SECURITIES AND EXCHANGE

COMMISSION

Washington, D.C. 20549

FORM 6-K

Report

of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 of the Securities Exchange Act of 1934

For the month of November,

2024

Commission File Number 001-41129

Nu Holdings Ltd.

(Exact name of registrant as specified

in its charter)

Nu Holdings Ltd.

(Translation of Registrant's

name into English)

Campbells Corporate Services

Limited, Floor 4, Willow House, Cricket Square, KY1-9010 Grand Cayman, Cayman Islands

+1 345 949 2648

(Address of principal executive

office)

Indicate by check mark whether

the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F (X) Form 40-F

Indicate by check mark whether the registrant by furnishing

the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the

Securities Exchange Act of 1934.

Yes No (X)

São Paulo – November 13, 2024 – Nu Holdings

Ltd. (“Nu”, “Nu Holdings” or “the Company”) (NYSE: NU), one of the world’s largest

digital banking platforms, today reported its unaudited results for the third quarter ended on September 30, 2024 (Q3'24). Financial results

are expressed in U.S. dollars and are presented in accordance with International

Financial Reporting Standards (IFRS), unless otherwise noted.

|

Nu Holdings Reports Q3’24 Financial and Operating Results |

|

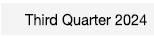

Added 5.2 million new customers during the quarter, marking a year-over-year (YoY) increase of 20.7 million and reaching a total of 109.7 million customers. This growth further strengthens Nu’s position as one of the largest and fastest-growing digital financial services platforms worldwide, and is one of the largest financial institution in Latin America by customer count1. In Brazil, Nu has already become the institution with the largest number of active customers in credit operations2. |

|

Net Income increased to $553.4 million, from $303.0 million in Q3'23, while Adjusted Net Income increased to $592.2 million, from $355.6 million in Q3'23. Revenues were up 56% YoY on an FXN basis, setting a new record at $2.9 billion. Monthly Average Revenue per Active Customer (ARPAC) increased 25% YoY FXN, to $11.0. |

|

Deposits expanded 60% YoY FXN to $28.3 billion, while funding cost increased to 89% of the blended interbank rates for the quarter, and a Loan-to-Deposit ratio (LDR) at 40%. Nu's total receivables from its credit card and lending portfolios increased 47% YoY and 8% QoQ FXN, respectively, totalling $20.9 billion, while its Interest-Earning Portfolio (IEP) expanded 81% FXN to $11.2 billion. |

|

Nu's asset quality leading indicator,

the 15-90 NPL ratio for the Brazil Consumer Credit Portfolio dropped 10 basis points (bp) sequentially to 4.4%3 this

quarter, while the 90+ NPL ratio increased to 7.2%3, in line with expectations.

|

|

Risk-adjusted NIM reached 10.1%,

reflecting an expansion of 110 bp from a year ago.

1: Source: Companies reports, BCB, Nu.

2: Source: BCB.

3: Data for Brazil only. |

A Summary of Consolidated Financial and Operating Metrics is

presented for the three-month periods ended September 30, 2024, 2023 and June 30, 2024. See definitions on page 16.

| Summary of Consolidated Operating Metrics |

Q3'24 |

Q3'23 |

Q2'24 |

| CUSTOMER METRICS |

|

|

|

| Number of Customers (in millions) |

109.7 |

89.1 |

104.5 |

| Number of Customers growth (%) |

23% |

27% |

25% |

| Active Customers (in millions) |

91.7 |

73.8 |

87.2 |

| Activity Rate |

84% |

83% |

83% |

| CUSTOMER ACTIVITY METRICS |

|

|

|

| Purchase Volume (in $ billions) |

30.9 |

29.0 |

31.3 |

| Purchase Volume growth (%) |

7% |

37% |

19% |

| Monthly Average Revenue per Active Customer (in $) |

11.0 |

10.0 |

11.2 |

| Monthly Average Cost to Serve per Active Customer (in $) |

0.7 |

0.9 |

0.9 |

| FX NEUTRAL |

|

|

|

| Purchase Volume (FX Neutral) (in $ billions) |

30.9 |

25.5 |

30.1 |

| Purchase Volume growth (%) |

21% |

28% |

29% |

| Monthly Average Revenue per Active Customer (in $) |

11.0 |

8.8 |

10.7 |

| Monthly Average Cost to Serve per Active Customer (in $) |

0.7 |

0.8 |

0.9 |

| CUSTOMER BALANCES |

|

|

|

| Total portfolio - credit card and lending (in $ billions) |

20.9 |

15.4 |

18.9 |

| Portfolio growth (%) |

36% |

59% |

28% |

| Deposits (in $ billions) |

28.3 |

19.1 |

25.2 |

| Deposits growth (%) |

48% |

36% |

40% |

| Interest-Earning Portfolio (in $ billions) |

11.2 |

6.7 |

9.8 |

| Interest-Earning growth (%) |

67% |

91% |

56% |

| FX NEUTRAL |

|

|

|

| Total portfolio - credit card and lending (in $ billions) |

20.9 |

14.2 |

19.4 |

| Portfolio growth (%) |

47% |

48% |

49% |

| Deposits (in $ billions) |

28.3 |

17.7 |

25.9 |

| Deposits growth (%) |

60% |

26% |

64% |

| Interest-Earning Portfolio (in $ billions) |

11.2 |

6.2 |

10.1 |

| Interest-Earning growth (%) |

81% |

77% |

84% |

Note 1: Adjusted CTS of $0.8 when adjusted for one-offs in the third quarter of

2024, mostly related to FX impacts on data and cloud costs that had been allocated under customer services and now were reallocated to

G&A.

| | | |

| |  | 3 |

| Summary of Consolidated Financial Metrics |

Q3'24 |

Q3'23 |

Q2'24 |

| COMPANY FINANCIAL METRICS |

|

|

|

| Revenue (in $ millions) |

2,943.2 |

2,136.8 |

2,848.7 |

| Revenue growth (%) |

38% |

64% |

52% |

| Gross Profit (in $ millions) |

1,348.6 |

914.8 |

1,359.4 |

| Gross Profit Margin (%) |

46% |

43% |

48% |

| Credit Loss Allowance Expenses / Credit Portfolio (%) |

3.7% |

4.1% |

4.0% |

| Net Income (in $ millions) |

553.4 |

303.0 |

487.3 |

| Adjusted Net Income (in $ millions) |

592.2 |

355.6 |

562.5 |

| FX NEUTRAL |

|

|

|

| Revenue (in $ millions) |

2,943.2 |

1,881.9 |

2,733.7 |

| Revenue growth (%) |

56% |

53% |

65% |

| Gross Profit (in $ millions) |

1,348.6 |

805.7 |

1,304.5 |

| Net Income (in $ million) |

553.4 |

266.9 |

467.6 |

| Adjusted Net Income (in $ millions) |

592.2 |

313.2 |

539.8 |

| | | |

| | | 4 |

Continued Growth of One of The World's Largest Digital Banking Platforms

Note 1: Adult population market share is calculated as the

Nu’s Brazilian adult customers divided by the adult population of the country. Adult Population of the country is estimated from

the 2023 Brazilian demographic census.

Note 2: Adult population is defined as 18+ years for Brazil.

Note 3: ‘Activity Rate’ is defined as monthly active

customers divided by the total number of customers as of a specific date.

Note 4: For additional detail on calculations of Adjusted Net

Income please refer to the appendix Non-IFRS Financial measures and reconciliations.

Note 5: Amounts are presented in US dollars and growth rates

on an FX Neutral basis. For additional details on calculations please refer to the appendix Non-IFRS Financial measures and reconciliations.

Note 6: ‘ROE’ stands for Return on Equity. It is

annualized and a non-GAAP measure. Refer to the appendix Non-IFRS Financial measures and reconciliations.

Source: IBGE, Nu.

Nu’s pace of customer growth continues to surpass expectations,

reaching 110 million customers at quarter-end, up 56% from the 70 million two years ago. The activity rate also reached

a new high of 84%. In Brazil, the customer base increased by 18% YoY to 98.8 million, accounting for 56% of

the country’s adult population, with 60% of monthly active customers designating Nu as their primary banking account (PBA).

Mexico also experienced strong growth, with 1.2 million net-adds over the quarter, bringing the total to 8.9 million customers

and underscoring the effectiveness of Nu's strategy to enhance deposit yields in the country, which has accelerated growth and strengthened

its position as Mexico’s leading digital financial platform. Additionally, Colombia reached a significant milestone of 2.0 million

customers, sustaining the positive momentum from the launch of the Nu Cuenta product.

| | | |

| | | 5 |

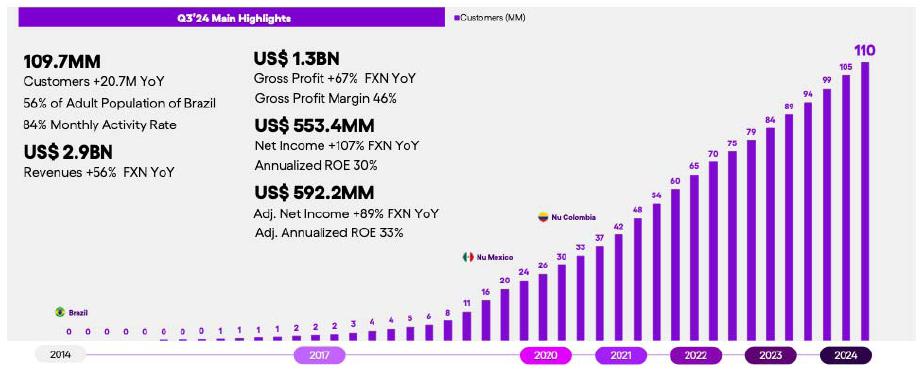

Compounding Growth Showcasing Robust Cohort Performance

Nota 1: ‘LTM’ is the last twelve months for

the period ended September 30, 2024. Source: Nu.

Nu’s flywheel effectively drives customer engagement,

as evidenced by strong cohort performance on revenues. This consistent compound growth across all cohorts underpins Nu’s ability

to cross-sell and upsell to customers.

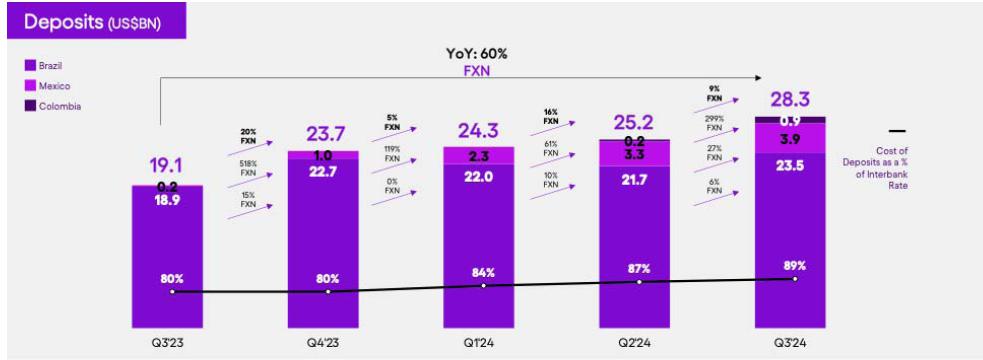

Robust Deposit Franchise Fueled By Volume Growth and Cost of Deposits Aligned with Nu’s

Strategy in New Geos

Note 1: Amounts are presented in US dollars and growth

rates on an FX Neutral basis. For additional detail on calculations please refer to the appendix Non-IFRS Financial measures and reconciliations.

Note 2: Rates presented are calculated as the ratio between

the interest expenses paid to customers in the period and the interest income of the same deposits yielding 100% of the respective interbank

rate: Mexico (“TIIE”), Colombia (”IBR”) and Brazil (“CDI”).

Source: Nu, BCB, Banxico, Banrep.

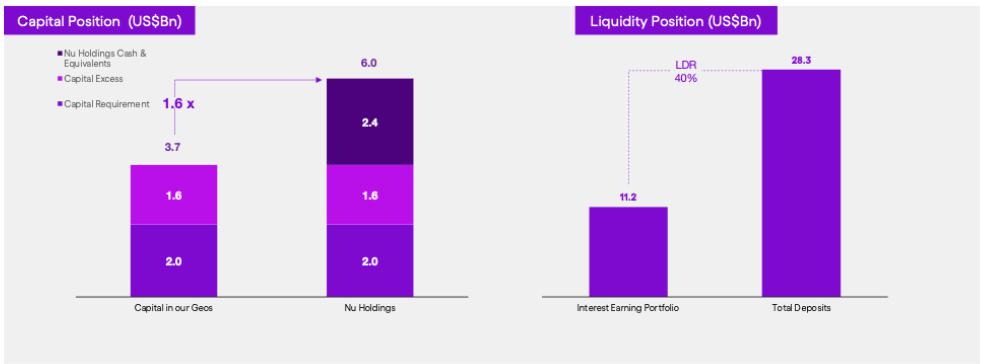

During the quarter,

deposits increased 60% YoY FXN, to $28.3 billion in Q3'24, while the funding cost reached 89% of the blended interbank

rates of the countries in which we operate in the quarter. The

loan-to-deposit ratio (LDR) was 40%, versus 39% in the previous quarter.

| | | |

| | | 6 |

Strong Performance for Both Credit Card and Lending Portfolios, with

Lending Gaining More Relevance Over Time

Note 1: Amounts are presented in US dollars and growth

rates on an FX Neutral basis. For additional detail on calculations please refer to the appendix Non-IFRS Financial measures and reconciliations.

Note 2: All amounts are presented gross of provisions.

Source: Nu.

Total credit card and lending gross receivables increased 47%

YoY FXN, reaching $20.9 billion in Q3'24 while the Interest Earning Portfolio (“IEP”) rose 81% YoY FXN, to $11.2

billion. Growth was mainly driven by sustained growth in credit card receivables, which were up 33% YoY FXN to $15.2 billion,

and in lending, which increased 97% YoY FXN to $5.7 billion.

Nu's interest-earning installments remained steady at 28%

of total credit card portfolio, aligning with expectations shared last quarter. While demand for PIX Financing products remains strong,

Nu has intentionally slowed the pace of eligibility expansion to more closely monitor performance over the coming quarters. If the portfolio

continues to perform well, Nu may resume growth in the near term. The focus is on gathering additional data to ensure credit models remain

resilient. The demand for this product is very clear, and Nu is strategically managing supply to safeguard credit quality and maintain

portfolio resilience.

| | | |

| | | 7 |

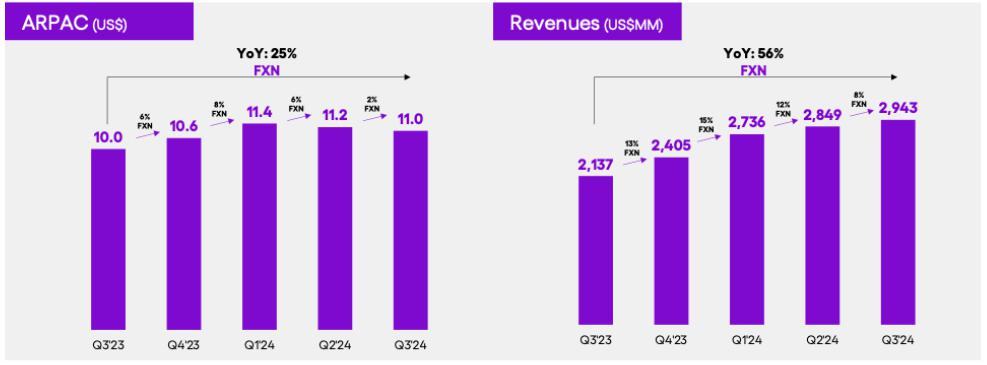

Sustained Revenue Growth Fueled by Customer Acquisition and ARPAC

Expansion

Note 1: Amounts are presented in US dollars and growth

rates on an FX Neutral basis. For additional detail on calculations please refer to the appendix Non-IFRS Financial measures and reconciliations.

Note 2: ‘Average revenue per active customer’

or ‘ARPAC’ is defined as the average monthly revenue (total revenue divided by the number of months in the period) divided

by the average number of individual active customers during the period (average number of individual active customers is defined as the

average of the number of monthly active customers at the beginning of the period measured, and the number of monthly active customers

at the end of the period).

Source: Nu.

ARPAC increased 25% YoY FXN to $11.0 in Q3'24,

while revenues reached a new record high of $2.9 billion, up 56% YoY FXN. The dynamics of ARPAC in this slide are affected

by the acceleration of Nu's customer base in Mexico and, more recently, in Colombia. While deposits strategy in these new geos may attract

customers who initially engage with the Cuenta product only, a product that generates relatively low ARPAC levels, Nu is very confident

in the long-term results that this growth strategy is expected to yield for the Company, as seen in Brazil for almost a decade now.

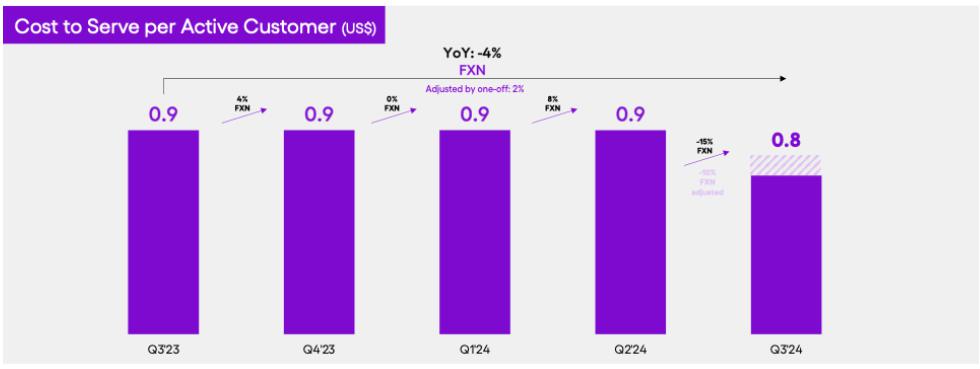

Decreasing Cost to Serve Underscores Operating Leverage Potential

Note 1: Amounts are presented in US dollars and growth

rates on an FX Neutral basis. For additional detail on calculations please refer to the appendix Non-IFRS Financial measures and reconciliations.

Note 2: ‘Cost to serve’ is defined as the

monthly average of the sum of transactional expenses, customer support and operations expenses (sum of these expenses in the period divided

by the number of months in the period) divided by the average number of individual active customers during the period (average number

of individual active customers is defined as the average of the number of monthly active customers at the beginning of the period measured,

and the number of monthly active customers at the end of the period).

Note 3: Q3’24 one-off adjustment was related to cloud

service provider retroactive fixed FX correction relocated from Customer Service to G&A.

Source: Nu.

| | | |

| | | 8 |

Monthly Average Cost to Serve Per Active Customer was $0.7

in Q3'24, or $0.8 adjusted by one-offs explained next, remaining below the $1 level. On an FX-neutral basis, this represents a

2% year-over-year increase when adjusted for one-offs in Q3'24, mostly related to FX impacts on data and cloud costs that had been allocated

under customer services and now were reallocated to G&A, as FX variations are unrelated to customer services and align better with

general administrative expenses. During the same period, Nu’s ARPAC grew by 25%, highlighting the strong operating leverage of

Nu’s business model.

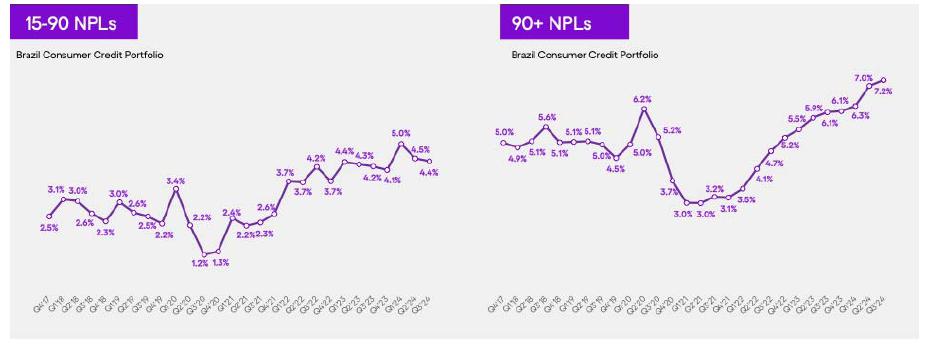

Delinquency Ratios Tracking Expectations

Note 1: Includes both credit card and lending excluding

SMEs (Small and Medium-sized Enterprises).

Note 2: ‘NPL’ is a non-performing loan.

Note 3: In Q2’22, we reviewed and changed our write-off

methodology for recovery of the contractual cash-flows of NPLs arising from unsecured lending from 360+ days to 120+ days. Figures consider

this change. Our write-off methodology for credit cards remained unchanged at 360+ days.

Note 4: Information presented for Brazil only.

Source: Nu, BCB.

Non-Performing

Loans The decline of Nu's leading indicator, the NPL 15-90 observed during the second quarter

of 2024, continued into this quarter, with NPLs decreasing by 10 basis points to 4.4%4.

Meanwhile, the 90+ NPL ratio increased 20bp sequentially to

7.2%4, aligned with expectations.

Recall that 90+ behaves as a stock rather than flow metric, in the sense that this quarter's 90+ houses inventory that was in 15-90 from

one quarter ago all the way to three quarters ago. Thus to understand the movement in 90+ from last quarter to this quarter it's important

to trace it back to the change in 15-90 from four quarters ago all the way to last quarter.

4: Data for Brazil only.

Comfortable Capital and Liquidity Positions

Note 1: Brazil figures consider the Capital Adequacy Ratio

(CAR) requirement of 8.75%, applicable to the conglomerate led by Nu Pagamentos S.A. as of September 2024, according to BCB Resolution

No. 200/22. Mexico's figures consider the NICAP required for a SOFIPO type 4, equivalent to a Capital Adequacy ratio of 10.5%; Colombia's

figures consider a minimum Capital Adequacy Ratio of 10.5%, applicable to Nu Financiera, as a regulated entity.

Note 2: ‘LDR’ stands for Loan to Deposit Ratio.

Source: Nu.

| | | |

| | | 9 |

Capital Nu

has further strengthened its position standing as one of the best-capitalized players in the region. Its Capital Adequacy Ratios (CARs)

are well-above the the regulatory minimums across countries of operations, even excluding the $2.4 billion excess liquidity held

by Nu Holdings.

REVENUE, FINANCIAL AND TRANSACTIONAL COSTS AND GROSS PROFIT

Revenue

Revenue increased 56% YoY FXN, to another record

high of $2,943.2 million in

Q3’24.

| Revenue ($ million) |

Q3'24 |

Q3'23 |

| Interest Income and Gains (Losses) on Financial Instruments |

2,473.8 |

1,732.7 |

| Fee and Commission Income |

469.4 |

404.1 |

| Total |

2,943.2 |

2,136.8 |

| FX Neutral |

|

|

| Interest income and Gains (Losses) on Financial Instruments |

2,473.8 |

1,526.0 |

| Fee and Commission Income |

469.4 |

355.9 |

| Total |

2,943.2 |

1,881.9 |

Interest Income and Gains on Financial Instruments increased

62% YoY FXN, reaching $2,473.8 million in Q3’24. This growth was mainly driven by two factors: (i) sustained high

interest income from the consumer finance portfolio, generated from the ongoing expansion of credit cards and lending; and (ii) the credit

mix, mainly related to the increase in installments with interest within the credit card portfolio. Fee and Commission Income in

Q3'24 increased 32% YoY FXN to $469.4 million. This growth was mainly driven by the following increases: (i) interchange

fees, supported by increased purchase volumes on credit and prepaid cards, reflecting ongoing growth of Nu's customer base and activity

rates; and (ii) late fees also due to the overall growth of Nu's credit portfolio.

| | | |

| | | 10 |

Cost of Financial and Transactional Services Provided

Cost of Financial and Transactional Services Provided increased

48% YoY FXN to $1,594.6 million. In Q3’24, this cost accounted for 54% of revenues in the quarter, versus 57%

in Q3'23, reflecting the following dynamics:

| Cost of Financial and Transactional Services Provided ($ million) |

Q3'24 |

Q3'23 |

| Interest and Other Financial Expenses |

(761.0) |

(537.6) |

| Transactional Expenses |

(59.5) |

(56.8) |

| Credit Loss Allowance Expenses |

(774.1) |

(627.5) |

| Total |

(1,594.6) |

(1,221.9) |

| % of Revenue |

54% |

57% |

| FX Neutral |

|

|

| Interest and Other Financial Expenses |

(761.0) |

(473.6) |

| Transactional Expenses |

(59.5) |

(50.0) |

| Credit Loss Allowance Expenses |

(774.1) |

(552.6) |

| Total |

(1,594.6) |

(1,076.2) |

| % of Revenue |

54% |

57% |

Interest

and Other Financial Expenses increased as a result of: (i) higher interest expenses on retail deposits reflecting the expansion of Nu’s

retail deposits balance, which reached $28.3 billion this quarter; and (ii) higher interest expenses over debt instruments and

financing due the issuance of financial letters, repurchase agreements

and interest related to new borrowings particularly derived from the

expansion of operations in Mexico and Colombia.

Finally, similar to prior quarters, Credit Loss Allowance Expenses

increased primarily driven by the growth of the credit portfolio, as Nu Holdings frontloads provisions based on the expected losses for

the life of the credit in accordance with the IFRS 9 methodology.

Gross Profit

Gross Profit reached $1,348.6 million, up 67% YoY

FXN while gross profit margin achieved 46% from 43% in Q3'23.

| | | |

| | | 11 |

OPERATING EXPENSES

Operating Expenses amounted to $624.8 million in Q3'24,

increasing 41% YoY FXN, but declining three percentage points as a percentage of revenues, from 24% in Q3'23 to 21%

this quarter.

| Operating Expenses ($ million) |

Q3'24 |

Q3'23 |

| Customer Support and Operations |

(135.2) |

(127.3) |

| General and Administrative Expenses |

(284.7) |

(264.3) |

| Marketing Expenses |

(99.8) |

(46.5) |

| Other expenses |

(105.1) |

(65.2) |

| Total |

(624.8) |

(503.3) |

| % of Revenue |

21% |

24% |

| FX Neutral |

|

|

| Customer Support and Operations |

(135.2) |

(112.1) |

| General and Administrative Expenses |

(284.7) |

(232.8) |

| Marketing Expenses |

(99.8) |

(41.0) |

| Other Income (Expenses) |

(105.1) |

(57.4) |

| Total |

(624.8) |

(443.3) |

| % of Revenue |

21% |

24% |

The absolute YoY growth in Operating Expenses was mainly driven

by the following increases: (i) Marketing Expenses, which rose 143% FXN as Nu made investments to further solidify and build brand

trust. Additionally, there were US$40 million in marketing expenses recorded in September, 2024, aimed at repositioning Nucoins within

a new loyalty program developed for Nubank's customers; (ii) General and Administrative Expenses, which increased 22% FXN due to

rising infrastructure and data processing costs, and higher salaries and associated benefits linked to the Company’s overall growth

as well as US$8 million one-off expenses attributed to the impairment of certain capitalized intangible assets associated with the discontinuation

of the liquidity pool feature for Nucoins5; and (iii) Other Income (Expenses) as a result of higher federal taxes due

the increase of interest income.

5: The post-tax effects associated with the repositioning

of Nucoins amounted to US$28.5 million as of Q3'24.

| | | |

| | | 12 |

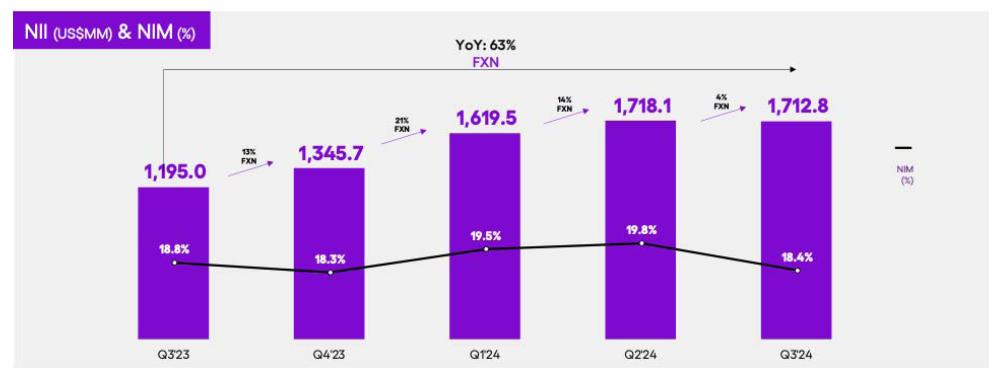

Net Interest Income Expansion Driven by Growth of Interest Earning

Portfolio

Note 1: ‘NII’ stands

for Net Interest Income and is calculated as Interest income and gains (losses) on financial instruments minus Interest and other financial

expenses.

Note 2: ‘NIM’ stands

for Net Interest Margin, is annualized, and is the ratio between NII in the numerator and the denominator is defined as the following

average balance sheet metrics: i) Cash and cash equivalents ii) Financial assets at fair value through profit or loss iii) Financial assets

at fair value through OCI iv) Compulsory deposits at central banks v) Credit Card Interest-earning portfolio vi) Loans to customers (gross)

vii) Interbank transactions viii) Other receivables ix) Other financial assets at amortized cost x) Securities.

Note 3: Amounts are presented

in US dollars and growth rates on an FX Neutral basis. For additional detail on calculations please refer to the appendix Non-IFRS Financial

measures and reconciliations.

Source: Nu.

Net interest income, or NII, increased by 63% YoY FXN,

reaching US$1.7 billion. Growth was driven by sustained expansion of Nu's credit card and lending portfolios, collectively boosting

NII and net interest margin (NIM) on an annual basis. The slowdown in growth QoQ was mainly driven by the combination of three factors:

(i) yields on the credit card portfolio declined reflecting an improved customer and product risk profile; (ii) lending yields declined

as secured loans continue to grow; and (iii) funding costs in Mexico and Colombia continue pressured, in line with Nu’s yield strategy

to quickly ramp-up deposit growth in new geos.

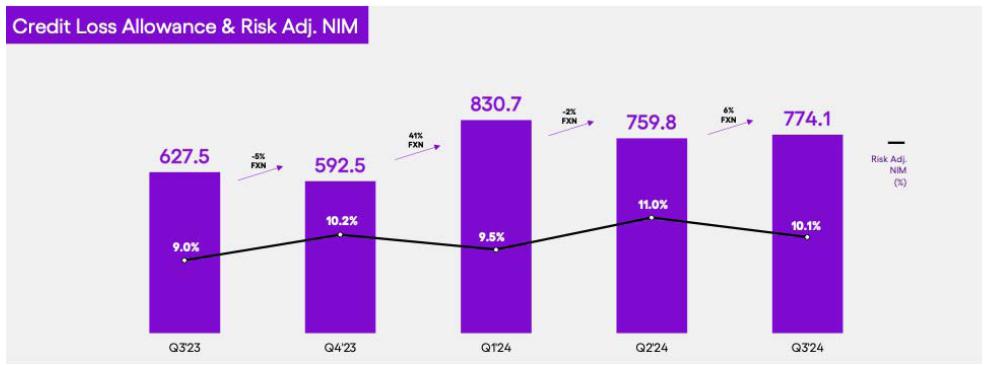

Risk-Adjusted NIM Performance Demonstrates Effective Pricing

for Marginal Risk

Note 1: ‘CLA’ stands for Credit Loss Allowance

Expenses.

Note 2: ‘Risk Adj. NIM’ stands for Risk Adjusted

Net Interest Margin, is annualized, and is calculated by dividing NII (Net Interest Income) net of CLA (Credit Loss Allowance) by Interest

Earning Assets defined as the following average balance sheet metrics: i) Cash and cash equivalents; ii) Financial assets at fair value

through profit or loss; iii) Financial assets at fair value through other comprehensive income; iv) Compulsory deposits at central banks;

v) Credit Card Interest-earning portfolio; vi) Loans to customers (gross); vii) Interbank transactions; viii) Other receivables; ix) Other

financial assets at amortized cost; and x) Securities.

Note 3: The amount of CLA is related to the Credit Loss

Allowance net of Recoveries.

Source: Nu.

| | | |

| | | 13 |

Credit loss allowance expenses increased to US$774.1 million

this quarter, expanding 6% QoQ FXN. This increase was aligned with the growth pace of Nu’s credit portfolio and early delinquency

performance.

Risk-Adjusted NIM reached 10.1% and decreased 90 bp

in the quarter, as a result of the 140 bp decrease in NIM, which was partially offset by a 50 bp improvement in cost of risk. On a year-on-year

basis, Risk-Adjusted NIM increased 110 bp, underscoring Nu’s focus on optimizing the lifetime value of customer relationship cohorts.

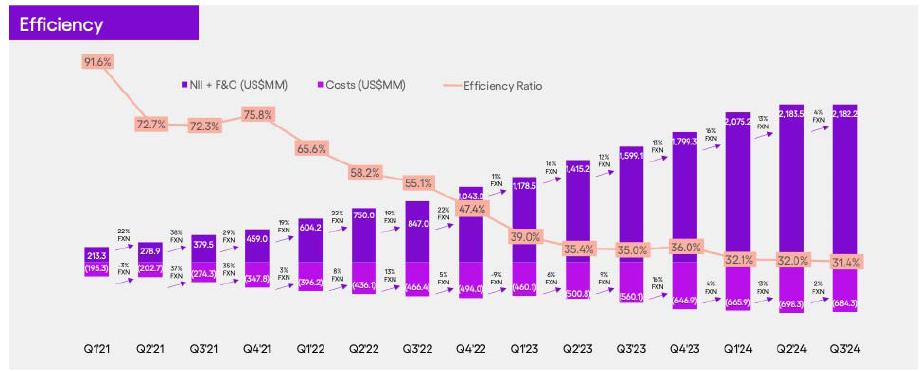

Strong Track Record of Driving Operating Leverage as Business

Scales

Note 1: ‘NII’ stands

for Net Interest Income and is calculated as Interest income and gains (losses) on financial instruments minus Interest and other financial

expenses.

Note 2: ‘F&C’

stands for Fee and Commission Income.

Note 3: ‘Costs’ include

transactional costs and operating expenses.

Note 4: Efficiency Ratio is defined

as Total Operating Expenses plus Transactional Expenses divided by NII and Fees and Commission Income.

Note 5: Q4’22 Efficiency

Ratio and Costs exclude the effect of the one-time non-cash recognition of the 2021 CSA termination. Unadjusted Efficiency Ratio was 81%,

and Unadjusted Costs was US$849.6 million. For additional detail on calculations please refer to the appendix Non-IFRS Financial measures

and reconciliations.

Source: Nu.

The efficiency ratio improved 60 bp QoQ and over 350 bp YoY

reaching 31.4% in Q3'24.

Nu is poised to capitalize on the platform's operating leverage

as it continues to expand its customer base, upsell and cross-sell products, introduce new features, and achieve profitability in the

new markets of Mexico and Colombia, which are currently in their investment phases.

EARNINGS

Net Income

Nu continues to deliver higher profitability with Net Income

increasing to $553.4 million in Q3'24, up from $303.0 million in Q3'23, highlighting the success of its strategy and business

model.

Adjusted Net Income

Adjusted Net Income increased to $592.2 million in Q3'24,

from $355.6 million in Q3'23. Adjusted Net Income is a non-IFRS measure calculated using profit (loss) adjusted for expenses related

to Nu’s share-based compensation as well as the tax effects related to these items, among others. For more information, please see

“Non-IFRS Financial Measures and Reconciliations".

| | | |

| | | 14 |

| | | |

| | | 15 |

Activity rate -

is defined as monthly active customers divided by the total number of customers as of a specific date.

CDI (“Certificado

de Depósito Interbancário”) - Brazilian interbank deposit rate.

Credit Loss Allowance

Expenses/Credit Portfolio - is defined as credit loss allowance expenses, divided by the sum of receivables from credit

card operations (current, installments and revolving) and loans to customers, in each case gross of ECL allowance, as of the period end

date.

Customer

- is defined as an individual or SME that has opened an account with Nu and does not include any such individuals or SMEs that have

been charged-off or blocked or have voluntarily closed their account.

ECL or ECL Allowance

- means the expected credit losses in Nu's credit operations, including loans and credit cards.

Efficiency ratio –

refers to the ratio between total non-interest operating expenses and transactional costs divided by net interest income plus fees and

commissions income.

Foreign Exchange ("FX”)

Neutral Measures - refer to certain measures prepared and presented in this earnings release to eliminate the effect

of FX volatility between the comparison periods, allowing management and investors to evaluate Nu's financial performance despite variations

in foreign currency exchange rates, which may not be indicative of the Company's core operating results and business outlook. For additional

information, see “Non-IFRS Financial Measures and Reconciliations”.

IBR (“Indicador

Bancario de Referencia”) - Colombian interbank deposit rate.

Interest-Earning Portfolio

("IEP")- consists of receivables from credit card operations on which Nu is accruing interest and loans to

customers, in each case prior to ECL allowance, as of the period end date.

Loan-to-Deposit Ratio

(“LDR”) - is calculated as the total balance for Interest-Earning Portfolio divided by the total amount

of deposits at the end of the same period.

Monthly Active Customers

- is defined as all customers that have generated revenue in the last 30 calendar days.

Monthly Average Cost

to Serve per Active Customer - is defined as the monthly average of the sum of transactional expenses and customer support

and operations expenses (sum of these expenses in the period divided by the number of months in the period) divided by the average number

of individual monthly active customers during the period (average number of individual monthly active customers is defined as the average

of the number of monthly active customers at the beginning of the period measured, and the number of monthly active customers at the end

of the period).

Monthly Average Revenue

per Active Customer or Monthly ARPAC ("ARPAC")- is defined as the average monthly revenue (total revenue divided

by the number of months in the period) divided by the average number of individual monthly active customers during the period (average

number of individual monthly active customers is defined as the average of the number of monthly active customers at the beginning of

the period measured, and the number of monthly active customers at the end of the period).

| | | |

| | | 16 |

Net Interest Income

("NII") - is defined as interest income and gains (losses) on financial instruments minus interest and other

financial expenses.

Net Interest Margin

("NIM") - is defined as the annualized ratio between NII in the numerator and the denominator is defined as

the following average balance sheet metrics: i) Cash and cash equivalents ii) Financial assets at fair value through profit or loss iii)

Financial assets at fair value through OCI iv) Compulsory deposits at central banks v) Credit Card Interest-earning portfolio vi) Loans

to customers (gross) vii) Interbank transactions viii) Other credit operations ix) Other financial assets at amortized cost.

Non-Performing Loans

("NPL") - is defined as the non-performing loans balance (e.g. NPLs 15 to 90 days or 90+ days) divided by the total

outstanding balance of consumer credit portfolio (i.e. excluding SMEs).

Nu Pagamentos -

Nu Holdings’ subsidiary in Brazil.

Nu Financiera

- Nu Holding’s subsidiary in Colombia.

Primary Banking Account

("PBA") - refers to Nu’s relationship with those customers who had at least 50% of their post-tax monthly

income transferred out of their NuAccount in any given month, excluding self transfers. We calculate the percent of customers with a primary

banking relationship as active customers with a primary banking relationship as a percentage of total active customers that have been

with us for more than 12 months.

Purchase Volume ("PV")

- is defined as the total value of transactions that are authorized through Nu's credit, prepaid cards and payments

through Nu's platform; it does not include other payment methods that we offer such as PIX transfers, WhatsApp payments or traditional

wire transfers.

Recovery - is the estimated

amount of a defaulted contract with a customer that the company expects to receive.

Risk-Adjusted Net Interest

Margin ("Risk-adjusted NIM") - is annualized, and is calculated by dividing NII net of CLA by Interest Earning Assets

defined as the following average balance sheet metrics: i) Cash and cash equivalents ii) Financial assets at fair value through profit

or loss iii) Financial assets at fair value through OCI iv) Compulsory deposits at central banks v) Credit Card Interest-earning portfolio

vi) Loans to customers (gross) vii) Interbank transactions viii) Other receivables ix) Other financial assets at amortized cost x) Securities.

SMEs -

small and medium-sized enterprises.

TIIE (“Tasa de

Interés Interbancaria de Equilibrio”) - Mexican interbank deposit rate.

Total Portfolio -

is the addition of credit card exposures and lending to customers.

Write-off - constitutes

a derecognition event when the institution has no reasonable expectations of recovering the contractual cash flows.

| | | |

| | | 17 |

This release speaks at the date hereof and the Company is under

no obligation to update or keep current the information contained in this release. Any information expressed herein is subject to change

without notice. Any market or other third-party data included in this release has been obtained by the Company from third-party sources.

While the Company has compiled and extracted the market data, it can provide no assurances of the accuracy and completeness of such information

and takes no responsibility for such data.

This release contains forward-looking statements. All statements

other than statements of historical fact contained in this release may be forward-looking statements and include, but are not limited

to, statements regarding the Company’s intent, belief or current expectations. These forward-looking statements are subject to risks

and uncertainties, and may include, among others, financial forecasts and estimates based on assumptions or statements regarding plans,

objectives and expectations. Although the Company believes that these estimates and forward-looking statements are based upon reasonable

assumptions, they are subject to several risks and uncertainties and are made in light of information currently available, and actual

results may differ materially from those expressed or implied in the forward-looking statements due to various factors, including those

risks and uncertainties included under the captions “Risk Factors” and “Management’s Discussion and Analysis of

Financial Condition and Results of Operations” in the prospectus dated December 8, 2021 filed with the Securities and Exchange Commission

pursuant to Rule 424(b) under the Securities Act of 1933, as amended, and in the Annual Report on Form 20-F for the year ended December

31, 2023, which was filed with the Securities and Exchange Commission on April 19, 2024. The Company, its advisers and each of their respective

directors, officers and employees disclaim any obligation to update the Company’s view of such risks and uncertainties or to publicly

announce the result of any revision to the forward-looking statements made herein, except where it would be required to do so under applicable

law. The forward-looking statements can be identified, in certain cases, through the use of words such as “believe,” “may,”

“might,” “can,” “could,” “is designed to,” “will,” “aim,” “estimate,”

“continue,” “anticipate,” “intend,” “expect,” “forecast”, “plan”,

“predict”, “potential”, “aspiration,” “should,” “purpose,” “belief,”

and similar, or variations of, or the negative of such words and expressions.

The financial information in this document includes forecasts,

projections and other predictive statements that represent the Company’s assumptions and expectations in light of currently available

information. These forecasts, projections and other predictive statements are based on the Company’s expectations and are subject

to variables and uncertainties. The Company’s actual performance results may differ. Consequently, no guarantee is presented or

implied as to the accuracy of specific forecasts, projections or predictive statements contained herein, and undue reliance should not

be placed on the forward-looking statements in this release, which are inherently uncertain. In addition to IFRS financials, this release

includes certain summarized, non-audited or non-IFRS financial information. These summarized, non-audited or non-IFRS financial measures

are in addition to, and not a substitute for or superior to, measures of financial performance prepared in accordance with IFRS. References

in this release to “R$” refer to the Brazilian Real, the official currency of Brazil.

| | | |

| | | 18 |

This release includes financial measures defined as “non-IFRS

financial measures” by the SEC, including: Adjusted Net Income and certain FX Neutral measures and provides reconciliations to the

most directly comparable IFRS financial measure. A non-IFRS financial measure is generally defined as a numerical measure of historical

or future financial performance or financial position that purports to measure financial performance but excludes or includes amounts

that would not be so adjusted in the most comparable IFRS measure. These non-IFRS financial measures are in addition to, and not a substitute

for or superior to, measures of financial performance prepared in accordance with IFRS.

Adjusted Net Income is

defined as profit (loss) attributable to shareholders of the parent company for the period, adjusted for the expenses and allocated tax

effects on share-based compensation.

Adjusted Net Income is presented because management believes

that this non-IFRS financial measure can provide useful information to investors, securities analysts and the public in their review of

the operating and financial performance of the Company, although it is not calculated in accordance with IFRS or any other generally accepted

accounting principles and should not be considered as a measure of performance in isolation. Nu also uses Adjusted Net Income as a key

profitability measure to assess the performance of the business. Nu believes Adjusted Net Income is useful to evaluate operating and financial

performance for the following reasons:

| ● | Adjusted Net Income is widely used

by investors and securities analysts to measure a company’s operating |

| ● | performance without regard to items that can

vary substantially from company to company and from period to period, depending on their accounting and tax methods, the book value and

the market value of their assets and liabilities, and the method by which their assets were acquired; and |

| ● | Non-cash equity grants made to executives,

employees or consultants at a certain price and point in time, and their hedge accounting effects for the corporate tax and social wages

and their income tax effects, do not necessarily reflect how the business is performing at any particular time and the related expenses

(and their subject impacts in the market value of assets and liabilities) are not key measures of core operating performance. |

Adjusted Net Income is not a substitute for Net Income, which

is the IFRS measure of earnings. Additionally, the calculation of Adjusted Net Income (Loss) may be different from the calculation used

by other companies, including competitors in the technology and financial services industries, because other companies may not calculate

these measures in the same manner as we do, and therefore, measure may not be comparable to those of other companies.

| | | |

| | | 19 |

Adjusted Net Income Reconciliation

For the three-month period ended September 30, 2024 and 2023

(In millions of U.S. Dollars)

| Nu Holdings (Consolidated) |

As reported |

| For the three months ended September 30, |

| Adjusted Net Income (US$ million) |

2024 |

2023 |

| Profit attributable to shareholders of the parent company |

553.4 |

303.0 |

| Share-based compensation |

87.2 |

71.2 |

| Allocated tax effects on share-based compensation |

(30.4) |

(20.5) |

| Hedge of the tax effects on share-based compensation |

(18.0) |

1.9 |

| Adjusted Net Income for the period/year |

592.2 |

355.6 |

FX Neutral measures

are prepared and presented to eliminate the effect of foreign exchange, or “FX,” volatility between the comparison periods,

allowing management and investors to evaluate financial performance despite variations in foreign currency exchange rates, which may not

be indicative of core operating results and business outlook.

FX Neutral measures are presented because management believes that these non-IFRS financial measures can provide useful information to

investors, securities analysts and the public in their review of operating and financial performance, although they are not calculated

in accordance with IFRS or any other generally accepted accounting principles and should not be considered as a measure of performance

in isolation.

The FX Neutral measures were calculated to present what such measures in preceding periods would have been had exchange rates remained

stable from these preceding periods until the date of the Company's most recent financial information.

The FX Neutral measures for the three months ended September 30, 2023 were calculated by multiplying the as reported amounts of Adjusted

Net Income and the key business metrics for such period by the average Brazilian reais/U.S. dollars exchange rate for the three months

ended September 30, 2023 (R$4.9050 to US$1.00) and using such results to re-translate the corresponding amounts back to U.S. dollars by

dividing them by the average Brazilian reais/U.S. dollars exchange rate for the three months ended September 30, 2024 (R$5.5693 to US$1.00),

so as to present what certain of statement of profit and loss amounts and key business metrics would have been had exchange rates remained

stable from this past period until the three months ended September 30, 2024.

The average Brazilian reais/U.S. dollars exchange rates were calculated as the average of the month-end rates for each month in the three

months ended September 30, 2024 and 2023 as reported by Bloomberg.

FX Neutral measures for deposits and interest-earning portfolio were calculated by multiplying the as reported amounts as of each date,

by the spot Brazilian reais/U.S. dollars exchange rates as of each date and using such results to re-translate the corresponding amounts

back to U.S. dollars by dividing them by using the spot rate as of September 30, 2024 (R$5.4500 to US$1.00) so as to present what these

amounts would have been had exchange rates been the same on September 30, 2023. The Brazilian reais/U.S. dollars exchange rates were calculated

using rates as of such dates as reported by Bloomberg.

| | | |

| | | 20 |

FX Rates - On a

monthly basis, Nu translates its subsidiaries figures from their individual functional currency into Nu Holdings functional currency,

the U.S. Dollars ("US$"), following the requirements of IAS 21 "The Effects of Changes in Foreign Exchange Rates".

The functional currency of the Brazilian operating entities is the Brazilian Real ("R$"), of the Mexican entities is the Mexican

Peso ("MXN"), and of the Colombian entities is the Colombian Peso ("COP").

As of January 31, 2024, income statement figures were divided by the average FX Rate of the month (R$ 4.9157, MXN 17.0776 and COP 3,919.7314

to US$ 1.00) and balance sheet figures were divided by the last price FX rate of the month (R$ 4.9554, MXN 17.2133 and COP 3,915.9800

to US$ 1.00).

As of February 29, 2024, income statement figures were divided by the average FX Rate of the month (R$ 4.9632, MXN 17.0855 and COP 3,930.5262

to US$ 1.00) and balance sheet figures were divided by the last price FX Rate of the month (R$ 4.9703, MXN 17.0542 and COP 3,926.0500

to US$ 1.00).

As of March 31, 2024, income statement figures were divided by the average FX Rate of the month (R$ 4.9797, MXN 16.7634 and COP 3,901.2955

to US$ 1.00) and balance sheet figures were divided by the last price FX Rate of the month (R$ 5.0145, MXN 16.5586 and COP 3,859.4300

to US$ 1.00).

As of April 30, 2024, income statement figures were divided by the average FX Rate of the month (R$ 5.1267, MXN 16.7992 and COP 3,866.3541

to US$ 1.00) and balance sheet figures were divided by the last price FX Rate of the month (R$ 5.1936, MXN 17.1402 and COP 3,921.7400

to US$ 1.00).

As of May 31, 2024, income statement figures were divided by the average FX Rate of the month (R$ 5.1356, MXN 16.8084 and COP 3,866.1114

to US$ 1.00) and balance sheet figures were divided by the last price FX Rate of the month (R$ 5.2459, MXN 17.0119 and COP 3,868.1900

to US$ 1.00).

As of June 30, 2024, income statement figures were divided by the average FX Rate of the month (R$ 5.3968, MXN 18.2429 and COP 4,063.0875

to US$ 1.00) and balance sheet figures were divided by the last price FX Rate of the month (R$ 5.5941, MXN 18.3183 and COP 4,148.6800

to US$ 1.00).

As of July 31, 2024, income statement figures were divided

by the average FX Rate of the month (R$ 5.5439, MXN 18.1169 and COP 4,034.8926 to US$ 1.00) and balance sheet figures were divided by

the last price FX Rate of the month (R$ 5.6505, MXN 18.6170 and COP 4,064.4600 to US$ 1.00).

As of August 31, 2024, income statement figures were divided

by the average FX Rate of the month (R$ 5.5539, MXN 19.1871 and COP 4,070.7200 to US$ 1.00) and balance sheet figures were divided by

the last price FX Rate of the month (R$ 5.6075, MXN 19.7282 and COP 4,177.5300 to US$ 1.00).

As of September 30, 2024, income statement figures were divided

by the average FX Rate of the month (R$ 5.5408, MXN 19.6054 and COP 4,191.7043 to US$ 1.00) and balance sheet figures were divided by

the last price FX Rate of the month (R$ 5.4500, MXN 19.6915 and COP 4,204.3400 to US$ 1.00).

Equity figures are translated using the FX Rate on the date

of each transaction.

| | | |

| | | 21 |

Profit or Loss

For the three-month period ended September 30, 2024 and 2023

(In thousands of U.S. Dollars)

| |

09/30/2024 |

|

09/30/2023 |

| |

|

|

|

| Interest income and gains (losses) on financial instruments |

2,473,807 |

|

1,732,699 |

| Fee and commission income |

469,381 |

|

404,059 |

| Total revenue |

2,943,188 |

|

2,136,758 |

| Interest and other financial expenses |

(760,959) |

|

(537,649) |

| Transactional expenses |

(59,454) |

|

(56,774) |

| Credit loss allowance expenses |

(774,144) |

|

(627,506) |

| Total cost of financial and transactional services provided |

(1,594,557) |

|

(1,221,929) |

| Gross profit |

1,348,631 |

|

914,829 |

| |

|

|

|

| Operating expenses |

|

|

|

| Customer support and operations |

(135,196) |

|

(127,295) |

| General and administrative expenses |

(284,706) |

|

(264,264) |

| Marketing expenses |

(99,818) |

|

(46,483) |

| Other income (expenses) |

(105,121) |

|

(65,242) |

| Total operating expenses |

(624,841) |

|

(503,284) |

| |

|

|

|

| Profit before income taxes |

723,790 |

|

411,545 |

| |

|

|

|

| Income taxes |

|

|

|

| Current taxes |

(335,468) |

|

(307,248) |

| Deferred taxes |

165,064 |

|

198,739 |

| Total income taxes |

(170,404) |

|

(108,509) |

| |

|

|

|

| Profit for the period |

553,386 |

|

303,036 |

| Earnings per share – Basic |

0.1153 |

|

0.0638 |

| Earnings per share – Diluted |

0.1132 |

|

0.0624 |

| Weighted average number of outstanding shares – Basic (in thousands of shares) |

4,797,673 |

|

4,752,303 |

| Weighted average number of outstanding shares – Diluted (in thousands of shares) |

4,889,409 |

|

4,856,845 |

| | | |

| | | 22 |

Financial Position

As of September 30, 2024 and December 31, 2023

(In thousands of U.S. Dollars)

| |

09/30/2024 |

|

12/31/2023 |

| |

|

|

|

| Assets |

|

|

|

| Cash and cash equivalents |

7,645,754 |

|

5,923,440 |

| Financial assets at fair value through profit or loss |

314,885 |

|

389,875 |

| Securities |

119,281 |

|

368,574 |

| Derivative financial instruments |

195,272 |

|

20,981 |

| Collateral for credit card operations |

332 |

|

320 |

| Financial assets at fair value through other comprehensive income |

11,019,200 |

|

8,805,745 |

| Securities |

11,019,200 |

|

8,805,745 |

| Financial assets at amortized cost |

26,240,578 |

|

24,988,919 |

| Credit card receivables |

12,689,210 |

|

12,414,133 |

| Loans to customers |

4,939,376 |

|

3,202,334 |

| Compulsory and other deposits at central banks |

6,800,215 |

|

7,447,483 |

| Other receivables |

971,286 |

|

1,689,030 |

| Other financial assets |

180,827 |

|

131,519 |

| Securities |

659,664 |

|

104,420 |

| Other assets |

667,126 |

|

936,209 |

| Deferred tax assets |

1,898,399 |

|

1,537,835 |

| Right-of-use assets |

23,606 |

|

30,459 |

| Property, plant and equipment |

29,873 |

|

39,294 |

| Intangible assets |

357,640 |

|

295,881 |

| Goodwill |

440,789 |

|

397,538 |

| Total assets |

48,637,850 |

|

43,345,195 |

| | | |

| | | 23 |

| |

09/30/2024 |

|

12/31/2023 |

| |

|

|

|

| Liabilities |

|

|

|

| Financial liabilities at fair value through profit or loss |

624,468 |

|

242,615 |

| Derivative financial instruments |

142,105 |

|

28,173 |

| Instruments eligible as capital |

- |

|

3,988 |

| Repurchase agreements |

482,363 |

|

210,454 |

| Financial liabilities at amortized cost |

38,374,202 |

|

34,582,759 |

| Deposits |

28,319,121 |

|

23,691,130 |

| Payables to network |

8,556,150 |

|

9,755,285 |

| Borrowings and financing |

1,498,931 |

|

1,136,344 |

| Salaries, allowances and social security contributions |

222,529 |

|

166,876 |

| Tax liabilities |

948,536 |

|

1,300,845 |

| Lease liabilities |

29,871 |

|

36,942 |

| Provision for lawsuits and administrative proceedings |

21,716 |

|

8,082 |

| Deferred income |

71,349 |

|

68,360 |

| Other liabilities |

700,831 |

|

532,331 |

| Total liabilities |

40,993,502 |

|

36,938,810 |

| |

|

|

|

| Equity |

|

|

|

| Share capital |

84 |

|

84 |

| Share premium reserve |

5,045,986 |

|

4,972,922 |

| Accumulated gains |

2,847,553 |

|

1,276,949 |

| Other comprehensive income (loss) |

(249,275) |

|

156,430 |

| Total equity |

7,644,348 |

|

6,406,385 |

| Total liabilities and equity |

48,637,850 |

|

43,345,195 |

| | | |

| | | 24 |

Cash Flows

For the six-month period ended September 30, 2024 and 2023

(In thousands of U.S. Dollars)

| |

09/30/2024 |

|

09/30/2023 |

| |

|

|

|

| Cash flows from operating activities |

|

|

|

| Reconciliation of profit to net cash flows from operating activities: |

|

|

|

| Profit for the period |

1,419,472 |

|

669,653 |

| Adjustments: |

|

|

|

| Depreciation and amortization |

56,067 |

|

46,350 |

| Credit loss allowance expenses |

2,569,667 |

|

1,784,854 |

| Deferred income taxes |

(566,243) |

|

(466,685) |

| Provision for lawsuits and administrative proceedings |

15,079 |

|

3,470 |

| Unrealized losses on other investments |

- |

|

21,720 |

| Unrealized (gains) losses on financial instruments |

(65,315) |

|

42,995 |

| Interest accrued |

147,924 |

|

68,843 |

| Share-based compensation |

224,766 |

|

168,970 |

| Others |

5,690 |

|

14,025 |

| |

3,807,107 |

|

2,354,195 |

| |

|

|

|

| Changes in operating assets and liabilities: |

|

|

|

| Securities |

(2,626,719) |

|

1,279,337 |

| Compulsory deposits and others at central banks |

672,489 |

|

(3,087,936) |

| Credit card receivables |

(2,800,856) |

|

(5,060,879) |

| Other assets |

223,682 |

|

33,994 |

| Loans to customers |

(3,529,963) |

|

(2,453,595) |

| Other receivables |

746,405 |

|

(1,086,236) |

| Deposits |

4,808,325 |

|

3,326,450 |

| Payables to network |

(1,266,302) |

|

943,798 |

| Deferred income |

3,105 |

|

19,649 |

| Other liabilities |

701,421 |

|

632,384 |

| Interest paid |

(87,840) |

|

(64,962) |

| Income tax paid |

(1,144,831) |

|

(532,231) |

| Interest received |

1,522,924 |

|

2,255,730 |

| Cash flows generated from operating activities |

1,028,947 |

|

(1,440,302) |

| |

|

|

|

| | | |

| | | 25 |

| |

09/30/2024 |

|

09/30/2023 |

| Cash flows from investing activities |

|

|

|

| Acquisition (disposal) of property, plant and equipment |

2,307 |

|

(15,453) |

| Acquisition (disposal) and development of intangible assets |

(79,377) |

|

(130,683) |

| Acquisition of subsidiary, net of cash acquired |

(5,637) |

|

- |

| Cash flow used in investing activities |

(82,707) |

|

(146,136) |

| |

|

|

|

| Cash flows from financing activities |

|

|

|

| Proceeds from borrowings and financing |

988,295 |

|

459,154 |

| Payments of borrowings and financing |

(580,642) |

|

(46,339) |

| Lease payments |

(5,209) |

|

(5,535) |

| Exercise of stock options |

3,848 |

|

8,041 |

| Cash flows generated from financing activities |

406,292 |

|

415,321 |

| Change in cash and cash equivalents |

1,352,532 |

|

(1,171,117) |

| |

|

|

|

| Cash and cash equivalents |

|

|

|

| Cash and cash equivalents - beginning of the period |

5,923,440 |

|

4,172,316 |

| Foreign exchange rate changes on cash and cash equivalents |

369,782 |

|

212,428 |

| Cash and cash equivalents - end of the period |

7,645,754 |

|

3,213,627 |

| Increase in cash and cash equivalents |

1,352,532 |

|

(1,171,117) |

| | | |

| | | 26 |

About Nu Holdings Ltd.

Nu is one of the world’s largest digital financial

services platforms, serving more than 109 million customers across Brazil, Mexico and Colombia. Nu uses proprietary technologies and innovative

business practices to create new financial solutions and experiences for individuals and SMEs that are simple, intuitive, convenient,

low-cost, empowering and human. Guided by a mission to fight complexity and empower people, Nu is focused on connecting profit and purpose

to create value for all stakeholders and have a positive impact on the communities it serves. Nu's shares are traded on the New York Stock

Exchange (NYSE: NU). For more information, please visit www.nubank.com.br.

| | | |

| | | 27 |

SIGNATURES

Pursuant to the requirements of the Securities Exchange

Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| |

Nu Holdings Ltd. |

| |

|

| |

By: |

/s/ Jorg

Friedemann |

| |

|

Jorg

Friedemann

Investor

Relations Officer |

Date: November

13, 2024

Nu (NYSE:NU)

Graphique Historique de l'Action

De Jan 2025 à Fév 2025

Nu (NYSE:NU)

Graphique Historique de l'Action

De Fév 2024 à Fév 2025