changing circumstances and industry developments. This information and data has been prepared from sources believed reliable, but the accuracy and completeness of the information cannot be guaranteed and is not a complete summary or statement of all available data.

Portfolio composition will change due to ongoing management of the Fund. References to individual financial instruments or sectors are for informational purposes only and should not be construed as recommendations by the Fund or the portfolio managers. It should not be assumed that future investments will be profitable or will equal the performance of the financial instrument or sector examples discussed. The portfolio holdings as of the most recent quarter-end may be obtained atwww.fpa.com.

Investing in closed-end funds involves risk, including loss of principal. Closed-end fund shares may frequently trade at a discount (less than) or premium (more than) to their net asset value. If the Fund's shares trade at a premium to net asset value, there is no assurance that any such premium will be sustained for any period of time and will not decrease, or that the shares will not trade at a discount to net asset value thereafter.

Capital markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. It is important to remember that there are risks inherent in any investment and there is no assurance that any investment or asset class will provide positive performance over time.

The Fund may purchase foreign securities, including American Depository Receipts (ADRs) and other depository receipts, which are subject to interest rate, currency exchange rate, economic and political risks; these risks may be heightened when investing in emerging markets. Non-U.S. investing presents additional risks, such as the potential for adverse political, currency, economic, social or regulatory developments in a country, including lack of liquidity, excessive taxation, and differing legal and accounting standards. Non-U.S. securities, including American Depository Receipts (ADRs) and other depository receipts, are also subject to interest rate and currency exchange rate risks.

The return of principal in a fund that invests in fixed income instruments is not guaranteed. The Fund's investments in fixed income instruments have the same issuer, interest rate, inflation and credit risks that are associated with underlying fixed income instruments owned by the Fund. Such investments may be secured, partially secured or unsecured and may be unrated, and whether or not rated, may have speculative characteristics. The market price of the Fund's fixed income investments will change in response to changes in interest rates and other factors.

Generally, when interest rates go up, the value of fixed income instruments, such as bonds, typically go down (and vice versa) and investors may lose principal value. Credit risk is the risk of loss of principle due to the issuer's failure to repay a loan. Generally, the lower the quality rating of an instrument, the greater the risk that the issuer will fail to pay interest fully and return principal in a timely manner. If an issuer defaults, the security may lose some or all its value. Lower rated bonds, convertible securities and other types of debt obligations involve greater risks than higher rated bonds.

Mortgage-related and asset-backed securities are subject to prepayment risk, can be highly sensitive to changes in interest rates, and are subject to credit risk/risk of default on the underlying assets... Convertible securities are generally not investment grade and are subject to greater credit risk than higher-rated investments. High yield securities can be volatile and subject to much higher instances

6

of default. The Fund may experience increased costs, losses and delays in liquidating underlying securities should the seller of a repurchase agreement declare bankruptcy or default.

The ratings agencies that provide ratings are Standard and Poor's, Moody's, and Fitch. Credit ratings range from AAA (highest) to D (lowest). Bonds rated BBB or above are considered investment grade (IG). Credit ratings of BB and below are lower-rated securities (junk bonds). High-yielding, non-investment grade bonds (junk bonds) (HY) involve higher risks than investment grade bonds. Bonds with credit ratings of CCC or below have high default risk.

Private placement securities are securities that are not registered under the federal securities laws and are generally eligible for sale only to certain eligible investors. Private placements may be illiquid, and thus more difficult to sell, because there may be relatively few potential purchasers for such investments, and the sale of such investments may also be restricted under securities laws.

The Fund may use leverage. While the use of leverage may help increase the distribution and return potential of the Fund, it also increases the volatility of the Fund's net asset value (NAV), and potentially increases volatility of its distributions and market price. There are costs associated with the use of leverage, including ongoing dividend and/or interest expenses. There also may be expenses for issuing or administering leverage. Leverage changes the Fund's capital structure through the issuance of preferred shares and/or debt, both of which are senior to the common shares in priority of claims. If short-term interest rates rise, the cost of leverage will increase and likely will reduce returns earned by the Fund's common stockholders.

Value style investing presents the risk that the holdings or securities may never reach their full market value because the market fails to recognize what the portfolio management team considers the true business value or because the portfolio management team has misjudged those values. In addition, value style investing may fall out of favor and underperform growth or other styles of investing during given periods.

Distribution Rate

Distributions may include the net income from dividends and interest earned by fund securities, net capital gains, or in certain cases it may include a return of capital. The Fund may also pay a special distribution at the end of a calendar year to comply with federal tax requirements. All mutual funds, including closed-end funds, periodically distribute profits they earn to investors. By law, if a fund has net gains from the sale of securities, or if it earns dividends and interest from securities, it must pass substantially all of those earnings to its shareholders or it will be subject to corporate income taxes and excise taxes. These taxes would, in effect, reduce investors' total return. First Pacific Advisors, LP does not provide legal, accounting, or tax advice.

The Fund's distribution rate may be affected by numerous factors, including changes in realized and projected market returns, Fund performance, and other factors. There can be no assurance that a change in market conditions or other factors will not result in a change in the Fund's distribution rate at a future time.

Index Definitions

Comparison to any index is for illustrative purposes only and should not be relied upon as a fully accurate measure of comparison. The Fund may be less diversified than the indices noted herein and may hold non-index securities or securities that are not comparable to those contained in an index. Indices will hold positions that are not within the Fund's investment strategy. Indices are unmanaged and do not reflect any commissions, transaction costs, or fees and expenses which would be incurred by an investor purchasing the underlying securities and which would reduce the performance in an actual account. You cannot invest directly in an index. The Fund does not include outperformance of any index in its investment objectives.

S&P 500 Index includes a representative sample of 500 hundred companies in leading industries of the U.S. economy. The Index focuses on the large-cap segment of the market, with over 80% coverage of U.S. equities, but is also considered a proxy for the total market.

The MSCI ACWI NR USD Index (MSCI ACWI) is an unmanaged free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ex-US Index captures the same opportunity set excluding the U.S.

Consumer Price Index (CPI) is an unmanaged index representing the rate of the inflation of U.S. consumer prices as determined by the U.S. Department of Labor Statistics. The CPI is presented to illustrate the Fund's purchasing power against changes in the prices of goods as opposed to a benchmark, which is used to compare the Fund's performance. There can be no guarantee that the CPI will reflect the exact level of inflation at any given time.

60% S&P500 / 40% Bloomberg US Aggregate Bond Index is a hypothetical combination of unmanaged indices and comprises 60% S&P 500 Index and 40% Bloomberg US Aggregate Bond Index.

60% MSCI ACWI / 40% Bloomberg US Aggregate Bond Index is a hypothetical combination of unmanaged indices and comprises 60% MSCI ACWI Index and 40% Bloomberg US Aggregate Bond Index.

7

S&P 500 Value Index is a subset of the S&P 500 index. Companies within the index are ranked based on growth and value factors including three-year change in earnings price/share, three-year sales/share growth rate, momentum, book value/price ratio, earnings/price ratio, sales/price ratio. The companies at the bottom of this list, that have a higher Value Rank, comprising 33% of the total index market capitalization are designated as the Value basket.

S&P 500 Growth Index is a subset of the S&P 500 index. Companies within the index are ranked based on growth and value factors including three-year change in earnings price/share, three-year sales/share growth rate, momentum, book value/price ratio, earnings/price ratio, sales/price ratio. The companies at the top of this list, that have a higher Growth Rank, comprising 33% of the total index market capitalization are designated as the Growth basket.

MSCI ACWI Value Index captures large and mid-cap securities exhibiting overall value style characteristics in Developed Markets countries and Emerging Markets countries. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield.

MSCI ACWI Growth Index captures large and mid-cap securities exhibiting overall growth style characteristics across Developed Markets (DM) countries and Emerging Markets (EM) countries. The growth investment style characteristics for index construction are defined using five variables: long-term forward EPS growth rate, short-term forward EPS growth rate, current internal growth rate and long-term historical EPS growth trend and long-term historical sales per share growth trend.

MSCI ACWI ex USA Index captures large and mid-cap representation across Developed Markets (DM) countries (excluding the US) and Emerging Markets (EM) countries.

MSCI EAFE Index is designed to represent the performance of large and mid-cap securities across 21 developed markets, including countries in Europe, Australasia and the Far East, excluding the U.S. and Canada.

MSCI Emerging Markets Index captures large and mid-cap representation across 24 Emerging Markets (EM) countries.

MSCI World Index captures large and mid-cap representation across 23 Developed Markets (DM) countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

Bloomberg US Aggregate Bond Index provides a measure of the performance of the US investment grade bonds market, which includes investment grade US Government bonds, investment grade corporate bonds, mortgage pass-through securities and asset-backed securities that are publicly offered for sale in the United States. The securities in the Index must have at least 1-year remaining in maturity. In addition, the securities must be denominated in US dollars and must be fixed rate, nonconvertible, and taxable.

Bloomberg US High Yield Index measures the market of USD-denominated, non-investment grade, fixed-rate, taxable corporate bonds.

Bloomberg US High Yield BB ex Energy Index measures the market of USD-denominated, non-investment grade, fixed-rate, taxable BB-rated corporate bonds excluding energy sector.

Bloomberg US Investment Grade Corporate Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility, and financial issuers.

Other Definitions

CAPE Ratio is a valuation measure that uses real earnings per share (EPS) over a 10-year period to smooth out fluctuations in corporate profits that occur over different periods of a business cycle.

Discount to Net Asset Value (NAV) is a pricing situation when a closed-end fund's market trading price is lower than its daily net asset value (NAV).

Dividend Yield, expressed as a percentage, is a financial ratio (dividend/price) that shows how much a company pays out in dividends each year relative to its stock price.

Earnings Per Share (EPS) is calculated as a company's profit divided by the outstanding shares of its common stock. The resulting number serves as an indicator of a company's profitability.

Earnings Per Share Growth is defined as the percentage change in normalized earnings per share over the previous 12-month period to the latest year end.

High Yield (HY) bond is a high paying bond with a lower credit rating (S&P and Fitch, BB+ and lower; Moody's, Ba1 or lower) than investment-grade corporate bonds, Treasury bonds and municipal bonds. Because of the higher risk of default, these bonds pay a higher yield than investment grade bonds.

Investment Grade (IG) is a rating (S&P and Fitch, BBB- and higher; Moody's Baa3 and higher) that indicates that a bond has a relatively low risk of default.

8

Market Capitalization refers to the total dollar market value of a company's outstanding shares of stock.

Market Cycles, also known as stock market cycles, is a wide term referring to trends or patterns that emerge during different markets or business environments.

Morningstar Large-Blend Category portfolios are fairly representative of the overall U.S. stock market in size, growth rates, and price. Stocks in the top 70% of the capitalization of the U.S. equity market are defined as large cap. The blend style is assigned to portfolios where neither growth nor value characteristics predominate. These portfolios tend to invest across the spectrum of U.S. industries, and owing to their broad exposure, the portfolios' returns are often similar to those of the S&P 500 Index. As of June 30, 2024, there were 324 funds in the category.

Morningstar Large-Growth Category portfolios are fairly representative of the overall U.S. stock market in size, growth rates, and price. Stocks in the top 70% of the capitalization of the U.S. equity market are defined as large cap. The growth style is assigned to portfolios where growth characteristics predominate. These portfolios tend to invest across the spectrum of U.S. industries, and owing to their broad exposure, the portfolios' returns are often similar to those of the S&P 500 Index. As of June 30, 2024, there were 318 funds in the category.

Morningstar Large-Value Category portfolios are fairly representative of the overall U.S. stock market in size, growth rates, and price. Stocks in the top 70% of the capitalization of the U.S. equity market are defined as large cap. The value style is assigned to portfolios where value characteristics predominate. These portfolios tend to invest across the spectrum of U.S. industries, and owing to their broad exposure, the portfolios' returns are often similar to those of the S&P 500 Index. As of June 30, 2024, there were 307 funds in the category.

Net Asset Value (NAV) represents the net value of a mutual fund and is calculated as the total value of the fund's assets minus the total value of its liabilities and is shown as a per share price.

Net Debt is calculated by subtracting a company's total cash and cash equivalents from its total short-term and long-term debt.

Net Income (NI), also called net earnings, is calculated as sales minus cost of goods sold, selling, general and administrative expenses, operating expenses, depreciation, interest, taxes, and other expenses.

Price to Book is used to compare a firm's market capitalization to its book value. It's calculated by dividing the company's stock price per share by its book value per share (BVPS). An asset's book value is equal to its carrying value on the balance sheet, and companies calculate it netting the asset against its accumulated depreciation.

Price to Earnings is the ratio for valuing a company that measures its current share price relative to its EPS. The price-to-earnings ratio is also sometimes known as the price multiple or the earnings multiple.

Trailing Price to Earnings is a relative valuation multiple that is based on the last 12 months of actual earnings.

Forward Price to Earnings is a version of the ratio of price-to-earnings (P/E) that uses forecasted earnings for the P/E calculation.

Risk Assets is any asset that carries a degree of risk. Risk asset generally refers to assets that have a significant degree of price volatility, such as equities, commodities, high-yield bonds, real estate, and currencies, but does not include cash and cash equivalents.

Shareholder Equity is a company's net worth and it is equal to the total dollar amount that would be returned to the shareholders if the company must be liquidated and all its debts are paid off. Thus, shareholder equity is equal to a company's total assets minus its total liabilities.

Standard Deviation is a measure of the dispersion of a set of data from its mean.

Volatility is a statistical measure of the dispersion of returns for a given security or market index. In most cases, the higher the volatility, the riskier the security. Volatility is often measured as either the standard deviation or variance between returns from that same security or market index.

Spread reflects the quoted spread of a bond that is relative to the security off which it is priced, typically an on the-run treasury.

Yield is the discount rate that links the bond's cash flows to its current dollar price.

Yield to Worst (YTW) is a measure of the lowest possible yield that can be received on a bond that fully operates within the terms of its contract without defaulting. It is a type of yield that is referenced when a bond has provisions that would allow the issuer to close it out before it matures.

9

SOURCE CAPITAL, INC.

SCHEDULE OF INVESTMENTS

As of June 30, 2024 (Unaudited)

BONDS & DEBENTURES — 29.8% | | Principal

Amount | | Value | |

ASSET-BACKED SECURITIES — 12.3% | |

COLLATERALIZED LOAN OBLIGATION — 6.5% | |

ABPCI Direct Lending Fund LLC

Series 2017-1A, Class ER, 13.186% (3-Month Term SOFR+786.161 basis points),

4/20/2032(a)(b) | | $ | 2,942,000 | | | $ | 2,941,673 | | |

Series 2016-1A, Class E2, 14.316% (3-Month Term SOFR+899.161 basis points),

7/20/2033(a)(b) | | | 2,056,000 | | | | 2,057,061 | | |

Barings Middle Market Ltd. Series 2021-IA, Class D, 14.236% (3-Month Term SOFR+891.161

basis points), 7/20/2033(a)(b) | | | 1,040,000 | | | | 1,040,483 | | |

BlackRock Maroon Bells LLC Series 2022-1A, Class E, 14.829% (3-Month Term SOFR+950

basis points), 10/15/2034(a)(b) | | | 3,243,750 | | | | 3,257,734 | | |

Fortress Credit Opportunities Ltd. Series 2017-9A, Class ER, 13.650% (3-Month Term

SOFR+832.161 basis points), 10/15/2033(a)(b) | | | 5,186,000 | | | | 5,186,223 | | |

Ivy Hill Middle Market Credit Fund Ltd.

Series 18A, Class E, 13.336% (3-Month Term SOFR+801.161 basis points), 4/22/2033(a)(b) | | | 3,464,000 | | | | 3,463,716 | | |

Series 12A, Class DR, 13.756% (3-Month Term SOFR+843.161 basis points), 7/20/2033(a)(b) | | | 814,000 | | | | 814,126 | | |

Series 20A, Class E, 15.325% (3-Month Term SOFR+1,000 basis points), 4/20/2035(a)(b) | | | 2,380,000 | | | | 2,417,004 | | |

Parliament Ltd. Series 2021-2A, Class D, 9.287% (3-Month Term SOFR+396.161 basis points),

8/20/2032(a)(b) | | | 1,854,000 | | | | 1,853,779 | | |

TCP Waterman LLC Series 2017-1A, Class ER, 13.748% (3-Month Term SOFR+842.161

basis points), 8/20/2033(a)(b) | | | 1,571,000 | | | | 1,571,806 | | |

| | | $ | 24,603,605 | | |

EQUIPMENT — 0.8% | |

Coinstar Funding LLC Series 2017-1A, Class A2, 5.216%, 4/25/2047(a) | | $ | 2,849,520 | | | $ | 2,509,794 | | |

Prop 2017-1A 5.300%, 3/15/2042(c)(d) | | | 335,102 | | | | 288,188 | | |

| | | $ | 2,797,982 | | |

OTHER — 5.0% | |

ABPCI Direct Lending Fund LLC Series 2022-2A, Class C, 8.236%, 3/1/2032(a) | | $ | 3,370,951 | | | $ | 3,134,418 | | |

ABPCI Direct Lending Fund Ltd.

Series 2020-1A, Class A, 3.199%, 12/20/2030(a) | | | 289,600 | | | | 285,430 | | |

Series 2020-1A, Class B, 4.935%, 12/20/2030(a) | | | 2,925,787 | | | | 2,852,241 | | |

Cologix Data Centers US Issuer LLC Series 2021-1A, Class C, 5.990%, 12/26/2051(a) | | | 1,765,000 | | | | 1,583,642 | | |

Diamond Infrastructure Funding LLC Series 2021-1A, Class C, 3.475%, 4/15/2049(a) | | | 384,000 | | | | 345,847 | | |

Diamond Issuer LLC Series 2021-1A, Class C, 3.787%, 11/20/2051(a) | | | 1,000,000 | | | | 847,883 | | |

Elm Trust Series 2020-3A, Class A2, 2.954%, 8/20/2029(a) | | | 31,629 | | | | 30,429 | | |

Series 2020-3A, Class B, 4.481%, 8/20/2029(a) | | | 85,003 | | | | 80,713 | | |

Series 2020-4A, Class B, 3.866%, 10/20/2029(a) | | | 543,439 | | | | 512,718 | | |

Golub Capital Partners Funding Ltd.

Series 2020-1A, Class B, 4.496%, 1/22/2029(a) | | | 956,987 | | | | 923,190 | | |

Series 2021-1A, Class B, 3.816%, 4/20/2029(a) | | | 1,397,493 | | | | 1,339,541 | | |

Series 2021-2A, Class B, 3.994%, 10/19/2029(a) | | | 3,339,965 | | | | 2,901,361 | | |

Hotwire Funding LLC Series 2021-1, Class C, 4.459%, 11/20/2051(a) | | | 750,000 | | | | 674,457 | | |

Monroe Capital Funding Ltd. Series 2021-1A, Class B, 3.908%, 4/22/2031(a) | | | 812,711 | | | | 781,086 | | |

TVEST LLC Series 2020-A, Class A, 4.500%, 7/15/2032(a) | | | 9,872 | | | | 9,848 | | |

VCP RRL Ltd.

Series 2021-1A, Class B, 2.848%, 10/20/2031(a) | | | 893,225 | | | | 829,105 | | |

Series 2021-1A, Class C, 5.425%, 10/20/2031(a) | | | 1,881,543 | | | | 1,712,037 | | |

| | | $ | 18,843,946 | | |

| TOTAL ASSET-BACKED SECURITIES (Cost $47,567,815) | | | | $ | 46,245,533 | | |

See accompanying Notes to Financial Statements.

10

SOURCE CAPITAL, INC.

SCHEDULE OF INVESTMENTS (Continued)

As of June 30, 2024 (Unaudited)

| BONDS & DEBENTURES (Continued) | | Principal

Amount | | Value | |

COMMERCIAL MORTGAGE-BACKED SECURITIES — 0.4% | |

AGENCY — 0.1% | |

Eleven Madison Mortgage Trust Series 2015-11MD, Class A, 3.673%, 9/10/2035(a)(b) | | $ | 344,000 | | | $ | 328,659 | | |

NON-AGENCY — 0.3% | |

BX Commercial Mortgage Trust Series 2021-VOLT, Class F, 7.843% (1-Month Term

SOFR+251.448 basis points), 9/15/2036(a)(b) | | $ | 1,311,000 | | | $ | 1,293,668 | | |

| TOTAL COMMERCIAL MORTGAGE-BACKED SECURITIES (Cost $1,617,958) | | | | $ | 1,622,327 | | |

CONVERTIBLE BONDS — 2.5% | |

Delivery Hero AG

1.000%, 4/30/2026 | | $ | 3,500,000 | | | $ | 3,383,632 | | |

1.000%, 1/23/2027 | | | 500,000 | | | | 442,906 | | |

1.500%, 1/15/2028 | | | 100,000 | | | | 82,471 | | |

3.250%, 2/21/2030 | | | 100,000 | | | | 93,171 | | |

Wayfair, Inc.

0.625%, 10/1/2025 | | | 5,078,000 | | | | 4,722,606 | | |

1.000%, 8/15/2026 | | | 122,000 | | | | 109,766 | | |

Zillow Group, Inc.

2.750%, 5/15/2025 | | | 48,000 | | | | 48,379 | | |

1.375%, 9/1/2026 | | | 350,000 | | | | 421,964 | | |

| TOTAL CONVERTIBLE BONDS (Cost $8,870,302) | | | | $ | 9,304,895 | | |

CORPORATE BANK DEBT — 4.7% | |

Axiom Global, Inc. 10.194% (1-Month USD Libor+475 basis points), 10/1/2026(b)(d)(e) | | $ | 1,708,790 | | | $ | 1,653,254 | | |

Capstone Acquisition Holdings, Inc. 2020 Delayed Draw Term Loan 10.194% (1-Month Term

SOFR+485 basis points), 11/12/2027(b)(c)(d)(e)(f) | | | 148,676 | | | | 141,426 | | |

Capstone Acquisition Holdings, Inc. 2020 Term Loan 10.194% (1-Month Term SOFR+485

basis points), 11/12/2027(b)(c)(d)(e) | | | 2,148,090 | | | | 2,043,347 | | |

CB&I STS Delaware LLC 13.096% (3-Month Term SOFR+776.2 basis points),

12/31/2026(b)(c)(d)(e)(g) | | | 2,208,134 | | | | 2,230,216 | | |

Cornerstone OnDemand, Inc. 9.343% (1-Month Term SOFR+375 basis points),

10/16/2028(b)(d)(e) | | | 72,698 | | | | 68,337 | | |

Element Commercial Funding LP 10.731% (1-Month Term SOFR+575 basis points),

9/15/2024(b)(c)(d)(e)(f) | | | 2,360,000 | | | | 2,341,741 | | |

Farfetch U.S. Holdings, Inc. 11.575% (3-Month Term SOFR+625 basis points),

10/20/2027(b)(d)(e) | | | 2,133,145 | | | | 1,978,492 | | |

Frontier Communications Holdings LLC 9.207% (1-Month Term SOFR+375 basis points),

10/8/2027(b)(d)(e) | | | 1,227,757 | | | | 1,224,688 | | |

JC Penney Corp., Inc. 5.568% (3-Month USD Libor+425 basis points), 6/23/2025*,(b)(c)(d)(e)(h) | | | 462,319 | | | | 46 | | |

Lealand Finance Company B.V. Senior Exit LC

3.500%, 6/30/2027(b)(c)(d)(e) | | | 1,493,118 | | | | (776,421 | ) | |

5.250%, 6/30/2027(b)(c)(d)(e)(f)(i) | | | 4,666,312 | | | | (1,633,209 | ) | |

Lealand Reficar LC Term Loan 12.798% (3-Month Term SOFR+750 basis points),

6/30/2027(b)(c)(d)(e) | | | 140,384 | | | | 91,250 | | |

Light Commercial Funding LP 11.153% (1-Month Term SOFR+600 basis points),

10/31/2026(b)(c)(d)(e)(f) | | | 1,480,000 | | | | 1,443,067 | | |

McDermott LC 9.593%, 6/30/2027(b)(c)(d)(e)(f) | | | 1,004,808 | | | | 522,500 | | |

McDermott Tanks Escrow LC 6.346% (3-Month Term SOFR+101.2 basis points),

12/31/2026(b)(c)(d)(e) | | | 228,693 | | | | 118,920 | | |

McDermott Tanks Secured LC 10.346% (3-Month Term SOFR+501.2 basis points),

12/31/2026(b)(c)(d)(e)(f)(i) | | | 2,513,909 | | | | (251,391 | ) | |

McDermott Technology Americas, Inc.

8.458% (1-Month Term SOFR+300 basis points), 6/30/2027(b)(d)(e) | | | 141,927 | | | | 78,060 | | |

9.457% (1-Month Term SOFR+400 basis points), 12/31/2027(b)(d)(e)(g) | | | 1,544,246 | | | | 679,468 | | |

See accompanying Notes to Financial Statements.

11

SOURCE CAPITAL, INC.

SCHEDULE OF INVESTMENTS (Continued)

As of June 30, 2024 (Unaudited)

| BONDS & DEBENTURES (Continued) | | Principal

Amount | | Value | |

Polaris Newco, LLC Term Loan B 9.343% (1-Month Term SOFR+400 basis points),

6/5/2028(b)(d)(e) | | $ | 1,133,935 | | | $ | 1,132,926 | | |

Project Myrtle 1.900% (1-Month Term SOFR+317.9 basis points), 6/15/2025(b)(c)(d)(e)(f)(i) | | | 3,000,000 | | | | 1,449,823 | | |

QBS Parent, Inc. 9.582% (3-Month Term SOFR+425 basis points), 9/22/2025(b)(d)(e) | | | 1,913,924 | | | | 1,867,664 | | |

Vision Solutions, Inc. 11.750% (3-Month Term SOFR+400 basis points), 4/24/2028(b)(d)(e) | | | 72,692 | | | | 71,511 | | |

WH Borrower LLC, Term Loan B 10.817% (1-Month Term SOFR+550 basis points),

2/16/2027(b)(d)(e) | | | 1,146,577 | | | | 1,117,913 | | |

Windstream Services LLC 11.694% (1-Month Term SOFR+625 basis points), 9/21/2027(b)(d)(e) | | | 250,424 | | | | 249,277 | | |

| TOTAL CORPORATE BANK DEBT (Cost $21,441,083) | | | | $ | 17,842,905 | | |

CORPORATE BONDS — 9.9% | |

COMMUNICATIONS — 1.0% | |

Consolidated Communications, Inc. 6.500%, 10/1/2028(a) | | $ | 1,272,000 | | | $ | 1,085,321 | | |

Frontier Communications Holdings LLC 5.875%, 10/15/2027(a) | | | 453,000 | | | | 441,109 | | |

Upwork, Inc. 0.250%, 8/15/2026 | | | 2,500,000 | | | | 2,217,715 | | |

| | | $ | 3,744,145 | | |

CONSUMER DISCRETIONARY — 0.7% | |

Air Canada Pass Through Trust Series 2020-1, Class C, 10.500%, 7/15/2026(a) | | $ | 1,500,000 | | | $ | 1,620,000 | | |

Cimpress PLC 7.000%, 6/15/2026 | | | 381,000 | | | | 380,459 | | |

VT Topco, Inc. 8.500%, 8/15/2030(a) | | | 421,000 | | | | 442,050 | | |

| | | $ | 2,442,509 | | |

ENERGY — 3.5% | |

Gulfport Energy Corp. 8.000%, 5/17/2026 | | $ | 11,736 | | | $ | 11,814 | | |

Tidewater, Inc.

8.500%, 11/16/2026 | | | 9,600,000 | | | | 9,972,000 | | |

10.375%, 7/3/2028(a) | | | 3,000,000 | | | | 3,225,000 | | |

| | | $ | 13,208,814 | | |

FINANCIALS — 3.3% | |

Apollo Debt Solutions BDC Senior Notes 8.620%, 9/28/2028(c)(d) | | $ | 2,333,000 | | | $ | 2,333,000 | | |

Blue Owl Credit Income Corp. 7.750%, 9/16/2027 | | | 2,243,000 | | | | 2,301,715 | | |

Charles Schwab Corp.

4.000% (USD 5 Year Tsy+316.8 basis points)(b)(j) | | | 549,000 | | | | 509,056 | | |

5.000% (3-Month USD Libor+257.5 basis points)(b)(j) | | | 75,000 | | | | 68,156 | | |

HPS Corporate Lending Fund 6.750%, 1/30/2029(a) | | | 520,000 | | | | 523,164 | | |

Midcap Financial Issuer Trust 6.500%, 5/1/2028(a) | | | 3,466,000 | | | | 3,266,705 | | |

Oaktree Strategic Credit Fund 8.400%, 11/14/2028(a) | | | 1,615,000 | | | | 1,704,027 | | |

OCREDIT BDC Senior Notes 7.770%, 3/7/2029(c)(d) | | | 552,000 | | | | 552,000 | | |

Vornado Realty LP

3.500%, 1/15/2025 | | | 1,000,000 | | | | 985,000 | | |

2.150%, 6/1/2026 | | | 250,000 | | | | 229,458 | | |

| | | $ | 12,472,281 | | |

HEALTH CARE — 0.5% | |

Heartland Dental LLC/Heartland Dental Finance Corp. 10.331% (1-Month Term SOFR+500

basis points), 4/30/2028(a)(d) | | $ | 1,796,000 | | | $ | 1,906,382 | | |

TECHNOLOGY — 0.9% | |

Hlend Senior Notes 8.170%, 3/15/2028(c)(d) | | $ | 3,500,000 | | | $ | 3,500,000 | | |

| TOTAL CORPORATE BONDS (Cost $36,368,033) | | | | $ | 37,274,131 | | |

| TOTAL BONDS & DEBENTURES (Cost $115,865,191) | | | | $ | 112,289,791 | | |

See accompanying Notes to Financial Statements.

12

SOURCE CAPITAL, INC.

SCHEDULE OF INVESTMENTS (Continued)

As of June 30, 2024 (Unaudited)

CLOSED-END FUNDS — 0.1% | | Number

of Shares | | Value | |

Altegrity, Inc.(c)(d) | | | 142,220 | | | $ | 331,373 | | |

| TOTAL CLOSED-END FUNDS (Cost $0) | | | | $ | 331,373 | | |

COMMON STOCKS — 39.7% | |

AEROSPACE & DEFENSE — 1.7% | |

Howmet Aerospace, Inc. | | | 23,249 | | | $ | 1,804,820 | | |

Safran S.A. | | | 21,166 | | | | 4,474,372 | | |

| | | $ | 6,279,192 | | |

APPAREL & TEXTILE PRODUCTS — 0.8% | |

Cie Financiere Richemont S.A. — Class A | | | 18,617 | | | $ | 2,905,993 | | |

ASSET MANAGEMENT — 0.2% | |

Groupe Bruxelles Lambert N.V. | | | 8,189 | | | $ | 584,490 | | |

Pershing Square Tontine Holdings Ltd.(c)(d) | | | 14,610 | | | | — | | |

| | | $ | 584,490 | | |

BANKING — 3.9% | |

Citigroup, Inc. | | | 134,615 | | | $ | 8,542,668 | | |

Wells Fargo & Co. | | | 105,255 | | | | 6,251,094 | | |

| | | $ | 14,793,762 | | |

BEVERAGES — 2.2% | |

Heineken Holding N.V. | | | 64,215 | | | $ | 5,064,719 | | |

JDE Peet's N.V. | | | 140,976 | | | | 2,808,046 | | |

Swire Pacific Ltd. — Class A | | | 62,216 | | | | 549,731 | | |

| | | $ | 8,422,496 | | |

CABLE & SATELLITE — 2.7% | |

Charter Communications, Inc. — Class A* | | | 5,983 | | | $ | 1,788,678 | | |

Comcast Corp. — Class A | | | 215,600 | | | | 8,442,896 | | |

| | | $ | 10,231,574 | | |

CHEMICALS — 2.0% | |

International Flavors & Fragrances, Inc. | | | 77,685 | | | $ | 7,396,389 | | |

COMMERCIAL SUPPORT SERVICES — 0.1% | |

Eurofins Scientific S.E. | | | 6,729 | | | $ | 335,441 | | |

Rentokil Initial PLC | | | 77 | | | | 449 | | |

| | | $ | 335,890 | | |

CONSTRUCTION MATERIALS — 2.7% | |

Holcim AG* | | | 115,552 | | | $ | 10,239,566 | | |

E-COMMERCE DISCRETIONARY — 0.9% | |

Alibaba Group Holding Ltd. | | | 28,187 | | | $ | 254,470 | | |

Amazon.com, Inc.* | | | 15,596 | | | | 3,013,927 | | |

| | | $ | 3,268,397 | | |

ELECTRIC UTILITIES — 0.7% | |

FirstEnergy Corp. | | | 68,180 | | | $ | 2,609,248 | | |

PG&E Corp. | | | 9,047 | | | | 157,961 | | |

| | | $ | 2,767,209 | | |

ELECTRICAL EQUIPMENT — 2.1% | |

TE Connectivity Ltd. | | | 53,212 | | | $ | 8,004,681 | | |

See accompanying Notes to Financial Statements.

13

SOURCE CAPITAL, INC.

SCHEDULE OF INVESTMENTS (Continued)

As of June 30, 2024 (Unaudited)

| COMMON STOCKS (Continued) | | Number

of Shares | | Value | |

ENGINEERING & CONSTRUCTION — 0.8% | |

McDermott International, Ltd.*,(c)(d) | | | 2,135,146 | | | $ | 619,193 | | |

Samsung C&T Corp. | | | 21,370 | | | | 2,204,533 | | |

| | | $ | 2,823,726 | | |

ENTERTAINMENT CONTENT — 0.7% | |

Epic Games, Inc.(c)(d) | | | 4,347 | | | $ | 1,156,302 | | |

Nexon Co., Ltd. | | | 83,639 | | | | 1,546,560 | | |

| | | $ | 2,702,862 | | |

HEALTH CARE FACILITIES & SVCS — 0.3% | |

ICON PLC* | | | 3,606 | | | $ | 1,130,373 | | |

INDUSTRIAL SUPPORT SERVICES — 1.1% | |

Ferguson PLC | | | 21,507 | | | $ | 4,164,831 | | |

INSURANCE — 1.3% | |

Aon PLC — Class A | | | 16,270 | | | $ | 4,776,547 | | |

INTERNET MEDIA & SERVICES — 5.2% | |

Alphabet, Inc. — Class A | | | 31,853 | | | $ | 5,802,024 | | |

Alphabet, Inc. — Class C | | | 19,721 | | | | 3,617,226 | | |

Delivery Hero S.E.* | | | 8,390 | | | | 199,013 | | |

Just Eat Takeaway.com N.V.* | | | 9,669 | | | | 116,332 | | |

Meta Platforms, Inc. — Class A | | | 10,387 | | | | 5,237,333 | | |

Netflix, Inc.* | | | 885 | | | | 597,269 | | |

Prosus N.V.* | | | 86,481 | | | | 3,080,272 | | |

Uber Technologies, Inc.* | | | 14,078 | | | | 1,023,189 | | |

| | | $ | 19,672,658 | | |

LEISURE FACILITIES & SERVICES — 0.9% | |

Entain PLC | | | 48,095 | | | $ | 383,009 | | |

Marriott International, Inc. — Class A | | | 12,342 | | | | 2,983,925 | | |

| | | $ | 3,366,934 | | |

METALS & MINING — 1.2% | |

Glencore PLC* | | | 788,595 | | | $ | 4,496,716 | | |

Metals Acquisition Corp. — Class A* | | | 4,213 | | | | 57,676 | | |

| | | $ | 4,554,392 | | |

OIL & GAS PRODUCERS — 1.1% | |

Gulfport Energy Corp.* | | | 6,110 | | | $ | 922,610 | | |

Kinder Morgan, Inc. | | | 160,090 | | | | 3,180,988 | | |

| | | $ | 4,103,598 | | |

REAL ESTATE SERVICES — 0.0% | |

Copper Property CTL Pass Through Trust(d) | | | 16,058 | | | $ | 146,288 | | |

RETAIL — DISCRETIONARY — 0.5% | |

CarMax, Inc.* | | | 23,348 | | | $ | 1,712,342 | | |

SEMICONDUCTORS — 4.3% | |

Analog Devices, Inc. | | | 41,465 | | | $ | 9,464,801 | | |

Broadcom, Inc. | | | 1,630 | | | | 2,617,014 | | |

NXP Semiconductors N.V. | | | 14,990 | | | | 4,033,659 | | |

| | | $ | 16,115,474 | | |

SOFTWARE — 0.0% | |

Windstream Holdings, Inc.(c) | | | 10,312 | | | $ | 134,056 | | |

See accompanying Notes to Financial Statements.

14

SOURCE CAPITAL, INC.

SCHEDULE OF INVESTMENTS (Continued)

As of June 30, 2024 (Unaudited)

| COMMON STOCKS (Continued) | | Number

of Shares | | Value | |

TECHNOLOGY HARDWARE — 0.7% | |

Nintendo Co., Ltd. | | | 49,244 | | | $ | 2,618,756 | | |

TECHNOLOGY SERVICES — 0.7% | |

LG Corp. | | | 44,825 | | | $ | 2,624,697 | | |

TRANSPORTATION & LOGISTICS — 0.4% | |

PHI Group, Inc.(c)(d) | | | 84,452 | | | $ | 1,689,040 | | |

TRANSPORTATION EQUIPMENT — 0.5% | |

Westinghouse Air Brake Technologies Corp. | | | 12,344 | | | $ | 1,950,969 | | |

| TOTAL COMMON STOCKS (Cost $95,703,803) | | | | $ | 149,517,182 | | |

LIMITED PARTNERSHIPS — 11.3% | |

Blue Torch Credit Opportunities Fund II LP(d)(k) | | | 55,000 | | | $ | 3,738,419 | | |

Clover Private Credit Opportunities Fund LP(d)(k) | | | 60,000 | | | | 4,115,318 | | |

HIG WhiteHorse Direct Lending 2020 LP(d)(k) | | | 55,000 | | | | 4,532,755 | | |

Metro Partners Fund VII LP(d)(k) | | | 80,000 | | | | 8,547,060 | | |

MSD Private Credit Opportunities Fund II LP(d)(k) | | | 80,000 | | | | 3,847,263 | | |

MSD Real Estate Credit Opportunities Fund(d)(k) | | | 30,000 | | | | 1,426,370 | | |

Nebari Natural Resources Credit Fund I LP(d)(k) | | | 55,000 | | | | 5,164,209 | | |

Piney Lake Opportunities Fund LP(d)(k) | | | 30,000 | | | | 3,077,477 | | |

Post Road Special Opportunity Fund II LP(d)(k) | | | 18,000 | | | | 1,646,357 | | |

Silverpeak Credit Opportunities LP(d)(k) | | | 34,745 | | | | 1,688,419 | | |

Silverpeak Special Situations(d)(k) | | | 48,500 | | | | 4,857,031 | | |

| TOTAL LIMITED PARTNERSHIPS (Cost $38,066,224) | | | | $ | 42,640,678 | | |

PREFERRED STOCKS — 0.1% | |

ENERGY — 0.0% | |

Gulfport Energy Corp., 10.000%(c) | | | 47 | | | $ | 43,892 | | |

INDUSTRIALS — 0.1% | |

McDermott International, Ltd., 8.000%(c)(d) | | | 909 | | | $ | 167,765 | | |

| TOTAL PREFERRED STOCKS (Cost $83,400) | | | | $ | 211,657 | | |

WARRANTS (SPAC) — 0.1% | |

American Oncology Network, Inc., Expiration Date: March 31, 2028* | | | 1,374 | | | $ | 41 | | |

Atlantic Coastal Acquisition Corp. II, Expiration Date: June 2, 2028* | | | 11,954 | | | | 717 | | |

BigBear.ai Holdings, Inc., Expiration Date: December 31, 2028* | | | 20,278 | | | | 3,194 | | |

Brand Engagement Network, Inc., Expiration Date: December 31, 2027* | | | 13,186 | | | | 425 | | |

BurTech Acquisition Corp., Expiration Date: December 18, 2026* | | | 94,574 | | | | 23,643 | | |

Churchill Capital Corp. VII, Expiration Date: February 29, 2028* | | | 9,384 | | | | 3,284 | | |

ECARX Holdings, Inc., Expiration Date: December 21, 2027* | | | 12,721 | | | | 438 | | |

Electriq Power Holdings, Inc., Expiration Date: January 25, 2028* | | | 31,567 | | | | 6 | | |

Global Partner Acquisition Corp. II, Expiration Date: December 30, 2027*,(c) | | | 4,908 | | | | — | | |

Golden Arrow Merger Corp., Expiration Date: July 31, 2027* | | | 26,146 | | | | 3,948 | | |

Heliogen, Inc., Expiration Date: March 31, 2028* | | | 7,538 | | | | 53 | | |

MariaDB PLC, Expiration Date: December 16, 2027* | | | 24,015 | | | | 2,498 | | |

NioCorp Developments Ltd., Expiration Date: March 17, 2028* | | | 16,476 | | | | 3,822 | | |

Northern Star Investment Corp. III, Expiration Date: February 24, 2028*,(c) | | | 6,999 | | | | 1 | | |

Northern Star Investment Corp. IV, Expiration Date: December 31, 2027*,(c) | | | 5,407 | | | | 1 | | |

Plum Acquisition Corp. I, Expiration Date: December 31, 2028* | | | 14,795 | | | | 1,258 | | |

Plum Acquisition Corp. III, Expiration Date: March 31, 2028* | | | 1,029 | | | | 67 | | |

See accompanying Notes to Financial Statements.

15

SOURCE CAPITAL, INC.

SCHEDULE OF INVESTMENTS (Continued)

As of June 30, 2024 (Unaudited)

| WARRANTS (Continued) | | Number

of Shares | | Value | |

PowerUp Acquisition Corp., Expiration Date: February 18, 2027* | | | 1,748 | | | $ | 48 | | |

Prenetics Global Ltd., Expiration Date: December 31, 2026* | | | 815 | | | | 11 | | |

Ross Acquisition Corp. II, Expiration Date: February 12, 2026*,(c) | | | 5,878 | | | | 530 | | |

Sable Offshore Corp., Expiration Date: December 31, 2028* | | | 39,217 | | | | 167,457 | | |

Slam Corp., Expiration Date: December 31, 2027* | | | 13,618 | | | | 3,404 | | |

Swvl Holdings Corp., Expiration Date: March 31, 2027* | | | 2,126 | | | | 30 | | |

| TOTAL WARRANTS (SPAC) (Cost $108,870) | | | | $ | 214,876 | | |

SHORT-TERM INVESTMENTS — 18.0% | |

MONEY MARKET INVESTMENTS — 18.0% | |

Morgan Stanley Institutional Liquidity Treasury Portfolio — Institutional Class, 5.06%(l) | | | 67,828,955 | | | $ | 67,828,955 | | |

| TOTAL SHORT-TERM INVESTMENTS (Cost $67,828,955) | | | | $ | 67,828,955 | | |

| TOTAL INVESTMENTS — 99.1% (Cost $317,656,443) | | | | $ | 373,034,512 | | |

Other Assets in Excess of Liabilities — 0.9% | | | | | 3,290,028 | | |

TOTAL NET ASSETS — 100.0% | | | | $ | 376,324,540 | | |

BDC — Business Development Company

LLC — Limited Liability Company

LP — Limited Partnership

PLC — Public Limited Company

US — United States

* Non-income producing security.

(a) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities are restricted and may be resold in transactions exempt from registration normally to qualified institutional buyers. The total value of these securities is $61,793,430, which represents 16.42% of Net Assets.

(b) Variable or floating rate security.

(c) The value of these securities was determined using significant unobservable inputs. These are reported as Level 3 securities in the Fair Value Hierarchy.

(d) Restricted securities. These restricted securities constituted 19.44% of total net assets at June 30, 2024, most of which are considered liquid by the Adviser. These securities are not registered and may not be sold to the public. There are legal and/or contractual restrictions on resale. The Fund does not have the right to demand that such securities be registered. The values of these securities are determined by valuations provided by pricing services, brokers, dealers, market makers, or in good faith under policies adopted by authority of the Fund's Board of Directors.

(e) Bank loans generally pay interest at rates which are periodically determined by reference to a base lending rate plus a premium. All loans carry a variable rate of interest. These base lending rates are generally (i) the Prime Rate offered by one or more major United States banks, (ii) the lending rate offered by one or more European banks such as the London Interbank Offered Rate ("LIBOR"), (iii) the Certificate of Deposit rate, or (iv) Secured Overnight Financing Rate ("SOFR"). Bank Loans, while exempt from registration, under the Securities Act of 1933, contain certain restrictions on resale and cannot be sold publicly. Floating rate bank loans often require prepayments from excess cash flow or permit the borrower to repay at its election. The degree to which borrowers repay, whether as a contractual requirement or at their election, cannot be predicted with accuracy.

(f) As of June 30, 2024, the Fund had entered into commitments to fund various delayed draw debt-related investments. Such commitments are subject to the satisfaction of certain conditions set forth in the documents governing those investments and there can be no assurance that such conditions will be satisfied. See Note 7 of the Notes to Financial Statements for further information on these commitments and contingencies.

(g) Payment-in-kind interest is generally paid by issuing additional par/shares of the security rather than paying cash.

(h) Security is in default.

(i) All or a portion of the loan is unfunded.

(j) Perpetual security. Maturity date is not applicable.

(k) Investment valued using net asset value per share (or its equivalent) as a practical expedient.

(l) The rate is the annualized seven-day yield at period end.

See accompanying Notes to Financial Statements.

16

SOURCE CAPITAL, INC.

SUMMARY OF INVESTMENTS

As of June 30, 2024 (Unaudited)

|

Security Type/Industry

|

|

Percent of Total

Net Assets |

|

|

Bonds & Debentures

|

|

|

Asset-Backed Securities

|

|

|

12.3

|

%

|

|

|

Corporate Bonds

|

|

|

9.9

|

%

|

|

|

Corporate Bank Debt

|

|

|

4.7

|

%

|

|

|

Convertible Bonds

|

|

|

2.5

|

%

|

|

|

Commercial Mortgage-Backed Securities

|

|

|

0.4

|

%

|

|

|

Total Bonds & Debentures

|

|

|

29.8

|

%

|

|

|

Closed-End Funds

|

|

|

0.1

|

%

|

|

|

Common Stocks

|

|

|

Internet Media & Services

|

|

|

5.2

|

%

|

|

|

Semiconductors

|

|

|

4.3

|

%

|

|

|

Banking

|

|

|

3.9

|

%

|

|

|

Construction Materials

|

|

|

2.7

|

%

|

|

|

Cable & Satellite

|

|

|

2.7

|

%

|

|

|

Beverages

|

|

|

2.2

|

%

|

|

|

Electrical Equipment

|

|

|

2.1

|

%

|

|

|

Chemicals

|

|

|

2.0

|

%

|

|

|

Aerospace & Defense

|

|

|

1.7

|

%

|

|

|

Insurance

|

|

|

1.3

|

%

|

|

|

Metals & Mining

|

|

|

1.2

|

%

|

|

|

Industrial Support Services

|

|

|

1.1

|

%

|

|

|

Oil & Gas Producers

|

|

|

1.1

|

%

|

|

|

Leisure Facilities & Services

|

|

|

0.9

|

%

|

|

|

E-Commerce Discretionary

|

|

|

0.9

|

%

|

|

|

Apparel & Textile Products

|

|

|

0.8

|

%

|

|

|

Engineering & Construction

|

|

|

0.8

|

%

|

|

|

Electric Utilities

|

|

|

0.7

|

%

|

|

|

Entertainment Content

|

|

|

0.7

|

%

|

|

|

Technology Services

|

|

|

0.7

|

%

|

|

|

Technology Hardware

|

|

|

0.7

|

%

|

|

|

Transportation Equipment

|

|

|

0.5

|

%

|

|

|

Retail — Discretionary

|

|

|

0.5

|

%

|

|

|

Transportation & Logistics

|

|

|

0.4

|

%

|

|

|

Health Care Facilities & Svcs

|

|

|

0.3

|

%

|

|

|

Asset Management

|

|

|

0.2

|

%

|

|

|

Commercial Support Services

|

|

|

0.1

|

%

|

|

|

Real Estate Services

|

|

|

0.0

|

%

|

|

|

Software

|

|

|

0.0

|

%

|

|

|

Total Common Stocks

|

|

|

39.7

|

%

|

|

|

Preferred Stocks

|

|

|

Industrials

|

|

|

0.1

|

%

|

|

|

Energy

|

|

|

0.0

|

%

|

|

|

Total Preferred Stocks

|

|

|

0.1

|

%

|

|

|

Limited Partnerships

|

|

|

11.3

|

%

|

|

|

Warrants (SPAC)

|

|

|

0.1

|

%

|

|

|

Short-Term Investments

|

|

|

18.0

|

%

|

|

|

Total Investments

|

|

|

99.1

|

%

|

|

|

Other Assets in Excess of Liabilities

|

|

|

0.9

|

%

|

|

|

Total Net Assets

|

|

|

100.0

|

%

|

|

See accompanying Notes to Financial Statements.

17

SOURCE CAPITAL, INC.

STATEMENT OF ASSETS AND LIABILITIES

As of June 30, 2024

(Unaudited)

|

ASSETS

|

|

|

Investments, at value (cost $317,656,443)

|

|

$

|

373,034,512

|

|

|

|

Foreign currency, at value (cost $33,973)

|

|

|

33,957

|

|

|

|

Cash

|

|

|

1,639

|

|

|

|

Deposits held at broker

|

|

|

1,058,715

|

|

|

|

Receivables:

|

|

|

Investment securities sold

|

|

|

983,692

|

|

|

|

Dividends and interest

|

|

|

2,139,293

|

|

|

|

Reclaims receivable

|

|

|

243,356

|

|

|

|

Total assets

|

|

|

377,495,164

|

|

|

|

LIABILITIES

|

|

|

Payables:

|

|

|

Investment securities purchased

|

|

|

748,934

|

|

|

|

Advisory fees

|

|

|

253,246

|

|

|

|

Fund services fees

|

|

|

106,743

|

|

|

|

Auditing fees

|

|

|

14,918

|

|

|

|

Shareholder reporting fees

|

|

|

8,166

|

|

|

|

Directors' fees and expenses

|

|

|

4,291

|

|

|

|

Legal fees

|

|

|

3,174

|

|

|

|

Chief Compliance Officer fees

|

|

|

897

|

|

|

|

Accrued other expenses

|

|

|

30,255

|

|

|

|

Total liabilities

|

|

|

1,170,624

|

|

|

|

Commitments and contingencies (Note 7)

|

|

|

NET ASSETS

|

|

$

|

376,324,540

|

|

|

|

COMPONENTS OF NET ASSETS

|

|

|

Capital Stock — par value $1 per share; authorized 12,000,000 shares; outstanding 8,199,745 shares

|

|

$

|

312,748,892

|

|

|

|

Total distributable earnings (accumulated deficit)

|

|

|

63,575,648

|

|

|

|

NET ASSETS

|

|

$

|

376,324,540

|

|

|

|

Number of shares issued and outstanding

|

|

|

8,199,745

|

|

|

|

Net asset value per share

|

|

$

|

45.89

|

|

|

|

Market price per share

|

|

|

44.26

|

|

|

See accompanying Notes to Financial Statements.

18

SOURCE CAPITAL, INC.

STATEMENT OF OPERATIONS

For the six months ended June 30, 2024

(Unaudited)

INVESTMENT INCOME | |

Interest | | $ | 7,435,803 | | |

Dividends (net of foreign withholding taxes of $50,537) | | | 2,910,321 | | |

Total investment income | | | 10,346,124 | | |

EXPENSES | |

Advisory fees | | | 1,320,155 | | |

Fund services fees | | | 216,242 | | |

Tax fees | | | 55,267 | | |

Shareholder reporting fees | | | 45,734 | | |

Miscellaneous | | | 30,145 | | |

Registration fees | | | 12,434 | | |

Directors' fees and expenses | | | 11,567 | | |

Auditing fees | | | 8,034 | | |

Legal fees | | | 5,229 | | |

Insurance fees | | | 4,944 | | |

Chief Compliance Officer fees | | | 1,070 | | |

Total expenses | | | 1,710,821 | | |

Net investment income (loss) | | | 8,635,303 | | |

REALIZED AND UNREALIZED GAIN (LOSS) | |

Net realized gain (loss) on: | |

Investments | | | 5,612,710 | | |

Foreign currency transactions | | | 9,573 | | |

Total realized gain (loss) | | | 5,622,283 | | |

Net change in unrealized appreciation (depreciation) on: | |

Investments | | | 12,231,890 | | |

Foreign currency translations | | | (9,872 | ) | |

Net change in unrealized appreciation (depreciation) | | | 12,222,018 | | |

Net realized and unrealized gain (loss) | | | 17,844,301 | | |

NET INCREASE (DECREASE) IN NET ASSETS FROM OPERATIONS | | $ | 26,479,604 | | |

See accompanying Notes to Financial Statements.

19

SOURCE CAPITAL, INC.

STATEMENTS OF CHANGES IN NET ASSETS

| |

|

For the

six months ended

June 30, 2024

(Unaudited) |

|

For the

year ended

December 31, 2023 |

|

|

INCREASE (DECREASE) IN NET ASSETS FROM

|

|

|

Operations:

|

|

|

Net investment income (loss)

|

|

$

|

8,635,303

|

|

|

$

|

16,191,801

|

|

|

|

Total realized gain (loss) on investments and foreign currency transactions

|

|

|

5,622,283

|

|

|

|

11,144,279

|

|

|

Net change in unrealized appreciation (depreciation) on investments and foreign

currency translations |

|

|

12,222,018

|

|

|

|

26,302,922

|

|

|

|

Net increase (decrease) in net assets resulting from operations

|

|

|

26,479,604

|

|

|

|

53,639,002

|

|

|

|

Distributions to Shareholders:

|

|

|

Distributions

|

|

|

(10,249,397

|

)

|

|

|

(24,019,810

|

)

|

|

|

Total distributions to shareholders

|

|

|

(10,249,397

|

)

|

|

|

(24,019,810

|

)

|

|

|

Capital Transactions:

|

|

|

Cost of capital stock

|

|

|

(319,255

|

)

|

|

|

(4,038,102

|

)

|

|

|

Net increase (decrease) in net assets from capital transactions

|

|

|

(319,255

|

)

|

|

|

(4,038,102

|

)

|

|

|

Total increase (decrease) in net assets

|

|

|

15,910,952

|

|

|

|

25,581,090

|

|

|

|

NET ASSETS

|

|

|

Beginning of period

|

|

|

360,413,588

|

|

|

|

334,832,498

|

|

|

|

End of period

|

|

$

|

376,324,540

|

|

|

$

|

360,413,588

|

|

|

|

CAPITAL SHARE TRANSACTIONS

|

|

|

Shares of capital stock repurchased

|

|

|

(7,968

|

)

|

|

|

(106,018

|

)

|

|

|

Net increase (decrease) in capital share transactions

|

|

|

(7,968

|

)

|

|

|

(106,018

|

)

|

|

See accompanying Notes to Financial Statements.

20

SOURCE CAPITAL, INC.

FINANCIAL HIGHLIGHTS

Per share operating performance. For a capital share outstanding throughout each period.

| |

|

For the

six months

ended

June 30,

2024 |

|

For the year ended December 31,

|

|

| |

|

(Unaudited)

|

|

2023

|

|

2022(1)

|

|

2021(1)

|

|

2020(1)

|

|

2019(1)

|

|

|

Net asset value, beginning of period

|

|

$

|

43.91

|

|

|

$

|

40.27

|

|

|

$

|

45.70

|

|

|

$

|

45.35

|

|

|

$

|

44.44

|

|

|

$

|

37.66

|

|

|

|

Income from Investment Operations:

|

|

|

Net investment income(2)

|

|

$

|

1.05

|

|

|

$

|

1.96

|

|

|

$

|

1.16

|

|

|

$

|

0.99

|

|

|

$

|

0.70

|

|

|

$

|

0.72

|

|

|

|

Net realized and unrealized gain (loss)

|

|

|

2.18

|

|

|

|

4.54

|

|

|

|

(4.40

|

)

|

|

|

3.94

|

|

|

|

1.82

|

|

|

|

7.02

|

|

|

|

Total from investment operations

|

|

$

|

3.23

|

|

|

$

|

6.50

|

|

|

$

|

(3.24

|

)

|

|

$

|

4.93

|

|

|

$

|

2.52

|

|

|

$

|

7.74

|

|

|

|

Less Distributions:

|

|

|

From net investment income

|

|

$

|

(1.25

|

)

|

|

$

|

(2.09

|

)

|

|

$

|

(1.06

|

)

|

|

$

|

(2.02

|

)

|

|

$

|

(1.00

|

)

|

|

$

|

(1.00

|

)

|

|

|

From net realized gains

|

|

|

—

|

|

|

|

(0.82

|

)

|

|

|

(1.16

|

)

|

|

|

(2.59

|

)

|

|

|

(0.64

|

)

|

|

|

—

|

|

|

|

Total distributions

|

|

$

|

(1.25

|

)

|

|

$

|

(2.91

|

)

|

|

$

|

(2.22

|

)

|

|

$

|

(4.61

|

)

|

|

$

|

(1.64

|

)

|

|

$

|

(1.00

|

)

|

|

|

Capital stock repurchased

|

|

$

|

0.00

|

(3)

|

|

$

|

0.05

|

|

|

$

|

0.03

|

|

|

$

|

0.03

|

|

|

$

|

0.03

|

|

|

$

|

0.04

|

|

|

|

Net asset value, end of period

|

|

$

|

45.89

|

|

|

$

|

43.91

|

|

|

$

|

40.27

|

|

|

$

|

45.70

|

|

|

$

|

45.35

|

|

|

$

|

44.44

|

|

|

|

Per share market value at end of period

|

|

$

|

44.26

|

|

|

$

|

40.38

|

|

|

$

|

38.66

|

|

|

$

|

43.21

|

|

|

$

|

39.91

|

|

|

$

|

38.69

|

|

|

|

Total investment return(4)

|

|

|

12.87

|

%

|

|

|

12.46

|

%

|

|

|

(5.28

|

)%

|

|

|

19.95

|

%

|

|

|

7.79

|

%

|

|

|

22.11

|

%

|

|

|

Net asset value total return(5)

|

|

|

7.47

|

%

|

|

|

16.74

|

%

|

|

|

(7.09

|

)%

|

|

|

11.16

|

%

|

|

|

5.98

|

%

|

|

|

20.89

|

%

|

|

|

Ratios and Supplemental Data:

|

|

|

Net assets, end of period (in thousands)

|

|

$

|

376,325