false

FY

0001964314

0001964314

2023-06-01

2024-05-31

0001964314

dei:BusinessContactMember

2023-06-01

2024-05-31

0001964314

2024-05-31

0001964314

2024-03-01

2024-05-31

0001964314

2023-05-31

0001964314

2022-06-01

2023-05-31

0001964314

2021-06-01

2022-05-31

0001964314

us-gaap:CommonStockMember

2021-05-31

0001964314

us-gaap:AdditionalPaidInCapitalMember

2021-05-31

0001964314

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-05-31

0001964314

JBDI:CapitalReservesMember

2021-05-31

0001964314

us-gaap:RetainedEarningsMember

2021-05-31

0001964314

2021-05-31

0001964314

us-gaap:CommonStockMember

2022-05-31

0001964314

us-gaap:AdditionalPaidInCapitalMember

2022-05-31

0001964314

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-05-31

0001964314

JBDI:CapitalReservesMember

2022-05-31

0001964314

us-gaap:RetainedEarningsMember

2022-05-31

0001964314

2022-05-31

0001964314

us-gaap:CommonStockMember

2023-05-31

0001964314

us-gaap:AdditionalPaidInCapitalMember

2023-05-31

0001964314

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-05-31

0001964314

JBDI:CapitalReservesMember

2023-05-31

0001964314

us-gaap:RetainedEarningsMember

2023-05-31

0001964314

us-gaap:CommonStockMember

2021-06-01

2022-05-31

0001964314

us-gaap:AdditionalPaidInCapitalMember

2021-06-01

2022-05-31

0001964314

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-06-01

2022-05-31

0001964314

JBDI:CapitalReservesMember

2021-06-01

2022-05-31

0001964314

us-gaap:RetainedEarningsMember

2021-06-01

2022-05-31

0001964314

us-gaap:CommonStockMember

2022-06-01

2023-05-31

0001964314

us-gaap:AdditionalPaidInCapitalMember

2022-06-01

2023-05-31

0001964314

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-06-01

2023-05-31

0001964314

JBDI:CapitalReservesMember

2022-06-01

2023-05-31

0001964314

us-gaap:RetainedEarningsMember

2022-06-01

2023-05-31

0001964314

us-gaap:CommonStockMember

2023-06-01

2024-05-31

0001964314

us-gaap:AdditionalPaidInCapitalMember

2023-06-01

2024-05-31

0001964314

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-06-01

2024-05-31

0001964314

JBDI:CapitalReservesMember

2023-06-01

2024-05-31

0001964314

us-gaap:RetainedEarningsMember

2023-06-01

2024-05-31

0001964314

us-gaap:CommonStockMember

2024-05-31

0001964314

us-gaap:AdditionalPaidInCapitalMember

2024-05-31

0001964314

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-05-31

0001964314

JBDI:CapitalReservesMember

2024-05-31

0001964314

us-gaap:RetainedEarningsMember

2024-05-31

0001964314

2022-10-11

2022-10-11

0001964314

2022-10-11

0001964314

2024-02-07

2024-02-07

0001964314

2024-02-07

0001964314

JBDI:AcquisitionAgreementMember

2022-10-10

2022-10-10

0001964314

JBDI:AcquisitionAgreementMember

2022-10-10

0001964314

JBDI:EUHoldingsMember

2022-10-10

2022-10-10

0001964314

JBDI:MrLimCPMember

2022-10-10

2022-10-10

0001964314

JBDI:MsSiowKLMember

2022-10-10

2022-10-10

0001964314

JBDI:MrLimKSMember

2022-10-10

2022-10-10

0001964314

JBDI:MrLimTCMember

2022-10-10

2022-10-10

0001964314

JBDI:ArcDevelopmentMember

2022-10-10

2022-10-10

0001964314

JBDI:EUHoldingsMember

JBDI:GoldsteinMember

2022-10-10

0001964314

JBDI:EUHoldingsMember

JBDI:ReorganizationAgreementMember

us-gaap:CommonStockMember

2023-05-30

2023-05-30

0001964314

JBDI:MrLimCPMember

JBDI:ReorganizationAgreementMember

us-gaap:CommonStockMember

2023-05-30

2023-05-30

0001964314

JBDI:MsSiowKLMember

JBDI:ReorganizationAgreementMember

us-gaap:CommonStockMember

2023-05-30

2023-05-30

0001964314

JBDI:MrLimKSMember

JBDI:ReorganizationAgreementMember

us-gaap:CommonStockMember

2023-05-30

2023-05-30

0001964314

JBDI:MrLimTCMember

JBDI:ReorganizationAgreementMember

us-gaap:CommonStockMember

2023-05-30

2023-05-30

0001964314

JBDI:GoldsteinMember

JBDI:ReorganizationAgreementMember

us-gaap:CommonStockMember

2023-05-30

2023-05-30

0001964314

JBDI:ArcDevelopmentMember

JBDI:ReorganizationAgreementMember

us-gaap:CommonStockMember

2023-05-30

2023-05-30

0001964314

JBDI:EUHoldingsMember

2023-05-30

2023-05-30

0001964314

JBDI:Mr.LimCPMember

2023-05-30

2023-05-30

0001964314

JBDI:MsSiowKLMember

2023-05-30

2023-05-30

0001964314

JBDI:MrLimKSMember

2023-05-30

2023-05-30

0001964314

JBDI:MrLimTCMember

2023-05-30

2023-05-30

0001964314

JBDI:GoldsteinMember

2023-05-30

2023-05-30

0001964314

JBDI:ArcDevelopmentMember

2023-05-30

2023-05-30

0001964314

JBDI:EUHoldingsMember

2023-05-30

0001964314

JBDI:MrLimCPMember

2023-05-30

0001964314

JBDI:MsSiowKLMember

2023-05-30

0001964314

JBDI:MrLimKSMember

2023-05-30

0001964314

JBDI:MrLimTCMember

2023-05-30

0001964314

JBDI:GoldsteinMember

2023-05-30

0001964314

JBDI:ArcDevelopmentMember

2023-05-30

0001964314

JBDI:EUHoldingsMember

us-gaap:CommonStockMember

2023-05-30

0001964314

JBDI:MrLimCPMember

us-gaap:CommonStockMember

2023-05-30

0001964314

JBDI:MsSiowKLMember

us-gaap:CommonStockMember

2023-05-30

0001964314

JBDI:MrLimKSMember

us-gaap:CommonStockMember

2023-05-30

0001964314

JBDI:MrLimTCMember

us-gaap:CommonStockMember

2023-05-30

0001964314

JBDI:GoldsteinMember

us-gaap:CommonStockMember

2023-05-30

0001964314

JBDI:ArcDevelopmentMember

us-gaap:CommonStockMember

2023-05-30

0001964314

JBDI:JBDIMember

2024-05-31

0001964314

JBDI:JurongBarrelsMember

2024-05-31

0001964314

JBDI:JBDISystemsMember

2024-05-31

0001964314

JBDI:YearEndExchangeRateMember

2024-05-31

0001964314

JBDI:YearEndExchangeRateMember

2023-05-31

0001964314

JBDI:AverageExchangeRateMember

2024-05-31

0001964314

JBDI:AverageExchangeRateMember

2023-05-31

0001964314

JBDI:FactoryAndOfficeEquipmentMember

2024-05-31

0001964314

JBDI:FactoryImprovementMember

2024-05-31

0001964314

us-gaap:LeaseholdImprovementsMember

2024-05-31

0001964314

us-gaap:FurnitureAndFixturesMember

2024-05-31

0001964314

us-gaap:MachineryAndEquipmentMember

2024-05-31

0001964314

us-gaap:VehiclesMember

2024-05-31

0001964314

JBDI:RenovationMember

2024-05-31

0001964314

JBDI:LeaseholdLandImprovementsMember

2024-05-31

0001964314

country:SG

2023-06-01

2024-05-31

0001964314

country:SG

2022-06-01

2023-05-31

0001964314

country:SG

2021-06-01

2022-05-31

0001964314

srt:MaximumMember

2024-05-31

0001964314

country:SG

2024-05-31

0001964314

country:SG

us-gaap:CreditRiskMember

2024-05-31

0001964314

JBDI:SalesOfContainersandRecycledMaterialsMember

us-gaap:TransferredAtPointInTimeMember

2023-06-01

2024-05-31

0001964314

JBDI:SalesOfContainersandRecycledMaterialsMember

us-gaap:TransferredAtPointInTimeMember

2022-06-01

2023-05-31

0001964314

JBDI:SalesOfContainersandRecycledMaterialsMember

us-gaap:TransferredAtPointInTimeMember

2021-06-01

2022-05-31

0001964314

JBDI:ServicesMember

us-gaap:TransferredAtPointInTimeMember

2023-06-01

2024-05-31

0001964314

JBDI:ServicesMember

us-gaap:TransferredAtPointInTimeMember

2022-06-01

2023-05-31

0001964314

JBDI:ServicesMember

us-gaap:TransferredAtPointInTimeMember

2021-06-01

2022-05-31

0001964314

us-gaap:TransferredAtPointInTimeMember

2023-06-01

2024-05-31

0001964314

us-gaap:TransferredAtPointInTimeMember

2022-06-01

2023-05-31

0001964314

us-gaap:TransferredAtPointInTimeMember

2021-06-01

2022-05-31

0001964314

us-gaap:TransferredOverTimeMember

2023-06-01

2024-05-31

0001964314

us-gaap:TransferredOverTimeMember

2022-06-01

2023-05-31

0001964314

us-gaap:TransferredOverTimeMember

2021-06-01

2022-05-31

0001964314

JBDI:RentalMember

2023-06-01

2024-05-31

0001964314

JBDI:RentalMember

2022-06-01

2023-05-31

0001964314

JBDI:RentalMember

2021-06-01

2022-05-31

0001964314

country:ID

2023-06-01

2024-05-31

0001964314

country:ID

2022-06-01

2023-05-31

0001964314

country:ID

2021-06-01

2022-05-31

0001964314

country:MY

2023-06-01

2024-05-31

0001964314

country:MY

2022-06-01

2023-05-31

0001964314

country:MY

2021-06-01

2022-05-31

0001964314

us-gaap:OfficeEquipmentMember

2024-05-31

0001964314

us-gaap:OfficeEquipmentMember

2023-05-31

0001964314

JBDI:FactoryImprovementMember

2023-05-31

0001964314

us-gaap:LeaseholdImprovementsMember

2023-05-31

0001964314

us-gaap:FurnitureAndFixturesMember

2023-05-31

0001964314

us-gaap:MachineryAndEquipmentMember

2023-05-31

0001964314

us-gaap:VehiclesMember

2023-05-31

0001964314

JBDI:RenovationMember

2023-05-31

0001964314

JBDI:RightOfUseAssetsMember

2024-05-31

0001964314

JBDI:RightOfUseAssetsMember

2023-05-31

0001964314

us-gaap:PropertyPlantAndEquipmentMember

2023-06-01

2024-05-31

0001964314

us-gaap:PropertyPlantAndEquipmentMember

2022-06-01

2023-05-31

0001964314

us-gaap:PropertyPlantAndEquipmentMember

2021-06-01

2022-05-31

0001964314

JBDI:EUHoldingsPteLtdMember

2024-05-31

0001964314

JBDI:EUHoldingsPteLtdMember

2023-05-31

0001964314

JBDI:SoonAikGlobalPteLtdMember

2024-05-31

0001964314

JBDI:SoonAikGlobalPteLtdMember

2023-05-31

0001964314

JBDI:AmountDueToShareholdersMember

2024-05-31

0001964314

JBDI:AmountDueToShareholdersMember

2023-05-31

0001964314

JBDI:AmountDueTodirectorToLoansMember

2024-05-31

0001964314

JBDI:AmountDueTodirectorToLoansMember

2023-05-31

0001964314

JBDI:AmountDueToKDSSteelPteLtdMember

2024-05-31

0001964314

JBDI:AmountDueToKDSSteelPteLtdMember

2023-05-31

0001964314

JBDI:EUHoldingsPteLtdMember

JBDI:MrNeoChinHengMember

2024-05-31

0001964314

JBDI:EUHoldingsPteLtdMember

JBDI:MrNgEngGuanMember

2024-05-31

0001964314

JBDI:SoonAikGlobalPteLtdMember

JBDI:MrNeoChinHengMember

2024-05-31

0001964314

JBDI:KDSSteelPteLtdMember

JBDI:EUHoldingsPteLtdMember

2024-05-31

0001964314

2023-05-30

2023-05-30

0001964314

JBDI:KDSSteelPteLtdMember

JBDI:LogisticsServicesMember

2024-05-31

0001964314

JBDI:KDSSteelPteLtdMember

JBDI:LogisticsServicesMember

2023-05-31

0001964314

JBDI:KDSSteelPteLtdMember

JBDI:LogisticsServicesMember

2022-05-31

0001964314

JBDI:KDSSteelPteLtdMember

JBDI:UtilitiesMember

2024-05-31

0001964314

JBDI:KDSSteelPteLtdMember

JBDI:UtilitiesMember

2023-05-31

0001964314

JBDI:KDSSteelPteLtdMember

JBDI:UtilitiesMember

2022-05-31

0001964314

JBDI:KDSSteelPteLtdMember

JBDI:OtherIncomeForServiceMember

2024-05-31

0001964314

JBDI:KDSSteelPteLtdMember

JBDI:OtherIncomeForServiceMember

2023-05-31

0001964314

JBDI:KDSSteelPteLtdMember

JBDI:OtherIncomeForServiceMember

2022-05-31

0001964314

JBDI:EUHoldingsPteLtdMember

JBDI:ManagementFeesMember

2024-05-31

0001964314

JBDI:EUHoldingsPteLtdMember

JBDI:ManagementFeesMember

2023-05-31

0001964314

JBDI:EUHoldingsPteLtdMember

JBDI:ManagementFeesMember

2022-05-31

0001964314

JBDI:EUHoldingsPteLtdMember

JBDI:ProfessionalFeesMember

2024-05-31

0001964314

JBDI:EUHoldingsPteLtdMember

JBDI:ProfessionalFeesMember

2023-05-31

0001964314

JBDI:EUHoldingsPteLtdMember

JBDI:ProfessionalFeesMember

2022-05-31

0001964314

JBDI:FiltecPrivateLimitedMember

us-gaap:SalesMember

2024-05-31

0001964314

JBDI:FiltecPrivateLimitedMember

us-gaap:SalesMember

2023-05-31

0001964314

JBDI:FiltecPrivateLimitedMember

us-gaap:SalesMember

2022-05-31

0001964314

JBDI:FiltecPrivateLimitedMember

JBDI:UpkeepOfMachineryMember

2024-05-31

0001964314

JBDI:FiltecPrivateLimitedMember

JBDI:UpkeepOfMachineryMember

2023-05-31

0001964314

JBDI:FiltecPrivateLimitedMember

JBDI:UpkeepOfMachineryMember

2022-05-31

0001964314

JBDI:FiltecPrivateLimitedMember

JBDI:UpkeepOfMotorVehiclesMember

2024-05-31

0001964314

JBDI:FiltecPrivateLimitedMember

JBDI:UpkeepOfMotorVehiclesMember

2023-05-31

0001964314

JBDI:FiltecPrivateLimitedMember

JBDI:UpkeepOfMotorVehiclesMember

2022-05-31

0001964314

JBDI:MrNeoChinHengMember

2024-05-31

0001964314

JBDI:MrNgEngGuanMember

2024-05-31

0001964314

JBDI:SoonAikGlobalPteLtdMember

2024-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:CustomerConcentrationRiskMember

JBDI:OneCustomerMember

2023-06-01

2024-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:CustomerConcentrationRiskMember

JBDI:OneCustomerMember

2022-06-01

2023-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:CustomerConcentrationRiskMember

JBDI:OneCustomerMember

2021-06-01

2022-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorAMember

2023-06-01

2024-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorBMember

2022-06-01

2023-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorBMember

2021-06-01

2022-05-31

0001964314

us-gaap:CreditRiskMember

2023-06-01

2024-05-31

0001964314

us-gaap:CreditRiskMember

2024-05-31

0001964314

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

JBDI:SingleCustomerMember

2024-05-31

0001964314

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

JBDI:SingleCustomerMember

2023-05-31

0001964314

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

JBDI:SingleCustomerMember

2022-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorAMember

2024-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorAMember

2022-06-01

2023-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorAMember

2023-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorAMember

2021-06-01

2022-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorAMember

2022-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorBMember

2023-06-01

2024-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorBMember

2024-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorBMember

2023-05-31

0001964314

us-gaap:RevenueFromContractWithCustomerMember

us-gaap:SupplierConcentrationRiskMember

JBDI:VendorBMember

2022-05-31

0001964314

us-gaap:IPOMember

us-gaap:SubsequentEventMember

2024-08-28

2024-08-28

0001964314

us-gaap:IPOMember

us-gaap:SubsequentEventMember

2024-08-28

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

iso4217:SGD

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

20-F

| ☐ |

REGISTRATION

STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ |

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For

the Fiscal Year Ended May 31, 2024

OR

| ☐ |

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☐ |

SHELL

COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission

File Number: 001-42259

JBDI

Holdings Limited

(Exact

name of Registrant as specified in its charter)

Cayman

Islands

(Jurisdiction

of incorporation or organization)

34

Gul Crescent

Singapore

629538

(Address

of principal executive offices)

Mr.

Lim Chwee Poh, Chief Executive Officer and Executive Director

Telephone:

+65 6861 4150

Email:

At

the address of the Company set forth above

(Name,

Telephone, email and/or fax number and address of Company Contact Person)

Securities

registered or to be registered pursuant to Section 12(b) of the Act:

| Title

of each class |

|

Trading

symbol |

|

Name

of each exchange on which registered |

| Ordinary Shares, par

value US$0.0005 per share |

|

JBDI |

|

The Nasdaq Capital Market

LLC |

Securities

registered pursuant to Section 12(g) of the Act: None

Securities

for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate

the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered

by the annual report.

18,037,500

Ordinary Shares, US$0.0005 per share, at May 31, 2024

Indicate

by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933.

Yes

☐ No ☒

If

the report is an annual or transition report, indicate by check mark if the Registrant is not required to file reports pursuant to Section

13 or 15D of the Securities Exchange Act of 1934.

Yes

☐ No ☒

Indicate

by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Yes

☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Yes

☒ No ☐

Indicate

by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth

company.

| Large Accelerated Filer ☐ |

|

Accelerated Filer ☐ |

|

Non-accelerated

filer ☒ |

| |

|

|

|

Emerging Growth Company ☒ |

If

an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant

to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. ☐

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate

by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark which basis of accounting the Registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ |

International Financial Reporting

Standards as issued by the International Accounting Standards Board ☐ |

Other ☐ |

If

“Other” has been checked in response to the previous question, indicate by check mark which financial statement item the

Registrant has elected to follow:

Item

17 ☐ Item 18 ☐

If

this is an annual report, indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange

Act.)

Yes

☐ No ☒

TABLE

OF CONTENTS

SPECIAL

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This

Annual Report on Form 20-F contains forward-looking statements that relate to our current expectations and views of future events. These

forward-looking statements are contained principally in the sections entitled “Risk Factors,” “Management’s Discussion

and Analysis of Financial Condition and Results of Operations,” “Industry Overview” and “Business.” These

statements relate to events that involve known and unknown risks, uncertainties and other factors, including those listed under “Risk

Factors,” which may cause our actual results, performance or achievements to be materially different from any future results, performance

or achievements expressed or implied by the forward-looking statements.

In

some cases, these forward-looking statements can be identified by words or phrases such as “believe”, “plan”,

“expect”, “intend”, “should”, “seek”, “estimate”, “will”, “aim”

and “anticipate”, or other similar expressions, but these are not the exclusive means of identifying such statements. All

statements other than statements of historical facts included in this document, including those regarding future financial position and

results, business strategy, plans and objectives of management for future operations (including development plans and dividends) and

statements on future industry growth are forward-looking statements. In addition, we and our representatives may from time to time make

other oral or written statements which are forward-looking statements, including in our periodic reports that we will file with the SEC,

other information sent to our shareholders and other written materials.

These

forward-looking statements are subject to risks, uncertainties and assumptions, some of which are beyond our control. In addition, these

forward-looking statements reflect our current views with respect to future events and are not a guarantee of future performance. Actual

outcomes may differ materially from the information contained in the forward-looking statements as a result of a number of factors, including,

without limitation, the risk factors set forth in “Risk Factors” and the following:

FINANCIAL

STATEMENTS AND CURRENCY PRESENTATION

Basis

of Presentation

Unless

otherwise indicated, all financial information contained in this Annual Report is prepared and presented in accordance with generally

accepted accounting principles in the United States of America (“U.S. GAAP” or “GAAP”).

Certain

amounts, percentages and other figures included in this Annual Report have been subject to rounding adjustments. Accordingly, amounts,

percentages and other figures shown as totals in certain tables or charts may not be the arithmetic aggregation of those that precede

them, and amounts and figures expressed as percentages in the text may not total 100% or, when aggregated may not be the arithmetic aggregation

of the percentages that precede them.

Financial

Information in U.S. Dollars

Our

reporting currency is the United States Dollar. This Form 20-F also contains translations of certain foreign currency amounts into United

States Dollars for the convenience of the reader. Unless otherwise stated, all translations of Singapore Dollars into United States Dollars

were made at S$1.3509 to US$1.00 for amounts relevant to the financial year ended May 31, 2024 and S$1.3181 to US$1.00 for amounts relevant

to the financial year ended May 31, 2023, in accordance with our internal exchange rate. We make no representation that the Singapore

Dollar or United States Dollar amounts referred to in this Annual Report could have been or could be converted into United States Dollars

or Singapore Dollars, as the case may be, at any particular rate or at all.

Recent

Events

On

August 28, 2024, we completed our initial public offering of 1,750,000 Ordinary Shares at a public offering price of US$5.00 per share

(the “Offering”). Total net proceeds to the Company from the Offering, after deducting discounts, expenses allowance and

expenses, were approximately $6.7 million. The Ordinary Shares began trading on August 27, 2024 on the Nasdaq Capital Market (the “Nasdaq”)

under the trading symbol “JBDI”.

As

of the date of this Annual Report, our Group is comprised of: (i) JBDI Investments Limited, a business company incorporated in the British

Virgin Islands on October 10, 2022 and a direct wholly-owned subsidiary of our Company (“JBDI”); (ii) Jurong Barrels &

Drums Industries Pte. Ltd. (“Jurong Barrels”), a company incorporated in Singapore on September 17, 1983 and a direct wholly-owned

subsidiary of JBDI; and (iii) JBD Systems Pte. Ltd. (“JBD Systems”), a company incorporated in Singapore on May 4, 2017 and

a direct wholly-owned subsidiary of Jurong Barrels. See “Item 4. Information of the Company – Corporate Structure”.

Our

operating subsidiaries are Jurong Barrels and JBD Systems (collectively, the “Operating Subsidiaries”).

PART

I

ITEM

1. IDENTITY OF DIRECTORS, OFFICERS, SENIOR MANAGEMENT AND ADVISORS

Not

Applicable

ITEM

2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not

Applicable

ITEM

3. KEY INFORMATION

A.

RESERVED

B.

CAPITALIZATION AND INDEBTEDNESS

Not

applicable

C.

REASONS FOR THE OFFER AND USE OF PROCEEDS.

Not

applicable

D.

RISK FACTORS

An

investment in our Ordinary Shares is highly speculative and involves a significant degree of risk. The risks discussed below could materially

and adversely affect our business, prospects, financial condition, results of operations, cash flows, ability to pay dividends and the

trading price of our Ordinary Shares. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial

may also materially and adversely affect our business, prospects, financial condition, results of operations, cash flows and ability

to pay dividends, and you may lose all or a part of your investment. The realization of any of the risks described below could have a

material adverse effect on our business, results of operations and future prospects.

Risks

Related to Our Business and Industry

Our

business is inherently susceptible to the cyclical fluctuations of the solvent, chemical, petroleum and edible oil product industries

worldwide and regionally, which our customers are operating in

Our

customers mainly operate in the solvent, chemical, petroleum and edible product oil industries, respectively. These industries are largely

cyclical in nature and economic downturns and resulting pricing pressures experienced by them have resulted in them reducing their capital

and operating expenditures. A slowdown in these industries or the occurrence of any event that may adversely affect these industries

such as changes in regulatory environment and economic conditions will result in a decrease in demand for our products and services,

and accordingly our business, profitability and financial performance may be adversely affected. These industries are also subject to

the impact of the industry cycle, general market and economic conditions and government policies and expenditures, which are factors

beyond our control. A decline in the number of purchase orders or service contracts due to these factors may cause us to operate in a

more competitive environment, and we may also be required to be more competitive in our pricing which, in turn, may adversely impact

our business, financial condition, results of operations and prospects.

We

are affected by regional and worldwide political, regulatory, social and economic conditions in the jurisdictions in which we and our

customers and suppliers operate and in the jurisdictions which we intend to expand our business

We

and our customers and suppliers are governed by the laws, regulations and government policies in each of the various jurisdictions in

which we and our customers and suppliers operate or into which we intend to expand our business and operations. Our business and future

growth are dependent on the political, regulatory, social and economic conditions in these jurisdictions, which are beyond our control.

Any economic downturn, changes in policies, currency and interest rate fluctuations, capital controls or capital restrictions, labor

laws, changes in environmental protection laws and regulations, duties and taxation and limitations on imports and exports in these countries

may materially and adversely affect our business, financial condition, results of operations and prospects.

Generally,

we fund our operations via our internal resources and short and long-term financing from banks and other financial institutions. Any

disruption, uncertainty and volatility in the global credit markets may limit our ability to obtain the required working capital and

financing for our business at reasonable terms and finance costs. If all or a substantial portion of our credit facilities are withdrawn

and we are unable to secure alternative funding on acceptable commercial terms, our operations and financial position will be adversely

affected. The interest rates for most of our credit facilities are subject to review from time to time by the relevant financial institutions.

Given that we rely on these credit facilities to finance our operations and that interest expenses represent a significant percentage

of our expenses, any increase in the interest rates of the credit facilities extended to us may have a material adverse impact on our

profitability.

Our

business is dependent on the general economic conditions in Singapore

Over

80% of our revenue was derived from our customers in Singapore during the financial years

ended May 31, 2024 and 2023. As such, our business is subject to the uncertainties and cyclical nature of the solvent, chemical, petroleum

and edible product oil industries in Singapore as the demand for our products and services is dependent, to a large extent, on the level

of business activities in the solvent, chemical, petroleum and edible product oil industries in Singapore. In particular, our revenue

and profitability may be adversely affected if the demand for solvent, chemical, petroleum and edible product oil products fall. In addition,

an economic downturn in Singapore may lead to a reduction in a numerous range of business activities, thereby leading to a subsequent

decline in demand for solvent, chemical, petroleum and edible product oil products, and this would have an adverse impact on our revenue

and financial performance.

As

our business is dependent on our customers’ demand for our products and services in Singapore and we do not enter into long-term

contracts with our customers, it is critical that we maintain a good relationship with our customers. We cannot assure you that we will

be able to do so. Accordingly, our historical performance may not be an indication of our future performance. In the event that we are

not able to maintain our customers and that we are not able to identify new ones to replace them, there would be an adverse impact on

our financial performance.

We

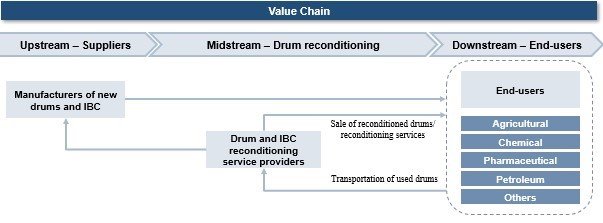

are dependent on the need to continually maintain a wide range of containers which are relevant to our customers’ needs

The

needs and preferences of our customers in terms of types and specifications of containers may change as a result of evolving needs, which

include plastic or metal industrial containers, new or used, with or without covers, caps, valves, handles, external metal frames, including

intermediate bulk containers (the “IBC”), plastic drums, metal drums, open-top drums and plastic carboys with different capacities

(the “Containers”).

Our

future success depends on our ability to obtain used and new Containers that meet evolving market demands of our customers. The preferences

and purchasing patterns of our customers can change rapidly due to developments in their respective industries. There is no assurance

that we will be able to respond to changes in the specifications of our customers in a timely manner. Our success depends on our ability

to adapt our products to the requirements and specifications of our customers. There is also no assurance that we will be able to sufficiently

and promptly respond to changes in customer preferences to make corresponding adjustments to our products or services, and failing to

do so may have a material and adverse effect on our business, financial condition, results of operations and prospects.

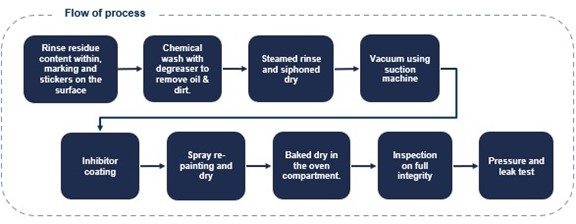

As

we want to ensure a quick turnaround time for our customers, we normally bid and tender for used Containers in bulk and recondition them

in anticipation of the needs of our customers. Reconditioned containers generally are used Containers, which have gone through the process

of: (i) revitalizing through removing their residues and labels; (ii) cleaning interiors and exteriors with vacuum suction, solvents

(such as kerosene, Toluene and degreaser), scrubber machines, high pressure water jets/washing hose shoots and/or specialized machines;

(iii) repainting their exterior; and/or (iv) restoring them through repairs As of May 31, 2024 and 2023 , we had inventories of

approximately $0.3 million and $0.3 million, respectively. Any change in customer demand for our products may have an adverse impact

on our product sales, which may in turn lead to inventory obsolescence, decline in inventory value or inventory write-off. In that case,

our business, financial condition, results of operations and prospects may be materially and adversely affected.

Escalating

steel price may increase our costs and adversely affect our profit margin

Over

70% of our revenue during the financial years ended May 31, 2024 and 2023 was derived from

the sale of Reconditioned and new Containers. The increase in the price of steel will generally lead to an increase in the price of new

steel Containers. As the price of used steel Containers is generally pegged to the price of new steel Containers, the fluctuation in

the price of steel (which is dependent on various factors such as the cost of raw materials, shipping cost, energy prices, demand and

supply) will have a direct impact on our operating costs, which in turn will affect our profit margin. As such, escalating steel price

may increase our costs and adversely affect our profit margin if we are unable to pass on the increase in costs to our customers, which

would have an adverse impact on our revenue and financial performance.

Our

continued success is dependent on our key management personnel and our experienced and skilled personnel and our business may be severely

disrupted if we are unable to retain them or to attract suitable replacements

Since

the commencement of our business, Mr. Lim CP, our Executive Director and Chief Executive Officer and one of our founding shareholders,

has been instrumental in expanding our business and his brother, Mr. Lim KS, has been supporting in sales since inception. His two sons,

namely and Mr. Lim TM and Mr. Lim TC also joined our Group in 1999 and 2003 to look after sales and operations, respectively. We rely

on the wide network, contacts and experience of our Executive Directors, Executive Officers and senior management Mr. Lim CP, Mr. Lim

KS, Mr. Lim TM, Mr. Lim TC, Mr. Liang Zhao Rong and Mr. Quek Che Wah, which was built collectively over four decades, in particular,

sourcing for used and new Containers from new and existing suppliers and sales of Reconditioned and used Containers.

Our

performance depends on the continued service and performance of our Executive Directors, Executive Officers and senior management, and

in particular Mr. Lim CP because he plays an important role in guiding the implementation of our business strategies and future plans.

The working and business relationships that our Executive Directors, Executive Officers and senior management have developed with our

main suppliers and customers over the years is important for the future development of our business. If any of our Executive Directors,

Executive Officers and senior management were to terminate their employment with our Group, there is no assurance that we would be able

to find suitable replacements with such a vast network of contacts and experience in a timely manner. The loss of services of any of

our Executive Directors, Executive Officers and senior management and/or the inability to identify, hire, train and retain other qualified

technical, mechanical and operations personnel in the future may materially and adversely affect our business, financial condition, results

of operations and prospects.

In

addition, although we are dependent on certain key personnel, we do not have any key man life insurance policies on any such individual.

Therefore, if any of our key management personnel dies or become disabled, we will not receive any compensation to assist with such individual’s

absence. The loss of such person could materially and adversely affect our business, financial condition, results of operations and growth

prospects.

We

are reliant on skilled labor

Our

operations are dependent on our ability to recruit and retain experienced and skilled workers, technicians, mechanics and drivers who

are trained and specialized in certain types of Reconditioning and water treatment processes, disposal of industrial wastes or provide

maintenance and repair support services. As there is a limited number of skilled personnel in the industry, competition for experienced

and skilled personnel is intense. In case of a shortage of such skilled labor for any part of our businesses, we may have to increase

their salaries in order to attract and retain their services which will result in an increase in our overall cost of sales and operating

expenses. In the event we are unable to pass on the increase in costs to our customers, our financial performance will be adversely affected.

We

rely on experienced and skilled personnel for our operations and services and our ability to provide good customer care service depends

to a large extent on whether we are able to secure adequately skilled personnel for our operations. If we are unable to employ suitable

personnel, or if our personnel do not fulfil their roles or if we experience a high turnover of experienced and skilled personnel without

suitable, timely or sufficient replacements, the quality of our products and/or services may decline, which may adversely affect our

business, financial condition, results of operations and prospects.

In

addition, the availability of both skilled and unskilled foreign labor is subject to policies imposed by the Ministry of Manpower of

Singapore (the “MOM”). The availability, requirements and costs of housing for such workers are also subject to government

policies. Over 50% of our employees as at May 31, 2024 were foreigner employees, any change in such policies may affect the supply of

foreign manpower and cause disruptions to our operations which will result in an increase in our labor costs and may have a material

adverse impact on our financial performance. Please refer to “Item 4. Information of the Company – Business Operations –

Regulatory Environment” on regulations on employment of foreign workers in Singapore.

We

are susceptible to fluctuations in the prices and quantity of available machineries and vehicles and their parts which are necessary

for our operations

The

operations of our Group are reliant on a lot of machineries and vehicles such as vacuum suction machine and forklifts. Please see “Item

4. Information on the Company – Business Operations” for further description of our machineries and vehicles. We are exposed

to fluctuations in the prices of machineries and vehicles which are necessary for our operations. In the event that we are unable to

source any specific parts required to maintain and service such machineries and vehicles at acceptable prices, or if we face any delays

or shortages in obtaining sufficient quantity of such parts, we may be unable to deliver our products and services in an efficient manner,

which may negatively impact our businesses. Such price fluctuations of machineries and vehicles and shortages and delays in machinery

and vehicle spare parts may have a negative impact on our profitability.

Our

reputation and profitability may be adversely affected if there are major defects or failures in our products or services sold to our

customers

As

our products may be used by our customers to carry toxic materials and/or hazardous substances and our services to our customers involve

the process, disposal and transport of industrial wastes, if there are major defects or failures in our products or services sold to

our customers, it may result in leakage of toxic materials and/or hazardous substances which may result in accidents, casualties as well

as serious environmental impacts, which in turn may lead to protracted legal disputes and damage to our reputation. We may also be subject

to legal and regulatory liabilities such as penalties, sanctions or significant costs and expenses in any dispute as a result of such

defects or failures in our products or services. In addition, the industry we operate in is highly regulated by the National Environment

Agency of Singapore (the “NEA”), the MOM and other regulatory authorities in Singapore. Where there is any non-compliance

of any regulatory requirement of the NEA, the MOM or other regulatory authorities in Singapore, we may be subject to penalties or sanctions

as may be imposed by them. This may have an adverse impact on our operations and financial performance.

We

believe that we have built up goodwill in our “Jurong Barrels” brand and thus customer loyalty over our close to 40 years

of operations. Hence, if there are any major defects or failures in our products or services, such as cracks and holes in our Containers,

negligence by our drivers, frequent breakdowns of our vehicles, or due to circumstances beyond our control resulting in negative publicity,

our reputation may be adversely affected and our customers may lose confidence in our products and services. In such event, our business

and hence our profitability and financial performance may be adversely affected.

Our

reputation and financial performance may be adversely affected if there is prolonged machine or vehicle downtime

Machine

or vehicle downtime occurs when our machine or vehicle is sent for repair and maintenance instead of being deployed for our operations

jobsites. In the event that any of our machineries or vehicle experience prolonged downtime due to repair and maintenance needs, our

operations and/or our services to our customers may be interrupted or delayed which may affect our reputation as well as our financial

performance. Further, newer forms of machineries or vehicles may also be more sophisticated with the incorporation of newer technologies

which makes repair and maintenance of such machineries or vehicles more time consuming. Although our repair and maintenance team are

constantly upgrading their technical skills and know-how to keep up with the advancement of technologies, there is no assurance that

we will be able to minimize the time required for repair and maintenance.

We

are exposed to disputes and claims arising from accidents due to the usage of our products and services

Our

customers mainly operate in the solvent, chemical, petroleum and edible product oil industries and some are a high-risk industries in

which risks of accidents and fatalities are more likely to occur. Claims may be made against us if our products and/or services are involved

in such accidents and/or fatalities on grounds such as cracks, holes or defects in our products and failure to adhere to health and safety

standards by our drivers or forklift operators. In the event that we are required to pay damages arising from disputes, our reputation

and profitability will be adversely affected.

Some

of these accidents may result in damages to property and equipment, personal injury and/or deaths to our employees or third parties.

Although we have sought to minimize the risk of such liabilities by regular servicing and maintenance of our machineries and vehicles,

our stringent internal quality control procedures and obtaining the appropriate and necessary insurance coverage for our operations and

employees, we believe that it is impossible for us to be fully insured against every conceivable risk that we may be exposed to.

If

any accidents are not covered by our insurance policies and claims arising from such accidents are in excess of our insurance coverage

or if any of our insurance claims are contested by any insurance company, we may be required to pay for such compensation, which may

have a material and adverse impact on our financial performance. In addition, the payment by our insurers of such insurance claims may

result in increases in the premiums payable by us for our insurances. This will also increase the costs of our operations and adversely

affect our financial performance.

Increased

competition in the Reconditioned and new Containers sales business in Singapore may affect our ability to maintain our market share and

growth

Our

revenue is mainly generated from the sale of Reconditioned and new Containers. Even though the market is relatively consolidated, our

competitors may possess greater financial resources and more up-to-date machineries with better specifications. They may also offer a

wider range of products and services with greater marketing resources and have a larger customer base.

Entry

of new competitors in the market or market consolidation could also increase the degree of competition within the industry. Our continued

success depends on our ability to compete with our competitors as well as our ability to compete successfully in the future against existing

or potential competitors or to adapt to changes in market conditions and demands. In the event we are unable to compete successfully

against existing or potential competitors or to adapt to changes in market conditions and demands, our business and financial performance

may be adversely affected.

We

maintain good working relationships with our suppliers and customers, and have a wide range of products and services for our customers’

needs. However, there is no assurance that our existing suppliers and customers will continue to work with us. In the event that our

suppliers and customers choose to work with our competitors and/or our experienced and skilled employees choose to join our competitors,

we may be unable to maintain our competitive position and our business, financial condition, results of operations and prospects may

be materially and adversely affected.

Our

business is significantly dependent on our major customers’ needs and our relationships with them. We may be unsuccessful in attracting

new customers

Our

aggregate sales generated from our top five customers amounted to approximately 30% and 31.6% of our revenue for the financial years

ended May 31, 2024 and 2023, respectively. In particular, sales to our largest customer amounted to approximately $1.3 million and

approximately $1.8 million, representing approximately 14.2% and 16.4% of our total revenue for the financial years ended May 31,

2024 and 2023, respectively. Accordingly, our sales would be significantly affected by changes in our relationship with or in the

needs of our major customers, particularly our largest customer, as well as other factors that may affect their purchases from us,

many of which are beyond our control. Any adverse changes in the economic conditions in the markets in which our customers operate

and in their business expansion plans may negatively affect their purchase decisions and result in a reduction in demand for our

products and services.

In

addition, there is generally no long-term commitment from customers for our products and services. If we fail to quote a competitive

price to a customer, or if the quality of our products and/or services does not meet a customer’s specifications or if there is

any disruption to our business relationship with a customer, we may be unable to secure further business from such customer. Any significant

decrease in sales to any of our customers for any reason, including any disruption to our business relationship with them, may materially

and adversely affect our business, financial condition, results of operations and prospects.

We

are exposed to the credit risks of our customers

We

extend credit terms to our customers. Our average accounts receivable turnover days were approximately 66 days and 78 days for the financial

years ended May 31, 2024 and 2023, respectively. Our customers may be unable to meet their contractual payment obligations to us, either

in a timely manner or at all. The reasons for payment delays, cancellations or default by our customers may include insolvency or bankruptcy,

or insufficient financing or working capital due to late payments by their respective customers. While we did not experience any material

order cancellations by our customers during the financial years ended May 31, 2024 and 2023, there is no assurance that our customers

will not cancel their orders and/or refuse to make payment in the future in a timely manner or at all, especially in times of economic

downturns. We may be unable to enforce our contractual rights to receive payment through legal proceedings. In the event we are unable

to collect payments from our customers, we are still obliged to pay our suppliers in a timely manner and thus our business, financial

condition and results of operations may be adversely affected.

We

are dependent on our key suppliers for our supply of Containers

We

have maintained long-standing relationships with a reliable group of suppliers, from whom we source good quality and competitively priced

Containers. Our sale of Containers business is dependent on our ability to obtain a supply of such good quality and reliable Containers

from our suppliers at competitive prices. We consider suppliers that account for more than 10% of our total purchasing as major suppliers.

We are dependent on one such major supplier who accounted for approximately 6.4% and 8.5% of our Group’s total purchases during

the financial years ended May 31, 2024 and 2023, respectively. As we do not have long-term supply contracts with our major suppliers,

and for used Containers, the supply is on an ad-hoc basis as and when they are available for sale, there can be no assurance that we

will have continued access to a sufficient supply of good quality used and new Containers at competitive prices. In the event we are

unable to obtain good quality Containers from our major suppliers at competitive prices, we may have to seek alternative sources from

other suppliers and may be charged higher prices and will be subject to the quality of the equipment purchased from alternative suppliers

whom we are not familiar with. In the event we purchase inferior Containers from such alternative suppliers, our operations, reputation,

profitability and financial performance may be materially and adversely affected.

Our

business is subject to potential supply chain interruptions

We

work with third party logistic providers for the import, export and transportation of our Containers. We depend on such third-party service

providers’ abilities to timely deliver our Containers as part of supply chain logistics. The factors that can potentially adversely

affect our operations include, but are not limited to:

| |

● |

interruptions to our delivery

capabilities; |

| |

● |

failure of third-party

service providers to meet our standards or their commitments to us; |

| |

● |

increasing transportation

costs, shipping constraint or other factors that could impact cost, such as having to find more expensive service providers which

may or may not be readily available; and |

| |

● |

COVID-19 and disruptions

as a result of efforts to control or mitigate the COVID-19 pandemic (such as facility closures, governmental orders, outbreaks and/or

transportation capacity). |

Any

disruption to, or inefficiency in, the supply chain network of our third-party service providers, whether due to geopolitical conflicts,

COVID-19, outbreaks, or other factors, could potentially affect our revenue and profitability. If we fail to manage these risks effectively,

we could potentially experience a material adverse impact to our reputation, financial performance and profitability.

We

may be affected if we are found to be in breach of any lease agreements entered into by us

We

have leased our plant located in Singapore (the “Plant”) from Jurong Town Corporation (“JTC”) up to May 15, 2041

and our warehouse also located in Singapore (the “Warehouse”) from KDS Steel Pte Ltd, (“KDS”), a company incorporated

in Singapore and a direct wholly-owned subsidiary of E U Holdings Pte Ltd, a company incorporated in Singapore (“E U Holdings”),

up to May 31, 2025 and are subject to certain terms and conditions under such lease agreements, such as requirement to obtain approval

from JTC for erecting any structure on the Plant. As such, we may be exposed to regulatory (in the case of the lease from JTC only) and

enforcement risks if we are found to be in breach of any term or condition of our leases agreements. See “Item 4. Information on

the Company – Business Operations – Real Property and Equipment”.

Our

business and operations may be materially and adversely affected in the event of a re-occurrence or a prolonged global pandemic outbreak

of COVID-19

The

global pandemic outbreak of COVID-19 announced by the World Health Organization in early 2020 has caused minimal disruption to our operations

as well as the operations of most of our customers and suppliers, as our businesses are classified as essential services by the Singapore

government which were allowed to operate normally during the lockdown periods. If the development of the COVID-19 outbreak becomes more

severe and/or new variants of COVID-19 evolve to be more transmissible and virulent than the existing strains, this may result in a tightening

of restrictions and regulations on businesses which may impact us and our customers and suppliers. If we or our customers and suppliers

are forced to close down our/their businesses with prolonged disruptions to our/their operations, we may fail to fulfill our orders on

time to our customers, experience a delay or shortage of raw materials, supplies and/or services by our suppliers, or termination of

our orders and contracts by our customers. In addition, if any of our employees are suspected of having contracted COVID-19, some or

all of our employees may be quarantined thus causing a shortage of labor and we will be required to disinfect our workplace and our production

and processing facilities. In such event, our operations may be severely disrupted. If the COVID-19 pandemic is prolonged, it will have

a negative impact on the local, regional and global economy, which will have negative impacts on our customers’ businesses and

hence our businesses will also be affected. All these may have a material and adverse effect on our business, financial condition and

results of operations.

In

addition, tightened travel restrictions by the Singapore or other governments may make it more difficult for us to hire suitable manpower

from overseas jurisdictions. This may lead to a stagnation in our workforce strength, thereby affecting our potential growth as we rely

heavily on skilled labor, which may be a material and adverse effect on our business, financial condition and results of operations.

We

may be affected by an outbreak of other infectious diseases

An

outbreak of infectious diseases such as severe acute respiratory syndrome and avian influenza or new forms of infectious diseases in

the future, such as monkey pox, may potentially affect our operations as well as the operations of our customers and suppliers. In the

event that any of the employees in any of our offices or plants or those of our customers and suppliers is affected by any infectious

disease, we or our customers and suppliers may be required to temporarily shut down our or their offices or plants to prevent the spread

of the diseases. This may have an adverse impact on our revenue and financial performance.

We

are exposed to risks arising from fluctuations of foreign currency exchange rates

Our

reporting currency is Singapore Dollar and a portion of our overseas procurement is denominated in foreign currencies, mainly in United

States Dollars. We may be exposed to foreign currency exchange gains or losses arising from transactions in currencies other than our

reporting currency.

We

may be unable to obtain the necessary licenses, approvals or permits for our operations

As

our business involves the transport, storage, process, use and disposal of toxic materials and/or hazardous substances, various licenses,

approvals and permits are material for our Group’s operation and some of our employees (such as drivers and forklift operators)

are also required to obtain certain permits or certifications. Please refer to the “Item 4. Information of the Company –

Business Operations”. The licenses, approvals and permits are generally subject to conditions stipulated in such licenses, approvals

and permits and/or the relevant laws and regulations under which such licenses and permits are issued. Failure to comply with such conditions,

laws or regulations could result in us being penalized or the revocation or non-renewal of the relevant license, approval or permit.

Accordingly, we have to constantly monitor and ensure our compliance with such conditions imposed, if any. A failure to comply with such

conditions may result in the revocation or non-renewal of any of the relevant licenses, approvals and permits which may impact our ability

to carry out our business and operations. In addition, compliance with changes in government legislation, regulations or policies may

increase our costs and any significant increase in licensing and compliance costs arising from such changes may adversely affect our

financial performance. In such event, our business and profitability would be materially and adversely affected.

We

are subject to environmental, health and safety regulations, and may be adversely affected by new and changing laws and regulations

We

are subject to laws, regulations and policies relating to the protection of the environment and to workplace health and safety. We are

required to adopt measures to control the discharge of polluting matters, wastewater discharge and hazardous substances and noise at

our Plant and Warehouse in accordance with such applicable laws and regulations and to implement such measures that ensure the safety

and health of our employees. Changes to current laws, regulations or policies or the imposition of new laws, regulations and policies

affecting our operations could impose new restrictions or prohibitions on our current practices. We may incur significant costs and expenses

and need to budget additional resources to comply with any such requirements, which may have a material and adverse effect on our business,

financial condition, results of operations and prospects.

Our

insurance policies may be inadequate to cover our assets, operations and any loss arising from business interruptions

We

face the risk of loss or damage to our Plant, Warehouse and our assets due to fire, theft or other natural disasters in Singapore. Such

events may also cause a disruption or cessation in our business operations, and thus may adversely affect our financial results. Our

insurance coverage may not be sufficient to cover all our potential losses. If there are losses which exceed the insurance coverage or

are not covered by our insurance policies, we will remain liable for any liability, debt or other financial obligation related to such

losses. We do not have any insurance coverage for business interruptions.

Due

to the nature of our operations, there is also a risk of accidents occurring either to our employees or to third parties on our premises

and/or on our customers’ premises during the course of operations. In the event that any claims arise in respect of such occurrences

and liability for such claims are attributed to us or that our insurance coverage is insufficient, we may be exposed to losses which

may adversely affect our profitability and financial position.

We

may require additional financing in the future to fund our operations and future growth

We

require financing to fund our operations. In view of the fast-changing business requirements and market conditions, we may be required

to expand our capabilities and business through acquisitions, investments, joint-ventures and/or strategic partnerships with parties

who are able to add value to our business. If such situation arises, we may require additional funds to take advantage of these opportunities.

If

our funding requirements are met by way of additional debt financing, we may be subject to restrictions under such debt financing arrangements

which may:

| |

● |

limit our ability to pay

dividends or require us to seek consent for the payment of dividends; |

| |

● |

increase our vulnerability

to general adverse economic and industry conditions; |

| |

● |

limit our ability to pursue

our growth plans; |

| |

● |

require us to dedicate

a substantial portion of our cash flow from operations to payment for our debt, thereby reducing the availability of our cash flow

to fund other capital expenditure, working capital requirements and other general corporate purposes; or |

| |

● |

limit our flexibility in

planning for, or reacting to, changes in our business and our industry. |

We

may be harmed by negative publicity

We

derive most of our customers through word of mouth and we rely on the positive feedback of our customers. Thus, customer satisfaction

with our products and services is critical to the success of our business as this will also result in potential referrals to new customers

from our existing customers. If we fail to meet our customers’ expectations, there may be negative feedback regarding our products

and/or services, which may have an adverse impact on our business and reputation. In the event we are unable to maintain a high level

of customer satisfaction or any customer dissatisfaction is inadequately addressed, our business, financial condition, results of operations

and prospects may also be adversely affected.

Our

reputation may also be adversely affected by negative publicity in reports, publications such as major newspapers and forums, or any

other negative publicity or rumors. There is no assurance that our Group will not experience negative publicity in the future or that

such negative publicity will not have a material and adverse effect on our reputation or prospects. This may result in our inability

to attract new customers or retain existing customers and may in turn adversely affect our business and results of operations.

If

we are unable to maintain and protect our intellectual property, or if third parties assert that we infringe on their intellectual property

rights, our business could suffer

Our

business depends, in part, on our ability to identify and protect proprietary information and other intellectual property such as our

customer lists and information and business methods. We rely on trade secrets, confidentiality policies, non-disclosure and other contractual

arrangements and copyright and trademark laws to protect our intellectual property rights. However, we may not adequately protect these

rights, and their disclosure to, or use by, third parties may harm our competitive position. Our inability to detect unauthorized use

of, or to take appropriate or timely steps to enforce, our intellectual property rights may harm our business. Also, third parties may

claim that our business operations infringe on their intellectual property rights. These claims may harm our reputation, be a financial

burden to defend, distract the attention of our management and prevent us from offering some products and/or services. Intellectual property

is increasingly stored or carried on mobile devices, such as laptop computers, which increases the risk of inadvertent disclosure if

the mobile devices are lost or stolen and the information has not been adequately safeguarded or encrypted. This also makes it easier

for someone with access to our systems, or someone who gains unauthorized access, to steal information and use it to our disadvantage.

The

war in Ukraine could materially and adversely affect our business and results of operations

The

recent outbreak of war in Ukraine has already affected global economic markets, including a dramatic increase in the price of oil and

gas, and the uncertain resolution of this conflict could result in protracted and/or severe damage to the global economy. Russia’s

recent military interventions in Ukraine have led to, and may lead to, additional sanctions being levied by the United States, European

Union, Singapore and other countries against Russia. Russia’s military incursion and the resulting sanctions could adversely affect

global energy and financial markets and thus could affect our customers’ businesses and our business, even though we do not have

any direct exposure to Russia or the adjoining geographic regions.

In

addition, Russia and Ukraine are major exporters of oil and critical minerals needed by our customers, which could have a significant

negative impact on many of our customers in the various industries as well as the cost of our metal Containers. The extent and duration

of the military action, sanctions and resulting market disruptions are impossible to predict, but could be substantial. Any such disruptions

caused by Russian military action or resulting sanctions may magnify the impact of other risks described in this section. As of the date

of this Annual Report, the war in Ukraine has not had a material or adverse effect upon the Company; however, we cannot predict the progress

or outcome of the situation in Ukraine, as the conflict and governmental reactions are rapidly developing and beyond their control. Prolonged

unrest, intensified military activities or more extensive sanctions impacting the region could have a material adverse effect on the

global economy, including the businesses of our customers, and such effect could in turn have a material adverse effect on our business,

financial condition, results of operations and prospects.

We

are exposed to risks in respect of acts of war, terrorist attacks, epidemics, political unrest, adverse weather conditions and other

uncontrollable events

Unforeseeable

circumstances and other factors such as power outages, labor disputes, adverse weather conditions or other catastrophes, epidemics or

outbreaks may disrupt our operations and cause loss and damage to our Plant and Warehouse, and acts of war, terrorist attacks or other

acts of violence may further materially and adversely affect the global financial markets and consumer confidence. Our business may also

be affected by macroeconomic factors in the countries in which we operate, such as general economic conditions, market sentiment, social

and political unrest and regulatory, fiscal and other governmental policies, all of which are beyond our control. Any such events may

cause damage or disruption to our business, markets, customers and suppliers, any of which may materially and adversely affect our business,

financial condition, results of operations and prospects.

We

may be unable to successfully implement our business strategies and future plans

As

part of our business strategies and future plans, we intend to expand our range of products and services, increase our storage facilities

and capabilities as well as consider potential business opportunities through mergers and acquisitions and joint ventures. While we have

planned such expansion based on our outlook regarding our business prospects, there is no assurance that such expansion plans will be

commercially successful or that the actual outcome of those expansion plans will match our expectations. The success and viability of

our expansion plans are dependent upon our ability to successfully predict the types of Containers which are popular amongst our customers

or potential customers, hire and retain skilled employees to carry out our business strategies and future plans and implement strategic

business development and marketing plans effectively and upon an increase in demand for our products and services by existing and new

customers in the future.

Further,

the implementation of our business strategies and future plans may require substantial capital expenditure and additional financial resources

and commitments. There is no assurance that these business strategies and future plans will achieve the expected results or outcome such

as an increase in revenue that will be commensurate with our investment costs or the ability to generate any costs savings, increased

operational efficiency and/or productivity improvements to our operations. There is also no assurance that we will be able to obtain

financing on terms that are favorable, if at all. If the results or outcome of our future plans do not meet our expectations, if we fail

to achieve a sufficient level of revenue or if we fail to manage our costs efficiently, we may not be able to recover our investment

costs and our business, financial condition, results of operation and prospects may be adversely affect

Risks

Related to Our Securities

There

has been no public market for our Ordinary Shares prior to our Offering. . If an active trading market for our Ordinary Shares does not

develop or continue to develop and the trading price for our Ordinary Shares fluctuates significantly, shareholders may not be able to

resell our Ordinary Shares at any reasonable price.

On

August 28, 2024, we completed our Offering of 1,750,000 Ordinary Shares at a public offering price of US$5.00 per share. The total net

proceeds to the Company from the Offering, after deducting discounts, expenses allowance and expenses, were approximately $6.7 million.

The Ordinary Shares began trading on August 27, 2024 on the Nasdaq under the trading symbol “JBDI”. We cannot assure you

that a liquid public market for our Ordinary Shares will be maintained. If an active public market for our Ordinary Shares is not maintained,

the market price and liquidity of our Ordinary Shares may be materially and adversely affected.

If

we fail to meet applicable listing requirements, Nasdaq may delist our Ordinary Shares from trading, in which case the liquidity and

market price of our Ordinary Shares could decline.

Our

Ordinary Shares are listed on Nasdaq. We cannot assure you, however, that we will be able to meet the continued listing standards of

Nasdaq in the future. If we fail to comply with the applicable listing standards and Nasdaq delists our Ordinary Shares, we and our shareholders

could face significant material adverse consequences, including:

| |

● |

a limited availability

of market quotations for our Ordinary Shares; |

| |

● |

reduced liquidity for our

Ordinary Shares; |

| |

● |

a determination that our

Ordinary Shares are “penny stock,” which would require brokers trading in our Ordinary Shares to adhere to more stringent

rules and possibly result in a reduced level of trading activity in the secondary trading market for our Ordinary Shares; |

| |

● |

a limited amount of news

about us and analyst coverage of us; and |

| |

● |

a decreased ability for

us to issue additional equity securities or obtain additional equity or debt financing in the future. |

The