As filed with the U.S. Securities and Exchange Commission on November 14, 2024.

Registration No. 333-282423

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

–––––––––––––––––––––––––––

AMENDMENT NO.1

TO

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

–––––––––––––––––––––––––––

Zhibao Technology Inc.

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

–––––––––––––––––––––––––––

|

Cayman Islands

|

|

6411

|

|

Not Applicable

|

|

(State or other jurisdiction of

incorporation or organization)

|

|

(Primary Standard Industrial

Classification Code Number)

|

|

(I.R.S. Employer

Identification number)

|

Floor 3, Building 6, Wuxing Road, Lane 727

Pudong New Area, Shanghai 201204

Tel: +86 (21) -5089-6502

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive office)

–––––––––––––––––––––––––––

Puglisi & Associates

850 Library Avenue, Suite 204

Newark, DE 19711

Tel: (302) 738-6680

(Name, address, including zip code, and telephone number, including area code, of agent for service)

–––––––––––––––––––––––––––

Copies to:

Richard I. Anslow, Esq.

Lijia Sanchez, Esq.

Ellenoff Grossman & Schole LLP

1345 Avenue of the Americas, 11th Floor

New York, NY 10105

Tel: (212) 370-1300

–––––––––––––––––––––––––––

Approximate date of commencement of proposed sale to the public: From time to time after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. The Selling Shareholder named in this prospectus may not sell these securities until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and the Selling Shareholder is not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

|

PRELIMINARY PROSPECTUS

|

|

Subject to Completion, DATED NOVEMBER 14, 2024

|

Up to 3,282,563 Class A Ordinary Shares

Issuable upon Conversion of a Senior Secured Convertible Promissory Note

Up to 154,050 Class A Ordinary Shares

Issuable upon Exercise of Warrants

Up to 984,769 Class A Ordinary Shares

Issuable upon Exercise of a Pre-Funded Warrant

Zhibao Technology Inc.

This prospectus relates to the resale, from time to time, by an institutional investor (the “Investor” or “Selling Shareholder”) identified in this prospectus under the caption “Selling Shareholder,” of (i) an aggregate of up to 3,282,563 Class A ordinary shares, par value $$0.0001 per share of Zhibao Technology Inc., which the Investor may acquire upon the full conversion of a senior secured 10% original issue discount convertible promissory note (the “Note”), (ii) an aggregate of up to 154,050 Class A ordinary shares, which the Investor may acquire upon the exercise of the outstanding warrants (each a “Common Warrant,” and collectively, the “Common Warrants”), and (iii) an aggregate of up to 984,769 Class A ordinary shares, which the Investor may acquire upon the exercise of the pre-funded warrant (each a “Pre-Funded Warrant,” and collectively, the “Pre-Funded Warrants,” together with the Common Warrants, the “Warrants”), exercisable only upon the occurrence of an Event of Default (as defined in the Note). We issued the Note and the Warrants to the Selling Shareholder in a private placement offering (the “Private Placement”), pursuant to the terms and condition of a securities purchase agreement, dated as of September 23, 2024, by and between the Company and the Investor (the “Securities Purchase Agreement”), where EF Hutton LLC acted as the sole placement agent in the Private Placement.

We are not selling any securities under this prospectus, and we will not receive proceeds from the sale of our Class A ordinary shares by the Selling Shareholder. However, we may receive proceeds from the cash exercise of the Common Warrants, which, if exercised in cash at the current applicable exercise price of (i) $4.71 per share with respect to 74,451 Class A ordinary shares and (ii) $4.47 per share with respect to 79,599 Class A ordinary shares, would result in gross proceeds to us of approximately $0.7 million. See “Use of Proceeds” beginning on page 64 and “Plan of Distribution” beginning on page 69 of this prospectus for more information.

We will pay the expenses of registering the Class A ordinary shares offered by this prospectus, but all selling and other expenses incurred by the Selling Shareholder will be paid by the Selling Shareholder. The Selling Shareholder may sell our Class A ordinary shares offered by this prospectus from time to time on terms to be determined at the time of sale through ordinary brokerage transactions or through any other means described in this prospectus under “Plan of Distribution.” The prices at which the Selling Shareholder may sell shares will be determined by the prevailing market price for our Class A ordinary shares or in negotiated transactions.

Our Class A ordinary shares are traded on the Nasdaq Capital Market, or Nasdaq, under the symbol “ZBAO.” On November 5, 2024, the last reported sale price for our Class A ordinary shares was $3.68 per share.

We are both an “emerging growth company” and a “foreign private issuer” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings. We are also a “controlled company” under the Nasdaq Rules. See “Prospectus Summary — Implications of Being an Emerging Growth Company”, “Prospectus Summary — Implications of Being a Foreign Private Issuer” and “Prospectus Summary — Implications of Being a Controlled Company.”

We currently have two classes of ordinary shares outstanding: Class A ordinary shares and Class B ordinary shares. The rights of the holders of our Class A ordinary shares and Class B ordinary shares are identical, except with respect to voting and conversion. Each Class A ordinary share is entitled to one vote and each Class B ordinary share is entitled to

Table of Contents

twenty votes. Each Class B ordinary share is convertible into one Class A ordinary share at the option of the holder of such Class B ordinary share at any time, but Class A ordinary shares shall not be convertible into Class B ordinary shares under any circumstances. Upon any transfer of Class B ordinary shares by a holder to any person or entity other than holders of Class B ordinary shares or their affiliates, such Class B ordinary shares shall be automatically and immediately converted into the equivalent number of Class A ordinary shares. Holders of Class A ordinary shares and Class B ordinary shares will vote together as a single class on all matters submitted to vote of our shareholders, unless otherwise required by law or our amended and restated memorandum and articles of association.

We may rely on dividends and other distributions on equity paid by our PRC Subsidiaries for our cash and financing requirements and we expect that our distribution of earnings or settlement of amounts owed will be done through our PRC Subsidiaries. If any of our PRC Subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict its ability to pay dividends to us. For a description of factors that may affect the ability of our PRC subsidiaries to transfer cash or assets to us, see” Prospectus Summary — Dividend and Other Distributions or Assets Transfer among Zhibao and Its Subsidiaries” on page 10. See “Risk Factors — Risks Related to Doing Business in China — We may rely on dividends and other distributions on equity paid by our PRC Subsidiaries to fund any cash and financing requirements we may have, and the PRC Subsidiaries’ restrictions on paying dividends or making other payments to us could restrict our ability to satisfy our liquidity requirements and have a material and adverse effect on our ability to conduct our business” on page 35.

Investors are cautioned that we are not a PRC operating company but a Cayman Islands holding company with operations conducted by our PRC Subsidiaries in China, and that you are purchasing shares of Zhibao, a Cayman Islands holding company instead of purchasing equity securities of our PRC Subsidiaries that have business operations in China and you may never hold any equity interests in our PRC Subsidiaries in China. We control and receive the economic benefits of our PRC Subsidiaries’ business operation, if any, through equity ownership. We do not have, nor had we ever, have a variable interest entity (“VIE”) structure. Our corporate structure, i.e., a Cayman Islands holding company with operations conducted by our PRC Subsidiaries, involves unique risks to investors. The PRC regulatory authorities could disallow this structure, which would likely result in a material change in our operations and/or a material change in the value of the securities we are registering for sale, including a significant decline in the value of such securities or such securities becoming worthless.

Investing in our securities involves a high degree of risk. Before buying any Class A ordinary shares, you should carefully read the discussion of the material risks of investing in our Class A ordinary shares under the heading “Risk Factors” beginning on page 21 of this prospectus and “Item 3. Key Information — D. Risk Factors” in our annual report on Form 20-F for the fiscal year ended June 30, 2024 (the “2024 Annual Report”) filed with the U.S. Securities and Exchange Commission (“SEC”) on October 31, 2024 for more information.

There are significant legal and operational risks associated with having operating structure as a Cayman Islands holding company with substantially all of operations conducted by our PRC Subsidiaries in China, including changes in the legal, political and economic policies of the PRC government, the relations between China and the United States, or Chinese or United States regulations, which risks could result in a material change in our operations and/or the value of the securities we are registering for sale, or could significantly limit or completely hinder our ability to continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. Given the PRC government’s authority, oversight may also extend to Zhibao Technology Limited (“Zhibao HK”), our Hong Kong subsidiary, and the legal and operational risks associated with operating in mainland China could also apply to Zhibao HK. Hong Kong is a special administrative region of the PRC and the basic policies of the PRC regarding Hong Kong are reflected in the Basic Law, namely, Hong Kong’s constitutional document, which provides Hong Kong with a high degree of autonomy and executive, legislative and independent judicial powers, including that of final adjudication under the principle of “one country, two systems”. We cannot assure you that there will not be any changes in the economic, political and legal environment in Hong Kong. We may be subject to uncertainty about any future actions of the PRC government and is possible that most of the legal and operational risks associated with operating in the PRC may also apply to the PRC operating entities’ operations in Hong Kong if they conduct business in Hong Kong in the future. The PRC government may intervene or influence the PRC operating entities’ future operations in Hong Kong at any time and exert more influence over the manner in which the PRC operating entities must conduct their business activities. Such government actions, if and when they occur, could result in a material change in their future operations in Hong Kong. As of the date of this prospectus, our Hong Kong subsidiary is only a holding company with no business operations since its incorporation in Hong Kong, and we believe the Hong Kong Laws and ordinances have no impact on our ability to conduct our business through our PRC Subsidiaries, accept

Table of Contents

foreign investment or listing on an U.S. exchange. For a description of our corporate structure as well as related risks, see “Corporate History and Structure” beginning on page 73, “Risk Factors — The PRC government exerts substantial influence over the manner in which we conduct our business activities. The PRC government may also intervene or influence our operations and this offering at any time, which could result in a material change in our operations and our Class A ordinary shares could decline in value or become worthless” beginning on page 27, and “Risk Factors — Within our direct holding structure, substantial uncertainties exist with respect to the requirement of National Financial Regulatory Administration and how it may impact the viability of our current corporate structure, corporate governance and business operations” on page 41.

We are both an “emerging growth company” and a “foreign private issuer” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings. We are also a “controlled company” under the Nasdaq Rules. See “Prospectus Summary — Implications of Being an Emerging Growth Company”, “Prospectus Summary — Implications of Being a Foreign Private Issuer” and “Prospectus Summary — Implications of Being a Controlled Company.”

Our officers and directors have significant influence over the Company due to their significant shareholding in the Company. Mr. Botao Ma, our Chairman of the board of directors and our Chief Executive Officer beneficially holding 16,579,977 Class B ordinary shares, beneficially own approximately 52.60% of our issued and outstanding ordinary shares (including Class A ordinary shares and Class B ordinary shares) and is able to exercise approximately 94.47% of the total voting power of our issued and outstanding ordinary shares. For more information regarding Mr. Ma’s beneficial ownership, see “Principal Shareholders” and “Risk Factors — Risks Related to Offering and Ownership of Class A Ordinary Shares — Our Chief Executive Officer and Chairman of the board of directors, Mr. Botao Ma, has a significant influence over our company. His interests may not be aligned with the interests of our other shareholders and he could prevent or cause a change of control or other transactions, which may cause a material decline in the value of our Class A ordinary shares” on page 54. As a result of Mr. Ma’s significant ownership, we may be deemed a “controlled company” under Nasdaq Rules. However, we do not intend to avail ourselves of the corporate governance exemptions offered to a “controlled company” under the Nasdaq Rules. See “Prospectus Summary — Implications of Being a Controlled Company.”

On December 28, 2021, the Cybersecurity Review Measures (2021 version) was promulgated and became effective on February 15, 2022, which iterates that any “online platform operators” possessing personal information of more than one million users which seeks to list in a foreign stock exchange should be subject to cybersecurity review. The Cybersecurity Review Measures (2021 version), further elaborates the factors to be considered when assessing the national security risks of the relevant activities, including, among others, (i) the risk of core data, important data or a large amount of personal information being stolen, leaked, destroyed, and illegally used or exited the country; and (ii) the risk of critical information infrastructure, core data, important data or a large amount of personal information being affected, controlled, or maliciously used by foreign governments after listing abroad. The Cyberspace Administration of China (“CAC”) requires that under the new rules, companies possessing personal information of more than 1,000,000 users must now apply for cybersecurity approval when seeking listings in other nations because of the risk that such data and personal information could be “affected, controlled, and maliciously exploited by foreign governments.” The cybersecurity review will also look into the potential national security risks from overseas IPOs. As a network platform operator who possesses personal information of more than one million users for purposes of the Cybersecurity Review Measures (2021 version), we have applied for and completed a cybersecurity review with respect to our initial public offering closed on April 3, 2024 (the “IPO”) and we are not required to do the cybersecurity review for this offering, pursuant to the Cybersecurity Review Measures (2021 version). See “Risk Factors — Risks Related to Doing Business in China — Uncertainties in the interpretation and enforcement of PRC laws and regulations could limit the legal protections available to you and us” beginning on page 24 and “Risk Factors — Risks Related to Doing Business in China — Our business processes a certain quantity of personal information, and failure to protect private or sensitive information of customers or improper handling of such information could have a material and adverse effect on our business. In light of recent events indicating greater oversight by the Cyberspace Administration of China, or CAC, over data security, we are subject to a variety of laws and other obligations regarding cybersecurity and data protection, and any failure to comply with applicable laws and obligations could have a material and adverse effect on our business, financial condition, results of operations, and the offering” beginning on page 27.

On February 17, 2023, the China Securities Regulatory Commission (the “CSRC”) released the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies (the “Trial Measures”) with five interpretive guidelines (together with the New Overseas Listing Rules, collectively, the “New Overseas

Table of Contents

Listing Rules”), which came into effect on March 31, 2023. The New Overseas Listing Rules apply to overseas securities offerings and/or listings conducted by (i) companies incorporated in the PRC, or PRC domestic companies, directly and (ii) companies incorporated overseas with operations primarily in the PRC and valued on the basis of interests in PRC domestic companies, or indirect offerings. Under the New Overseas Listing Rules, a filing-based regulatory system applies to “indirect overseas offerings and listings” of companies in mainland China, which refers to securities offerings and listings in an overseas market made under the name of an offshore entity but based on the underlying equity, assets, earnings or other similar rights of a company in mainland China that operates its main business in mainland China. The New Overseas Listing Rules state that, any post-listing follow-on offering by an issuer in an overseas market, including issuance of shares, convertible notes, exchangeable notes and preferred shares, shall be subject to filing requirement within three business days after the completion of the offering. Additionally, if we do not obtain the permissions and approvals of the filing procedure for any subsequent offering in a timely manner under PRC laws and regulations, we may be subject to investigations by competent PRC regulators, fines or penalties, ordered to suspend our relevant operations and rectify any non-compliance, prohibited from engaging in relevant business or conducting any offering, and these risks could result in a material adverse change in our operations, limit our ability to continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless. Based on our understanding of the rules, we are required to submit the filing report to the CSRC within three business days upon the first closing of the transactions contemplated under the Securities Purchase Agreements and report share issuance status to the CSRC upon completion of all subsequent closings. On September 26, 2024, we made the initial CSRC Filing with the CSRC and will report share issuance status to the CSRC upon completion of all subsequent closings in compliance with New Overseas Listing Rules. It is uncertain whether such filing can be completed or how long it will take to complete such filing. Any delay in completing such filing procedures might affect the other filing procedures with respect to other applicable circumstances, under the New Overseas Listing Rules in the future, such as the secondary listing, primary listing, spin-off listing and making overseas offering and listing anew after being delisted from an overseas exchange, which might affect our future public market financings and capital market transactions. To date, there are uncertainties in the interpretation and enforcement of these new laws and guidelines, which could materially and adversely impact our business and financial outlook and may impact our ability to accept foreign investments, or continue to list on a U.S. or other foreign exchange. See “Risks Related to Doing Business in China — The CSRC released the New Overseas Listing Rules for China-based companies seeking to conduct overseas offering and listing in foreign markets, effective as of March 31, 2023. Under the New Overseas Listing Rules, the PRC government exerts more oversight and control over offerings that are conducted overseas and foreign investment in China-based issuers, which could significantly limit or completely hinder our ability to continue to offer our Class A ordinary shares to investors and could cause the value of our Class A ordinary shares to significantly decline or such shares to become worthless” beginning on page 37 for a description of the New Overseas Listing Rules and how they may impact our company and this offering.

Furthermore, as more stringent criteria have been imposed by the U.S. Securities and Exchange Commission and the Public Company Accounting Oversight Board (the “PCAOB”) recently, trading in our Class A ordinary shares may be prohibited if the PCAOB determines that it cannot completely inspect or investigate our auditor, and as a result Nasdaq may determine to delist our Class A ordinary shares. Pursuant to the Holding Foreign Companies Accountable Act (the “HFCA Act”), if the PCAOB is unable to inspect an issuer’s auditors for three consecutive years, the issuer’s securities are prohibited to trade on a U.S. stock exchange. On December 16, 2021, the PCAOB issued its determination that the PCAOB is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong, because of positions taken by PRC authorities in those jurisdictions, and the PCAOB included in the report of its determination a list of the accounting firms that are headquartered in mainland China or Hong Kong. On August 26, 2022, the “CSRC, the Ministry of Finance of the PRC (the “MOF”), and the PCAOB signed a Statement of Protocol (the “Protocol”) to allow the PCAOB to inspect and investigate completely registered public accounting firms headquartered in mainland China and Hong Kong, consistent with the HFCA Act, and the PCAOB will be required to reassess its determinations by the end of 2022. Pursuant to the fact sheet with respect to the Protocol disclosed by the SEC, the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and has the unfettered ability to transfer information to the SEC. On December 15, 2022, the PCAOB announced that it was able to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong completely. On December 29, 2022, the Accelerating Holding Foreign Companies Accountable Act was enacted, which amended the HFCA Act by decreasing the number of non-inspection years from three years to two, thus reducing the time period before our Class A ordinary shares may be prohibited from trading or delisted. Our auditor, Marcum Asia CPAs LLP, the headquarter of which is based in New York, is currently subject to inspection by the PCAOB at least every

Table of Contents

three years. Therefore, it is not subject to the determinations announced by the PCAOB on December 16, 2021 as it is not on the list published by the PCAOB. However, our auditor’s China affiliate is located in, and organized under the laws of the PRC. We cannot assure you that we will not be identified by the SEC under the HFCA Act as an issuer that has retained an auditor that has a branch or office located in a foreign jurisdiction that the PCAOB determines it is unable to inspect or investigate completely because of a position taken by an authority in that foreign jurisdiction. In the event the PRC authorities would further strengthen regulations over auditing work of the PRC companies listed on the U.S. stock exchanges, which would prohibit our current auditor to perform work in China, then we would need to change our auditor and the audit workpapers prepared by our new auditor may not be inspected by the PCAOB without the approval of the PRC authorities, in which case the PCAOB may not be able to fully evaluate the audit or the auditors’ quality control procedures. In addition, there can be no assurance that, if we have a “non-inspection” year, we will be able to take any remedial measures. If any such event were to occur, trading in our securities could in the future be prohibited under the HFCA Act and, as a result, we cannot assure you that we will be able to maintain the listing of our Class A ordinary shares on Nasdaq or that you will be allowed to trade our Class A ordinary shares in the United States on the “over-the-counter” markets or otherwise. Notwithstanding the foregoing, in the event it is later determined that the PCAOB is unable to inspect or investigate completely our auditor, then such lack of inspection could cause our securities to be delisted from the stock exchange. See “Risk Factors — Risks Related to Doing Business in China — Our Class A ordinary shares may be delisted under the HFCA Act if the PRC adopts positions at any time in the future that would prevent the PCAOB from continuing to inspect or investigate completely accounting firms headquartered in mainland China or Hong Kong. The delisting of our Class A ordinary shares, or the threat of their being delisted, may materially and adversely affect the value of your investment. Furthermore, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which amends the HFCA Act and requires the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three, thus reducing the time before our Class A ordinary shares may be prohibited from trading or delisted. The HFCA Act, the Accelerating Holding Foreign Companies Accountable Act, which amends the HFCA Act, together with recent joint statement by the SEC and PCAOB, the PCAOB’s determinations, and the Nasdaq rule changes all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. These developments add uncertainties to our offering.” beginning on page 21 of this prospectus.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense. The securities are not being offered in any jurisdiction where the offer is not permitted.

The date of this prospectus is [ ], 2024.

Table of Contents

TABLE OF CONTENTS

This prospectus is part of a registration statement that we have filed with the Securities and Exchange Commission (the “SEC”). We incorporate by reference important information into this prospectus. You may obtain the information incorporated by reference without charge by following the instructions under “Where You Can Find More Information.” This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus forms a part, and you may obtain copies of those documents as described below. You should carefully read this prospectus as well as additional information described under “Incorporation of Certain Information by Reference,” before deciding to invest in our securities. This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.”

i

Table of Contents

ABOUT THIS PROSPECTUS

Unless otherwise indicated, in this prospectus, the following terms shall have the meaning set out below:

|

“BVI”

|

|

British Virgin Islands.

|

|

“China” or the “PRC”

|

|

The People’s Republic of China, including Taiwan, Hong Kong and Macau, and the term “Chinese” has a correlative meaning for the purposes of this prospectus only, unless the context otherwise indicates. The references to laws and regulations of “China” or the “PRC” are only to such laws and regulations of mainland China, excluding, for the purpose of this prospectus only, Taiwan, Hong Kong and Macau.

|

|

“Code”

|

|

The Internal Revenue Code of 1986, as amended.

|

|

“Class A ordinary shares”

|

|

Class A ordinary shares, par value $0.0001 per share, of Zhibao Technology Inc.

|

|

“Class B ordinary shares”

|

|

Class B ordinary shares, par value $0.0001 per share, of Zhibao Technology Inc.

|

|

“Common Warrants”

|

|

Refers to the Class A ordinary shares warrants issued by the Company to the Investor on September 23, 2024.

|

|

“Exchange Act”

|

|

Securities Exchange Act of 1934, as amended.

|

|

“Hong Kong”

|

|

The Hong Kong Special Administrative Region of the People’s Republic of China.

|

|

“Investor” or “Selling Shareholder”

|

|

Refer to L1 Capital Global Opportunities Master Fund.

|

|

“Macau”

|

|

The Macao Special Administrative Region of the People’s Republic of China.

|

|

“mainland China”

|

|

The People’s Republic of Mainland China, excluding Taiwan, Hong Kong and Macau for the purpose of this prospectus.

|

|

“Nasdaq”

|

|

Nasdaq Capital Market.

|

|

“Note”

|

|

Refers to the senior secured 10% original issue discount convertible note in the principal amount of up to $2,500,000 issued by the Company to the Investor on September 23, 2024.

|

|

“ODI Filings”

|

|

The formalities and filings of overseas direct investment of PRC enterprises, including but not limited to fulfilling the filing, approval or registration procedures in the development and reform authorities, the competent commercial authorities, and foreign exchange administration authorities and competent banks authorized by such authorities.

|

|

“ordinary shares”

|

|

Ordinary shares, par value $0.0001 per share, of Zhibao Technology Inc., including Class A ordinary shares and Class B ordinary shares.

|

|

“PCAOB”

|

|

Public Company Accounting Oversight Board.

|

|

“PRC Subsidiaries” or “Zhibao China Group”

|

|

All references to “PRC Subsidiaries” or “Zhibao China Group” are to Zhibao China, Shanghai Anyi, Sunshine Insurance Brokers, and Zhibao Health.

|

|

“Pre-Funded Warrants”

|

|

Refers to the pre-funded class A ordinary shares purchase warrants issued by the Company to the Investor on September 23, 2024.

|

|

“RMB”, “Chinese Yuan” or “Renminbi”

|

|

Legal currency of mainland China.

|

|

“SEC”

|

|

The United States Securities and Exchange Commission.

|

ii

Table of Contents

|

“Securities Act”

|

|

The Securities Act of 1933, as amended.

|

|

“Shanghai Anyi”

|

|

Shanghai Anyi Network Technology Co., Ltd., a limited liability company organized under the laws of China and a wholly-owned subsidiary of WFOE.

|

|

“Securities Purchase Agreement”

|

|

Refers to the securities purchase agreement, dated as of September 23, 2024, entered into by and between the Company and the Investor

|

|

“Sunshine Insurance Brokers”

|

|

Sunshine Insurance Brokers (Shanghai) Co., Ltd., a limited liability company organized under the laws of China and a wholly-owned subsidiary of WFOE.

|

|

“US”, “U.S.” or “USA”

|

|

The United States of America.

|

|

“US$,” “U.S. dollars,” “$,” or “dollars”

|

|

Legal currency of the United States.

|

|

“WFOE” or “Zhibao China”

|

|

Zhibao Technology Co., Ltd., previously known as Shanghai Julai Investment Management Co., Ltd. and Zhibao Technology (Shanghai) Co., Ltd., successively, a limited liability company organized under the laws of China, which is wholly-owned by Zhibao HK.

|

|

“Zhibao,” “our company,” “Company,” “we,” “us,” “our,” or “ourselves”

|

|

All references to “Zhibao,” “our company,” “Company,” “we,” “us,” “our,” “ourselves” or similar terms used in this prospectus are to Zhibao Technology Inc., an exempted company incorporated with limited liability under the laws of Cayman Islands, unless the context otherwise indicates.

|

|

“Zhibao BVI”

|

|

Zhibao Technology Holdings Limited, a limited company incorporated under the laws of British Virgin Islands and a wholly owned subsidiary of Zhibao.

|

|

“Zhibao HK”

|

|

Zhibao Technology Limited, a limited company organized under the laws of Hong Kong and a wholly owned subsidiary of Zhibao BVI.

|

|

“Zhibao Health”

|

|

Shanghai Zhibao Health Management Co., Ltd., a limited liability company organized under the laws of China and a wholly-owned subsidiary of WFOE.

|

|

“Zhibao Labuan Reinsurance”

|

|

Zhibao Labuan Reinsurance Company Limited, a limited company organized under the laws of Malaysia and a wholly-owned subsidiary of Zhibao BVI.

|

Our reporting currency is the US$. The functional currency of our PRC Subsidiaries is RMB. This prospectus contains conversion of certain RMB amounts into U.S. dollar amounts at specified rates solely for the convenience of the reader. The conversion of RMB into U.S. dollars in this prospectus is based on the exchange rate set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System. Unless otherwise noted, all translations from RMB to U.S. dollars and from U.S. dollars to RMB in this prospectus are made at the rate of RMB 7.2672 to US$1.00, the rate in effect as of June 30, 2024. Notwithstanding the foregoing, we make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange.

Numerical figures included in this prospectus may be subject to rounding adjustments. Accordingly, numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures that precede them.

For the sake of clarity, this prospectus follows the English naming convention of first name followed by last name, regardless of whether an individual’s name is Chinese or English. For example, the name of our Chairman is presented as “Botao Ma”, even though, in Chinese, Mr. Ma’s name is presented as “Ma Botao”.

iii

Table of Contents

Our fiscal year end is June 30. References to a particular “fiscal year” are to our fiscal year ended June 30 of that calendar year. References to a particular “year” are also to our fiscal year ended June 30 of that calendar year unless the text indicates otherwise. Our audited consolidated financial statements have been prepared in accordance with the generally accepted accounting principles in the United States (the “U.S. GAAP”).

Except where indicated or where the context otherwise requires, all information in this prospectus assumes no exercise by the underwriters of their over-allotment option.

We obtained the industry, market and competitive position data in this prospectus from our own internal estimates, surveys, and research as well as from publicly available information, industry and general publications and research, surveys and studies conducted by third parties, including, but not limited to, an industry report (“Frost & Sullivan Report”) issued in June 2021 and updated in February 2023 that was commissioned by us and prepared by Frost & Sullivan, a third-party industry research firm, to provide information regarding our industry and market position in China. The information disclosed in the Frost & Sullivan Report reflects estimates of market conditions based on publicly available sources and trade opinion surveys, and is prepared primarily as a market research tool. Industry publications, research, surveys, studies and forecasts generally state that the information they contain has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this prospectus, and to risks due to a variety of factors, including those described under “Risk Factors.” These and other factors could cause results to differ materially from those expressed in these forecasts and other forward-looking information.

Our PRC Subsidiaries have proprietary rights to trademarks used in this prospectus that are important to their business, many of which are registered under applicable intellectual property laws. Solely for convenience, some of the trademarks, service marks and trade names referred to in this prospectus are without the ®, ™ and other similar symbols, but such references are not intended to indicate, in any way, that our PRC Subsidiaries will not assert, to the fullest extent under applicable law, their rights to these trademarks, service marks and trade names.

This prospectus contains additional trademarks, service marks and trade names of others. All trademarks, service marks and trade names appearing in this prospectus are, to our knowledge, the property of their respective owners. We do not intend our use or display of other companies’ trademarks, service marks or trade names to imply a relationship with, or endorsement or sponsorship of us by, any other person.

iv

Table of Contents

PROSPECTUS SUMMARY

This summary highlights certain information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before buying shares in this offering. You should read the entire prospectus carefully, including our financial statements and related notes and the risks described under “Risk Factors.” This summary contains forward-looking statements that involve risks and uncertainties, such as statements about our plans, objectives, expectations, assumptions or future events. These statements involve estimates, assumptions, known and unknown risks, uncertainties and other factors that could cause actual results to differ materially from any future results, performances or achievements expressed or implied by the forward-looking statements. See “Cautionary Note Regarding Forward-Looking Statements.”

Overview

Zhibao Technology Inc. is a holding company incorporated as an exempted company on January 11, 2023 under the laws of the Cayman Islands. It operates substantially all of its business through its PRC Subsidiaries, or Zhibao China Group, in particular Zhibao China and Sunshine Insurance Brokers.

We are a leading and high growth InsurTech company primarily engaging in providing digital insurance brokerage services through Zhibao China Group in China. 2B2C (“to-business-to-customer”) digital embedded insurance is our innovative business model, which Zhibao China Group pioneered in China. Zhibao China Group launched the first digital insurance brokerage platform in China in 2020, which is powered by their proprietary PaaS (“Platform as a Service”). According to the Frost & Sullivan Report, the total market size of the 2B2C digital insurance brokerage services sector in China, contributed by over 20 market players in the PRC market, was approximately RMB807.4 million in 2022, among which Zhibao China Group ranked number one, with a market share of approximately 17.4% and a revenue of approximately RMB140.6 million. According to the Frost & Sullivan Report, the 2B2C digital insurance brokerage services sector is the fastest growing segment within the digital insurance brokerage service industry, with a historical compound annual growth rate (“CAGR”) of approximately 54.6% from 2018 to 2022, which also presents a substantial growth potential to reach approximately RMB6.2 billion in 2027, with an estimated CAGR of approximately 50.1% from 2022 to 2027. We believe that 2B2C digital embedded insurance is shaping the future of the industry.

2B2C digital embedded insurance refers to our one-stop customized insurance brokerage model conducted through Zhibao China Group, under which we provide proprietary and customized insurance solutions to be digitally embedded in the existing customer engagement matrix of business entities (our “business channels” or “B channels”) to reach and serve such B channels’ existing pool of end customers (“end customers” or “C”). Each B channel encompasses a specific scenario where its end customers also have potential, untapped insurance needs. For example, a Chinese travel agency (our B channel) has an average of 100,000 Chinese tourists traveling to the U.S. for tourism every year. We believe this presents an untapped scenario-specific opportunity for international travel accident insurance needs for a pool of 100,000 Chinese tourists as end customers. These end customers might otherwise have to search for and purchase insurance separately or might not purchase insurance at all. After Zhibao China Group reaching an agreement with such travel agency to become one of our B channels, they build and embed a travel insurance solution across this travel agency’s matrix of digital channels, including its website, App, Douyin (the Chinese equivalent of TikTok), WeChat Mini Program, and other social media accounts. Consequently, we, through Zhibao China Group, may pinpoint the 100,000-strong customer base and provide insurance brokerage services which are specifically and accurately tailored to the insurance needs of these end customers.

Our service portfolio through Zhibao China Group includes (1) insurance brokerage services, and (2) managing general underwriting (“MGU”) services, a specialized insurance brokerage service whereby the insurance companies authorize us to assist them in underwriting, claims and risk control services. It broadly covers insurance product design and customization, selection of insurance companies, technology system interconnection and delivery, customer AARRR (Acquisition, Activation, Retention, Referral, Revenue) operation, customer service, compliance management, data analysis, all of which are integrated in each of our insurance solutions. Each insurance solution generally applies to one specific scenario in a particular sector, with customized product design and services relevant for that scenario and sector. As of the date of this prospectus, we, through Zhibao China Group, have developed more than 40 proprietary and innovative digital insurance solutions addressing different scenarios in a wide range of industries, including but not limited to travel, sports, logistics, utilities (i.e., gas and electricity), and e-commerce. Zhibao China Group acquire and analyze customer data, utilize big data and artificial intelligence (“AI”) technology

1

Table of Contents

to continually iterate and enhance our digital insurance solutions. This iterative process, in addition to continually improving our digital insurance solutions, will keep us abreast of the new trends and customer preferences in the market.

Zhibao China Group secure and serve our end customers through our B channels. Our B channels cover a wide range of industries and organizations, including but not limited to internet platforms, large and medium-sized enterprises, and government agencies. While B channels have end customers with potential insurance needs relevant and specific to their primary operations, they usually do not have the experience and expertise to effectively provide insurance related services. In order to address this pain-point, we, through Zhibao China Group, provide them with our customized digital insurance solutions specifically tailored to their business. Our 2B2C model thrives because our relationship with B channels is mutually beneficial and sustainable for all participants. Our B channels view us as a valuable partner as we empower them to provide insurance as a value-added service to their end customers, a potential competitive advantage for them. By embedding our digital insurance solutions into our B channels’ online matrix to reach their customer base, we maintain a captive, stable and sustainable source of end customers at low cost. The end customers, as a result, can conveniently and efficiently access quality brokerage services and suitable insurance products tailored to their actual needs. As of the date of this prospectus, we, through Zhibao China Group, have cooperated with more than 1,800 B channels, and secured more than 15 million end customers through them. We will expand the number of B channels as a key growth strategy of our business.

Under our business model, Zhibao China Group represent end customers as their authorized insurance broker to negotiate with insurance companies and select the most suitable insurance products for our end customers. As of the date of this prospectus, we have partnered with over 100 insurance companies (including their subsidiaries and branches) through Zhibao China Group.

While embedded insurance brokerage is still at an early stage of development in China, we believe it is the future of insurance brokerage industry.

Our revenue reached approximately RMB 183.7 million (US$25.3 million) for the fiscal year ended June 30, 2024, representing an increase of approximately RMB 41.6 million (US$5.7 million), or 29%, from approximately RMB 142.1 million (US$19.6 million) for the fiscal year ended June 30, 2023. For the fiscal year ended June 30, 2024, we generated net income of approximately RMB 13.3 million (US$1.8 million). For the fiscal year ended June 30, 2023, we incurred net loss of approximately RMB 43.1 million (US$5.9 million), among which RMB 54.7 million ($7.5 million) related to share-based compensation expenses arising from issuance of ordinary shares to a related party. Excluding such one-off expenses, we would have achieved net income of approximately RMB 11.6 million ($1.6 million).

Our Revenue Model

Our revenue consists of (i) brokerage Zhibao China Group receive for their general digital insurance brokerage services (“Insurance Brokerage”), and (ii) MGU service fees (“MGU Service Fees”) Zhibao China Group receive for their MGU services.

Insurance Brokerage refer to the commissions or fees Zhibao China Group receive from insurance companies for the digital insurance brokerage services they offer to our end customers (who pay insurance premium to insurance companies according to the terms of their policies), primarily at the range of 10% – 35% for property & casualty insurance products, 10% – 35% for health insurance products and 50% – 80% for life insurance products, of gross written premium per insurance policy depending on the type of the insurance, the specific insurance products, and their negotiated terms with each insurance company. Insurance Brokerage accounted for approximately 84% and 94%, respectively, of our total revenues for the fiscal years ended June 30, 2023 and 2024.

MGU Service Fees refer to service fees Zhibao China Group receive from insurance companies for the MGU services they provide to such insurance companies, usually at an average of approximately 15% of gross written premium per insurance policy depending on the type of insurance, and their negotiated terms with each insurance company. MGU Service Fees accounted for approximately 16% and 6%, respectively, of our total revenues for the fiscal years ended June 30, 2023 and 2024.

2

Table of Contents

Strengths

We believe that the following strengths contribute to Zhibao China Group’s growth and differentiate us from our competitors:

• Innovative Business Model — 2B2C Embedded Insurance

We are a pioneer and market leader through Zhibao China Group in 2B2C embedded insurance business in China. Our 2B2C model is key to enable us to acquire end customers at minimal cost and therefore to achieve higher efficiency compared with our industry peers, who might gain customers by investing a large amount of capital through direct-to-consumer advertisement and other marketing channels. Each of our B channels has already developed a stable relationship with their end customers. By embedding our customized digital insurance solutions into B channels’ online matrix, we can reach end customers more precisely and efficiently. As the first-mover and a market leader in 2B2C embedded insurance brokerage service in China, we have entrenched relationships with B channels and other industry participants through Zhibao China Group. As of the date of this prospectus, we have cumulatively cooperated with over 1,800 B channels and will continue to expand the number of B channels as a key growth strategy.

• Market Leading Digital Insurance Solutions

As of the date of this prospectus, we, through Zhibao China Group, have developed over 40 proprietary and innovative digital insurance solutions which are built and operated based on their PaaS. Each of our proprietary digital insurance solutions primarily consists of insurance product(s), a solution-specific technology system, customer AARRR operations plan, and customer service plan. They are specifically tailored to the various scenarios of our B channels and their end customers’ insurance needs. Our digital insurance solutions can largely reduce point-of-sale friction and deliver the digital insurance brokerage services which are relevant and tailored to the separate needs of our B channels and end customers. Through our digital insurance solutions on Zhibao China Group’s PaaS, Zhibao China Group acquire and analyze customer data, and utilize big data and AI technology to continually iterate and enhance our digital solutions. This iterative process, in addition to continually improving our digital solutions, will keep us abreast of the new trends and customer preferences in the market.

• Advanced Technology Platform

Zhibao China Group launched the first digital insurance brokerage platform in China in 2020. This platform includes (i) 2B2C insurance PaaS, (ii) digital insurance solutions, and (iii) delivery system. Through their platform, they can provide SaaS (“Software as a service”) to our various B channels and insurance brokerage services to our end customers effectively and efficiently.

(i) Zhibao China Group’s PaaS is a cloud-based development platform which offers a collection of 2B2C insurance tools for building the systems required for various insurance solutions efficiently. Their PaaS was developed out of their professional knowledge and experience gained from real-world deployment of systems in the past eight years. The tools of their PaaS are analogous to providing “pre-washed” and “pre-cut” raw materials, allowing them to quickly and reliably output “cooked dishes”. Without such a PaaS, building the necessary solution-specific systems would be a complicated and slow process with no guarantee of a positive user experience. Their PaaS is not only for our internal solution-specific systems but can be extended to our independent sales partners. It allows such partners to share our tools and workflows, and incubate new solutions without having to start from scratch each time. Furthermore, the unified design foundation of their PaaS allows them to develop brand new solutions as well as to piggyback additional solutions on top of those already deployed with reusable system components, data consistency and customer convenience.

(ii) Our various insurance solutions are built and run based on the PaaS. These solutions are delivered to B channels by embedding within the B channels’ platforms, including but not limited to WeChat Official Accounts, websites, and insurance modules within Apps. Our end customers may purchase insurance products and have access to insurance services through our embedded insurance solutions on our B channels’ website, App, H5 page, or QR codes.

3

Table of Contents

(iii) The delivery system, developed according to the best practices of digital insurance brokerage services, breaks down our various solutions into workflows, work nodes, automatic resource assignments, and deliverable standards. On the delivery system, business opportunities are segregated into different industries which are automatically mapped to our various solutions. It also allows Zhibao China Group to collect and consider the specific needs from each B channel. The delivery system then runs the pre-set workflow, standardizing the processes and providing higher-quality and higher-efficiency deliverables. According to the specific needs of our B channels, the delivery system is capable of making changes to the standard workflow to meet these customizations. The delivery system helps us greatly improve our delivery efficiency, quality and channel satisfaction.

• Experienced Management Team with Extensive Expertise in Insurance Industry and Digital Technology

We have an experienced and devoted management team that has helmed the acceleration of our growth and steered our strategic direction. Our management team is passionate about innovation in providing digital insurance solutions to end customers. Our founder and Chief Executive Officer, Mr. Botao Ma has accumulated more than 30 years of management experience in the insurance industry. Our Chief Financial Officer, Mr. Yuanwen Xia, has more than 15 years of experience in PwC and investment sector. Our Chief Operating Officer, Mr. Xiao Luo has more than 15 years of experience in insurance brokerage business. Our Chief Technology Officer, Mr. Yugang Wang, has more than 20 years of digital technology and management experience in the insurance industry. Our management team has extensive experience in China’s insurance market; in particular, our team’s expertise in the insurance brokerage industry will help steer the Company to continuously maintain and extend our leading position in the digitalization of the insurance brokerage industry in China. Their influences across the market have already, and will continue to, attract more B channels and deepen relationships with existing B channels and insurance companies, all of which will sustain and accelerate the rapid-paced growth of the Company.

Growth Strategies

We intend to grow our business by pursuing the following key strategies through Zhibao China Group:

• Accelerate the Expansion of B Channels

We plan to scale up our business by rapidly expanding the number of B channels. We intend to penetrate new markets, increase market share in existing markets and access a broader range of B channels in China. With the continuing development of our 2B2C business, we, through Zhibao China Group, have developed insurance companies as a special type of B channel, providing digital brokerage services and supports for their existing individual policyholders. We plan to cooperate with more insurance companies as a key focus for expansion.

• Expand Our Sales Force

We plan to increase the number of sales teams both in the head office and branch offices. We also plan to develop more independent sales partners who are not directly employed by us or Zhibao China Group but provide leads for new B channels, for example smaller-scale niche players in the 2B2C business sector. We have an established workflow to efficiently establish relations with sales partners powered by Zhibao China Group’s delivery system, which provides contracting, training, online customer AARRR operations, and an online portal for requesting sales support. The growth of our nationwide network of sales partners is integral to our rapid expansion and growth of the market.

• Drive Additional Conversions for Existing End Customers — Our 2C Business

Through our B channels, we are accumulating an ever-larger pool of potential end customers. Although the initial customer interaction is related to the specific scenario and sector of the B channel, end customer may have additional needs that have not yet been addressed. For example, a medical insurance end customer might have additional demand for travel, household, or life insurance. We intend to strengthen our to-customer, or 2C business through Zhibao China Group by targeting our existing customer base to meet the additional needs of each end customer. Our 2C business is an increasingly important part of our business growth in the coming years.

4

Table of Contents

• Upgrade and Enrich Our Digital Insurance Solutions

Currently we have over 40 proprietary digital insurance solutions on Zhibao China Group’s platform, which covers various scenarios in a variety of industries. We will keep refining and upgrading our insurance solutions to keep abreast of new trends and customer preferences. In addition to optimizing our existing insurance solutions, we are developing new insurance solutions to meet emerging demands. We intend to develop solutions across every sector of the economy, thus ultimately covering every aspect of the end customers’ daily life to deliver all-around insurance coverage.

• Upgrade and Enhance Our PaaS

Zhibao China Group are the first to establish a PaaS in the digital insurance brokerage market in China. We intend to invest in the research and development (“R&D”) of new technologies to upgrade and enhance the PaaS to maintain our leadership position in China. In particular, we plan to enrich the technology infrastructure tools and functionalities of the business components of the PaaS, and introduce new AI and business intelligence (BI) functionalities, continually strengthening our data security and governance.

• Expand the Scale of the MGU business.

Zhibao China Group pioneered the MGU business model in China. Under this model, in addition to providing general digital insurance brokerage services to our end customers, Zhibao China Group also assist insurance companies in product design, underwriting, reinsurance, claims and risk control services. We intend to increase the number of MGU partners (insurance companies) from 7 to 15 by the end of 2024, and expand the insurance products from the current high-end medical insurance and long-term disability lines to mid-end medical and personal accident lines in the future.

• Support our brokerage and MGU services through our subsidiary reinsurance company in Labuan, Malaysia.

In July 2024, we incorporated Zhibao Labuan Reinsurance, our wholly-owned subsidiary reinsurance company in Labuan, Malaysia, and in October 2024, we received a license approval. Through this subsidiary, we intend to support our brokerage and MGU services.

• M&A Opportunities

There is a fragmented constellation of smaller-scale firms engaged in online insurance agency or brokerage business in China. They are commonly lacking in industry recognition, technological capacity, team expertise, capital, and market resources, therefore they face significant headwinds in scaling up their business and attaining profitability. However, some of them have built strong ties with B channels in niche industries, providing us with potential targets for M&A. We plan to invest in potential M&A targets in the future, especially those who can bring new B channel resources.

Market Opportunity

Along with the development of the PRC insurance industry and the progress of digital industrial transformation in the PRC in recent years, insurance brokerage service institutions are recognized by more policyholders and insurance companies. According to the Frost & Sullivan Report, the total market size of the Chinese insurance industry in terms of insurance premium grew steadily and is expected to reach approximately RMB 5.8 trillion by 2027, at a CAGR of 4.3% from 2022 to 2027. Within the insurance industry, the insurance brokerage services industry in terms of revenue grew substantially at a CAGR of 21.1% from 2018 to 2022 and is estimated to grow at a CAGR of 13.9% from 2022 to 2027. Furthermore, the market size of the digital insurance brokerage services industry in terms of revenue is estimated to substantially grow at a CAGR of 28.2% from 2022 to 2027. It is noteworthy that, within the market, the digital scenario-embedded insurance brokerage (also known as 2B2C) services industry is the fastest growing segment, with a historical CAGR of 54.6% from 2018 to 2022. It also presents a substantial growth potential, with an estimated CAGR of 50.1% from 2022 to 2027.

5

Table of Contents

The convergence of digital technology and changing consumer preferences in the insurance industry give digital insurance brokerage service providers, like us, a competitive advantage as digital technology assists us in connecting end customers through more channels, thus enhancing our operation efficiency. We believe, in the future, the digital insurance brokerage service will take more market share.

In recent years, consumer behaviors have undergone profound changes. Research shows that insurance customers in the internet era pay more attention to product transparency and service experience while demonstrating a strong preference for personalization, customization, and scenario orientation. In addition, millennials (who were generally born between the early 1980s and the mid-to-late 1990s) are gradually becoming the leading consumption group of insurance, which are expected to surpass generation X (who is generally born between the mid-1960s and the late 1970s) to become the main consumption group within the next decade. The millennials can obtain information through the internet more conveniently and efficiently, and are more receptive to digital insurance and pay more attention to product diversity and personalization, which provide great potential for the development of digital embedded insurance brokerage services.

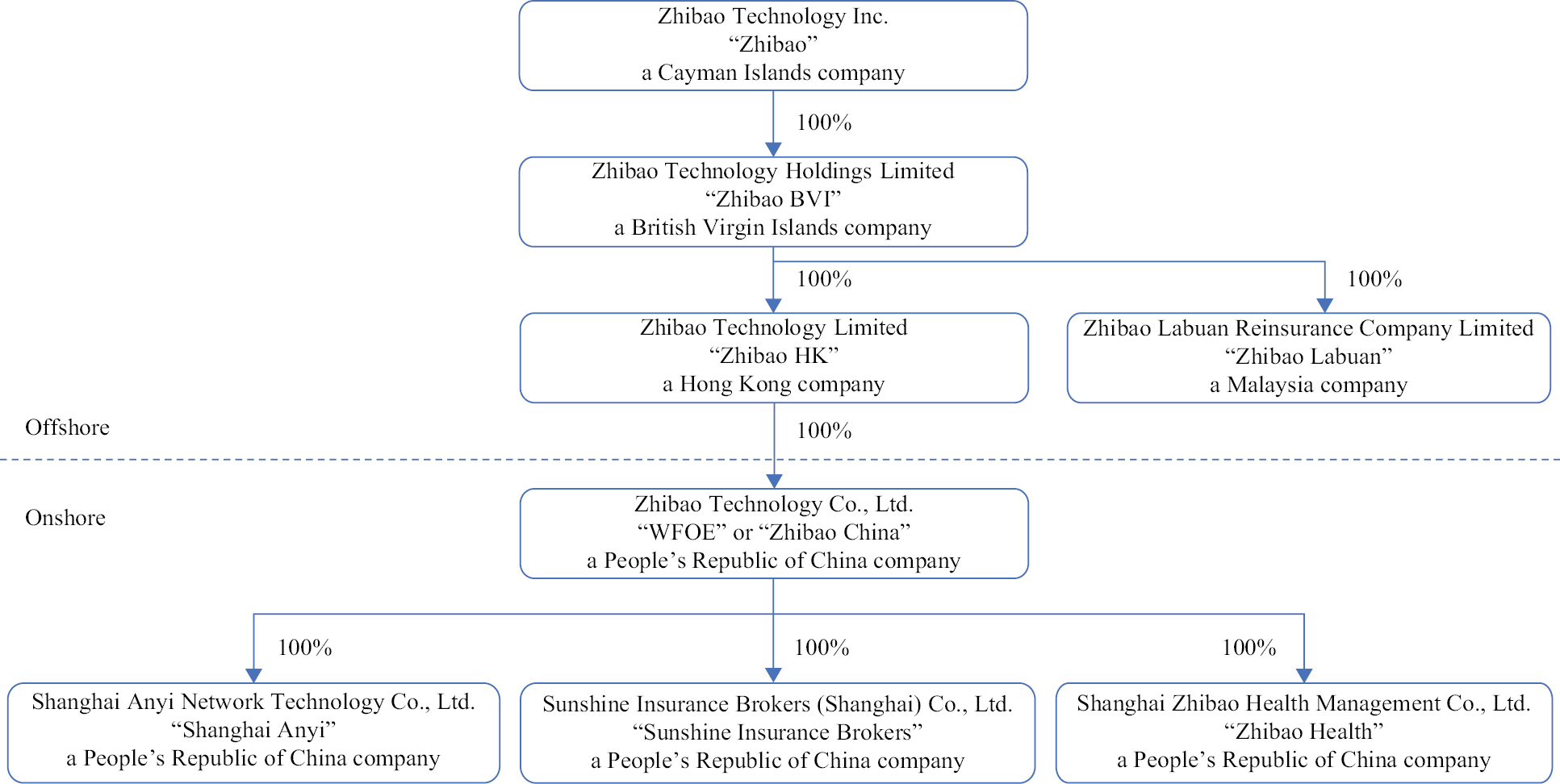

Our Corporate History and Structure

Zhibao is a Cayman Islands exempted company incorporated on January 11, 2023. Structured as a holding company with no material operations, Zhibao conducts its operations in China through its PRC Subsidiaries, primarily Zhibao China and Sunshine Insurance Brokers.

Zhibao China, previously known as Shanghai Julai Investment Management Co., Ltd. and Zhibao Technology (Shanghai) Co., Ltd., successively, started its business in the insurance brokerage industry since 2016 in China. With the growth of our business and in order to facilitate international capital investment in us, we started a reorganization as described below involving new offshore and onshore entities in December 2022 and completed it in March 2023.

Zhibao BVI, incorporated on January 12, 2023 under the laws of British Virgin Islands, is our wholly-owned subsidiary in BVI and a holding company with no business operations, which, in turn, wholly owns all of the equity interest of Zhibao HK, a limited company incorporated on January 19, 2023 under the laws of Hong Kong.

Zhibao HK, as a wholly-owned subsidiary of Zhibao BVI, is a holding company with no business operations, which, in turn, wholly owns all of the equity interest of Zhibao China or WFOE, a wholly foreign-owned enterprise formed on November 24, 2015 in Shanghai under the laws of China, currently with a registered capital of RMB 85,000,000. Zhibao China wholly owns Shanghai Anyi, Sunshine Insurance Brokers and Zhibao Health, primarily providing MGU services.

Shanghai Anyi was incorporated in Shanghai under the laws of China on September 18, 2015, currently with a registered capital of RMB10 million. Shanghai Anyi was originally 100% controlled by Shanghai Xinhui Investment Consulting Co., Ltd. (“Shanghai Xinhui”), a related party controlled by our Chief Executive Officer, Mr. Botao Ma. All of the equity interest of Shanghai Anyi was later transferred to Zhibao China on July 12, 2016, with a consideration of RMB 10 million. After such transfer, Shanghai Anyi became a wholly-owned subsidiary of Zhibao China, primarily providing R&D services to Sunshine Insurance Brokers and Zhibao China.

Sunshine Insurance Brokers was incorporated in Shanghai under the laws of China on November 17, 2011, currently with a registered capital of RMB 50 million. Sunshine Insurance Brokers was originally 100% controlled by an unrelated third party, all of the equity interest of which was thereafter transferred to Zhibao China on January 4, 2016, with a consideration of RMB 10 million. After such transfer, Sunshine Insurance Brokers became a wholly-owned subsidiary of Zhibao China, primarily providing insurance brokerage services.

Zhibao Health, previously known as Shanghai Zhongzhi Chengcheng Healthy Service Co., Ltd., was incorporated in Shanghai under the laws of China on November 16, 2022, currently with a registered capital of RMB 1 million. Zhibao Health is a wholly-owned subsidiary of Zhibao China, primarily engaged in the health management services.

Zhibao Labuan Reinsurance was incorporated in Labuan, Malaysia, on July 29, 2024, and received a license approval on October 24, 2024. Zhibao Labuan Reinsurance is a wholly-owned subsidiary of Zhibao BVI, primarily engaged in brokerage and MGU services. As of the date of this prospectus, it has not commenced operation yet.

6

Table of Contents

The chart below shows our corporate structure as of the date of this prospectus:

For more details regarding our corporate structure, see “Corporate History and Structure” on page 73.

Recent Regulatory Developments in China

In recent years, the PRC government initiated a series of regulatory actions and made a number of public statements on the regulation of business operations in China, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas, adopting new measures to extend the scope of cybersecurity reviews, and expanding efforts in anti-monopoly enforcement.

Among other things, the Regulations on Mergers and Acquisitions of Domestic Enterprises by Foreign Investors (the “M&A Rules”) and the Anti-Monopoly Law of the People’s Republic of China promulgated by the SCNPC which became effective in 2008, amended in 2022 (“Anti-Monopoly Law”), established additional procedures and requirements that could make merger and acquisition activities by foreign investors more time-consuming and complex. Such regulation requires, among other things, that the Ministry of Commerce of the People’s Republic of China (the “MOFCOM”) be notified in advance of any change-of-control transaction in which a foreign investor acquires control of a PRC domestic enterprise or a foreign company with substantial PRC operations, if certain thresholds under the Provisions of the State Council on the Standard for Declaration of Concentration of Business Operators, issued by the State Council in 2008, revised in 2018 and 2024, are triggered. Moreover, the Anti-Monopoly Law requires that transactions which involve the national security, the examination on the national security shall also be conducted according to the relevant provisions of the Measures for the Safety Examination of Foreign Investment. In addition, the PRC Measures for the Security Review of Foreign Investment which became effective in January 2021 require acquisitions by foreign investors of PRC companies engaged in military-related or certain other industries that are crucial to national security be subject to security review before consummation of any such acquisition.

On July 6, 2021, the relevant PRC government authorities made public the Opinions on Strictly Cracking Down on Illegal Securities Activities in Accordance with the Law (the “Opinions”). These opinions emphasized the need to strengthen the administration over illegal securities activities and the supervision on overseas listings by China-based companies and proposed to take effective measures, such as promoting the construction of relevant regulatory systems to deal with the risks and incidents faced by China-based overseas-listed companies. Pursuant to the Opinions, Chinese regulators are required to accelerate rulemaking related to the overseas issuance and listing of securities, and update the existing laws and regulations related to data security, cross-border data flow, and management of confidential information. Numerous regulations, guidelines and other measures are expected to be adopted under the umbrella of or in addition to the Cybersecurity Law of the PRC (the “Cybersecurity Law”) and the Data Security Law. As of the date of this prospectus, no official guidance or related implementation rules have been issued yet and the

7

Table of Contents

interpretation of these opinions remains unclear at this stage. See “Risk Factors — Risks Related to Doing Business in China — Uncertainties in the interpretation and enforcement of PRC laws and regulations could limit the legal protections available to you and us” on page 24 and “Risk Factors — Risks Related to Doing Business in China — Our business processes a certain quantity of personal information, and failure to protect private or sensitive information of customers or improper handling of such information could have a material and adverse effect on our business. In light of recent events indicating greater oversight by the Cyberspace Administration of China, or CAC, over data security, we are subject to a variety of laws and other obligations regarding cybersecurity and data protection, and any failure to comply with applicable laws and obligations could have a material and adverse effect on our business, financial condition, results of operations, and the offering” on page 27.

On December 28, 2021, the Cybersecurity Review Measures (2021 version), which were promulgated and became effective on February 15, 2022, provide that any “online platform operators” possessing personal information of more than one million users which seeks to list in a foreign stock exchange should be subject to cybersecurity review. The Cybersecurity Review Measures (2021 version), further list the factors to be considered when assessing the national security risks of the relevant activities, including, among others, (i) the risk of core data, important data or a large amount of personal information being stolen, leaked, destroyed, and illegally used or exited the country; and (ii) the risk of critical information infrastructure, core data, important data or a large amount of personal information being affected, controlled, or maliciously used by foreign governments after listing abroad. The CAC requires that under the new rules, companies possessing personal information of more than 1,000,000 users must now apply for cybersecurity approval when seeking listings in other nations because of the risk that such data and personal information could be “affected, controlled, and maliciously exploited by foreign governments.” The cybersecurity review will also look into the potential national security risks from overseas IPOs. As a network platform operator who possesses personal information of more than one million users for purposes of the Cybersecurity Review Measures (2021 version), we have applied for and completed a cybersecurity review with respect to the IPO and we are not required to do the cybersecurity review for this offering pursuant to the Cybersecurity Review Measures (2021 version). See “Risk Factors — Risks Related to Doing Business in China — Uncertainties in the interpretation and enforcement of PRC laws and regulations could limit the legal protections available to you and us” on page 24 and “Risk Factors — Risks Related to Doing Business in China — Our business processes a certain quantity of personal information, and failure to protect private or sensitive information of customers or improper handling of such information could have a material and adverse effect on our business. In light of recent events indicating greater oversight by the Cyberspace Administration of China, or CAC, over data security, we are subject to a variety of laws and other obligations regarding cybersecurity and data protection, and any failure to comply with applicable laws and obligations could have a material and adverse effect on our business, financial condition, results of operations, and the offering” on page 27.

On February 17, 2023, the CSRC released the New Overseas Listing Rules, which came into effect on March 31, 2023. The New Overseas Listing Rules apply to overseas securities offerings and/or listings conducted by (i) companies incorporated in the PRC, or PRC domestic companies, directly and (ii) companies incorporated overseas with operations primarily in the PRC and valued on the basis of interests in PRC domestic companies, or indirect offerings. The New Overseas Listing Rules requires (1) the filings of the overseas offering and listing plan by the PRC domestic companies with the CSRC under certain conditions, and (2) the filing of their underwriters with the CSRC under certain conditions and the submission of an annual report to of such filed underwriters the CSRC within the required timeline. The required filing scope is not limited to the initial public offering, but also includes subsequent overseas securities offerings, single or multiple acquisition(s), share swap, transfer of shares or other means to seek an overseas direct or indirect listing, a secondary listing or dual listing.

Under the New Overseas Listing Rules, a filing-based regulatory system applies to “indirect overseas offerings and listings” of companies in mainland China, which refers to securities offerings and listings in an overseas market made under the name of an offshore entity but based on the underlying equity, assets, earnings or other similar rights of a company in mainland China that operates its main business in mainland China. The New Overseas Listing Rules state that, any post-listing follow-on offering by an issuer in an overseas market, including issuance of shares, convertible notes, exchangeable notes and preferred shares, shall be subject to filing requirement within three business days after the completion of the offering.

8

Table of Contents