Filed by AltC Acquisition Corp.

pursuant to Rule 425 under the Securities Act

of 1933

and deemed filed pursuant to Rule 14a-12

under the Securities Exchange Act of 1934

Subject Company: AltC Acquisition Corp.

Commission File No. 001-40583

Date: July 20, 2023

On July 11, 2023, AltC Acquisition Corp. (“AltC”) announced

that it had entered into a definitive agreement for a business combination with Oklo Inc. (the “Business Combination”). On

July 20, 2023, AltC made available the following updated investor presentation relating to the Business Combination:

Investor Presentation July 2023 Oklo’s Aurora powerhouse 15 MWe liquid metal fast fission power plant site and fuel secured for commercial plant deployment at the Idaho National Laboratory (“INL”) to go public in partnership with Alt C Acquisition Corp. Experimental Breeder Reactor II (“ EBR - II”) The inspiration for the Aurora powerhouse Digital rendering for illustrative purposes only

| Alt C Acquisition Corp. 2 About this presentation This presentation is provided for informational purposes only and has been prepared to assist interested parties in making their own evaluation with respect to a potential transaction (the “proposed transaction”) between Oklo Inc . (“Oklo”) and AltC Acquisition Corp . (“ AltC ”) and related transactions and for no other purpose . The information contained herein does not purport to be all inclusive and no representations or warranties, express or implied, are given in, or in respect of, this presentation . To the fullest extent permitted by law, in no circumstances will Oklo, AltC or any of their respective subsidiaries, interest holders, affiliates, representatives, partners, directors, officers, employees, advisers or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of this presentation, its contents, its omissions, reliance on the information contained within it, or on opinions communicated in relation thereto or otherwise arising in connection therewith . Forward - Looking Statements This communication includes “forward - looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995 . Forward - looking statements may be identified by the use of words such as “estimate,” “plan,” “project,” “forecast,” “intend,” “will,” “expect,” “anticipate,” “believe,” “seek,” “target,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict” or other similar expressions that predict or indicate future events or trends or that are not statements of historical matters . We have based these forward - looking statements on our current expectations and projections about future events . These forward - looking statements include, but are not limited to, statements regarding estimates and forecasts of financial and operational metrics ; estimates and projections regarding future manufacturing capacity and plant performance ; estimates and projections of market opportunity and market share ; estimates and projections of adjacent energy sector opportunities ; Oklo’s projected commercialization costs and timeline ; Oklo’s ability to demonstrate scientific and engineering feasibility of its technologies ; Oklo’s ability to attract, retain, and expand its future customer base ; Oklo’s ability to timely and effectively meet construction timelines and scale its production and manufacturing processes ; Oklo’s ability to develop products and services and bring them to market in a timely manner ; Oklo’s ability to achieve a competitive levelized cost of electricity ; Oklo’s ability to compete successfully with fission energy products and solutions offered by other companies, including fusion, as well as with other sources of clean energy ; Oklo’s expectations concerning relationships with strategic partners, suppliers, governments, regulatory bodies and other third parties ; Oklo’s ability to maintain, protect, and enhance its intellectual property ; future ventures or investments in companies or products, services, or technologies ; Oklo’s ability to attract and retain qualified employees ; development of favorable regulations and government incentives affecting the markets in which Oklo operates ; Oklo’s expectations regarding regulatory framework development ; the potential for and timing of receipt of a license to operate nuclear facilities from the U . S . Nuclear Regulatory Commission ; the ability to achieve the results illustrated in the unit economics ; the potential benefits of the proposed transaction and expectations related to the terms and timing of the proposed transaction ; and the success of proposed projects for which Oklo’s powerhouses would provide power, which is outside of Oklo’s control . These statements are based on various assumptions, whether or not identified in this communication, and on the current expectations of Oklo’s and AltC’s management and are not predictions of actual performance . These forward - looking statements are provided for illustrative purposes only and are not intended to serve as and must not be relied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability . Actual events and circumstances are difficult or impossible to predict and will differ from assumptions . Many actual events and circumstances are beyond the control of Oklo and AltC . These forward - looking statements are subject to known and unknown risks, uncertainties and assumptions about us that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward - looking statements . Such risks and uncertainties include changes in domestic and foreign business, the risk that Oklo is pursuing an emerging market, with no commercial project operating, regulatory uncertainties, the fact that Oklo has not entered into any definitive agreements with customers for the sale of power or recycling of nuclear fuel, the potential need for financing to construct plants, market, financial, political and legal conditions ; the inability of the parties to successfully or timely consummate the proposed transaction, including the risk that any required regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect the combined company or the expected benefits of the proposed transaction or that the approval of the shareholders of AltC or Oklo is not obtained ; the risk that shareholders of AltC could elect to have their shares redeemed by AltC , thus leaving the combined company insufficient cash to grow its business ; the outcome of any legal proceedings that may be instituted against Oklo or AltC following announcement of the proposed transaction ; failure to realize the anticipated benefits of the proposed transaction ; risks relating to the uncertainty of the projected financial information with respect to Oklo ; the effects of competition ; changes in applicable laws or regulations ; the ability of Oklo to manage expenses and recruit and retain key employees ; the ability of AltC or the combined company to issue equity or equity - linked securities in connection with the proposed transaction or in the future ; the outcome of any potential litigation, government and regulatory proceedings, investigations and inquiries ; and the impact of the global COVID - 19 pandemic on Oklo, AltC , the combined company’s projected results of operations, financial performance or other financial metrics, or on any of the foregoing risks ; those factors discussed in AltC’s Quarterly Reports filed by AltC with the U . S . Securities and Exchange Commission (“SEC”) on Form 10 - Q and the Annual Reports filed by AltC with the SEC on Form 10 - K, in each case, under the heading “Risk Factors,” as well as the factors summarized in this presentation under “Risk Factors” and other documents filed, or to be filed, with the SEC by AltC . If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward - looking statements . There may be additional risks that neither Oklo nor AltC presently know or that Oklo and AltC currently believe are immaterial that could also cause actual results to differ from those contained in the forward - looking statements . In addition, forward - looking statements reflect Oklo’s and AltC’s expectations, plans or forecasts of future events and views as of the date of this communication . Oklo and AltC anticipate that subsequent events and developments will cause Oklo’s and AltC’s assessments to change . However, while Oklo and AltC may elect to update these forward - looking statements at some point in the future, Oklo and AltC specifically disclaim any obligation to do so . These forward - looking statements should not be relied upon as representing Oklo’s and AltC’s assessments as of any date subsequent to the date of this communication . Accordingly, undue reliance should not be placed upon the forward - looking statements . An investment in AltC is not an investment in any of our founders' or sponsors' past investments or companies or any funds affiliated with any of the foregoing . The historical results of these investments are not indicative of future performance of AltC , which may differ materially from the performance of the founders or sponsors past investments, companies or affiliated funds . Additional Information About the Proposed Transaction and Where to Find It The proposed transaction will be submitted to shareholders of AltC for their consideration . AltC intends to file a registration statement on Form S - 4 (the “Registration Statement”) with the SEC, which will include preliminary and definitive proxy statements to be distributed to AltC’s shareholders in connection with AltC’s solicitation for proxies for the vote by AltC’s shareholders in connection with the proposed transaction and other matters to be described in the Registration Statement, as well as the prospectus relating to the offer of the securities to be issued to Oklo’s shareholders in connection with the completion of the proposed transaction . After the Registration Statement has been filed and declared effective, AltC will mail a definitive proxy statement/prospectus/consent solicitation statement and other relevant documents to its shareholders as of the record date established for voting on the proposed transaction . AltC’s shareholders and other interested persons are advised to read, once available, the preliminary proxy statement/prospectus/consent solicitation statement and any amendments thereto and, once available, the definitive proxy statement/prospectus/consent solicitation statement, in connection with AltC’s solicitation of proxies for its special meeting of shareholders to be held to approve, among other things, the proposed transaction, as well as other documents filed with the SEC by AltC in connection with the proposed transaction, as these documents will contain important information about AltC , Oklo and the proposed transaction . Shareholders may obtain a copy of the preliminary or definitive proxy statement/prospectus/consent solicitation statement, once available, as well as other documents filed by AltC with the SEC, without charge, at the SEC’s website located at www . sec . gov or by directing a written request to AltC Acquisition Corp . , 640 Fifth Avenue, 12 th Floor, New York, NY 10019 .

| Alt C Acquisition Corp. 3 About this presentation Participants in the Solicitation AltC , Oklo and certain of their respective directors, executive officers and other members of management and employees may, under SEC rules, be deemed to be participants in the solicitation of proxies from AltC’s shareholders in connection with the proposed transaction . Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of AltC’s shareholders in connection with the proposed transaction will be set forth in AltC’s proxy statement/prospectus/consent solicitation statement when it is filed with the SEC . You can find more information about AltC’s directors and executive officers in AltC’s final prospectus filed with the SEC on July 7 , 2021 and in the Annual Reports filed by AltC with the SEC on Form 10 - K . Additional information regarding the participants in the proxy solicitation and a description of their direct and indirect interests will be included in the proxy statement/prospectus/consent solicitation statement when it becomes available . Shareholders, potential investors and other interested persons should read the proxy statement/prospectus/consent solicitation statement carefully when it becomes available before making any voting or investment decisions . You may obtain free copies of these documents from the sources indicated above . No Offer or Solicitation This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction . This communication is not, and under no circumstances is to be construed as, a prospectus, an advertisement or a public offering of the securities described herein in the United States or any other jurisdiction . No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933 , as amended, or exemptions therefrom . INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN . ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE . Unit Economics and Use of Projections The unit economics in this presentation (“Unit Economics”) were prepared solely for internal use and not with a view toward public disclosure or toward complying with Generally Accepted Accounting Principles, any published guidelines of the SEC or any guidelines established by the American Institute of Certified Public Accountants . The Unit Economics have been prepared by Oklo’s financial advisors and are the responsibility of Oklo’s management . The Unit Economics constitute forward - looking information, and is for illustrative purposes only, and should not be relied upon as necessarily being indicative of future results . The assumptions and estimates underlying the Unit Economics are inherently uncertain and are subject to a wide variety of significant business, economic, competitive, and other risks and uncertainties . See “Forward - Looking Statements” earlier in this presentation as well as “Risk Factors” at the end of this presentation . Actual results may differ materially from the results contemplated by Unit Economics contained in this presentation, and the inclusion of such information in this presentation should not be regarded as a representation by any person that the results reflected by the Unit Economics will be achieved . No Incorporation by Reference The information contained in the third party citations referenced in this communication is not incorporated by reference into this communication . Trademarks This presentation contains trademarks, service marks, trade names and copyrights of AltC , Oklo and other companies, which are the property of their respective owners . Risk Factors For a description of certain risks relating to Oklo, including its business and operations, and the proposed transaction, we refer you to “Risk Factors” at the end of this presentation .

| Alt C Acquisition Corp. 4 Introduction video Click image to view video | Alt C Acquisition Corp.

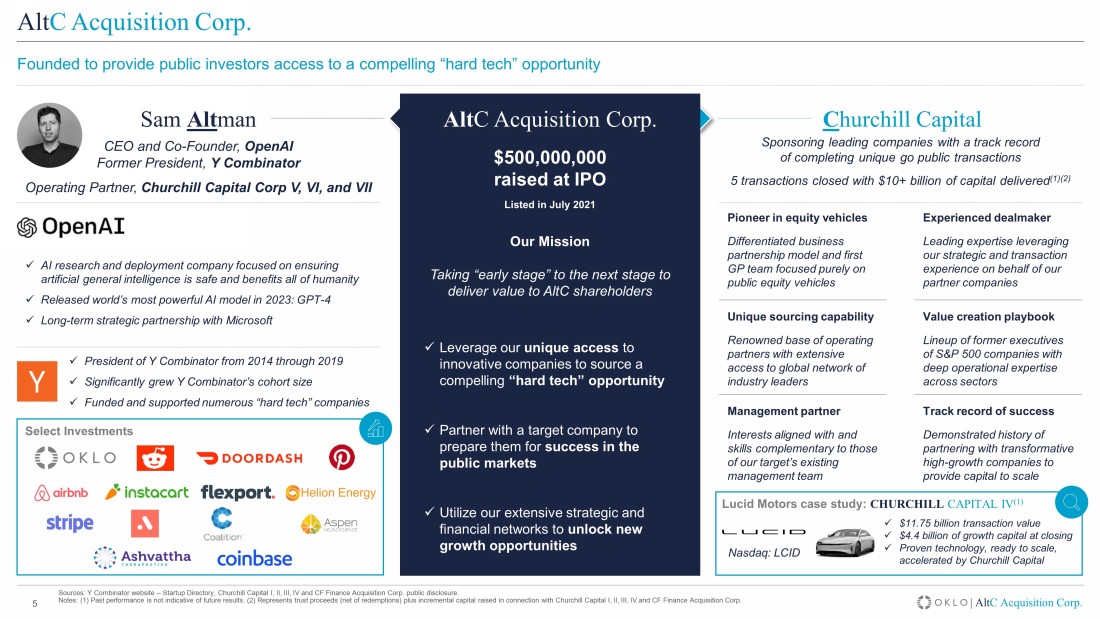

| Alt C Acquisition Corp. Sources: Y Combinator website – Startup Directory, Churchill Capital I, II, III, IV and CF Finance Acquisition Corp. public disc losure. Notes: (1) Past performance is not indicative of future results. (2) Represents trust proceeds (net of redemptions) plus incr eme ntal capital raised in connection with Churchill Capital I, II, III, IV and CF Finance Acquisition Corp. 5 Alt C Acquisition Corp. Alt C Acquisition Corp. $500,000,000 raised at IPO Listed in July 2021 Our Mission Taking “early stage” to the next stage to deliver value to AltC shareholders x Leverage our unique access to innovative companies to source a compelling “hard tech” opportunity x Partner with a target company to prepare them for success in the public markets x Utilize our extensive strategic and financial networks to unlock new growth opportunities C hurchill Capital Sam Alt man Sponsoring leading companies with a track record of completing unique go public transactions 5 transactions closed with $10+ billion of capital delivered (1)(2) Pioneer in equity vehicles Differentiated business partnership model and first GP team focused purely on public equity vehicles Experienced dealmaker Leading expertise leveraging our strategic and transaction experience on behalf of our partner companies Unique sourcing capability Renowned base of operating partners with extensive access to global network of industry leaders Value creation playbook Lineup of former executives of S&P 500 companies with deep operational expertise across sectors Track record of success Demonstrated history of partnering with transformative high - growth companies to provide capital to scale Management partner Interests aligned with and skills complementary to those of our target’s existing management team Lucid Motors case study: CHURCHILL CAPITAL IV (1) Nasdaq: LCID x $11.75 billion transaction value x $4.4 billion of growth capital at closing x Proven technology, ready to scale, accelerated by Churchill Capital CEO and Co - Founder, OpenAI Former President, Y Combinator Operating Partner, Churchill Capital Corp V, VI, and VII Select Investments x AI research and deployment company focused on ensuring artificial general intelligence is safe and benefits all of humanity x Released world’s most powerful AI model in 2023: GPT - 4 x Long - term strategic partnership with Microsoft Founded to provide public investors access to a compelling “hard tech” opportunity x President of Y Combinator from 2014 through 2019 x Significantly grew Y Combinator’s cohort size x Funded and supported numerous “hard tech” companies

| Alt C Acquisition Corp. 6 Advancing atomic energy has been a long - standing investment focus of Sam Altman… …and nuclear technology was set as a “hard tech” vertical of interest for AltC at formation Energy Sam Altman June 29 , 2015 ( 1 ) I think a lot about how important cheap, safe, and abundant energy is to our future . A lot of problems – economic, environmental, war, poverty, food and water availability, bad side effects of globalization, etc . – are deeply related to the energy problem . I believe that if you could choose one single technological development to help the most people in the world, radically better energy generation is probably it . Throughout history, quality of life has gone up as the cost of energy has gone down . The 20 th century was the century of carbon - based energy . I am confident the 22 nd century is going to be the century of atomic energy (i . e . terrestrial atomic generation and energy relatively directly from the sun’s fusion) . I am unsure how the majority of the 21 st century will be powered, but I’d like to help get things moving . Although a lot of people are working on solar, I don’t think enough people are working on terrestrial - based atomic energy , which has major advantages when it comes to cost, density, and predictability . Given the potential importance, I’m making an exception to my normal policy of not joining YC boards for Helion and Oklo . Both of these companies went through YC about a year ago . Helion is working on fusion and Oklo is working on fission ; I’ve looked at many companies working on both and think these are the two best . I’ll be the chairman of both companies and I’m also investing in the seed/A rounds for both companies . “ ” Source: (1) https://blog.samaltman.com/energy. | AltC Acquisition Corp.

| Alt C Acquisition Corp. 7 Partnership team Jacob DeWitte Co - Founder and CEO Co - Founded Oklo in 2013 • 15+ years of experience in nuclear technology • PhD in nuclear engineering, MIT • Prior experiences at GE, Sandia National Labs, Urenco U.S., and the U.S. Naval Nuclear Laboratory Caroline Cochran Co - Founder and COO Co - Founded Oklo in 2013 • 15+ years of experience in nuclear technology • MS in nuclear engineering, MIT • Prior experiences in the Office of the Secretary of Defense and U.S. Department of Energy Nuclear Energy Advisory Committee Alt C Acquisition Corp. Michael Klein Co - Founder and Chairman • Founder, Churchill Capital and Archimedes Advisors • Managing Partner, M. Klein & Company • Former Vice Chairman and CEO of Global Banking, Citi CHURCHILL CAPITAL Sam Altman Co - Founder, CEO, and Director Initial lead investor in Oklo and Chairman since 2015 • CEO and Co - Founder, OpenAI • Former President, Y Combinator • Operating Partner, Churchill Capital Corp V, VI and VII • Thought leader in artificial intelligence and energy technology

| Alt C Acquisition Corp. Oklo to go public in partnership with AltC 1 6 Power sales: targeting profitable recurring revenue Fuel recycling: embedded potential upside opportunity Compelling anticipated unit economics Simple transaction with an attractive valuation Importance of clean, reliable, and abundant energy 2 3 4 5 Agenda

| Alt C Acquisition Corp. Note: (1) AltC cash - in - trust was $515,791,749 as of June 30, 2023. For illustrative purposes only. Assumes no AltC shareholders exercise their redemption rights to receive cash from the trust account at closing. 9 Oklo to go public in partnership with AltC Acquisition Corp. AltC ( NYSE: ALCC ) proposes to combine with Oklo at an $850 million pre - money equity value with net transaction proceeds to be invested in growth initiatives to accelerate the business plan and fund the first deployment of the Aurora powerhouse (1) Sam Altman was an early investor in Oklo and has been Chairman since 2015 – partnership is consistent with AltC’s objective to provide public investors access to a compelling “hard tech” opportunity 1 2 3 4 6 Nuclear energy was a “hard tech” vertical of interest for AltC at formation and Oklo’s mission is to provide clean, reliable, and affordable energy through the deployment of next generation fast reactor technology Oklo seeks customer adoption by targeting unaddressed decentralized grid use cases (e.g., data centers, defense) and by pursuing an attractive owner - operator model with an intention to sell power directly to customers under long - term contracts Oklo believes it has embedded opportunity to enhance its business with advanced fuel recycling technology to convert spent fuel to clean energy, which could provide future margin uplift and new revenue streams Oklo shareholders will roll 100% of their existing equity into the combined company, AltC’s sponsor will subject 100% of its founder equity to performance hurdles , and Oklo’s founders and AltC’s sponsor have a staggered lock - up over 3 years 5

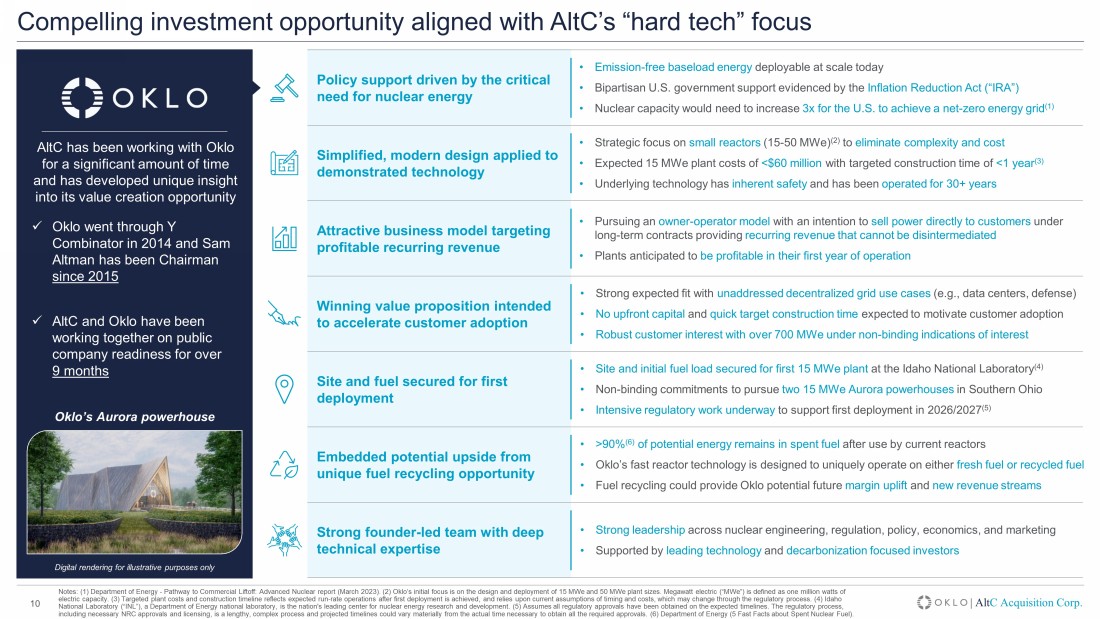

| Alt C Acquisition Corp. Notes: (1) Department of Energy - Pathway to Commercial Liftoff: Advanced Nuclear report (March 2023). (2) Oklo’s initial focus is on the design and deployment of 15 MWe and 50 MWe plant sizes. Megawatt electric (“MWe”) is defined as one m il lion watts of electric capacity. (3) Targeted plant costs and construction timeline reflects expected run - rate operations after first deployme nt is achieved, and relies upon current assumptions of timing and costs, which may change through the regulatory process. (4) Id aho National Laboratory (“INL”), a Department of Energy national laboratory, is the nation's leading center for nuclear energy re sea rch and development. (5) Assumes all regulatory approvals have been obtained on the expected timelines. The regulatory proces s, including necessary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially fro m the actual time necessary to obtain all the required approvals. (6) Department of Energy (5 Fast Facts about Spent Nuclear Fue l). 10 Compelling investment opportunity aligned with AltC’s “hard tech” focus Oklo’s Aurora powerhouse Policy support driven by the critical need for nuclear energy • Emission - free baseload energy deployable at scale today • Bipartisan U.S. government support evidenced by the Inflation Reduction Act (“IRA”) • Nuclear capacity would need to increase 3x for the U.S. to achieve a net - zero energy grid (1) AltC has been working with Oklo for a significant amount of time and has developed unique insight into its value creation opportunity x Oklo went through Y Combinator in 2014 and Sam Altman has been Chairman since 2015 x AltC and Oklo have been working together on public company readiness for over 9 months Simplified, modern design applied to demonstrated technology Attractive business model targeting profitable recurring revenue Winning value proposition intended to accelerate customer adoption Embedded potential upside from unique fuel recycling opportunity Strong founder - led team with deep technical expertise Site and fuel secured for first deployment • Strategic focus on small reactors (15 - 50 MWe) (2) to eliminate complexity and cost • Expected 15 MWe plant costs of <$60 million with targeted construction time of <1 year (3) • Underlying technology has inherent safety and has been operated for 30+ years • Pursuing an owner - operator model with an intention to sell power directly to customers under long - term contracts providing recurring revenue that cannot be disintermediated • Plants anticipated to be profitable in their first year of operation • Strong expected fit with unaddressed decentralized grid use cases (e.g., data centers, defense) • No upfront capital and quick target construction time expected to motivate customer adoption • Robust customer interest with over 700 MWe under non - binding indications of interest • Site and initial fuel load secured for first 15 MWe plant at the Idaho National Laboratory (4) • Non - binding commitments to pursue two 15 MWe Aurora powerhouses in Southern Ohio • Intensive regulatory work underway to support first deployment in 2026/2027 (5) • >90% (6) of potential energy remains in spent fuel after use by current reactors • Oklo’s fast reactor technology is designed to uniquely operate on either fresh fuel or recycled fuel • Fuel recycling could provide Oklo potential future margin uplift and new revenue streams • Strong leadership across nuclear engineering, regulation, policy, economics, and marketing • Supported by leading technology and decarbonization focused investors Digital rendering for illustrative purposes only

| AltC Acquisition Corp. 11 Our mission is to provide clean, reliable, and affordable energy on a global scale We are executing our mission through the design and deployment of next generation fast reactor technology We believe we have an embedded opportunity to enhance our mission with advanced fuel recycling technology to convert spent fuel into clean energy

| AltC Acquisition Corp. 12 | Alt C Acquisition Corp. ✓ Power the energy needs of artificial intelligence Accelerate energy transition and reliability Enhance energy security and access Revitalize domestic nuclear fuel manufacturing ✓ ✓ ✓ How we intend to deliver value to the world: Our mission is to provide clean, reliable, affordable energy on a global scale

| AltC Acquisition Corp. Oklo was founded a decade ago to address stagnation in the U.S. nuclear industry Oklo origin story | AltC Acquisition Corp. 13 U.S. operable nuclear power capacity ( GWe ) (1) 0 50 100 1970 1980 1990 2000 2010 2020 2.8 4.1 1990 2022 U.S. nuclear capacity stagnant for over 30 - years… …meanwhile, U.S electricity consumption grew over 40% U.S. electricity consumption (trillion kWh) (2) Notes: (1) World Nuclear Association (Nuclear Power in the USA – June 2023). (2) U.S. Energy Information Administration (Electri city explained – Use of electricity webpage last updated April 20, 2023). Industry challenges observed by Oklo founders Lack of innovation and activity Project models disconnected from changing customer needs ✗ Large, complex, high - risk projects ✗ Intensive, specialized on - site labor ✗ Expensive (multi - billions of dollars) ✗ Multi - year construction prone to delays Opportunity Oklo founders saw x Forward signals indicated need for clean, abundant, reliable, and affordable energy x Potential design simplification of advanced reactor technology could address observed industry challenges

| AltC Acquisition Corp. Notes: (1) Targeted plant costs and construction timeline reflects expected run - rate operations after first deployment is achiev ed, and relies upon current assumptions of timing and costs, which may change through the regulatory process. (2) Department of Energy (5 Fast Facts about Spent Nuclear Fuel). 14 Purpose - built to solve legacy nuclear deployment and fuel challenges Power sales Base business x Demonstrated technology, inherent safety, and recycled fuel capabilities x Strategically focused on small reactors using a modern design approach to develop the Aurora powerhouse x Reduced plant complexity and cost to streamline deployment Expected 15 MWe plant costs of <$60 million with targeted construction time of <1 year (1) x Pursuing an attractive owner - operator business model that is designed to accelerate customer adoption Strong customer interest with over 700 MWe under non - binding indications of interest x Three project sites; targeting first deployment in 2026/27 x Intensive regulatory work underway Fuel recycling Upside opportunity x Spent fuel recycling is done in other countries but not in the U.S. x Spent nuclear fuel still contains >90% (2) of its energy content x Oklo selected fast reactor technology due to its ability to use either fresh or recycled fuel x Oklo selected by the Department of Energy for four cost - share awards to potentially commercialize recycling technologies x Fuel recycling could provide potential future margin uplift and new revenue streams Oklo business model

| Alt C Acquisition Corp. 15 Deep and differentiated “hard tech,” nuclear engineering, and regulatory expertise …with a highly experienced team Founder - led organization with deep technical expertise and a highly experienced team x Oklo's team comes from Fortune 500 and global companies, as well as government and science backgrounds x Bringing together expertise and experience from several industries to deliver an advanced energy product (e.g., nuclear power, aerospace, automotive and tech) Jacob DeWitte Co - Founder and CEO Co - Founded Oklo in 2013 Caroline Cochran Co - Founder and COO Co - Founded Oklo in 2013 • 15+ years of experience in nuclear technology • PhD in nuclear engineering, MIT • Prior experiences at GE, Sandia National Labs, Urenco U.S., and the U.S. Naval Nuclear Laboratory • 15+ years of experience in nuclear technology • MS in nuclear engineering, MIT • Prior experiences in the Office of the Secretary of Defense and U.S. Department of Energy Nuclear Energy Advisory Committee Founder - led organization… 51 employees, including 8 PhDs (16%) and 20 Masters in Engineering / Science (39%) Multiple engineers and regulatory experts have joined the Oklo team since the last licensing process Six former NRC staff members to assist with the next application filing Board of Directors includes leading hard tech investors

| Alt C Acquisition Corp. Notes: (1) For illustrative purposes only. The assumptions used to determine the LCOE estimates for advanced nuclear, renewables with battery storage, and natural gas with carbon capture are not currently availa bl e. Accordingly, the respective LCOE figures presented herein may not provide a suitable basis for comparison with Oklo estimates. Actual results may differ materially. (2) Upper limit LCOE based on FOAK single unit plant without investment ta x credit (“ITC") benefit. Lower limit LCOE based on NOAK single unit plant with ITC benefit. (3) Estimates for Oklo LCOE rang e a ssume: ( i ) All regulatory approvals have been obtained on expected timelines; (ii) a run - rate of 20 units to achieve NOAK unit economics; (iii) 30% ITC with 90% transferability; (iv) power output s of 15 - 50 MWe; total refueling capital expenditures over the expected 40 - year life of the Aurora powerhouse assumed to be $53 - 8 4mm; (v) excludes overnight cost contingency or decommissioning cost; (vi) levelized average lifetime cost approach, using the discounted cash flow (“DCF”) method; and (vii) a weighted - average - cost of ca pital of 8% based on the International Energy Agency sensitivity analysis range of 4 - 8%. (4) Department of Energy (Pathway to Co mmercial Liftoff: Advanced Nuclear report - March 2023). 16 Oklo expects to deliver emission - free energy at a highly competitive cost Levelized cost of energy (“ LCOE ”) estimated to be below other advanced nuclear approaches and other potential clean, firm energy resources Estimated LCOE of clean, firm energy resources ($ / MWh) (1)(2) x Strategically small ‒ 15 MWe initial design is targeting reduced complexity and a broad set of use cases ‒ Oklo intends to scale design to 50 MWe x Modern design approach ‒ Fewer parts, non - pressurized ‒ Readily available components ‒ Inherent safety attributes, enabling passive safety system ‒ Standardized, factory fabrication x Targeting streamlined deployment ‒ Low land use enables greater site availability ‒ Cost - competitive and capital efficient ‒ Unique fuel flexibility (fresh or recycled) ‒ Reduced supply chain complexity and risk ‒ Highly repeatable factory fabrication ‒ Rapid target construction time x Strong expected fit with unaddressed target markets given plant size ‒ Data centers, defense, factories, industrial, off - grid / rural, and utilities Oklo’s simplified approach $40 $66 $69 $63 $90 $109 $119 $99 Advanced nuclear (4) Renewables with battery storage (4) Natural gas with carbon capture (4) Nuclear is a reliable clean energy solution deployable at scale today Other clean, firm energy options are not deployable at scale today ✓ ✗ (3)

| Alt C Acquisition Corp. 17 Pursuing an owner - operator business model targeting profitable recurring revenue Expected to generate double - digit unlevered cash - on - cash returns with upside from investment tax credits , project finance , and fuel recycling Illustrative unit economics Illustrative cash flow sensitivity (4)(5) Notes: (1) Assumes all regulatory approvals have been obtained on the expected timelines. The regulatory process, including n ece ssary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actua l t ime necessary to obtain all the required approvals. The unit economics provided herein are for illustrative purposes only. Actual re sults may differ materially. Refer to slides 43 - 47 for additional details. (2) Run - rate of 20 units is expected requirement to a chieve NOAK unit economics. (3) Excludes ongoing refueling requirements, which is expected to take place every 10 years. (4) For illustra tiv e purposes only. Actual results may differ materially. Cash flow figures rounded to the nearest $5 million. (5) Excludes corp ora te, general, and administrative costs. (6) Department of Energy (Pathway to Commercial Liftoff: Advanced Nuclear report - March 2023). $34 $24 $86 $61 $35 $33 $56 $55 $69 $57 $142 $116 Initial fuel cost Plant cost $ million 15 MWe (1)(2) 50 MWe (1)(2) FOAK NOAK FOAK NOAK Annual revenue 13 13 36 36 Annual expenses (5) (3) (9) (7) Annual cash flow 8 10 27 29 Unlevered return (3) 12% 17% 19% 25% Payback (3) 8 years 6 years 5 years 4 years First - of - a - kind nth - of - a - kind Oklo has been awarded fuel for its first plant at INL, lowering the capital required to only plant costs <1% of DOE estimated 200 GWe of new U.S. nuclear capacity required by 2050 to reach a net - zero energy grid (6) 1,375 MWe deployed 5 10 15 20 25 0 $40 $80 $125 $165 $210 5 $175 $215 $260 $300 $345 10 $310 $350 $395 $435 $480 15 $445 $485 $530 $570 $615 20 $580 $620 $665 $705 $750 Number of 50 MWe units deployed Number of 15 MWe units deployed $ millions Unit economics do not include investment tax credits, project finance, or fuel recycling upside

| Alt C Acquisition Corp. Note: (1) Regulatory process subject to change. Status of regulatory process is based on management's estimates only which ma y b e incorrect. (2) U.S. NRC website: Design Certification – NuScale US600; second design approval application announced through company press release dated March 17, 2023. (3) Based on company’s S - 4/A filing dated July 3, 2023. 18 Regulatory strategy aimed to accelerate time to market and scalability Oklo is pursuing a Combined License Application (“COLA”) – intensive regulatory work underway to support first deployment in 202 6/27 Siting Oklo is pursuing a Combined License Application Design certification Construction license Operations license Nuclear fuel First plant Future plants Site permit at INL provided by DOE Fuel allocation provided by INL ✓ COLA allows applicant to combine siting, design, construction, and operations into one application Up to 3 - year review Oklo plans submission of an update COLA in 2024/2025 Sites identified for projects 2 and 3 x Fresh or recycled fuel x Centrus partnership Future sites can reference Oklo’s initial COLA Each subsequent COLA (called an S - COLA) expected to have a faster review period, potentially enabling Oklo to deploy future sites more quickly X - energy has not submitted an application to the regulator. Understood to be pursuing a two - part application pathway which includes submitting a construction permit and then an operations license. Each step could take up to 3 years to review. These two steps would need to be done at each subsequent site. x High engagement ‒ Initiated engagement with the U.S. Nuclear Regulatory Commission (“NRC”) in 2016 ‒ Oklo has one of the longest continuous regulatory engagements of any advanced, non - light - water reactor company x Minimize time to market and maximize future scalability ‒ COLA combines siting, design, construction, and operations approval into a single review that can take up to 3 years (vs. a potential 3 - year process for each component piece) ‒ Potential COLA approval could expedite Oklo’s time to first deployment ‒ COLA approach supports Oklo’s intended owner - operator model by providing scalability benefits given application reviews for future sites can potentially be expedited x Iterative approach ‒ Oklo gained valuable experience during its first COLA application process in 2020 - 2022 and used the NRC’s responses to enhance its regulatory model Oklo’s regulatory philosophy NuScale has received a design certification from the NRC for a 50 MWe reactor in a 12 - unit plant and is seeking another for an uprated reactor (77 MWe) and smaller total plant size (6 reactors). Plant design would likely be sold to a customer who would then seek regulatory approval for constructing and operating its plant. ✓ (2) (1) (3)

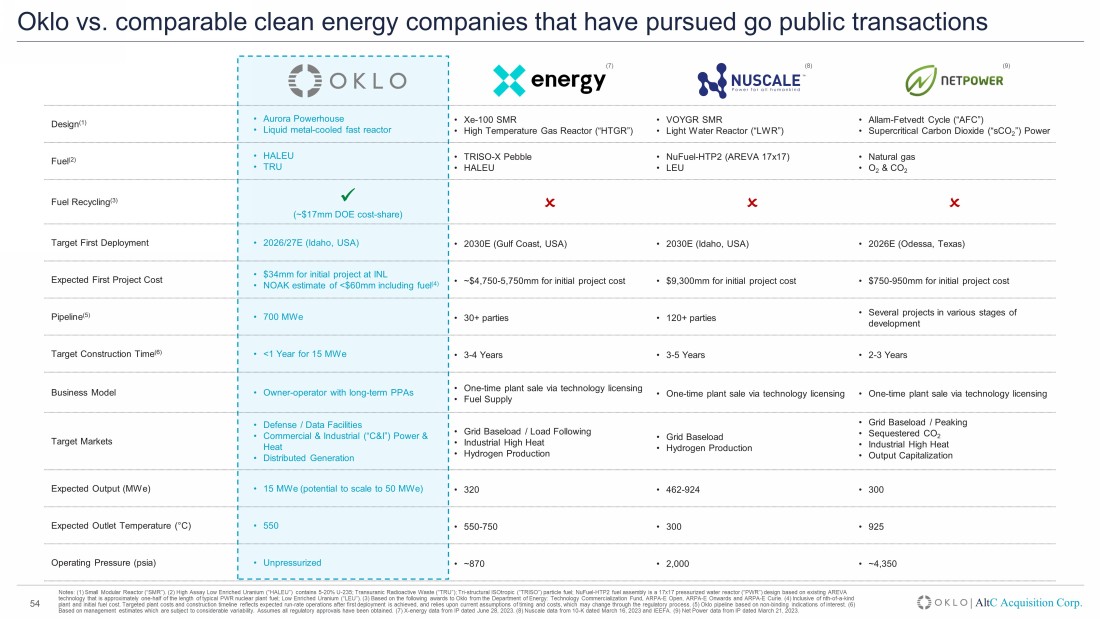

| Alt C Acquisition Corp. $1.5 $1.7 $2.0 $2.6 $0.85 $1.8 $3.4 $3.8 $3.1 $3.7 Sources: X - energy, NuScale, and NetPower information is per public disclosure by the respective companies. Market data is per FactSet as of July 7, 2023. Notes: (1) Targeted plant costs and construction timeline reflects expected run - rate operations after first deployment is achiev ed, and relies upon current assumptions of timing and costs, which may change through the regulatory process. Estimated plant co st of $60 million reflects NOAK cost inclusive of the cost for the initial fuel load. Expected costs for the first deployment at INL reflects FOAK plant cost of $34 million and excludes cost of the initial fuel load given fuel materials have been awarded to Oklo by INL. ( 2) Oklo pre - money equity value excludes potential earnout shares and adjustments for permitted financings. (3) Pre - money equity value per X - energy press release on June 12, 2023. Operating metrics from investor presentation dates June 28, 2023. (4) NuScale operating metrics from 10 - K dated March 16, 2023 and IEEFA. (5) Net Power operating metrics from investor presentation d ated March 21, 2023. (6) All - time high estimated fully diluted equity value and enterprise value. (7) Current estimated fully diluted equity value and enterprise value. 19 Attractive entry valuation with upside potential Transaction values Oklo at a pre - money equity value of $850 million, which is roughly half the value of comparable clean energy go public transactions Oklo’s $850 million valuation relative to comparable clean energy go public transactions x Efficient cost structure ‒ Expected annual operating costs of $19.5 million in 2024 ‒ Expected 15 MWe plant costs of <$60 million with targeted construction time of <1 year (1) x Differentiated owner - operator model ‒ Intention to sell power directly to customers under long - term contracts providing recurring revenue that cannot be disintermediated ‒ Intended to accelerate adoption with zero upfront capital costs to the customer x Strong expected fit with unaddressed target markets given small plant size ‒ Decentralized grid use cases (e.g., data centers, defense) x First deployment targeted by 2026/27 x Embedded potential upside from unique fuel recycling opportunity x AltC is a unique vehicle with no dilutive warrants Value drivers Announced Closed – Trading Value (3) Transaction Pre - Money Equity Value ($ in billions) Enterprise Value Equity Value Enterprise Value Equity Value Current Value (7) Max Value (6) Nuclear Nuclear Nuclear Natural gas Business model Owner - operator License License License Initial output 15 MWe 320 MWe 462 - 924 MWe 300 MWe Expected first plant cost $34.0mm (INL) (1) $4,750 – 5,750mm $9,300mm $750 – 950mm Outlet temp 550 ° C 550 – 750 ° C 300 ° C 925 ° C Pressure Unpressurized ~870 psia ~2,000 psia ~4,350 psia Targeted first deployment 2026 or 2027 2030 2030 2026 Target construction time <1 year (1) 3 - 4 years 3 - 5 years 2 - 3 years Fuel recycling potential ✓ ✗ ✗ ✗ (2) (4) (5)

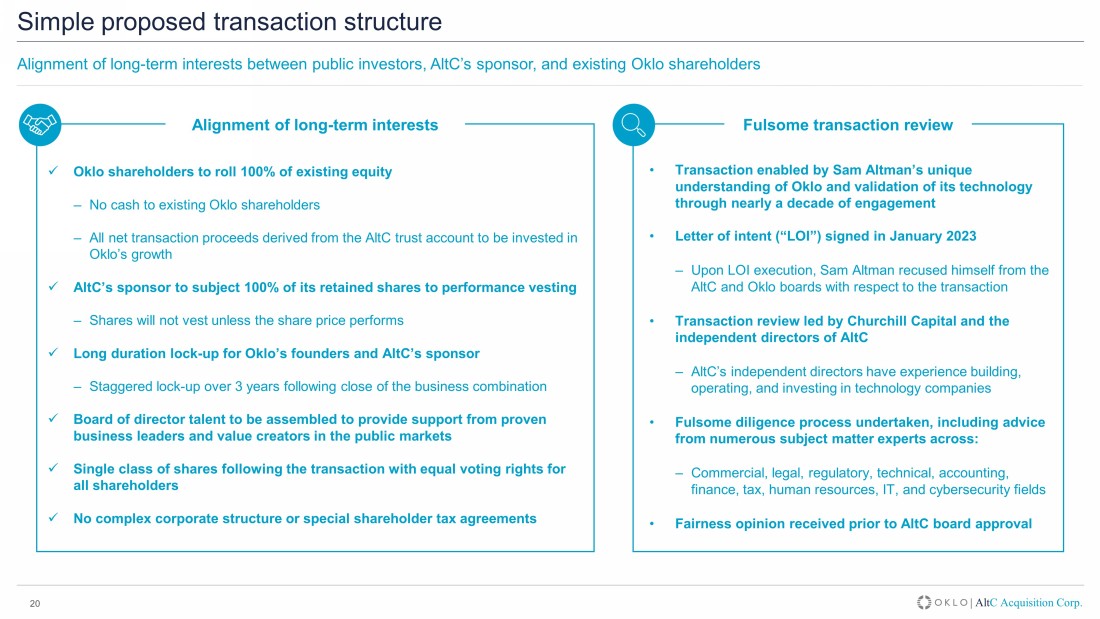

| Alt C Acquisition Corp. 20 Simple proposed transaction structure Alignment of long - term interests between public investors, AltC’s sponsor, and existing Oklo shareholders Alignment of long - term interests Fulsome transaction review x Oklo shareholders to roll 100% of existing equity ‒ No cash to existing Oklo shareholders ‒ All net transaction proceeds derived from the AltC trust account to be invested in Oklo’s growth x AltC’s sponsor to subject 100% of its retained shares to performance vesting ‒ Shares will not vest unless the share price performs x Long duration lock - up for Oklo’s founders and AltC’s sponsor ‒ Staggered lock - up over 3 years following close of the business combination x Board of director talent to be assembled to provide support from proven business leaders and value creators in the public markets x Single class of shares following the transaction with equal voting rights for all shareholders x No complex corporate structure or special shareholder tax agreements • Transaction enabled by Sam Altman’s unique understanding of Oklo and validation of its technology through nearly a decade of engagement • Letter of intent (“LOI”) signed in January 2023 ‒ Upon LOI execution, Sam Altman recused himself from the AltC and Oklo boards with respect to the transaction • Transaction review led by Churchill Capital and the independent directors of AltC ‒ AltC’s independent directors have experience building, operating, and investing in technology companies • Fulsome diligence process undertaken, including advice from numerous subject matter experts across: ‒ Commercial, legal, regulatory, technical, accounting, finance, tax, human resources, IT, and cybersecurity fields • Fairness opinion received prior to AltC board approval

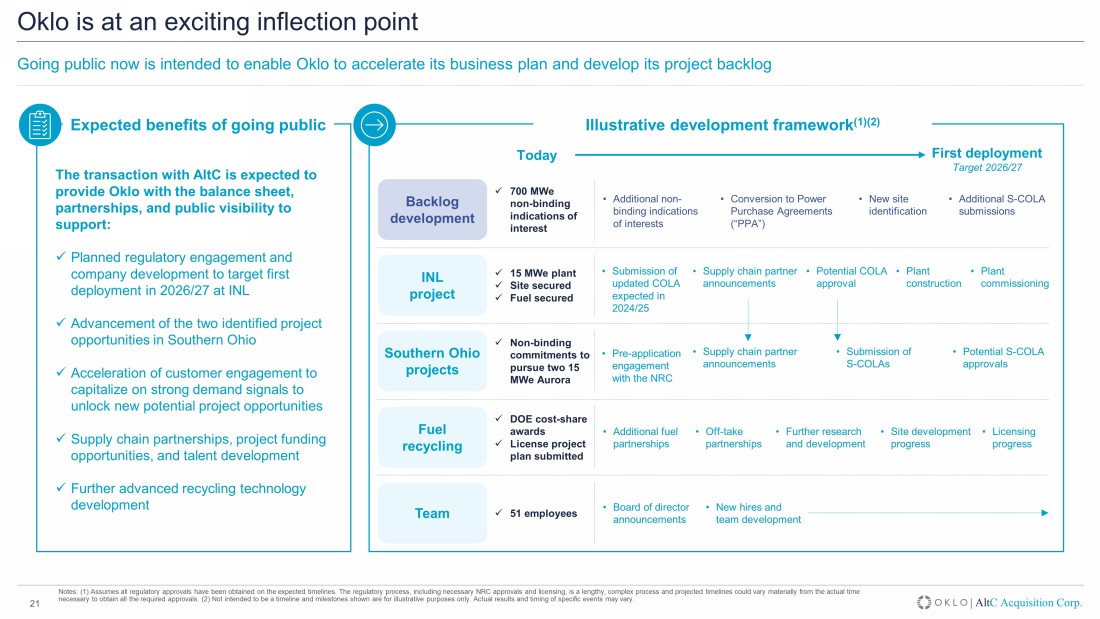

| Alt C Acquisition Corp. 21 Oklo is at an exciting inflection point Going public now is intended to enable Oklo to accelerate its business plan and develop its project backlog Expected benefits of going public Illustrative development framework (1)(2) The transaction with AltC is expected to provide Oklo with the balance sheet, partnerships, and public visibility to support: x Planned regulatory engagement and company development to target first deployment in 2026/27 at INL x Advancement of the two identified project opportunities in Southern Ohio x Acceleration of customer engagement to capitalize on strong demand signals to unlock new potential project opportunities x Supply chain partnerships, project funding opportunities, and talent development x Further advanced recycling technology development Today First deployment Target 2026/27 INL project Southern Ohio projects Fuel recycling Team • Submission of updated COLA expected in 2024/25 • Supply chain partner announcements • Potential COLA approval • Plant construction • Submission of S - COLAs • Potential S - COLA approvals • Supply chain partner announcements • Plant commissioning x 15 MWe plant x Site secured x Fuel secured x Non - binding commitments to pursue two 15 MWe Aurora x DOE cost - share awards x License project plan submitted x 51 employees • Further research and development • Additional fuel partnerships • Site development progress • New hires and team development • Board of director announcements Notes: (1) Assumes all regulatory approvals have been obtained on the expected timelines. The regulatory process, including n ece ssary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actua l t ime necessary to obtain all the required approvals. (2) Not intended to be a timeline and milestones shown are for illustrative p urp oses only. Actual results and timing of specific events may vary. Backlog development x 700 MWe non - binding indications of interest • Additional non - binding indications of interests • Conversion to Power Purchase Agreements (“PPA”) • New site identification • Additional S - COLA submissions • Pre - application engagement with the NRC • Off - take partnerships • Licensing progress

| Alt C Acquisition Corp. Oklo to go public in partnership with AltC 1 6 Power sales: targeting profitable recurring revenue Fuel recycling: embedded potential upside opportunity Compelling anticipated unit economics Importance of clean, reliable, and abundant energy 2 3 4 5 Agenda Simple transaction with an attractive valuation

| Alt C Acquisition Corp. 23 Clean, reliable, and abundant energy is critical to our future Daily Life Emerging U.S. grid reliability issues as demand grows and severe weather events strain aging infrastructure Global electricity demand to triple by 2050 as electrification and living standards grow The problem: The world is simultaneously growing its energy consumption while trying to reverse climate change C - U.S. energy grid grade by the American Society of Civil Engineers 64% Increase in U.S. power outages in the last decade Sources: World Health Organization (climate change and health), McKinsey & Company (Global Energy Perspectives 2022), America n S ociety of Civil Engineers (Report Card for America’s Infrastructure), Department of Energy – Office of Energy Efficiency & Renewable Energy (Data Centers and Servers), Climate Central. Health Climate change viewed as the biggest health threat facing humanity 250,000 Expected additional deaths per year globally between 2030 and 2050 due to climate change Innovation Innovation in artificial intelligence is driving unprecedented computing power and data storage needs 10 – 50x Energy intensity of a data center vs. a traditional office

| Alt C Acquisition Corp. 24 Nuclear is a reliable clean energy solution deployable at scale today Emission - free Firm Deployable at Scale Today Nuclear energy advantages ✓ ✓ ✓ x Lowest lifecycle emissions of any major generating energy source x Highest capacity utilization of any major generating energy source at 93% x Operated reliably for over 60 years with 400+ GW of installed capacity in 32 countries x Safe baseload energy source x Most efficient land use of any energy source x Ability to use existing transmission infrastructure x Wide variety of applications providing grid flexibility and decarbonization beyond the grid o n - demand , uninterruptible Source: Department of Energy - Pathway to Commercial Liftoff: Advanced Nuclear report (March 2023). How other energy solutions compare ✗ Natural gas provides firm, baseload energy but it is not clean ✗ Requires expensive gas distribution infrastructure ✗ Carbon capture technology not scalable today ✗ Wind and solar are clean but cannot provide firm, baseload energy ✗ Requires expensive electric transmission infrastructure ✗ Battery storage technology not scalable today Natural gas with carbon capture Renewables with battery storage

| Alt C Acquisition Corp. Source: Department of Energy (Pathway to Commercial Liftoff: Advanced Nuclear report - March 2023). Notes: (1) Firm power is generating capacity that is intended to be always available. Clean, firm power options include nucle ar, renewables paired with long duration energy storage, fossil with carbon capture, and geothermal. (2) Includes estimates for l im itations on renewables buildout that come from current understanding of land - use intensity, regional siting requirements, supply chain, tran smission, and interconnection difficulties that may impact utility - scale renewables deployment. 25 Nuclear capacity would need to increase 3x for the U.S. to achieve a net - zero energy grid Nuclear has the potential to replace fossil fuels with clean baseload power and solve the variability issues with current ren ewa ble technology, at scale Up to 770 GW of new clean baseload power required in the U.S. to reach a net - zero energy grid by 2050 Nuclear could provide 200+ GW as the most viable clean baseload option Renewables with variable capacity Non - clean baseload power (fossil fuels) Clean baseload power (1) 206 979 866 515 205 1,175 1,278 GW 2,669 GW 2021 2050 ~5.0x (770 GW) (2) Declining ~6.0x (970 GW) Clean % of total 16% 37% Clean % of baseload 19% 66% Renewables require large growth in clean baseload power ~ 100 ~ 200 ~ 300 GW Current operating U.S. nuclear capacity New advanced nuclear capacity required by 2050 to reach a net - zero (2) energy grid 2050 nuclear capacity +3.0x x 2050 nuclear capacity as a multiple of currently operating U.S. nuclear capacity

| Alt C Acquisition Corp. 26 Policymakers recognize the importance of U.S. leadership in nuclear technology Bipartisan action has delivered meaningful funding and support via the Inflation Reduction Act In August 2022, Congress passed the Inflation Reduction Act , representing a meaningful increase in government support for advanced nuclear through the IRA’s Investment and Production Tax Credits Benefits under the IRA for nuclear include: $700 million Funding for advanced nuclear fuel $250 b illion For Department of Energy Loan Program Office x FY23 and FY24 Appropriations providing $3 billion to support nuclear x ADVANCE (1) Act , introduced in April 2023, to support development and deployment of nuclear energy technologies x International Nuclear Energy Act , reintroduced in March 2023 to promote the facilitation of nuclear energy cooperation with ally and partner nations Up to 50% Investment tax credits Additional bipartisan U.S. support for nuclear Source: The Inflation Reduction Act of 2022, Department of Energy (Inflation Reduction Act Keeps Momentum Building for Nuclea r P ower). Note: (1) Defined as Accelerating Deployment of Versatile, Advanced Nuclear for Clean Energy.

| Alt C Acquisition Corp. Oklo to go public in partnership with AltC 1 6 Power sales: targeting profitable recurring revenue Fuel recycling: embedded potential upside opportunity Compelling anticipated unit economics Importance of clean, reliable, and abundant energy 2 3 4 5 Agenda Simple transaction with an attractive valuation

| AltC Acquisition Corp. Notes: (1) Targeted plant costs and construction timeline reflects expected run - rate operations after first deployment is achiev ed, and relies on current assumptions of timing and costs, which may change through the regulatory process. (2) Idaho Nationa l L aboratory (“INL”), a Department of Energy national laboratory, is the nation's leading center for nuclear energy research and developme nt. 28 Modern design approach Attractive business model Winning value proposition Progressing first deployment Demonstrated technology Power sales Oklo was inspired by the Experimental Breeder Reactor II x Ability to produce and sell commercial power x Inherent safety x Fuel flexibility (fresh fuel and recycled fuel) x Competitive with light water reactors EBR - II demonstrated at scale the unique benefits of fast reactor technology Strategically focused on small reactors to eliminate complexity and cost x Fewer parts x Readily available components x Passive safety systems x Factory fabrication x Streamlined deployment Expected 15 MWe plant cost of <$60 million and <1 - year targeted construction time (1) Owner - operator model enabled by unique product attributes x Capital efficient x Low land use x Quick expected construction time x Operating simplicity x Attractive expected unit economics with upside Existing competitors cannot replicate model due to larger and more expensive designs Compelling offering that is expected to accelerate customer adoption x Low capex solution designed to quickly meet customer needs x Contracted access to clean, reliable energy x Demonstrated technology with low expected risk (execution and operations) Strong customer interest with over 700 MWe under non - binding indications of interest First Aurora powerhouse deployment target of 2026/27 x Advancing three projects x Site and fuel secured for first plant at INL (2) x Non - binding commitments to pursue two sites in Southern Ohio Intensive regulatory work underway to support first deployment Base business Oklo

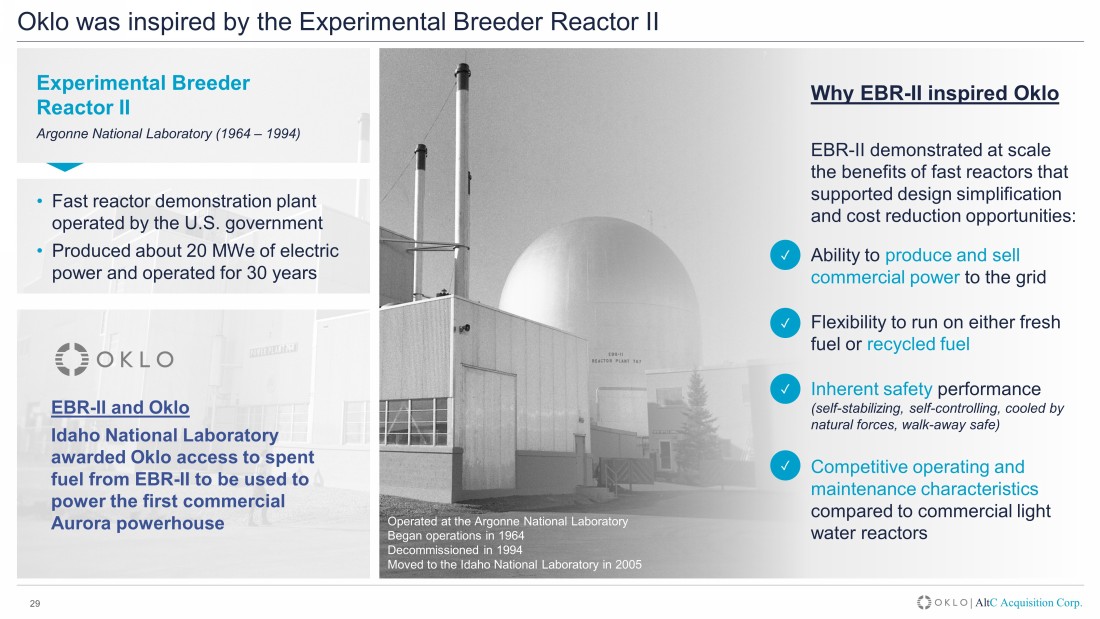

| Alt C Acquisition Corp. 29 Oklo was inspired by the Experimental Breeder Reactor II Experimental Breeder Reactor II Argonne National Laboratory (1964 – 1994) • Fast reactor demonstration plant operated by the U.S. government • Produced about 20 MWe of electric power and operated for 30 years Operated at the Argonne National Laboratory Began operations in 1964 Decommissioned in 1994 Moved to the Idaho National Laboratory in 2005 Why EBR - II inspired Oklo EBR - II demonstrated at scale the benefits of fast reactors that supported design simplification and cost reduction opportunities: Ability to produce and sell commercial power to the grid Flexibility to run on either fresh fuel or recycled fuel Inherent safety performance (self - stabilizing, self - controlling, cooled by natural forces, walk - away safe) Competitive operating and maintenance characteristics compared to commercial light water reactors ✓ ✓ ✓ ✓ EBR - II and Oklo Idaho National Laboratory awarded Oklo access to spent fuel from EBR - II to be used to power the first commercial Aurora powerhouse

| Alt C Acquisition Corp. Notes: (1) Oklo’s initial focus is on the design and deployment of 15 MWe and 50 MWe plant sizes. (2) Targeted plant costs and construction tim el ine reflects expected run - rate operations after first deployment is achieved, and relies upon current assumptions of timing and costs, which may change through the regulatory process. (3) Inclusive of the Emergency Planning Zone, which for th e A urora reactor is expected to be bounded within the powerhouse building structure. 30 Simplified, modern design approach to enable streamlined deployment Aurora powerhouse design is intended to reduce plant complexity, cost, and construction time Aurora powerhouse <1 year Estimated construction time 40+ years Estimated plant design life <$60 million Estimated construction costs (2) 15+ MWe Design is expected to be scalable to 50+ MWe (1) Liquid metal fast reactor technology for electricity and heat production <2 acre of land required (3) Strategically small • 15 MWe initial design is expected to reduce complexity while providing a broad set of use cases • Oklo intends to scale design to 50 MWe Modern design approach • Fewer parts, non - pressurized • Readily available components • Inherent safety attributes, enabling passive safety system • Standardized, factory fabrication Targeting streamlined deployment • Low land use enables greater site availability • Cost - competitive and capital efficient • Unique fuel flexibility (fresh or recycled) • Reduced supply chain complexity and risk • Highly repeatable factory fabrication • Rapid target construction time Digital rendering for illustrative purposes only External reactor design Page 1 of 2

| Alt C Acquisition Corp. Notes: (1) Inclusive of the Emergency Planning Zone, which for the Aurora reactor is expected to be bounded within the powerh ous e building structure. 31 Simplified, modern design approach to enable streamlined deployment Aurora powerhouse design is intended to reduce plant complexity, cost, and construction time Aurora powerhouse (15 MWe) Internal reactor design Reactor placed underground Reactor vessel cooling system Power conversion heat exchangers Power conversion system Expected design driven cost efficiencies • Minimal site improvements required ‒ Low land use results in minimal site improvements required to accommodate the reactor • Small structures ‒ Single building with small footprint enabled by small component sizes (no large concrete or pool structure required) • Non - pressurized reactor equipment ‒ Small and simple double vessel system designed to be fabricated from readily available stainless steel ‒ Designed such that no specialized pressure vessels, specialty superalloys, or nuclear graphite required • Simple heat rejection system ‒ Air naturally cools the reactor • Conventional power conversion system ‒ High operating temperature expected to enable uses of systems already made for the fossil fuel industry • Rapid expected construction timeline reduces potential project carrying costs / financing costs <2 acre of land required (1) 1 2 3 4 5 1 2 3 4 5 6 <1 year Estimated construction time 6 Digital rendering for illustrative purposes only Page 2 of 2

| Alt C Acquisition Corp. Source: Department of Energy - Pathway to Commercial Liftoff: Advanced Nuclear report (March 2023), Center for Advanced Nuclear Energy Systems. Notes: (1) Targeted plant costs and construction timeline reflects expected run - rate operations after first deployment is achiev ed, and relies upon current assumptions of timing and costs, which may change through the regulatory process. (2) Advanced reactor overnight capital costs for next - of - a - kind (“NOAK”) assumed to be $3,600 / kw based on Department of Energ y analysis. (3) Overnight capital costs based on the AP - 1000. 32 Owner - operator model enabled by reduced product complexity and cost Oklo intends to build, own, and operate Aurora powerhouses – reactor design enables cost, land, material, and construction time advantages Lower anticipated plant cost Small footprint Reduced complexity Quick installation Unique business model 15 MWe plant capacity (Technology is potentially scalable to 50 MWe) x <$60 million (1) x <2 acres of land required x Advantaged proximity to customers x Fewer parts than traditional nuclear x Readily available components x Simple operations with passive safety systems x <1 year manufacturing and installation timeline (1) x Standardized, factory fabrication x Build, own, and operate Aurora powerhouses x Sell electricity/heat under long - term contracts ~30 acres High - cost specialty material 3 – 4 years 500+ acres High - cost legacy supply chain 6+ years $2.0+ billion $5.0+ billion Competing approaches 1+ GWe (3) Traditional nuclear 300+ MWe (2) Other advanced nuclear Large utility - scale projects pursued under a traditional licensing model where customers must fund high project costs and bear multi - year construction timelines

| Alt C Acquisition Corp. Notes: (1) The unit economics described herein, including any potential margin upside, is forward - looking information and should not be relied upon as necessarily being indicative of future results. Actual results may differ materially. (2) Reflects mark et capitalization as sourced from FactSet as of July 7, 2023. 33 Attractive business model expected to generate compelling recurring revenue Oklo is pursuing a widely - used revenue model in the global power markets with the sale of electricity under long - term contracts Shareholder opportunity Revenue model proven across markets Oklo value proposition for shareholders x Large market opportunity – Oklo is targeting unaddressed decentralized grid use cases (e.g., data centers, defense) x Long duration contracted revenue that is expected to be recurring and grow over time x Revenue source cannot be disintermediated by competitors x Expected profitable unit economics from first year of plant operations (1) x High repeatability to drive unit growth and launch higher output versions (e.g., 50 MWe) x Fuel recycling could provide potential future margin uplift and new revenue streams Country Focus Market Value (2) Denmark Canada Canada Canada Canada France Wind Diverse Wind Wind / Solar Wind / Solar Wind / Solar ~$38 billion ~$19 billion ~$5 billion ~$5 billion ~$3 billion ~$2 billion Portugal Wind / Solar ~$19 billion

| Alt C Acquisition Corp. 34 Winning value proposition intended to accelerate customer adoption Strong customer interest with over 700 MWe under non - binding indications of interest Potential customers Oklo target markets What customers want □ To buy power, not own/operate plants □ Low capex solutions that meet environmental and operational goals □ Access to affordable and reliable carbon - free energy □ Proven technology with low execution and operational risk Oklo value proposition x Potential for zero upfront customer cost , accelerating adoption x Reliable, affordable emission - free energy under long - term contracts , a proven and standard model in global power markets x Underlying technology that has been demonstrated at scale Data centers Defense Factories Industrial Off - grid/ rural Utilities ✓ ✓ ✓ ✓ ✓ ✓ ✓ Active dialogues with potential customers

| Alt C Acquisition Corp. 35 Advancing three exciting projects towards deployment Site and initial fuel load secured for 15 MWe plant at the Idaho National Laboratory. Opportunity to deploy two 15 MWe plants in Southern Ohio Idaho National Laboratory Aurora powerhouse (15 MWe) #1 Oklo signs an MOU with the DOE for a site and High - Assay Low - Enriched Uranium (“HALEU”) DOE issues Oklo a Site Use Permit at Idaho National Laboratory Idaho National Laboratory awards fuel material to Oklo 2017 2019 2021 2024 2024 – 26 2026/27 2020 Oklo obtains DOE Site Use Permit for Aurora powerhouse Targeted application acceptance review with the NRC (1) Anticipated NRC review period for Oklo supply chain development Targeting first electricity production Fuel Secured ✓ Site Identified ✓ x Partnership with the Southern Ohio Diversification Initiative ( SODI ) (2) announced on May 18, 2023 x Non - binding commitments to deploy two commercial Oklo power plants in Southern Ohio Site Identified ✓ • Plants expected to provide clean electric power and heat, with opportunities to expand • The plants support job creation in the area, furthering SODI’s mission to improve the quality of life for the southern Ohio community through economic diversification and the advancement of clean energy solutions • SODI is funded through a grant from the DOE Office of Nuclear Energy to support the deployment of advanced reactor technology and the use of a former nuclear plant site Southern Ohio Diversification Initiative Two Aurora powerhouses (15 MWe each) #2 - 3 Notes: (1) The U.S. Nuclear Regulatory Commission (“NRC”). (2) The Southern Ohio Diversification Initiative ( SODI ) mission is to improve the quality of life for Jackson, Pike, Ross, and Scioto Counties through economic diversification, de vel opment of underutilized land and facilities on the Department of Energy (DOE) Portsmouth Gaseous Diffusion Plant Site, and continued support of local in dustry.

| Alt C Acquisition Corp. 36 Intensive regulatory work underway to support first deployment Oklo has one of the longest continuous regulatory engagements of any advanced, non - light - water reactor company First ever advanced reactor Combined License Application (“COLA ”) submitted x NRC engagement initiated in 2016 x COLA submitted in March 2020 x Deep engagement with the NRC staff in 2020 through 2022 during the COLA review process x Valuable experience being leveraged to succeed in its next application submission x NRC approved Oklo’s Quality Assurance Program Description Intensive work underway in preparation for the next application filing x Substantially expanded the licensing and regulatory team to bring in - house former NRC staff and regulatory experts ‒ Nearly 10% of Oklo’s current employees are former NRC staff members x Frequent engagement and information sharing in 2022 - 23 ‒ 9 formal pre - application meetings held on key licensing topics ‒ Over 70 coordination meetings held ‒ Over 50 licensing documents shared x Oklo intends to pursue a pre - application audit in 2024 x Application submission targeted for late 2024 / early 2025 x Oklo is deeply appreciative of the NRC staff’s hard work and commitment to advancing safe nuclear solutions • COLA is a licensing pathway with the NRC combining a construction permit and an operating license • Oklo was the first advanced reactor company in history to submit a COLA for NRC review • In 2022, the NRC denied Oklo’s COLA, requesting additional information to resume its review • Oklo gained valuable experience during the process and used the NRC’s responses to enhance its regulatory model

| Alt C Acquisition Corp. Oklo to go public in partnership with AltC 1 6 Power sales: targeting profitable recurring revenue Fuel recycling: embedded potential upside opportunity Compelling anticipated unit economics Importance of clean, reliable, and abundant energy 2 3 4 5 Agenda Simple transaction with an attractive valuation

| AltC Acquisition Corp. Notes: (1) U.S. Energy Information Administration (Uranium Marketing Annual Report – 2022). (2) Department of Energy (5 Fast Fac ts about Spent Nuclear Fuel). 38 Fuel recycling Upside opportunity Oklo Large spent fuel stockpiles Spent fuel potential Oklo design advantage Unique upside opportunity Fuel supply constraints The U.S. currently relies on imports for fresh nuclear fuel ✗ In 2022, 95% (1) of uranium for U.S. nuclear plants was foreign - sourced ✗ In 2022, 33% (1) of uranium enrichment services for U.S. nuclear plants were purchased from Russia ✗ U.S. has limited HALEU production, which is the fuel for advanced reactors Limited U.S. fuel capabilities is a pressing concern for advanced reactor growth The U.S. has large and growing spent fuel stockpiles ✗ Expensive to manage ✗ U.S. reactors have generated 90,000 tons of spent fuel since 1950 (2) ✗ 2,000 tons of spent fuel generated each year (2) ✗ Spent fuel is currently stored at 70 reactor sites across 35 states (2) Spent fuel management is complex; needs will grow with new reactor deployment Spent fuel retains its energy potential and can be recycled x Fuel can be recycled and is done so in other countries, such as France x >90% of potential energy remains in spent fuel after use by current reactors (2) ✗ The U.S. does not currently recycle fuel Opportunity to address fuel supply constraints and spent fuel stockpiles with recycling Fast reactors can use either fresh or recycled fuel x EBR - II demonstrated fast reactor’s ability to use recycled fuel x Oklo plants designed with flexibility to use either fresh or recycled fuel x First Aurora powerhouse to be fueled by spent fuel recovered from EBR - II Fuel recycling could provide future margin uplift and new revenue streams Oklo is developing fuel recycling capabilities x Waste to clean energy x Selected for four projects with the Department of Energy to develop fuel recycling technologies x Initial plans to pursue a commercial - scale fuel recycling facility in the U.S. by 2030’s Oklo has the potential opportunity to lead the industry in fuel recycling

| AltC Acquisition Corp. U.S. nuclear power plants are heavily reliant on imported nuclear fuel Nuclear fuel imports | AltC Acquisition Corp. 39 Source of uranium for U.S. nuclear power plants (Uranium oxide, million pounds) (1) Notes: (1) U.S. Energy Information Administration (Nuclear explained – where our uranium comes from). (2) U.S. Energy Information Administration (Uranium Marketing Annual Report – 2022), (3) Orano (All about used fuel processing and recycling). Evolving geopolitical concerns In 2022, 95% (2) of uranium for U.S. nuclear plants was foreign - sourced In 2022, 33% (2) of foreign uranium enrichment services required by U.S. nuclear plants were purchased from Russia 0 20 40 60 80 1950 1960 1970 1980 1990 2000 2010 2020 Domestic production Purchased imports Fuel recycling could reduce U.S. imports The U.S. does not currently recycle spent fuel However, fuel can be recycled and is done so in other countries, such as France Nearly 1 in 10 light bulbs in France runs on recycled nuclear materials (3)

| Alt C Acquisition Corp. 40 Fuel recycling could provide potential future margin uplift and new revenue streams Potential opportunity to build and operate facilities that could supply recycled fuel to Aurora powerhouses as well as third - par ty customers Spent fuel recycling is a significant potential cost savings opportunity for Oklo that could reduce both initial plant capital costs as well as ongoing operating costs Vertically integrated fuel source will provide security and assurance Oklo’s recycling approach utilizes pyro - processing, which is a mature technology Additional potential revenue streams through the sale of spent fuel management services as well as the sale of byproducts and specialty isotopes to various end markets Fuel recycling solves a longstanding issue in the market and can create a sustainab le competitive advantage In January 2023, Oklo submitted a commercial - scale fuel recycling facility licensing project plan to the Nuclear Regulatory Commission How fuel recycling works Separate fuel material via electrochemistry Produce power in reactor Fabricate fuel by casting Dissolve fuel Chop up used fuel 1 2 3 4 5

| Alt C Acquisition Corp. 41 Oklo has the potential opportunity to lead the industry in fuel recycling Oklo selected by the Department of Energy for four cost - share awards to potentially commercialize recycling technologies Oklo’s recycling technology development projects Technology Commercialization Fund x Develop advanced sensors for key recycling process efficiency improvements ARPA – E Open x Utilize machine learning and digital twinning for recycling efficiency improvements and material accountability ARPA – E Onwards x Demonstrate the recycling process end - to - end and develop the technical basis for commercial - scale fuel recycling facility ARPA – E Curie x Demonstrate the conversion of used oxide fuel into metal, enabling the recycling of waste from the current fleet into advanced reactor fuel

| Alt C Acquisition Corp. Oklo to go public in partnership with AltC 1 6 Power sales: targeting profitable recurring revenue Fuel recycling: embedded potential upside opportunity Compelling anticipated unit economics Importance of clean, reliable, and abundant energy 2 3 4 5 Agenda Simple transaction with an attractive valuation

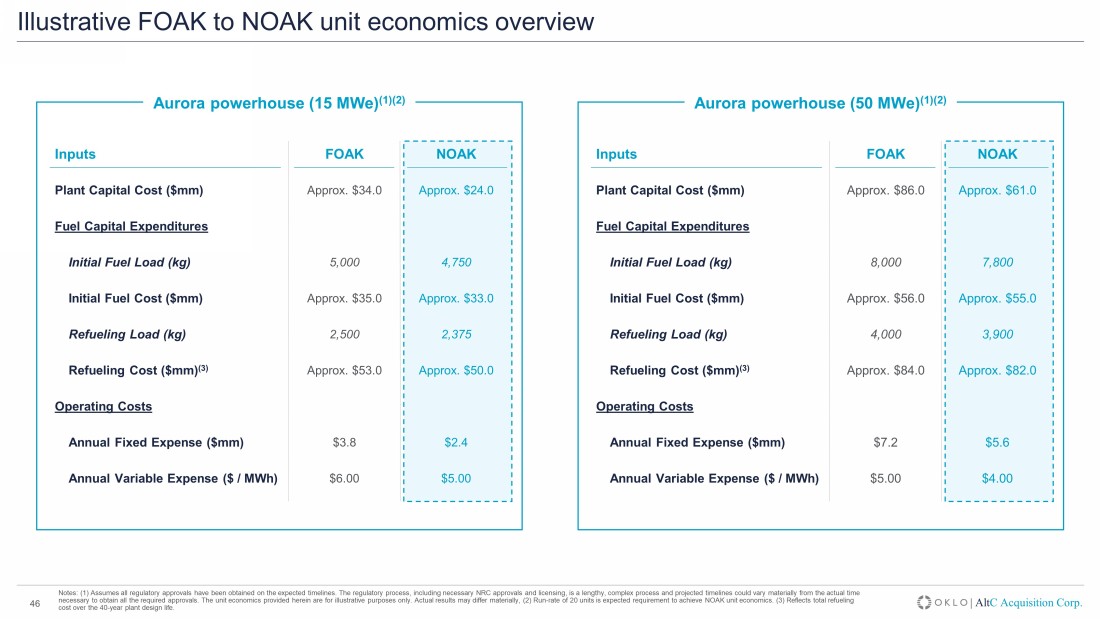

| Alt C Acquisition Corp. Note: (1) Assumes all regulatory approvals have been obtained on the expected timelines. The regulatory process, including ne ces sary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actual ti me necessary to obtain all the required approvals. Assumes capital costs of $24 million and $61 million for the 15 MWe and 50 MW e A urora powerhouse, respectively, and a 40 - year life span for each powerhouse. Assumes NOAK status for each. The unit economics are presented in real terms. Additionally, the unit economics provided herein are for illustrative purposes only. Actual resu lts may differ materially. Refer to slides 44 and 45 for additional details. (2) Excludes ongoing refueling requirements, which i s expected to take place every 10 years. 43 Compelling anticipated unit economics with potential upside Illustrative unit economics: 15 MWe Aurora powerhouse (1) Cumulative 40 - year unit economics ($ millions) $288 $198 $1,452 $1,163 $966 Revenue from power sales Operating expenses Plant profit Capital costs Plant cash flow Capital cost build-up $198 80% 5.0x $120 $107 $508 $388 $281 Revenue from power sales Operating expenses Plant profit Capital costs Plant cash flow Capital cost build-up $107 • Initial plant cost: $24 • Initial fuel cost: $33 • Refueling cost: $50 75% 2.5x Illustrative unit economics: 50 MWe Aurora powerhouse (1) Cumulative 40 - year unit economics ($ millions ) • Initial plant cost: $61 • Initial fuel cost: $55 • Refueling cost: $82 Potential upside levers: x Investment tax credits x Project finance x Fuel recycling 6 Years of operation to payback initial plant and fuel cost 17% Unlevered annual cash - on - cash return (2) Potential upside levers: x Investment tax credits x Project finance x Fuel recycling 4 Years of operation to payback initial plant and fuel cost 25% Unlevered annual cash - on - cash return (2) 75% 2.5x Potential life of plant profit margin Potential plant cash flow vs. total capital costs (including refueling) 80% 5.0x Potential life of plant profit margin Potential plant cash flow vs. total capital costs (including refueling)

| Alt C Acquisition Corp. 44 Illustrative unit economics: Aurora powerhouse (15 MWe) Oklo believes that expected cumulative plant cash flow equals more than 2.5x expected cumulative capital costs Notes: (1) Key assumptions based on expected NOAK (nth of a kind) plant. (2) Assumes all regulatory approvals have been obtai ned on the expected timelines. The regulatory process, including necessary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actual time necessary to obtain all the required approvals. Th e u nit economics are presented in real terms and are presented as of May 2023. The unit economics provided herein are for illust rat ive purposes only. Actual results may differ materially. (3) FOAK (first - of - a - kind) plant cost expected to be ~$34 million. (4) Repr esents 15 MWe generating capacity at a 92% capacity factor. Aurora powerhouse (15 MWe) (2) T+0 T+1 T+2 T+3 T+4 T+5 T+10 40-Yr Life of Plant ($ in Millions) Capital Expenditures ($57) ($17) ($107) Plant Cost ($24) ($24) Initial Fuel Cost ($33) ($33) Refueling Cost ($17) ($50) Revenue $13 $13 $13 $13 $13 $13 $508 Revenue from Power Sales $13 $13 $13 $13 $13 $13 $508 Expenses ($3) ($3) ($3) ($3) ($3) ($3) ($120) Fixed Plant ($2) ($2) ($2) ($2) ($2) ($2) ($96) Variable Plant ($1) ($1) ($1) ($1) ($1) ($1) ($24) Annual Plant Cash Flow ($57) $10 $10 $10 $10 $10 ($7) $281 Cash Margin NA 76.4% 76.4% 76.4% 76.4% 76.4% (54.4%) 55.4% 0 50 100 150 Year 2 Year 4 Year 6 Year 8 Year 10 Illustrative Annual Deployments (Units) Low High • 40 - year plant design life • Plant capital expenditures: ‒ Initial plant cost of approximately $24.0 million (excluding initial fuel load) (3) • Fuel capital expenditures: ‒ Initial fuel load of 4,750 kg ‒ Refueling load of 2,375 kg every 10 years over the 40 - year plant design life ‒ Does not assume Oklo recycles fuel for internal supply. Assumes all fuel is newly fabricated HALEU purchased from a third - party supplier at a cost of $7,000 / kg • Revenue from annual power sales : recurring revenue of approximately $13.0 million assuming annual generation of approximately 121,000 MWh (4) and average real power price of $105 / MWh • Operating costs: ‒ Annual fixed expense of $2.4 million ‒ Annual variable expense of $5.00 / MWh Key Assumptions (1)(2) Aurora 15 MWe Illustrative Unit Economics (1)(2)

| Alt C Acquisition Corp. 45 Illustrative unit economics: Aurora powerhouse (50 MWe) Oklo believes that expected cumulative plant cash flow equals more than 5.0x expected cumulative capital costs Notes: (1) Key assumptions based on expected NOAK (nth of a kind) plant. (2) Assumes all regulatory approvals have been obtai ned on the expected timelines. The regulatory process, including necessary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actual time necessary to obtain all the required approvals. Th e u nit economics are presented in real terms and are presented as of May 2023. The unit economics provided herein are for illust rat ive purposes only. Actual results may differ materially. (3) FOAK (first - of - a - kind) plant cost expected to be ~$86 million. (4) Repr esents 50 MWe generating capacity at a 92% capacity factor. • 40 - year plant design life • Plant capital expenditures: ‒ Initial plant cost of approximately $61.0 million (excluding initial fuel load) (3) • Fuel capital expenditures: ‒ Initial fuel load of 7,800 kg ‒ Refueling load of 3,900 kg every 10 years over the 40 - year plant design life ‒ Does not assume Oklo recycles fuel for internal supply. Assumes all fuel is newly fabricated HALEU purchased from a third - party supplier at a cost of $7,000 / kg • Revenue from annual power sales : recurring revenue of approximately $36.0 million assuming annual generation of approximately 403,000 MWh (4) and average real power price of $90 / MWh • Operating costs: ‒ Annual fixed expense of $5.6 million ‒ Annual variable expense of $4.00 / MWh Key Assumptions (1)(2) Aurora 50 MWe Illustrative Unit Economics (1)(2) T+0 T+1 T+2 T+3 T+4 T+5 T+10 40-Yr Life of Plant ($ in Millions) Capital Expenditures ($116) ($27) ($198) Plant Cost ($61) ($61) Initial Fuel Cost ($55) ($55) Refueling Cost ($27) ($82) Revenue $36 $36 $36 $36 $36 $36 $1,452 Revenue from Power Sales $36 $36 $36 $36 $36 $36 $1,452 Expenses ($7) ($7) ($7) ($7) ($7) ($7) ($288) Fixed Plant ($6) ($6) ($6) ($6) ($6) ($6) ($224) Variable Plant ($2) ($2) ($2) ($2) ($2) ($2) ($65) Annual Plant Cash Flow ($116) $29 $29 $29 $29 $29 $2 $966 Cash Margin NA 80.1% 80.1% 80.1% 80.1% 80.1% 4.9% 66.5% Aurora powerhouse (50 MWe) (2) 0 50 100 150 Year 2 Year 4 Year 6 Year 8 Year 10 Illustrative Annual Deployments (Units) Low High