Delivered on all key guidance metrics

Achieved record free cash flow of more than $1.3 billion and repaid

$800 million of debt

Strong three-year outlook of 2.0 million Au eq. oz. per year

TORONTO, Feb. 12, 2025 (GLOBE NEWSWIRE) --

Kinross Gold Corporation (TSX: K, NYSE: KGC) (“Kinross” or the

“Company”) today announced its results for the fourth quarter and

year ended December 31, 20241.

This news release contains forward-looking information

about expected future events and financial and operating

performance of the Company. We refer to the risks and assumptions

set out in our Cautionary Statement on Forward-Looking Information

located on pages 41 and 42 of this release. All dollar amounts are

expressed in U.S. dollars, unless otherwise noted.

2024 full-year results and 2025

guidance:

|

|

2024

guidance

(+/- 5%) |

Q4 2024

results |

2024 full-year

results |

2025

guidance

(+/- 5%) |

Gold equivalent

production1

(ounces) |

2.1 million |

501,209 |

2.13 million |

2.0 million |

Production cost of sales2

Attributable production cost of

sales1

($ per Au eq. oz.) |

-

$1,020

|

$1,098

$1,096

|

$1,020

$1,021

|

-

$1,120

|

Attributable all-in sustaining

cost1

($ per Au eq. oz.) |

$1,360 |

$1,510 |

$1,388 |

$1,500 |

Capital expenditures3

Attributable capital

expenditures1

(million) |

-

$1,050 |

$281

$279

|

$1,076

$1,051

|

-

$1,150

|

- Kinross has forecasted stable

production guidance of approximately 2.0 million attributable

Au eq. oz. (+/- 5%) in 2026 and 2027.

2024 Q4 and full-year

highlights:

-

Margins4 of $1,565 per Au eq. oz. sold

in Q4 2024, and $1,373 for 2024.

- Operating cash

flow5 of $734.5 million in Q4 2024, and

$2,446.4 million in 2024.

- Attributable free cash

flow1 was $434.4 million in Q4 2024, and

$1,340.2 million in 2024, both of which are Company records.

- Reported net

earnings6 of $275.6 million in Q4 2024, or

$0.22 per share, and $948.8 million, or $0.77 per share, in

2024.

- Adjusted net

earnings7, 8 of $240.0

million, or $0.20 per share in Q4 2024, and $838.3 million, or

$0.68 per share, in 2024.

- Cash and cash

equivalents of $611.5 million, and total

liquidity9 of $2.3 billion at December

31, 2024. The Company also continued to prioritize debt reduction,

repaying the remaining balance on its term loan on February 10,

2025.

- Kinross’ Board of Directors

declared a quarterly dividend of $0.03 per common

share payable on March 20, 2025, to shareholders of record

at the close of business on March 5, 2025.

- Catherine McLeod-Seltzer has announced that she will not be

standing for election. Kelly Osborne, a Board member since 2015,

has been approved as Chair of the Board, effective upon his

re-election.

________________________

1 Unless otherwise stated, production figures in this news

release are on an attributable basis. “Attributable” includes

Kinross’ 70% share of Manh Choh production, costs and capital

expenditures. Financial figures include 100% of Manh Choh results

except when denoted as attributable. Attributable figures are

non-GAAP financial measures and ratios. Refer to footnote

7.

2 “Production cost of sales per equivalent ounce sold” is

defined as production cost of sales, as reported on the

consolidated statements of operations, divided by total gold

equivalent ounces sold.

3 Capital expenditures is reported as "Additions to

property, plant and equipment" on the consolidated statements of

cash flows.

4 “Margins” per equivalent ounce sold is defined as

average realized gold price per ounce less production cost of sales

per equivalent ounce sold.

5 Operating cash flow figures in this release represent

“Net cash flow provided from operating activities,” as reported on

the consolidated statements of cash flows.

6 Earnings, net earnings, and reported net

earnings figures in this release represent “Net earnings

attributable to common shareholders,” as reported on the

consolidated statements of operations.

7 These figures are non-GAAP financial measures and

ratios, as applicable. They are defined and actual results are

reconciled on pages 25 to 31 of this news

release. Non-GAAP financial measures and ratios have no

standardized meaning under International Financial Reporting

Standards “IFRS” and therefore, may not be comparable to similar

measures presented by other issuers.

8 Adjusted net earnings figures in this news release

represent “Adjusted net earnings attributable to common

shareholders.”

9 “Total liquidity” is defined as the sum of cash and cash

equivalents, as reported on the consolidated balance sheets, and

available credit under the Company’s credit facilities (as

calculated in Section 6 Liquidity and Capital Resources of Kinross’

MD&A for the year ended December 31, 2024).

Operational highlights:

- Tasiast delivered

record throughput, production and cash flow in 2024, and was the

highest-margin operation.

- Paracatu had

another strong year, delivering over 500,000 gold ounces for the

7th consecutive year.

- Fort Knox

significantly increased annual production as a result of first gold

from Manh Choh in Q3 2024.

Development project and exploration

highlights:

- At Great Bear, the

Advanced Exploration (AEX) program is making strong progress with

early works underway.

- At Bald Mountain,

approved the Redbird pit, extending mine life and adding ~1 million

gold ounces to reserves.

- At Lobo-Marte, the

dedicated project team is progressing baseline studies to support

permitting.

- At Round Mountain Phase

X, wide, high-grade intercepts in upper and lower targets,

confirming exploration thesis.

- At Curlew,

exploration efforts resulted in high-grade, high-quality resource

growth.

CEO Commentary:

J. Paul Rollinson, CEO, made the following comments in relation

to 2024 fourth-quarter and year-end results:

“2024 marked another excellent year for Kinross

and we have, once again, met our production and cost guidance. We

delivered record free cash flow7 of $1.3 billion, which

more than doubled year-over-year, repaid $800 million of debt, and

grew our margins by 37%, significantly outpacing the rise in gold

price.

“Three years ago, in February 2022, we acquired

Great Bear through a combination of cash and shares. I’m proud to

say that, since then, we have fully repaid the debt associated with

that acquisition and have fewer shares outstanding due to our share

buyback program. We have also outlined a high-grade resource and

published an attractive Preliminary Economic Assessment

demonstrating top-tier, high-margin production potential.

"We converted nearly 1 million resource ounces

to reserves at Bald Mountain, which, coupled with the receipt of

our Juniper permit in 2024, resulted in the decision to proceed

with mining at Redbird.

“In Sustainability, we advanced environmental,

social and governance initiatives across our host countries and

look forward to publishing our detailed 2024 Sustainability Report

in May. Highlights from 2024 include:

- Completed more than 15 energy efficiency projects across the

portfolio and on track to achieve 30% reduction in emissions

intensity by 2030;

- Provided flood relief aid to communities in the south of both

Mauritania and Brazil; and

- Recognized as the top gold company and in the top 10% overall

in The Globe and Mail’s corporate governance ranking.

“We are forecasting another strong year of

production of approximately 2.0 million gold equivalent ounces

while maintaining our consistent operational performance. Our

operational focus in 2025 will be on cost control, capital

discipline and delivering on planned grades. We are also

anticipating additional returns of capital to shareholders later in

2025.”

Financial results

Summary of financial and operating

results

|

|

Three months ended |

Years ended |

|

|

(in millions of U.S. dollars, except ounces, per share amounts, and

per ounce amounts) |

December 31, |

December 31, |

|

|

|

2024 |

|

2023 |

|

2024 |

|

|

2023 |

|

|

Operating

Highlights(a) |

|

|

|

|

|

|

Total gold equivalent ounces(b) |

|

|

|

|

|

|

Produced |

|

514,355 |

|

546,513 |

|

2,170,791 |

|

|

2,153,020 |

|

|

Sold |

|

531,729 |

|

565,389 |

|

2,153,212 |

|

|

2,179,936 |

|

|

|

|

|

|

|

|

|

Attributable gold equivalent ounces(b) |

|

|

|

|

|

|

Produced |

|

501,209 |

|

546,513 |

|

2,128,052 |

|

|

2,153,020 |

|

|

Sold |

|

517,980 |

|

565,389 |

|

2,111,688 |

|

|

2,179,936 |

|

|

|

|

|

|

|

|

|

Earnings(a) |

|

|

|

|

|

|

Metal sales |

$ |

1,415.8 |

$ |

1,115.7 |

$ |

5,148.8 |

|

$ |

4,239.7 |

|

|

Production cost of sales |

$ |

583.8 |

$ |

552.0 |

$ |

2,197.1 |

|

$ |

2,054.4 |

|

|

Depreciation, depletion and amortization |

$ |

284.8 |

$ |

271.7 |

$ |

1,147.5 |

|

$ |

986.8 |

|

|

Impairment charge (reversal) |

$ |

- |

$ |

38.9 |

$ |

(74.1 |

) |

$ |

38.9 |

|

|

Operating earnings |

$ |

501.1 |

$ |

193.5 |

$ |

1,540.3 |

|

$ |

801.4 |

|

|

Net earnings attributable to common shareholders |

$ |

275.6 |

$ |

65.4 |

$ |

948.8 |

|

$ |

416.3 |

|

|

Basic and diluted earnings per share attributable to common

shareholders |

$ |

0.22 |

$ |

0.06 |

$ |

0.77 |

|

$ |

0.34 |

|

|

Adjusted net earnings attributable to common

shareholders(c) |

$ |

240.0 |

$ |

140.0 |

$ |

838.3 |

|

$ |

539.8 |

|

|

Adjusted net earnings per share(c) |

$ |

0.20 |

$ |

0.11 |

$ |

0.68 |

|

$ |

0.44 |

|

|

|

|

|

|

|

|

|

Cash Flow(a) |

|

|

|

|

|

|

Net cash flow provided from operating activities |

$ |

734.5 |

$ |

410.9 |

$ |

2,446.4 |

|

$ |

1,605.3 |

|

|

Attributable adjusted operating cash flow(c) |

$ |

614.1 |

$ |

409.6 |

$ |

2,143.1 |

|

$ |

1,676.7 |

|

|

Capital expenditures(d) |

$ |

280.7 |

$ |

311.3 |

$ |

1,075.5 |

|

$ |

1,098.3 |

|

|

Attributable capital expenditures(c) |

$ |

278.8 |

$ |

297.7 |

$ |

1,050.9 |

|

$ |

1,055.0 |

|

|

Attributable free cash flow(c) |

$ |

434.4 |

$ |

116.7 |

$ |

1,340.2 |

|

$ |

559.7 |

|

|

|

|

|

|

|

|

|

Per Ounce

Metrics(a) |

|

|

|

|

|

|

Average realized gold price per ounce(e) |

$ |

2,663 |

$ |

1,974 |

$ |

2,393 |

|

$ |

1,945 |

|

|

Attributable average realized gold price per

ounce(c) |

$ |

2,665 |

$ |

1,974 |

$ |

2,391 |

|

$ |

1,945 |

|

|

Production cost of sales per equivalent ounce(b)

sold(f) |

$ |

1,098 |

$ |

976 |

$ |

1,020 |

|

$ |

942 |

|

|

Attributable production cost of sales per equivalent

ounce(b) sold(c) |

$ |

1,096 |

$ |

976 |

$ |

1,021 |

|

$ |

942 |

|

|

Attributable production cost of sales per ounce sold on a

by-product basis(c) |

$ |

1,069 |

$ |

936 |

$ |

988 |

|

$ |

892 |

|

|

Attributable all-in sustaining cost per equivalent

ounce(b) sold(c) |

$ |

1,510 |

$ |

1,353 |

$ |

1,388 |

|

$ |

1,316 |

|

|

Attributable all-in sustaining cost per ounce sold on a by-product

basis(c) |

$ |

1,490 |

$ |

1,328 |

$ |

1,365 |

|

$ |

1,284 |

|

|

Attributable all-in cost per equivalent ounce(b)

sold(c) |

$ |

1,868 |

$ |

1,709 |

$ |

1,739 |

|

$ |

1,634 |

|

|

Attributable all-in cost per ounce sold on a by-product

basis(c) |

$ |

1,854 |

$ |

1,699 |

$ |

1,725 |

|

$ |

1,619 |

|

(a) All measures and ratios include

100% of the results from Manh Choh, except measures and ratios

denoted as “attributable.” “Attributable” measures and ratios

include Kinross’ 70% share of Manh Choh production, sales, cash

flow, capital expenditures and costs, as applicable.

(b) “Gold equivalent ounces” include

silver ounces produced and sold converted to a gold equivalent

based on a ratio of the average spot market prices for the

commodities for each period. The ratio for the fourth quarter and

full year 2024 was 84.67:1 and 84.43:1, respectively (fourth

quarter and full year 2023 – 85.00:1 and 83.13:1,

respectively).

(c) The definition and reconciliation of

these non-GAAP financial measures and ratios is included on pages

25 to 31 of this news release. Non-GAAP financial measures and

ratios have no standardized meaning under IFRS and therefore, may

not be comparable to similar measures presented by other

issuers.

(d) “Capital expenditures” is as reported

as “Additions to property, plant and equipment” on the consolidated

statements of cash flows.

(e) “Average realized gold price per

ounce” is defined as gold revenue divided by total gold ounces

sold.

(f) “Production cost of sales

per equivalent ounce sold” is defined as production cost of sales

divided by total gold equivalent ounces sold.

The following operating and financial results

are based on fourth-quarter and year-end 2024 gold equivalent

production:

Production: Kinross produced

501,209 Au eq. oz. in Q4 2024, compared with 546,513 Au eq. oz. in

Q4 2023.

Over the full year, Kinross produced 2,128,052

Au eq. oz., largely in line with full-year 2023 production of

2,153,020 Au eq. oz.

Average realized gold

price10: The average realized gold price in Q4

2024 was $2,663 per ounce, compared with $1,974 per ounce in Q4

2023. For full-year 2024, the average realized gold price per ounce

was $2,393, compared with $1,945 per ounce for full-year 2023.

Revenue: During the fourth

quarter, revenue increased to $1,415.8 million, compared with

$1,115.7 million during Q4 2023. Revenue increased to $5,148.8

million for full-year 2024, compared with $4,239.7 million for

full-year 2023. The 21% year-over-year increase is primarily due to

the increase in the average realized gold price.

Production cost of sales:

Production cost of sales per Au eq. oz.2 sold was $1,098

for Q4 2024, compared with $976 in Q4 2023. Production cost of

sales per Au eq. oz.2 sold was $1,020 for full-year

2024, compared with $942 for full-year 2023.

Attributable production cost of sales per Au eq.

oz. sold1 was $1,096 in Q4 2024, compared with $976 in

Q4 2023, based on attributable gold sales of 517,980 ounces.

Attributable production cost of sales per Au eq. oz.

sold1 was $1,021 for full-year 2024, compared with $942

for full-year 2023, based on attributable gold sales of

2,111,688.

Margins4: Kinross’

margin per Au eq. oz. sold was $1,565 for Q4 2024, compared with

the Q4 2023 margin of $998. Full-year 2024 margin per Au eq. oz.

sold was $1,373, compared with $1,003 for full-year 2023.

Attributable all-in sustaining

cost1: Attributable all-in sustaining cost per

Au eq. oz. sold was $1,510 in Q4 2024, compared with $1,353 in Q4

2023. Full-year attributable all-in sustaining cost per Au eq. oz.

sold was $1,388, compared with $1,316 for full-year 2023.

In Q4 2024, attributable all-in sustaining cost

per Au oz. sold on a by-product basis1 was $1,490,

compared with $1,328 in Q4 2023. Attributable all-in sustaining

cost per Au oz. sold on a by-product basis1 was $1,365

for full-year 2024, compared with $1,284 in 2023.

Operating cash

flow5: Operating cash flow was $734.5 million

for Q4 2024, compared with $410.9 million for Q4 2023. Operating

cash flow for full-year 2024 was $2,446.4 million, compared with

$1,605.3 million for full-year 2023, primarily due to the increase

in margins and favourable working capital movements.

Attributable adjusted operating cash

flow1 for Q4 2024 was $614.1 million, compared with

$409.6 million for Q4 2023. Attributable adjusted operating cash

flow1 for full-year 2024 was $2,143.1 million, compared

with $1,676.7 million in 2023.

Attributable free cash

flow1: Record attributable

free cash flow was $434.4 million in Q4 2024, compared with $116.7

million in Q4 2023. Record attributable free cash flow for

full-year 2024 was $1,340.2 million compared with attributable free

cash flow of $559.7 million in 2023.

Earnings6: Reported

net earnings were $275.6 million for Q4 2024, or $0.22 per share,

compared with reported net earnings of $65.4 million, or $0.06 per

share, for Q4 2023. Full year reported net earnings in 2024 were

$948.8 million, or $0.77 per share, compared with reported net

earnings of $416.3 million, or $0.34 per share, in 2023.

Adjusted net earnings7, 8

were $240.0 million, or $0.20 per share, for Q4 2024, compared with

$140.0 million, or $0.11 per share, for Q4 2023. Full-year adjusted

net earnings7, 8 were $838.3 million, or

$0.68 per share, compared with $539.8 million, or $0.44 per share,

for full-year 2023.

Attributable capital

expenditures1: Attributable capital

expenditures were $278.8 million for Q4 2024, compared with $297.7

million for Q4 2023. Attributable capital expenditures for

full-year 2024 were $1,050.9 million, compared with $1,055.0

million in 2023, which included the start of Phase S development at

Round Mountain, continued work at Great Bear, and increased capital

development at Tasiast for West Branch 5.

________________________

10 “Average realized gold price per ounce” is defined as

gold revenue divided by total gold ounces sold.

Balance sheet

The Company continued to strengthen its balance

sheet by repaying $250.0 million on its term loan in the quarter,

totalling $800.0 million during 2024. The Company repaid the

remaining $200.0 million on February 10, 2025, completing repayment

of the $1.0 billion term loan.

Kinross had cash and cash equivalents of $611.5

million as of December 31, 2024, compared with $352.4 million at

December 31, 2023.

The Company had additional available

credit11 of $1.65 billion as of December 31, 2024, and

total liquidity9 of approximately $2.3 billion.

________________________

11 “Available credit” is defined as available credit under

the Company’s credit facilities and is calculated in Section 6

Liquidity and Capital Resources of Kinross’ MD&A for the year

ended December 31, 2024.

Return of capital

Kinross is committed to enhancing shareholder

returns through its continuing quarterly dividend. The dividend of

$0.03 per common share is payable on March 20, 2025, to

shareholders of record as of March 5, 2025.

Kinross is currently in the process of renewing

its normal course issuer bid with the Toronto Stock Exchange, and

at current gold prices, intends to reinstate a share buyback

program later in 2025.

Operating results

Mine-by-mine summaries for 2024 fourth-quarter

and full-year operating results may be found on pages 19 and 23 of

this news release. Highlights include the following:

Tasiast had another excellent

year in 2024, achieving record annual production and cash flow. The

record annual production was mainly a result of record throughput

following the completion of the Tasiast 24k project in the second

half of 2023. Quarter-over-quarter, production was lower as a

result of planned lower grades and mill maintenance, partially

offset by improvements in recovery.

Tasiast’s full-year cost of sales per ounce sold

was higher year-over-year primarily due to higher royalties as

a result of the increase in gold prices and higher labour

costs, largely offset by a higher proportion of costs allocated to

capital development. Cost of sales per ounce sold increased

quarter-over-quarter, mainly due to the decrease in

production.

At Paracatu, full-year

production decreased compared with 2023, mainly as a result of

lower grades due to planned mine sequencing into harder material in

the southwest area of the pit. Cost of sales per ounce sold was

higher year-over-year due to lower production, higher drilling

contractor and blasting supply costs, partially offset by

favourable foreign exchange rates. Production decreased

quarter-over-quarter mainly due to the lower throughput from the

timing of mill maintenance and mine sequencing. Cost of sales per

ounce sold was higher quarter-over-quarter due to the decrease in

production, partially offset by favorable foreign exchange

rates. In 2025, annual production is expected to increase as

the site moves into higher-grade portions of the mine plan.

At La Coipa, full year

production decreased compared with 2023 due to a decrease in silver

grades and throughput, partially offset by an increase in gold

grades. Production increased quarter-over-quarter due to higher

throughput. Cost of sales per ounce sold was higher in both

comparable periods primarily due to a lower proportion of mining

activities related to capital development in 2024 and higher mill

maintenance costs and optimization, partially offset by favourable

foreign exchange rates. Kinross continues to progress permitting

work for mine life extensions at La Coipa.

Full-year production at Fort

Knox increased significantly compared with 2023, primarily

due to first production from the higher-grade, higher-recovery ore

from Manh Choh in the second half of 2024. Cost of sales per ounce

sold was in line with 2023. Quarter-over-quarter production

decreased and cost of sales per ounce sold increased due to the

timing of processing Manh Choh ore, which was more heavily weighted

to Q3 2024.

At Round Mountain, full-year

production decreased compared with 2023 due to fewer ounces

recovered from the heap leach pads, partially offset by higher mill

production. Cost of sales per ounce sold was in line with 2023.

Quarter-over-quarter, production was in line and cost of sales per

ounce sold increased largely due to higher cost ounces produced

from the heap leach pads.

At Bald Mountain, full-year

production increased compared with 2023 due to higher grades.

Full-year cost of sales per ounce sold decreased mainly due to

lower supplies costs and higher production, partially offset by a

lower proportion of mining activities related to capital

development. Quarter-over-quarter, production was largely in line

and cost of sales per ounce sold was lower mainly due to the timing

of sales.

Development projects

Great Bear

At Great Bear, Kinross

continues to progress its AEX program and Main Project

permitting.

For the AEX program, early works, including tree

clearing and earthworks, has commenced with the necessary permits

received for all current activities. The two remaining permits

required for full AEX completion and operation are under review by

the regulatory authorities and are expected to be received later in

the year, when they are required. Detailed engineering and

procurement continue to advance.

The Company is focused on progressing AEX

activities including construction of the exploration decline

planned to commence in late 2025.

For the Main Project, Kinross is advancing

detailed engineering and execution planning. The selection of

design partners is well underway and work is planned to commence in

Q1 2025. This work will provide key engineering information for

permitting and construction.

The Company continues to work with the Impact

Assessment Agency of Canada on advancing its Impact Statement,

which is planned to be submitted later in 2025.

Consultation continues with designated Indigenous communities,

including discussions to finalize related agreements.

In 2025, Kinross has shifted from deep

underground resource drilling to regional exploration work with the

goal of identifying new open pit and underground deposits.

Kinross released its Preliminary Economic

Assessment for Great Bear on September 10, 2024. The Project is

expected to produce over 500,000 ounces per year at an all-in

sustaining cost of approximately $800 per ounce during the

first 8 years through a conventional, modest capital 10,000 tonne

per day mill. In parallel, Kinross also released an updated mineral

resource estimate increasing the inferred resource estimate by 568

koz. to 3.9 Moz. which was in addition to the M&I resource

estimate of 2.7 Moz.

Bald Mountain Redbird

Kinross is pleased to announce plans to proceed

with mining at the Redbird pit at Bald

Mountain, which contains approximately 1 million oz. of

gold reserve, following the receipt of the Juniper permit in the

second half of 2024.

Kinross has approved mining of Phase 1 at

Redbird, which contains 270 koz. and is expected to produce

approximately 175 koz., extending production into 2028. Phase 2,

unlocking another 680 koz. contained, could begin in 2026 and

extend production from Bald Mountain through 2031.

Phase 1 lowers the initial capital risk by

leveraging existing heap leach infrastructure, pulls forward

production into 2027, and can progress in 2025 while work continues

on optimizing the design and execution plan for Phase 2.

Phase 1 initial capex of $120 million is

primarily pre-strip mining cost, and the project has an all-in

sustaining cost of approximately $1,500/oz.

Lobo-Marte

Kinross is progressing baseline studies to

support the Environmental Impact Assessment (EIA) for the

Lobo-Marte project. Lobo-Marte continues to be a

potential large, low-cost mine and Kinross is committed to

progressing next steps to advance the project.

Company Guidance

The following section of the news release represents

forward-looking information and users are cautioned that actual

results may vary. We refer to the risks and assumptions contained

in the Cautionary Statement on Forward-Looking Information on pages

41 and 42 of this news release.

This Company Guidance section below

references attributable production cost of sales per equivalent

ounce, attributable all-in sustaining cost per equivalent ounce

sold, and sustaining, non-sustaining and attributable capital

expenditures, which are non-GAAP ratios and financial measures, as

applicable, with no standardized meaning under IFRS and therefore,

may not be comparable to similar measures presented by other

issuers. The definitions of these non-GAAP ratios and financial

measures and comparable reconciliations are included on pages

25 to 31 of this news release.

Attributable1

production guidance

In 2025, Kinross expects to produce 2.0 million

attributable Au eq. oz.12 (+/- 5%) from its operations.

Production is expected to remain stable at 2.0 million attributable

Au eq. oz.12 (+/- 5%) for each of 2026 and

2027. In 2024, Kinross produced 2.13 Au eq. oz.

Annual attributable1

gold equivalent production guidance

(+/- 5%) |

|

2025 |

2.0 million oz. |

|

2026 |

2.0 million oz. |

|

2027 |

2.0 million oz. |

________________________

12 Attributable gold equivalent ounce production guidance

for 2025 includes approximately 4.3 million ounces of

silver.

Attributable1

cost guidance

Attributable production cost of sales is

expected to be $1,120 per Au eq. oz.1 (+/- 5%) for 2025.

In 2024, production cost of sales2 and attributable

production cost of sales1 were $1,020 per Au eq. oz. and

$1,021 per Au eq. oz., respectively. The moderate year-over-year

increase in 2025 is mainly due to lower overall production with a

change in sales mix, including lower production at Tasiast, and

inflationary impacts.

The Company expects its attributable all-in

sustaining cost1 to be $1,500 per Au eq. oz. (+/- 5%)

for 2025. In 2024, attributable all-in sustaining cost1

was $1,388 per Au eq. oz. sold. The expected increase in 2025 is

largely a result of the increase in attributable production cost of

sales.

2025 attributable1

production and cost guidance

|

|

Q4 2024

results |

2024 full-year

results |

2025 guidance

(+/- 5%) |

|

Gold equivalent basis |

|

|

|

|

Production (Au eq. oz.) |

501,209 |

2.13 million |

2.0 million11 |

|

Attributable production cost of sales per Au eq. oz.

sold1 |

$1,096 |

$1,021 |

$1,120 |

|

Production cost of sales per Au eq. oz. sold2 |

$1,098 |

$1,020 |

|

|

Attributable all-in sustaining cost per Au eq. oz.

sold1 |

$1,510 |

$1,388 |

$1,500 |

2025 attributable1

production and cost guidance by country

|

Country |

2025

attributable production guidance

(Au eq. oz.)1, 12

(+/-5%) |

|

Percentage of total forecast

production13 |

|

2025

attributable production cost of sales guidance

(per Au eq. oz. sold)1,12

(+/-5%) |

|

2024

production cost of sales

(per Au eq. oz. sold)2 |

|

2024

attributable production cost of sales

(per Au eq. oz. sold)2 |

|

Mauritania |

500,000 |

|

25% |

|

$860 |

|

$681 |

|

$681 |

|

Brazil |

585,000 |

|

29% |

|

$1,025 |

|

$1,039 |

|

$1,039 |

|

Chile |

230,000 |

|

12% |

|

$1,060 |

|

$959 |

|

$959 |

|

United States |

685,000 |

|

34% |

|

$1,420 |

|

$1,295 |

|

$1,313 |

|

TOTAL |

2.0 million |

|

100% |

|

$1,120 |

|

$1,020 |

|

$1,021 |

Material assumptions used to forecast 2025 guidance, most notably

relating to production cost of sales, are as follows:

- a gold price of $2,500 per

ounce;

- a silver price of $30 per

ounce;

- an oil price of $80 per

barrel;

- foreign exchange rates of:

- 5.25 Brazilian reais to the U.S.

dollar;

- 900 Chilean pesos to the U.S.

dollar;

- 37.50 Mauritanian ouguiyas to the

U.S. dollar; and

- 1.35 Canadian dollars to the U.S.

dollar;

Taking into account existing currency and oil hedges:

- a 10% change in foreign currency

exchange rates14 would be expected to result in an

approximate $25 impact on attributable production cost of sales per

equivalent ounce sold1;

- specific to the Brazilian real, a

10% change in this exchange rate would be expected to result in an

approximate $45 impact on Brazilian attributable production cost of

sales per equivalent ounce sold1;

- specific to the Chilean peso, a 10%

change in this exchange rate would be expected to result in an

approximate $50 impact on Chilean attributable production cost of

sales per equivalent ounce sold1;

- a $10 per barrel change in the

price of oil would be expected to result in an approximate $3

impact on fuel consumption costs on attributable production cost of

sales per equivalent ounce sold1; and

- a $100 change in the price of gold

would be expected to result in an approximate $5 impact on

attributable production cost of sales per equivalent ounce

sold1 as a result of a change in royalties.

________________________

13 The percentages are calculated based on the mid-point

of country 2025 forecast production.

14 Refers to all of the currencies in the countries where

the Company has mining operations, fluctuating simultaneously by

10% in the same direction, either appreciating or depreciating,

taking into consideration the impact of hedging and the weighting

of each currency within our consolidated cost

structure.

Attributable capital

expenditures15

guidance

Attributable capital expenditures for 2025 are

forecast to be approximately $1,150 million (+/- 5%) and are

summarized in the table below. In 2024, capital

expenditures3 and attributable capital expenditures were

$1,076 million and $1,051 million, respectively.

Kinross’ attributable capital expenditures

outlook for 2026 and 2027 is approximately expected to be in line

with 2025, subject to ongoing inflationary impacts.

Country |

Forecast 2025

sustaining capital15

(+/-5%)

(attributable)

(million) |

|

Forecast 2025

non-sustaining capital15

(+/-5%)

(attributable)

(million) |

|

Total 2025 forecast

capital15

(+/-5%)

(attributable)

(million)

|

|

2024

sustaining capital15

(million)

|

|

2024 non-sustaining capital15

(million)

|

|

2024 total

capital15

(consolidated)

(million)

|

|

2024 total

capital15

(attributable)

(million)

|

|

Mauritania |

$105 |

|

$255 |

|

$360 |

|

$64 |

|

$280 |

|

$344 |

|

$344 |

|

Brazil |

$195 |

|

$0 |

|

$195 |

|

$141 |

|

$0 |

|

$141 |

|

$141 |

|

Chile |

$50 |

|

$10 |

|

$60 |

|

$66 |

|

$15 |

|

$81 |

|

$81 |

|

U.S. |

$185 |

|

$200 |

|

$385 |

|

$257 |

|

$211 |

|

$468 |

|

$443 |

Canada

and other |

$0 |

|

$150 |

|

$150 |

|

$(1) |

|

$43 |

|

$42 |

|

$42 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL |

$535 |

|

$615 |

|

$1,150 |

|

$527 |

|

$549 |

|

$1,076 |

|

$1,051 |

2025 sustaining capital15 includes the

following forecast spending estimates:

|

• |

Mine development: |

|

$55 million (United States), $10 million (Chile), $20 million

(Mauritania) |

|

• |

Mobile equipment: |

|

$65 million (United States), $90

million (Brazil), $5 million (Chile), $35 million (Mauritania) |

|

• |

Mill facilities:

|

|

$5 million (United States), $25

million (Brazil), $20 million (Chile), $10 million

(Mauritania) |

•

|

Leach facilities: |

|

$25 million (United States), $5

million (Chile) |

|

• |

Tailings facilities: |

|

$5 million (United States), $75

million (Brazil), $5 million (Chile), $10 million (Mauritania) |

|

|

|

|

|

2025 non-sustaining

capital15 includes the following forecast

spending estimates:

|

• |

Tasiast West Branch stripping: |

|

$255 million |

|

• |

Great Bear AEX construction, detailed engineering and other: |

|

$150 million |

|

• |

Bald Mountain Redbird 1: |

|

$75 million |

|

• |

Round Mountain Phase S: |

|

$75 million |

________________________

15 Forecast 2025 sustaining, non-sustaining and

total forecast capital expenditures are on an attributable basis

and include Kinross’ share of Manh Choh (70%) capital expenditures.

Actual results as reported for the year ended December 31, 2024,

for sustaining, non-sustaining and total capital expenditures

(refer to footnote 3) are on a total basis and include 100% of Manh

Choh capital expenditures. Sustaining, non-sustaining and

attributable capital expenditures are non-GAAP financial measures

(refer to footnote 7) and are defined and reconciled on pages 30

and 31 of this news release.

Other 2025 guidance

|

Category |

|

2025 Guidance |

|

Summary |

|

|

Exploration and Business Development ($M) |

|

$200 (+/- 5%) |

|

2025 guidance includes approximately $175 million of exploration

spend on brownfields, minex and greenfields exploration targets

(2024 – $166.4 million).

For details about the 2025 exploration program, see page 11. |

|

|

General and Administrative ($M) |

|

$125 (+/- 5%) |

|

In line with 2024 results. |

|

|

Other Operating Costs ($M) |

|

$125-$150 |

|

Primarily relates to studies and permitting activities that do not

meet the criteria for capitalization, as well as care and

maintenance and reclamation activities at non-operating sites. |

|

|

Effective Tax Rate (ETR)16 |

|

32% - 37% |

|

ETR based on adjusted net earnings. |

|

|

Taxes paid (cash) ($M) |

|

$330 |

|

Taxes paid is expected to increase by approximately $4 million for

every $100/oz movement in the realized gold price. |

|

|

DD&A ($/oz.)17 |

|

$540 (+/- 5%) |

|

In line with 2024 results. |

|

|

Interest paid ($M) (incl. capitalized interest) |

|

$75 |

|

Includes approximately $20 million of capitalized interest and $55

million of interest expense.

Interest expense excludes accretion of the Company’s reclamation

and remediation obligations, as well as lease liabilities, which

for 2024 totaled $42.3 million.

(2024 – Total interest paid of $128.2 million, of which $92.6

million was capitalized. The 2025 decrease is due to the full

repayment of the term loan on February 10th,

2025.)

|

|

________________________

16 The

forecast ETR range for 2025 assumes gold price, foreign exchange

and tax rates in the jurisdictions in which the Company operates

remain stable and within 2025 guidance assumptions. The ETR does

not include the impact of items which the Company believes are not

reflective of the Company’s underlying performance, such as the

impact of net foreign currency translations on tax deductions and

taxes related to prior periods. Management believes that the ETR

range provides investors with the ability to better evaluate the

Company’s underlying performance. However, the ETR range is not

necessarily an indicator of tax expense recognized under IFRS. The

rate is sensitive to the relative proportion of sales between the

Company’s various tax jurisdictions and realized gold

prices.

17 DD&A ($/oz) is defined as depreciation,

depletion and amortization, as reported on the consolidated

statements of operations, divided by total gold equivalent ounces

sold.

Sustainability

Kinross continued to deliver strong

sustainability performance throughout the year, reflected in strong

Sustainability scores as measured by MSCI, LSEG, Moody’s, and

Sustainalytics, and was named to the S&P 2025 Global

Sustainability Yearbook for the 12th time since 2012.

Kinross’ robust approach to

environmental performance includes advancing its

climate change strategy. The Company is on track to achieve its

greenhouse gas (GHG) target of reducing emissions intensity by 30%

by 2030 from its 2021 baseline. In 2024, Kinross implemented more

than 15 energy efficiency projects across sites, including haul

route optimization, switching from diesel generators to electricity

at fuel islands and lime silos, incorporation of electric buses,

and other energy efficiency initiatives. The Company also advanced

its estimation of Scope 3 GHG emissions and completed outreach with

the suppliers representing the majority of total spend to

understand their approaches to emissions reduction.

Kinross engages directly with local

communities around its operations to understand

their economic, social and development

goals, working together to ensure that meaningful, long-term

benefits are realized through job creation, training programs,

procurement, tax payments, and targeted community programs. Flood

relief aid was provided to communities in the south of both

Mauritania and Brazil, including essential food supplies and

emergency shelter. Paracatu worked with the World Gold Council to

publish a video demonstrating

the positive impact of community partnerships to support programs

and projects that enhance the well-being of local people, with a

particular focus on sustainability after mine closure. Kinross was

also recognized with a 2024 award for Business Achievement in

Sustainability by the Canadian Council for the Americas.

Kinross’ robust

corporate governance standards for its

Board of Directors continue to be driven by a focus on delivering

value through a mix of skills and experience, diversity, director

independence and succession planning. Kinross was the top scoring

gold mining company in The Globe and Mail’s annual

corporate governance ranking and increased its score by four points

from 2023, ranking in the top 10% of companies overall.

Exploration update

In 2024, approximately 318,000 metres of

drilling was completed for all exploration projects (brownfields,

minex and greenfields).

Brownfields and minex

exploration

The Company’s brownfields and minex exploration

efforts – which accounted for approximately 85% of the Company’s

exploration – continued to focus within the footprint of existing

mines and projects during 2024.

Great Bear

Kinross’ exploration efforts at Great Bear in

2024 primarily focused on directional drilling beyond the

1,000-metre depth to show the underground potential of the asset,

resulting in the addition of 568 koz. to the inferred resource,

which was updated in September along with the release of a PEA.

The 2024 drilling intersected mineralization

beyond the current resource and PEA inventory across multiple zones

up to a vertical depth of 1,600 metres, demonstrating the system is

still open with continuation of high-grade mineralization at depth

and highlighting the potential for further resource additions.

Given the costs of drilling to this depth from

surface and the significant resource already identified, late last

year the exploration focus shifted to regional exploration work on

the ~120 square kilometre land package to look for additional open

pit and underground opportunities. In parallel, work on the AEX

decline will be progressed to support future exploration at LP from

underground.

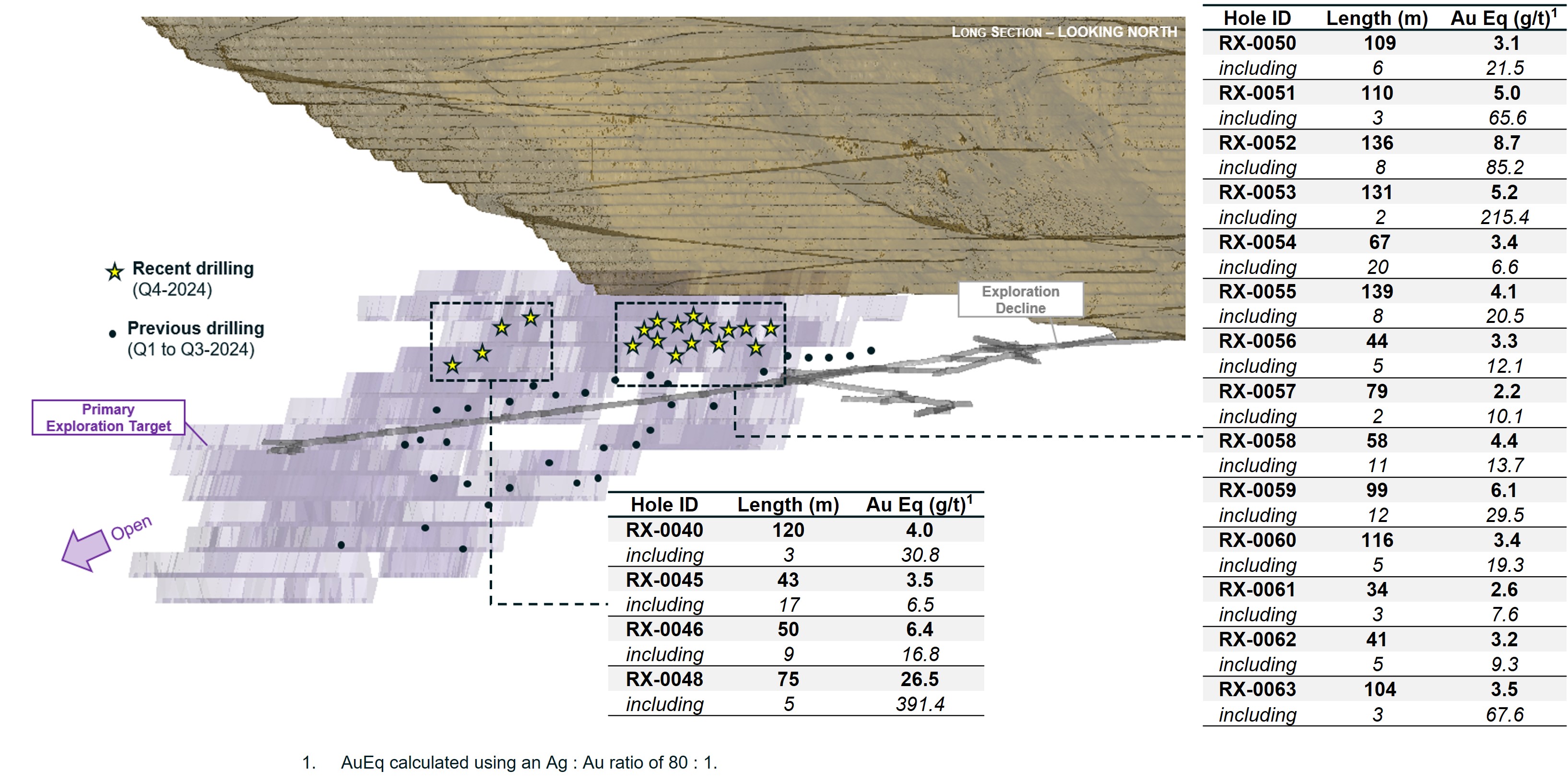

Round Mountain

At Phase X, drilling in Q4 expanded infill

drilling into the upper zone of the primary exploration target,

with results showing numerous intercepts with strong widths and

grades, supporting the thesis of potential for bulk mining at Phase

X. Approximately 21,000 metres have been drilled at Phase X since

starting the exploration decline in 2023. The program in 2024

successfully intersected both the upper and lower exploration

targets, demonstrating continuous wide mineralization with strong

grades, confirming our exploration thesis. Highlights from 2024

drilling include:

- RX-0050 – 109m @ 3.1 g/t Au

- Including 6m @ 21.5 g/t Au

- RX-0051 – 110m @5.0 g/t Au

- Including 3m @ 65.6 g/t Au

- RX-0052 – 136m @ 8.7 g/t Au

- Including 8m @ 85.2 g/t Au

- RX-0053 – 131m @ 5.2 g/t Au

- Including 2m @ 215.4 g/t Au

- RX-0054 – 67m @ 3.4 g/t Au

- Including 20m @ 6.6 g/t Au

- RX-0055 – 139m @ 4.1 g/t Au

- Including 8m @ 20.5 g/t Au

- RX-0056 – 44m @ 3.3 g/t Au

- Including 5m @ 12.1 g/t Au

- RX-0057 – 79m @ 2.2 g/t Au

- Including 2m @ 10.1 g/t Au

- RX-0058 – 58m @ 4.4 g/t Au

- Including 11m @ 13.7 g/t Au

- RX-0059 – 99m @ 6.1 g/t Au

- Including 12m @ 29.5 g/t Au

- RX-0060 – 116m @ 3.4 g/t Au

- Including 5m @ 19.3 g/t Au

- RX-0061 – 34m @ 2.6 g/t Au

- Including 3m @ 7.6 g/t Au

- RX-0062 – 41m @ 3.2 g/t Au

- Including 5m @ 9.3 g/t Au

- RX-0063 – 104m @ 3.5 g/t Au

- Including 3m @ 67.6 g/t Au

In 2025 Kinross will focus on completing infill

drilling of the exploration target at Phase X to support further

studies to progress the project.

At Gold Hill, approximately 5,000 metres of

drilling were completed both from the bottom of the pit to better

define the vein system and from surface, which extended one of the

main targets 150 metres on strike.

Curlew Basin

The 30,400 metre 2024 drilling program at Curlew

Basin successfully targeted higher grade extensions of

mineralization and delivered the following successes:

- Inferred resource addition of 125

koz with a strong average grade of 9.0 g/t Au at the North Stealth

Zone, which remains open on strike and dip.

- Intersected further high-grade

mineralization at the Roadrunner vein system (reported in Q3 2023

14.2m @ 16.5 g/t Au, includes 7.3m @ 25.3 g/t Au).

- Confirmed extensions and continuity

in several other vein zones with multiple wide, high-grade

intercepts. Highlights include:

- WZ-1456 – 2.3m @ 448.9 g/t Au,

including 1.0m @ 1045.4 g/t Au

- K5-1469 – 4.9m @15.2 g/t Au,

including 2.3m @ 22.78 g/t Au

- ST-1211 – 8.5m @ 7.9 g/t Au,

including 1.4m @ 12.68 g/t Au

In 2025, Kinross plans to continue this focus on

higher-grade mineralization, targeting new discoveries and

extensions of mineralization at North Stealth and Roadrunner.

Alaska

Drilling this year at Fort Knox focused on

growth at two main targets: around the satellite Gil pit and around

the Fort Knox pit. The growth highlights at Fort Knox have not been

included in the current resource update and may offer potential to

augment medium-term production plans at Fort Knox.

Gil highlights include:

- GC24-872 – 9.9m @ 1.5 g/t Au

- GC24-874 – 10.1m @ 3.4 g/t Au,

including 2.0m @ 6.4 g/t Au

- GC24-876 – 9.4m @ 7.1 g/t Au,

including 1.8m @ 23.8 g/t Au

- GC24-877 – 6.2m @ 6.2 g/t Au,

including 1.4m @ 24.6 g/t Au

Fort Knox highlights include:

- FFC24-1912 – 2.3m @ 2.9 g/t Au

- FFC24-1913 – 3.3m @ 5.0 g/t Au

- FFC24-1916 – 15.4m @ 0.9 g/t

Au

An additional 2,466 metres of drilling occurred

on the Fort Knox property, testing new target areas between the

Fort Knox and Gil mines.

In 2025, drilling at Fort Knox will continue to

focus on growth opportunities at Gil and around the Fort Knox pit,

and will also target exploration along the structural trend between

the Fort Knox and Gil deposits.

At Manh Choh, 4,760 metres of drilling was

completed across six target areas identifying encouraging skarn

alteration at three targets that will be followed up on in 2025.

Surface sampling to identify new drill targets was completed along

the mine road corridor and greater Tetlin lease in 2024.

Bald Mountain

Exploration drilling at Bald Mountain in 2024

focused on low-strip, near-pit extensions in the North and South

area of operations and within the Bida trend, with roughly 21,000

metres drilled in the year on brownfields and minex programs.

2025 drilling will be focused on conversion of

inferred resources at the Redbird pit and on generative projects

looking for new deposits on the large, highly prospective land

package at Bald Mountain.

Tasiast

At Tasiast, drill testing of the West Branch

orebody at depth, to provide additional data for assessing future

underground mining, commenced in the second half of the year. Wide

zones of mineralization have been intersected down plunge of the

current underground resource of 1.1 Moz. at 2.52 g/t, extending

mineralization on strike and down plunge 700 metres to date.

At Fennec, which is a satellite deposit on the

TMLSA license, work completed during the year resulted in the

addition of 110 koz. to reserve.

On the SENISA licenses, two RC and two diamond

drill rigs were actively drilling target areas. A total of 51,135

metres had been drilled by year end and drilling will continue

throughout 2025.

Chile

The brownfields drilling program further

delineated the gold porphyry mineralization potential at Cerros

Bravos. The porphyry is located approximately 8 kilometres due

north of Kinross’ mine facilities. Step out drilling and geophysics

carried out in 2024 helped define new targets for further work in

2025 at Cerros Bravos.

2025 drilling in Chile will also focus on existing known trends

on the La Coipa license looking for extensions of previously mined

orebodies and for new mineralization.

Brazil

Brownfields exploration focused on

systematically testing targets on the Company’s extensive land

packages, which extend over 35 kilometres along the northwest

corridor from the Paracatu mine, with results showing similar style

and grade of mineralization to Paracatu. Along the south corridor

from Paracatu, reconnaissance mapping, soil sampling, and ground IP

and Lidar surveys were also completed in 2024, generating

additional targets, which will be drill tested in 2025.

Greenfields exploration

update

The greenfields exploration strategy is to

identify and explore in areas that have the potential to host

high-grade gold deposits. The Company looks for opportunities where

it can stake its own claims or collaborate with high-quality junior

exploration companies through either joint venture agreements or

via equity investment. The primary focus is exploring for orogenic,

epithermal, Carlin and intrusion related gold and gold-copper style

deposits.

The greenfields exploration programs in 2024

were focused on targets located in Canada, the U.S.A. and Finland

with approximately 45,000 metres of drilling completed on all

projects.

Canada

Outside of Great Bear, the focus in Canada was

primarily on the large land holdings in Snow Lake, Manitoba, where

Kinross has 100% ownership of six exploration properties: Laguna,

Laguna North, Puella Bay, Lucky Jack, DSN and SLG.

Drilling on the Laguna and the Laguna North

properties has continued to define and extend high-grade

mineralization on multiple gold rich, shear hosted vein systems.

Kinross is focused on expanding identified veins and discovering

additional vein systems on the property to increase the critical

mass of mineralization to support further work.

Kinross is also progressing prospecting and

mapping on the SLG property to find new veins after identifying a

200 metres long shear zone in 2023. The 2024 work identified two

new shear zones 1.5 kilometres and 4 kilometres from the 2023 shear

zone, with grab samples on the new zones showing strong grades

including 78.9 g/t, 38.2 g/t, 30.8 g/t, 23.9 g/t, 14.2 g/t,13.75

g/t, 13.25 g/t, and 12.25 g/t within quartz veins.

Outside of Manitoba, Kinross has 100% ownership

of four greenfield exploration properties in northwest Ontario,

three of which are in the Red Lake district outside of the Great

Bear property. Initial reconnaissance mapping and prospecting on

one of those properties yielded grab samples of 12.35 g/t, 2.3 g/t,

3.55 g/t, 3.17 g/t and 5.16 g/t Au in newly identified quartz

veins. Kinross plans to follow-up with detailed mapping and

prospecting in 2025.

In October 2024, an option agreement was signed

with Puma Exploration Inc. for a 65% interest in their Williams

Brook property in New Brunswick. The Williams Brook project has

seen early-stage work completed by Puma which has identified 5

anomalous zones including Lynx, Tiger, Cheetah, Jaguar, and Cougar.

Highlights from each target include 5.55 g/t Au over 50.15m at Lynx

and grab samples of values up to up to 34 g/t Au at Jaguar, 60.10

g/t Au at Cougar, 6.69 g/t Au at Cheetah and 19.9 g/t Au at

Tiger.

U.S.A.

Kinross holds a number of projects in Nevada

that are either 100% owned or are in joint venture with private

individuals, or state agencies. Work on Kinross’ Nevada projects in

2024 included geophysics, prospecting, mapping, and RC and diamond

drilling of early-stage targets.

In March 2024, a joint venture was established

with Riley Gold Corporation on its PWC project, which is contiguous

with the western boundary of Nevada Gold Mines’ Pipeline Complex.

In September 2024, Kinross completed an initial diamond drill hole,

designed to test for favourable lower plate carbonate Carlin-type

host rocks. The initial 1,095 metre drill hole successfully

intercepted the favourable lower plate carbonates starting at a

depth of 715 metres, demonstrating that known Cortez District host

lithologies exist at explorable drill depths over a large, untested

area. Further drilling will begin in Q2 2025.

Work continues evaluating and advancing new

pipeline projects through third party agreements and on

opportunistic claim staking and drill testing of opportunities in

the principal metallogenic belts throughout the U.S. Great Basin,

including the Walker Lane and the primary trends of Carlin-type

deposits.

Finland

Kinross is progressing exploration on its own

land positions and with joint venture partners in Finland on the

Central Lapland Greenstone Belt, along a greenstone belt of similar

scale to the Abitibi that has had limited historical gold

exploration and development. Kinross’ land positions are proximal

to Agnico Eagle’s Kittilä Gold mine and Rupert Resource’s Ikkari

gold deposit, which reported more than 4 million ounces at 2.2 g/t

Au in indicated resources.

Work in 2024 included approximately 11,000

meters of base-of-till drilling which is used to test the surface

of bedrock under cover for gold anomalies. Base-of-till drilling

was used successfully in the discoveries of Rupert Resource’s

Ikkari gold deposit and Agnico Eagle’s Kittilä gold mine, and the

work on Kinross’ properties in 2024 identified numerous gold

anomalies.

Kinross also completed approximately 4,800

metres of diamond drilling to follow up on identified gold

anomalies in 2024, with results showing encouraging gold grades at

Launi-East including 5.23 g/t over 3.65m and 10.05 g/t over 0.95m.

Kinross will continue to follow up on identified targets in

2025.

2025 Focus

2025 exploration expenditure guidance

(brownfields, minex and greenfields) is $175 million (+/-5%)

compared with the $166.4 million spent in 2024. The 2025 programs

are designed to follow-up on existing zones of mineralization and

to make new discoveries in all of Kinross’ jurisdictions.

Priority exploration projects:

- At Great Bear, focused on the

discovery of new open pit and underground targets outside of the

LP, Hinge and Limb areas on Kinross’ 120 square kilometre land

package

- At Curlew, delineate and extend

zones of high-grade mineralization at North Stealth and

Roadrunner

- At Round Mountain, complete initial

infill drilling of the Phase X exploration target

- At Tasiast, underground potential

focused drilling from surface at West Branch, Prolongation and

Piment, as well as continued exploration of the SENISA land package

and on satellite deposits on the TMLSA land package

- In Chile, drill test a number of greenfields and brownfields,

targeting both porphyry and high sulphidation epithermal styles of

mineralization as well as extension of known oxide deposits

- At Paracatu, test targets along the

mine trend

- In Canada, continue to explore on

the large Snow Lake, Manitoba land package

Appendix A: Refer to page 39 of

this news release for supplementary illustrations.

Full drill results are available here: https://www.kinross.com/Exploration-Drill-Results-Appendix-A-Q4-YE-2024

2024 Mineral Reserves and Mineral Resources

update

(See the Company’s detailed Annual

Mineral Reserve and Mineral Resource Statement estimated as at

December 31, 2024 and explanatory notes starting at page

33.)

Kinross increased its gold price assumptions

from $1,400 per ounce to $1,600 per ounce for its mineral reserve

estimates and from $1,700 per ounce to $2,000 per ounce for its

mineral resource estimates, as of December 31,

202418.

The Company also increased its silver price

assumptions to $20 per ounce and $25 per ounce for its mineral

reserve and mineral resource estimates, respectively.

Kinross continues to prioritize quality,

high-margin, low-cost ounces in its portfolio, and maintained its

fully loaded costing methodology.

Kinross is focused on upgrading the quality of

its resources through delineating high-grade gold ounces with the

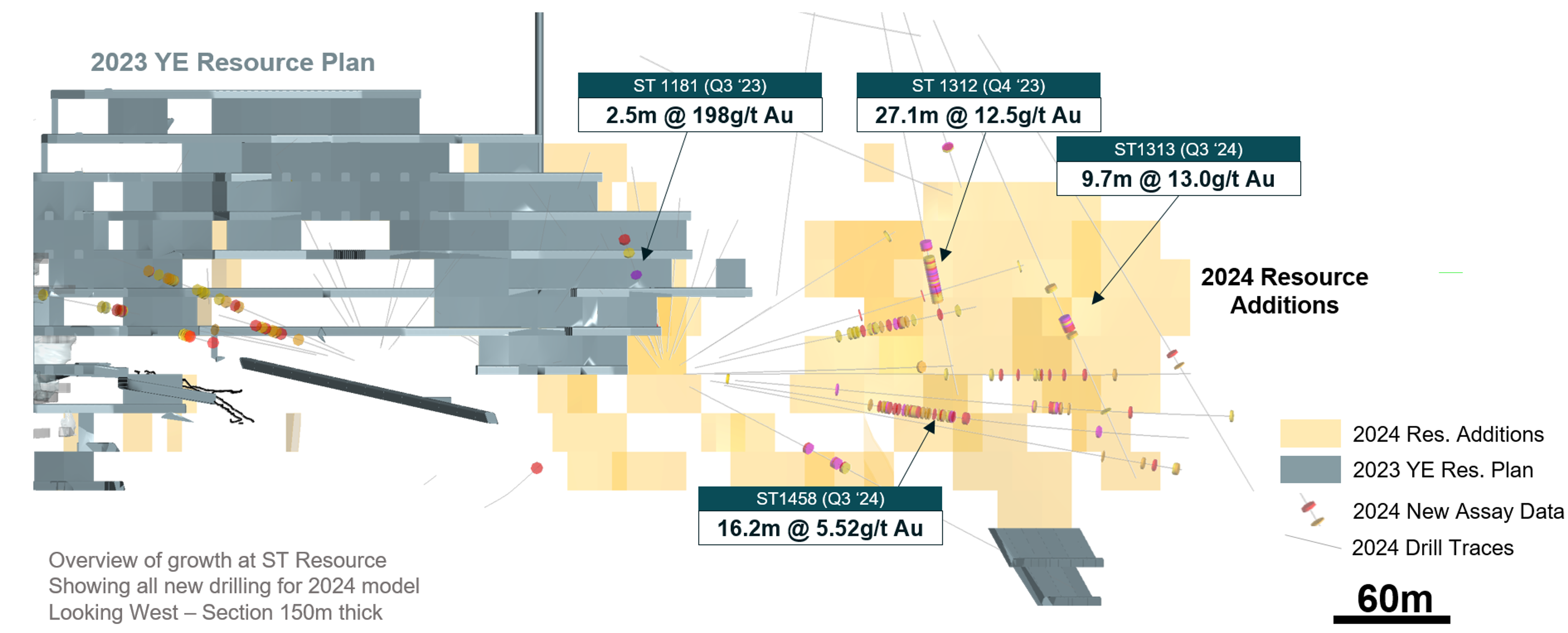

objective of converting to reserves. In 2024, Kinross added 1.7

million ounces to its inferred resource, which included high-grade

additions at both Great Bear and Curlew.

|

Kinross Gold Mineral Reserve and Mineral Resource

estimates19 |

|

|

2023

(Au koz.) |

Depletion

(Au koz.) |

Geology & Engineering

(Au koz.) |

2024

(Au koz.) |

|

Proven and Probable Reserves |

22,757 |

(2,360) |

1,461 |

21,857 |

|

Measured and Indicated Resources |

25,968 |

11820 |

(220) |

25,867 |

|

Inferred Resources |

11,484 |

(25) |

1,734 |

13,193 |

________________________

18 Please see pages 36 and 37 for Mineral Reserve and

Mineral Resource Statement Notes.

19 Rounding of values to the 000s may result in apparent

discrepancies.

20 M&I depletion is positive due to the addition of 221

koz. stockpile to resource at Tasiast in

2024.

Proven and Probable Mineral

Reserves

Kinross’ total proven and probable mineral

reserve estimates decreased by 4%, or 0.9 million Au oz., to 21.9

million Au oz. at year-end 2024 compared with 22.8 million Au oz.

at year-end 2023. The net decrease was mostly due to depletion,

with decreases offset by a net increase of 1.5 million ounces

driven by increases at Bald Mountain, Tasiast, and Paracatu.

Bald Mountain reserves increased by 971 koz.

before depletion driven by conversion of resources to reserves at

Redbird after receiving permits for the Juniper land

package.

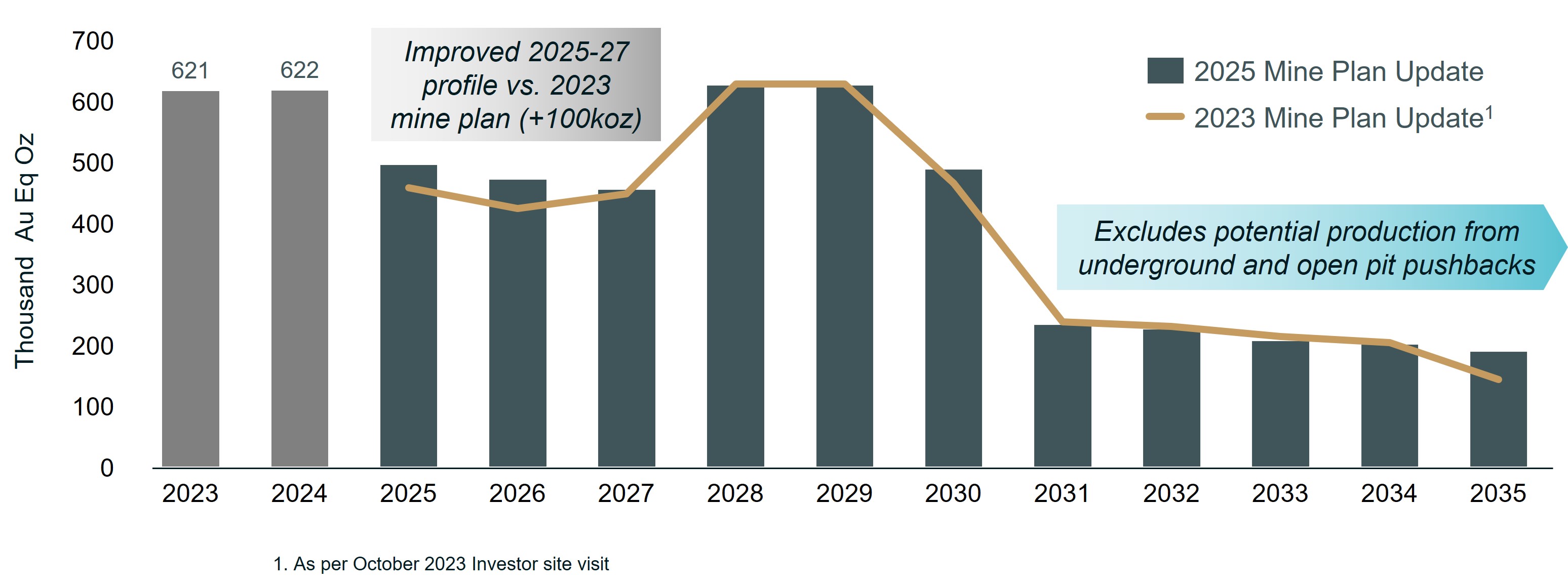

At Tasiast, a new life of mine plan has been

completed following the 2024 reserve update. Production from

Tasiast from 2025 through 2027 is decreasing compared to 2024

driven by mine plan sequencing and lower grades during the

stripping phase of West Branch 5. The new life of mine plan has

shown an increase of 100 koz. over that 3-year period as compared

to the previous life of mine plan on the back of operational

improvements, design optimizations, and the addition of the Fennec

satellite pit.

The following graph illustrates Tasiast’s

reserve and mine plan update:

Measured and Indicated Mineral

Resources

Kinross’ total measured and indicated mineral

resource estimate at year-end 2024 was 25.9 million Au oz. compared

with 26.0 million Au oz. at year-end 2023. The slight decrease is

the result of net growth on the higher gold price and new drilling

less the conversion of resources to reserves.

Inferred Mineral Resources

Kinross’ total inferred mineral resource

estimate increased by 15% or 1.7 million Au oz. to 13.2 million Au

oz. at year-end 2024, compared with 11.5 million Au oz. at year-end

2023. The increase in net growth, with additions from most sites

across the portfolio, was driven by new drilling at Great Bear and

Curlew and growth on higher gold price.

Board update

As previously disclosed, Catherine

McLeod-Seltzer, an independent Board member since 2005 and Chair of

the Board since 2019, has announced that she will not be

standing for election at the Company’s annual meeting of

shareholders in May 2025. Following a robust succession process,

Kelly Osborne has been approved as Chair of the Board, effective

upon his re-election as an independent director at the Company’s

annual meeting of shareholders on May 7, 2025.

Ms. McLeod-Seltzer has made numerous and

significant contributions during her 20-year directorship at the

Company. She has overseen the dramatic reshaping of Kinross’

portfolio as the Company exited and entered new operating

jurisdictions, acquired the Great Bear development project, and

lead the strong focus on debt reduction and returning capital to

shareholders. During her tenure, she championed diversity at all

levels of the organization, including at the Board level and Senior

Leadership Team, drove a results-based focus on Sustainability

performance, and also oversaw a number of key governance

initiatives including an effective Board succession program that

has added six new Directors during her tenure as Chair.

Ms. McLeod-Seltzer’s extensive leadership,

having been a founder, Board member and Chief Executive Officer in

numerous mineral companies, has been recognized with several

awards: She was named “Mining Man of the Year” by The Northern

Miner in 1999; given the “Award for Performance” in 1997 and

the Peak Award for Significant Board Contribution in 2021 by the

Association of Women in Finance; named on the Financial Post’s

“Power 50”; has received the “Canada’s Most Powerful Women Top 100

Award”; and was named one of “100 Global Inspirational Women in

Mining” in 2013 and 2016 by Women In Mining (UK).

Mr. Osborne, an independent Director of Kinross

since 2015, has served on the Corporate Governance and Nominating

Committee and Corporate Responsibility and Technical Committee

during his tenure, and served as Chair of the Corporate

Responsibility and Technical Committee from 2018 until 2024. In

addition, Mr. Osborne had an extensive career in the mining

industry as an operator and senior executive, most recently serving

as the CEO of a U.S.-based, wholly owned subsidiary of Antofagasta

plc., until his retirement in June 2022.

“We are pleased that Kelly Osborne will take on

the role of Independent Chair and look forward to his guidance and

stewardship as we continue to deliver value for our shareholders,”

said J. Paul Rollinson, CEO. “On behalf of the Board and Kinross

management, I would like to extend a sincere thank you to Catherine

for her leadership and dedication to the Company over the last 20

years. Catherine has been a central part of our culture and values,

and the strong position Kinross is in today is largely due to her

support as we advanced and executed on our strategic

priorities."

The Board of Directors has appointed Dr. George

Albino as a Director with an effective date of January 1, 2025. Dr.

Albino is a geologist with over 45 years of experience in mining

and finance, including 19 years as a sell-side mining analyst

primarily focused on gold stocks. Dr. Albino was previously a

Director with Eldorado Gold Corporation, including serving as

Chair, and a Director with Orla Mining. He holds a Ph.D. in

Economic Geology and Geochemistry from the University of Western

Ontario, a M.Sc. in Economic Geology from Colorado State

University, and a B.A.Sc. in Geological Engineering from Queen’s

University.

Conference call details

In connection with this news release, Kinross

will hold a conference call and audio webcast on Thursday, February

13, 2025, at 8 a.m. ET to discuss the results, followed by a

question-and-answer session. To access the call, please dial:

Canada & US toll-free – +1

(888) 596-4144; Passcode: 8057299

Outside of Canada & US – +1 (646) 968-2525;

Passcode: 8057299

Replay (available up to 14 days after the

call):

Canada & US toll-free – +1 (800) 770-2030;

Passcode: 8057299

Outside of Canada & US – +1 (647) 362-9199;

Passcode: 8057299

You may also access the conference call on a

listen-only basis via webcast at our website www.kinross.com. The

audio webcast will be archived on www.kinross.com.

This release should be read in conjunction with

Kinross’ 2024 year-end Financial Statements and Management’s

Discussion and Analysis report at www.kinross.com. Kinross’ 2024

year-end Financial Statements and Management’s Discussion and

Analysis have been filed with Canadian securities regulators

(available at www.sedarplus.ca) and furnished

with the U.S. Securities and Exchange Commission (available at

www.sec.gov). Kinross

shareholders may obtain a copy of the financial statements free of

charge upon request to the Company.

About Kinross Gold Corporation

Kinross is a Canadian-based global senior gold

mining company with operations and projects in the United States,

Brazil, Mauritania, Chile and Canada. Our focus is on delivering

value based on the core principles of responsible mining,

operational excellence, disciplined growth, and balance sheet

strength. Kinross maintains listings on the Toronto Stock Exchange

(symbol: K) and the New York Stock Exchange (symbol: KGC).

Media Contact

Victoria Barrington

Senior Director, Corporate Communications

phone: 647-788-4153

victoria.barrington@kinross.com

Investor Relations Contact

David Shaver

Senior Vice-President, Investor Relations &

Communications

phone: 416-365-2761

InvestorRelations@Kinross.com

Review of operations

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Three months ended December 31, |

|

Gold equivalent ounces |

|

|

|

|

|

|

|

|

|

|

Produced |

|

Sold |

|

Production cost of

sales

($millions) |

|

Production cost of

sales/equivalent ounce sold |

|

|

2024 |

|

2023 |

|

2024 |

|

2023 |

|

2024 |

|

2023 |

|

2024 |

|

2023 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tasiast |

139,411 |

|

160,764 |

|

144,041 |

|

171,199 |

|

104.4 |

|

110.4 |

|

725 |

|

645 |

|

Paracatu |

123,899 |

|

127,940 |

|

124,690 |

|

132,886 |

|

131.6 |

|

144.2 |

|

1,055 |

|

1,085 |

|

La Coipa |

58,533 |

|

73,823 |

|

57,852 |

|

73,477 |

|

68.2 |

|

52.9 |

|

1,179 |

|

720 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fort Knox |

104,901 |

|

84,215 |

|

108,512 |

|

81,306 |

|

141.0 |

|

104.3 |

|

1,299 |

|

1,283 |

|

Round Mountain |

42,969 |

|

55,764 |

|

45,342 |

|

56,495 |

|

80.0 |

|

82.6 |

|

1,764 |

|

1,462 |

|

Bald Mountain |

44,642 |

|

44,007 |

|

51,291 |

|

49,375 |

|

58.7 |

|

57.1 |

|

1,144 |

|

1,156 |

|

United States Total |

192,512 |

|

183,986 |

|

205,145 |

|

187,176 |

|

279.7 |

|

244.0 |

|

1,363 |

|

1,304 |

|

Less: Manh Choh non-controlling interest (30%) |

(13,146 |

) |

- |

|

(13,749 |

) |

- |

|

(15.9 |

) |

- |

|

|

|

|

|

United States Attributable Total |

179,366 |

|

183,986 |

|

191,396 |

|

187,176 |

|

263.8 |

|

244.0 |

|

1,378 |

|

1,304 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operations

Total(a) |

514,355 |

|

546,513 |

|

531,729 |

|

565,389 |

|

583.8 |

|

552.0 |

|

1,098 |

|

976 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Attributable

Total(a) |

501,209 |

|

546,513 |

|

517,980 |

|

565,389 |

|

567.9 |

|

552.0 |

|

1,096 |

|

976 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Years ended December 31, |

|

Gold equivalent ounces |

|

|

|

|

|

|

|

|

|

|

Produced |

|

Sold |

|

Production cost of

sales

($millions) |

|

Production cost of sales/equivalent ounce

sold |

|

|

2024 |

|

2023 |

|

2024 |

|

2023 |

|

2024 |

|

2023 |

|

2024 |

|

2023 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tasiast |

622,394 |

|

620,793 |

|

609,614 |

|

615,065 |

|

415.4 |

|

406.8 |

|

681 |

|

661 |

|

Paracatu |

528,574 |

|

587,999 |

|

528,209 |

|

592,224 |

|

548.6 |

|

538.6 |

|

1,039 |

|

909 |

|

La Coipa |

246,131 |

|

260,138 |

|

241,077 |

|

268,491 |

|

231.3 |

|

182.8 |

|

959 |

|

681 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fort Knox |

377,258 |

|

290,651 |

|

375,402 |

|

287,532 |

|

452.5 |

|

343.5 |

|

1,205 |

|

1,195 |

|

Round Mountain |

215,387 |

|

235,690 |

|

214,996 |

|

234,064 |

|

328.3 |

|

357.7 |

|

1,527 |

|

1,528 |

|

Bald Mountain |

181,047 |

|

157,749 |

|

182,760 |

|

180,139 |

|

220.3 |

|

223.5 |

|

1,205 |

|

1,241 |

|

United States Total |

773,692 |

|

684,090 |

|

773,158 |

|

701,735 |

|

1,001.1 |

|

924.7 |

|

1,295 |

|

1,318 |

|

Less: Manh Choh non-controlling interest (30%) |

(42,739 |

) |

- |

|

(41,524 |

) |

- |

|

(40.8 |

) |

- |

|

|

|

|

|

United States Attributable Total |

730,953 |

|

684,090 |

|

731,634 |

|

701,735 |

|

960.3 |

|

924.7 |

|

1,313 |

|

1,318 |

|

|

|

|

|

|

|

|

|