false

2024

Q2

--12-31

Non-accelerated Filer

0001230058

false

true

NONE

false

false

false

false

false

0001230058

2024-01-01

2024-06-30

0001230058

2024-08-13

0001230058

2024-06-30

0001230058

2023-12-31

0001230058

us-gaap:CommonClassCMember

2024-06-30

0001230058

us-gaap:CommonClassCMember

2023-12-31

0001230058

2024-04-01

2024-06-30

0001230058

2023-04-01

2023-06-30

0001230058

2023-01-01

2023-06-30

0001230058

us-gaap:CommonStockMember

2023-12-31

0001230058

us-gaap:AdditionalPaidInCapitalMember

2023-12-31

0001230058

us-gaap:RetainedEarningsMember

2023-12-31

0001230058

us-gaap:CommonStockMember

2024-03-31

0001230058

us-gaap:AdditionalPaidInCapitalMember

2024-03-31

0001230058

us-gaap:RetainedEarningsMember

2024-03-31

0001230058

2024-03-31

0001230058

us-gaap:CommonStockMember

2022-12-31

0001230058

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001230058

us-gaap:RetainedEarningsMember

2022-12-31

0001230058

2022-12-31

0001230058

us-gaap:CommonStockMember

2023-03-31

0001230058

us-gaap:AdditionalPaidInCapitalMember

2023-03-31

0001230058

us-gaap:RetainedEarningsMember

2023-03-31

0001230058

2023-03-31

0001230058

us-gaap:CommonStockMember

2024-01-01

2024-03-31

0001230058

us-gaap:AdditionalPaidInCapitalMember

2024-01-01

2024-03-31

0001230058

us-gaap:RetainedEarningsMember

2024-01-01

2024-03-31

0001230058

2024-01-01

2024-03-31

0001230058

us-gaap:CommonStockMember

2024-04-01

2024-06-30

0001230058

us-gaap:AdditionalPaidInCapitalMember

2024-04-01

2024-06-30

0001230058

us-gaap:RetainedEarningsMember

2024-04-01

2024-06-30

0001230058

us-gaap:CommonStockMember

2023-01-01

2023-03-31

0001230058

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-03-31

0001230058

us-gaap:RetainedEarningsMember

2023-01-01

2023-03-31

0001230058

2023-01-01

2023-03-31

0001230058

us-gaap:CommonStockMember

2023-04-01

2023-06-30

0001230058

us-gaap:AdditionalPaidInCapitalMember

2023-04-01

2023-06-30

0001230058

us-gaap:RetainedEarningsMember

2023-04-01

2023-06-30

0001230058

us-gaap:CommonStockMember

2024-06-30

0001230058

us-gaap:AdditionalPaidInCapitalMember

2024-06-30

0001230058

us-gaap:RetainedEarningsMember

2024-06-30

0001230058

us-gaap:CommonStockMember

2023-06-30

0001230058

us-gaap:AdditionalPaidInCapitalMember

2023-06-30

0001230058

us-gaap:RetainedEarningsMember

2023-06-30

0001230058

2023-06-30

0001230058

2023-10-01

2023-10-31

0001230058

kanp:SalesOfRealEstateMember

2024-04-01

2024-06-30

0001230058

kanp:SalesOfRealEstateMember

2023-04-01

2023-06-30

0001230058

kanp:SalesOfRealEstateMember

2024-01-01

2024-06-30

0001230058

kanp:SalesOfRealEstateMember

2023-01-01

2023-06-30

0001230058

kanp:CoffeeAndOtherSalesMember

2024-04-01

2024-06-30

0001230058

kanp:CoffeeAndOtherSalesMember

2023-04-01

2023-06-30

0001230058

kanp:CoffeeAndOtherSalesMember

2024-01-01

2024-06-30

0001230058

kanp:CoffeeAndOtherSalesMember

2023-01-01

2023-06-30

0001230058

2014-09-01

2014-09-30

0001230058

srt:MaximumMember

2014-09-01

2014-09-30

0001230058

2024-06-03

0001230058

2024-06-13

0001230058

2022-10-01

2022-10-31

0001230058

2023-09-15

0001230058

2023-09-08

0001230058

2023-09-07

2023-09-08

0001230058

2024-02-25

2024-02-26

0001230058

srt:AffiliatedEntityMember

2024-04-01

2024-06-30

0001230058

srt:AffiliatedEntityMember

2024-01-01

2024-06-30

0001230058

srt:AffiliatedEntityMember

2023-04-01

2023-06-30

0001230058

srt:AffiliatedEntityMember

2023-01-01

2023-06-30

0001230058

kanp:DcDistributionsBankruptcyMember

2014-09-30

0001230058

kanp:PropertyMember

2024-04-01

2024-06-30

0001230058

kanp:PropertyMember

2023-04-01

2023-06-30

0001230058

kanp:PropertyMember

2024-01-01

2024-06-30

0001230058

kanp:PropertyMember

2023-01-01

2023-06-30

0001230058

kanp:AgricultureMember

2024-04-01

2024-06-30

0001230058

kanp:AgricultureMember

2023-04-01

2023-06-30

0001230058

kanp:AgricultureMember

2024-01-01

2024-06-30

0001230058

kanp:AgricultureMember

2023-01-01

2023-06-30

0001230058

us-gaap:CorporateMember

2024-04-01

2024-06-30

0001230058

us-gaap:CorporateMember

2023-04-01

2023-06-30

0001230058

us-gaap:CorporateMember

2024-01-01

2024-06-30

0001230058

us-gaap:CorporateMember

2023-01-01

2023-06-30

0001230058

kanp:PropertyAndAgricultureMember

2024-04-01

2024-06-30

0001230058

kanp:PropertyAndAgricultureMember

2023-04-01

2023-06-30

0001230058

kanp:PropertyAndAgricultureMember

2024-01-01

2024-06-30

0001230058

kanp:PropertyAndAgricultureMember

2023-01-01

2023-06-30

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

utr:acre

kanp:lots

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

[ X ] Quarterly Report pursuant

to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period

ended June 30, 2024

or

[ ] Transition

Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from _______ to __________

Commission file

0-50273

KAANAPALI LAND, LLC

(Exact name of registrant as specified in its

charter)

|

Delaware

(State or other jurisdiction

of incorporation or organization) |

01-0731997

(I.R.S. Employer Identification No.) |

| |

|

|

900 N. Michigan Ave., Chicago, Illinois

(Address of principal executive offices) |

60611

(Zip Code) |

Registrant's telephone number, including area

code: 312-915-1987

Securities registered pursuant to Section 12(b)

of the Act: None

| Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange

on which registered |

| N/A |

|

N/A |

|

N/A |

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934during the preceding 12 months

(or for such a shorter period that registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Yes [ X ] No

[ ]

Indicate by check

mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of

Regulation S-T(§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes [ X ] No

[ ]

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company.

See the definitions of "large accelerated filer," "accelerated filer,""smaller reporting company," and “emerging

growth company” in Rule 12b-2 of the Exchange Act.

| |

Large accelerated filer |

[ ] |

|

Accelerated filer |

[ ] |

|

| |

Non-accelerated filer |

[ X ] |

|

Smaller reporting company |

[ X ] |

|

| |

|

|

Emerging growth company |

[ ] |

|

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No

[ X ]

As of August 13, 2024, the registrant had

1,792,613 Common Shares and 52,000 Class C Shares outstanding. Shares represent membership interests in the Company.

TABLE OF CONTENTS

Part I. Financial Information

Item

1. Financial Statements

KAANAPALI LAND, LLC

Condensed Consolidated Balance Sheets

June 30, 2024 and December 31, 2023

(Dollars in Thousands, except share data)

(Unaudited)

| |

|

|

|

|

|

| |

June 30,

2024 |

|

December 31,

2023 |

| Assets |

| |

|

|

|

|

|

| |

|

|

|

|

|

| Cash and cash equivalents |

$ |

26,001 |

|

$ |

26,260 |

| Property, net |

|

62,025 |

|

|

60,200 |

| Retirement plan investments |

|

4,158 |

|

|

5,067 |

| Other assets |

|

640 |

|

|

1,492 |

| Total assets |

$ |

92,824 |

|

$ |

93,019 |

| |

|

|

|

|

|

| Liabilities |

| |

|

|

|

|

|

| Accounts payable and accrued expenses |

$ |

307 |

|

$ |

346 |

| Deposits and deferred gains |

|

1,006 |

|

|

1,433 |

| Deferred income taxes |

|

5,494 |

|

|

5,979 |

| Other liabilities |

|

2,144 |

|

|

1,550 |

| |

|

|

|

|

|

| Total liabilities |

|

8,951 |

|

|

9,308 |

| |

|

|

|

|

|

| Commitments and contingencies (Note 7) |

|

|

|

|

|

| |

|

|

|

|

|

| Equity |

| |

|

|

|

|

|

|

Common equity, at 6/30/2024 and 12/31/2023

Shares authorized – unlimited, Class C shares

52,000;Common

shares issued and outstanding 1,792,613

at 6/30/2024

and 12/31/2023, Class C shares issued and

outstanding

52,000 at 6/30/2024 and 12/31/2023 |

|

-- |

|

|

-- |

| Additional paid-in capital |

|

5,471 |

|

|

5,471 |

| Accumulated earnings |

|

78,402 |

|

|

78,240 |

| |

|

|

|

|

|

| Total shareholders’ equity |

|

83,873 |

|

|

83,711 |

| |

|

|

|

|

|

| Total liabilities and shareholders’ equity |

$ |

92,824 |

|

$ |

93,019 |

The accompanying notes are an integral part of

the condensed consolidated financial statements.

KAANAPALI LAND, LLC

Condensed Consolidated Statements of Operations

Three and Six Months Ended June 30, 2024 and

2023

(Unaudited)

(Dollars in Thousands, except per share data)

| |

|

|

|

|

|

|

|

|

|

|

|

| |

Three Months Ended

June 30, |

|

Six Months Ended

June 30, |

| |

2024 |

|

2023 |

|

2024 |

|

2023 |

| Revenues: |

|

|

|

|

|

|

|

|

|

|

|

| Sales |

$ |

65 |

|

$ |

1,147 |

|

$ |

224 |

|

$ |

2,300 |

| Interest and other income |

|

358 |

|

|

426 |

|

|

740 |

|

|

768 |

| Total revenues |

|

423 |

|

|

1,573 |

|

|

964 |

|

|

3,068 |

| Cost and expenses: |

|

|

|

|

|

|

|

|

|

|

|

| Cost of sales |

|

606 |

|

|

722 |

|

|

1,268 |

|

|

1,424 |

|

Selling, general and

administrative |

|

2,834 |

|

|

(4,235) |

|

|

4,140 |

|

|

(3,040) |

|

Depreciation and

amortization |

|

52 |

|

|

52 |

|

|

99 |

|

|

104 |

| Total cost and expenses |

|

3,492 |

|

|

(3,461) |

|

|

5,507 |

|

|

(1,512) |

|

Operating income (loss)

before other income and

income taxes |

|

(3,069) |

|

|

5,034 |

|

|

(4,543) |

|

|

4,580 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

Other income:

Insurance proceeds |

|

4,882 |

|

|

-- |

|

|

5,155 |

|

|

-- |

| |

|

4,882 |

|

|

-- |

|

|

5,155 |

|

|

-- |

| |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Income tax benefit (expense) |

|

220 |

|

|

(1,309) |

|

|

387 |

|

|

(1,191) |

| |

|

|

|

|

|

|

|

|

|

|

|

| Net income |

$ |

2,033 |

|

$ |

3,725 |

|

$ |

999 |

|

$ |

3,389 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

Net income per share

- basic and diluted |

$ |

1.10 |

|

$ |

2.02 |

|

$ |

0.54 |

|

$ |

1.84 |

The accompanying notes are an integral part of

the condensed consolidated financial statements.

KAANAPALI LAND, LLC

Condensed Consolidated Statements of Equity

Three and Six Months Ended June 30, 2024

(Unaudited)

(Dollars in Thousands)

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Common

Equity |

|

Additional

Paid-In

Capital |

|

Accumulated

(Deficit)

Earnings |

|

Total

Shareholders’

Equity |

|

Balance December 31, 2023 |

|

$ |

-- |

|

$ |

5,471 |

|

$ |

78,240 |

|

$ |

83,711 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Distribution for retirement plan

contribution for employees of

affiliates under common control |

|

|

-- |

|

|

-- |

|

|

(837) |

|

|

(837) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Net loss |

|

|

-- |

|

|

-- |

|

|

(1,034) |

|

|

(1,034) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance March 31, 2024 |

|

|

-- |

|

|

5,471 |

|

|

76,369 |

|

|

81,840 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Net income |

|

|

-- |

|

|

-- |

|

|

2,033 |

|

|

2,033 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance June 30, 2024 |

|

$ |

-- |

|

$ |

5,471 |

|

$ |

78,402 |

|

$ |

83,873 |

The accompanying notes are an integral part of

the condensed consolidated financial statements.

KAANAPALI LAND, LLC

Condensed Consolidated Statements of Equity

Three and Six Months Ended June 30, 2023

(Unaudited)

(Dollars in Thousands)

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Common

Equity |

|

Additional

Paid-In

Capital |

|

Accumulated

(Deficit)

Earnings |

|

Total

Shareholders’

Equity |

|

Balance December 31, 2022 |

|

$ |

-- |

|

$ |

5,471 |

|

$ |

74,533 |

|

$ |

80,004 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Net loss |

|

|

-- |

|

|

-- |

|

|

(336) |

|

|

(336) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance March 31, 2023 |

|

|

-- |

|

|

5,471 |

|

|

74,197 |

|

|

79,668 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Net income |

|

|

-- |

|

|

-- |

|

|

3,725 |

|

|

3,725 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance June 30, 2023 |

|

$ |

-- |

|

$ |

5,471 |

|

$ |

77,922 |

|

$ |

83,393 |

The accompanying notes are an integral part of

the condensed consolidated financial statements.

KAANAPALI LAND, LLC

Condensed Consolidated Statements of Cash Flows

Six Months Ended June 30, 2024 and 2023

(Unaudited)

(Dollars in Thousands)

| |

|

|

|

|

|

| |

2024 |

|

2023 |

| Net cash provided by (used in) operating activities |

$ |

86 |

|

$ |

(1,963) |

| |

|

|

|

|

|

| Net cash provided by (used in) investing activities: |

|

|

|

|

|

| Property additions |

|

(1,924) |

|

|

(325) |

| Receivable due to sewer line installation |

|

-- |

|

|

(638) |

| Proceeds from insurance |

|

2,416 |

|

|

-- |

| |

|

492 |

|

|

(963) |

| Net cash used in financing activities: |

|

|

|

|

|

|

Distribution for retirement plan contribution for employees

of affiliates under common control |

|

(837) |

|

|

-- |

| |

|

(837) |

|

|

-- |

| |

|

|

|

|

|

| Net decrease in cash and cash equivalents |

|

(259) |

|

|

(2,926) |

| Cash and cash equivalents at beginning of period |

|

26,260 |

|

|

19,815 |

| |

|

|

|

|

|

| Cash and cash equivalents at end of period |

$ |

26,001 |

|

$ |

16,889 |

The accompanying notes are an integral part of

the condensed consolidated financial statements.

KAANAPALI LAND, LLC

Notes to Condensed Consolidated Financial Statements

(Unaudited)

(Dollars in Thousands)

(1) Summary of Significant Accounting

Policies

Basis of Presentation

The accompanying condensed

consolidated financial statements include the accounts of Kaanapali Land, LLC (“Kaanapali Land”) and all of its subsidiaries

and its predecessors (collectively, the “Company”).

The Company's continuing

operations are in two business segments - Agriculture and Property. The Agriculture segment primarily engages in farming, harvesting and

milling operations relating to coffee orchards and also cultivates, harvests and sells bananas and citrus fruits, and engages in certain

ranching operations. The Property segment primarily develops land for sale and negotiates bulk sales of undeveloped land. The Property

and Agriculture segments operate exclusively in the State of Hawaii. For further information on the Company’s business segments

see Note 8.

The accompanying unaudited

condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United

States (“U.S. GAAP”) for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation

S-X promulgated by the U.S. Securities and Exchange Commission (the “SEC”). Accordingly, they do not include all of the information

and footnotes required by U.S. GAAP for complete financial statements, and therefore, should be read in conjunction with the Company's

Annual Report on Form 10-K for the year ended December 31, 2023 (“2023 Form 10-K”). These unaudited condensed consolidated

financial statements include all normal and recurring adjustments considered necessary for a fair presentation of the financial position

and results of operations and cash flows for interim periods in accordance with U.S. GAAP.

A description of the Company’s

significant accounting policies is included in Note 1 to the Notes to the Consolidated Financial Statements included in the 2023 Form

10-K. Except as noted below, there were no material changes in the Company’s significant accounting policies during the three and

six months ended June 30, 2024.

Property

The Company's significant

property holdings are on the island of Maui and consist of approximately 3,900 acres, of which approximately 1,500 acres are classified

as conservation land, which precludes development. The Company has determined, based on its current projections for the development and/or

disposition of its property holdings, that the property holdings are not currently recorded in an amount in excess of proceeds that the

Company expects that it will ultimately obtain from the operation and disposition thereof.

Inventory of land held for sale,

if any, is carried at the lower of cost or fair market value, less costs to sell, which is based on current and foreseeable market conditions,

discussions with real estate brokers and review of historical land sale activity fair value hierarchy (Levels 2 and 3). Land is currently

utilized for commercial specialty coffee farming operations which also support the Company's land development program, as well as farming

bananas, citrus and other farm products and ranching operations. Additionally, miscellaneous parcels of land have been leased or licensed

to third parties on a short term basis prior to the Lahaina wildfire, as discussed below.

Beginning on August 8, 2023,

a wildfire occurred due east of historic Lahaina town in Maui. The fire spread rapidly due to extreme wind conditions caused in part by

Hurricane Dora which traveled 800 miles offshore west of Maui. The fires caused multiple fatalities, widespread damage to Lahaina town

and the surrounding area including the Company’s 19-acre Pioneer Mill site. The Company’s offices and coffee mill were located

on the site as well as various other structures, including a building which was leased to an unrelated third party and used to operate

a coffee store. The Company also utilized portions of the property for short term license agreements with third parties that generated

income for the Company. Although no employees were injured in the fire, the Company’s offices and coffee store building were destroyed.

Additionally, most of the personal property of the licensees and the coffee mill was destroyed. The widespread destruction is likely to

cause disruptions in the Company’s development plans. The damage to the coffee mill has disrupted operations and prevented the Company

from processing and selling the 2023 year coffee crop. It is also likely that the fires and devastation caused thereby will adversely

affect the long-term Maui economy and businesses operated on Maui. Clean up of Lahaina town, including the Pioneer Mill Site, has commenced

by U.S. Army Corps of Engineers (“USACE”) contractors. Access to the property remains restricted, and such restrictions are

expected to continue while the clean-up of Lahaina town continues, estimated by USACE to be completed in the first quarter of 2025. The

Company has initiated claims with its insurance carriers. In October 2023, the Company received an initial, unallocated advance payment

of $1,000 and in June 2024, the Company received $4,882, from its insurance carrier. The $4,882 is recorded within insurance proceeds

in the consolidated statement of operations for the three and six months ended June 30, 2024. Although the Company currently expects

that the Company’s insurance coverage will compensate the Company for the majority of its losses incurred in connection with the

fire and related devastation, including the costs of its structures and equipment lost in the fire, the loss in revenue from the lack

of coffee sales, and the loss of income from the licensees, there can be no assurances the Company will be fully compensated for such

losses. The Company could experience losses in excess of our insured limits, and further, claims for certain losses could be denied or

subject to deductibles or exclusions under our insurance policies. The Company has relocated its offices to temporary office facilities

located on its lands in Kaanapali and is in the planning stages of relocating its coffee mill to its farm in Kaanapali. Recovery efforts

continue.

The Company reviews its property

for impairment of value if events or circumstances indicate that the carrying amount of its property may not be recoverable. Such reviews

contain uncertainties due to assumptions and judgments considering certain indicators of impairment such as significant changes in asset

usage, significant deterioration in the surrounding economy or environmental problems.

Provisions for impairment losses

related to long-lived assets, if any, are recognized when expected future cash flows are less than the carrying values of the assets.

If indicators of impairment are present, the Company evaluates the carrying value of the related long-lived assets in relation to the

future undiscounted cash flows of the underlying operations or anticipated sales proceeds. The Company adjusts the net book value of property

to fair value if the sum of the expected undiscounted future cash flow or sales proceeds is less than book value. Assets held for sale

are recorded at the lower of the carrying value of the asset or fair value less costs to sell.

As a result of the fires, the

Company performed an impairment evaluation of its asset groups to determine if provisions for impairment losses should be recognized.

Based on the evaluation and continued monitoring, the Company concluded a provision for impairment should not be recognized for the current

period. The Company will continue to monitor and evaluate the indicators for evidence of impairment in future periods. There can be no

assurance that future impairment testing will not indicate that impairment has occurred and that a provision for impairment will be required.

Use of Estimates

The preparation of financial

statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the amounts reported in the

financial statements and accompanying notes. Actual results could differ from those estimates.

Operating results for the

six months ended June 30, 2024 are not necessarily indicative of the results that may be achieved for the full year ending December 31,

2024 or in any other future periods.

Cash and Cash Equivalents

The Company considers as

cash equivalents all investments with maturities of three months or less when purchased. Included in this balance as of June 30,

2024 is a money market fund for $20,100 that is considered to be a fair value hierarchy Level 1 investment. The Company’s cash balances

are maintained primarily in two financial institutions. Such balances significantly exceed the Federal Deposit Insurance Corporation insurance

limits. Management does not believe the Company is exposed to significant risk of loss on cash and cash equivalents.

Subsequent Events

The Company has performed an evaluation

of subsequent events from the date of the financial statements included in this quarterly report through the date of its filing with the

Securities and Exchange Commission.

Revenue Recognition

Revenue from real property

sales is recognized at the time of closing when control of the property transfers to the buyer. After closing of the sale transaction,

the Company has no remaining performance obligation.

Other revenues are recognized

when control of goods or services transfers to the customers, in the amount that the Company expects to receive for the transfer of goods

or provision of services.

Revenue recognition standards

require entities to recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the

consideration to which the entity expects to be entitled to receive in exchange. The revenue recognition standards have implications for

all revenues, excluding those that are under the specific scope of other accounting standards.

The Company’s revenues

that were subject to revenue recognition standards were as follows (in thousands):

| |

Three Months Ended

June 30, |

|

Six Months Ended

June 30, |

| |

2024 |

|

2023 |

|

2024 |

|

2023 |

| Sales of real estate |

$ |

-- |

|

$ |

-- |

|

$ |

-- |

|

$ |

-- |

| Coffee and other sales |

|

19 |

|

|

860 |

|

|

119 |

|

|

1,715 |

| Total |

$ |

19 |

|

$ |

860 |

|

$ |

119 |

|

$ |

1,715 |

The revenue recognition standards

require the use of a five-step model to recognize revenue from customer contracts. The five-step model requires that the Company

(i) identify the contract with the customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction

price, including variable consideration to the extent that it is probable that a significant future reversal will not occur,

(iv) allocate the transaction price to the respective performance obligations in the contract, and (v) recognize revenue when (or as)

the Company satisfies the performance obligation.

Lease Accounting

The Company’s lease arrangements,

both as lessor and as lessee, are short-term leases. The Company leases land to tenants under operating leases, and the Company leases

property, primarily office and storage space, from lessors under operating leases. During the three and six months ended June 30,

2024, the Company recognized $46 and $105, respectively, and $287 and $585 during the three and six months ended June 30, 2023, respectively,

of lease income, substantially comprised of non-variable lease payments. During the three and six months ended June 30, 2024, the

Company recognized $32 and $58, respectively, and during the three and six months ended June 30, 2023, recognized $26 and $49, respectively,

of lease expense, substantially comprised of non-variable lease payments.

Recently Issued Accounting

Pronouncements

In October 2023, the

Financial Accounting Standards Board (the “FASB”) issued Accounting Standards Update (“ASU”) No. 2023-06 (“ASU

2023-06”), Disclosure Improvements - Codification Amendment in Response to the SEC’s Disclosure Update and Simplification

Initiative. This ASU modified the disclosure and presentation requirements of a variety of codification topics by aligning them with the

SEC’s regulations. The amendments to the various topics should be applied prospectively, and the effective date will be determined

for each individual disclosure based on the effective date of the SEC’s removal of the related disclosure. If the SEC has not removed

the applicable requirements from Regulation S-X or Regulation S-K by June 30, 2027, then this ASU will not become effective. Early adoption

is prohibited. While the Company is currently evaluating the effect that implementation of this update will have on its consolidated financial

statements, no significant impact is anticipated.

In November 2023, the FASB

issued ASU No. 2023-07 (“ASU 2023-07”), Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures to improve

reportable segment disclosure requirements, primarily through enhanced disclosures about significant segment expenses. In addition, the

amendments in the ASU enhance interim disclosure requirements, clarify circumstances in which an entity can disclose multiple segment

measures of profit or loss, provide new segment disclosure requirements for entities with a single reportable segment, and contain other

disclosure requirements. ASU 2023-07 is effective for fiscal years beginning after December 15, 2023, and interim periods within fiscal

years beginning after December 15, 2024, and requires retrospective application to all prior periods presented in the financial statements.

Early adoption is permitted. While the Company is currently evaluating the effect that implementation of this update will have on its

consolidated financial statements, no significant impact is anticipated.

In December 2023, the FASB

issued ASU No. 2023-09 (“ASU 2023-09”), Income Taxes (Topic 740): Improvement to Income Tax Disclosures to enhance the transparency

and decision usefulness of income tax disclosures, primarily related to the rate reconciliation and income taxes paid information. ASU

2023-09 is effective for annual periods beginning after December 15, 2024, on a prospective basis. Early adoption is permitted. While

the Company is currently evaluating the effect that implementation of this update will have on its consolidated financial statements,

no significant impact is anticipated.

(2) Land Development

In September 2014, Kaanapali Land

Management Corp. (“KLMC”), pursuant to a property and option purchase agreement (“Purchase Agreement”) with Newport

Hospital Corporation (“NHC”), sold a parcel of approximately 14.9 acres in West Maui. The Purchase Agreement included an Infrastructure

Improvement Agreement (as subsequently amended) which commits KLMC to fund up to $583, depending on various factors, for off-site roadway,

sewer and electrical improvements that will also provide service to other KLMC properties. KLMC may, at its discretion, design, construct,

install, and complete all or portions of the off-site road, sewer and/or electrical improvements, in which case the developer shall pay

to KLMC the total costs thereof, less the KLMC committed amount. In relation to such sewer line improvement, KLMC entered into a contract

for $1,137, as amended, to install the sewer line. KLMC paid $1,108 on the contract which has been recorded as a receivable, less KLMC’s

sewer line commitment of $208. In accordance with the Infrastructure Improvement Agreement, the receivable accrues interest of 6.5% and

is secured by the 14.9 acre property. Due to the receipt of a Demand for Arbitration, discussed in Note 6 Commitments and Contingencies

as of June 30, 2024, the Company recorded a $953 credit loss reserve on its receivable with NHC based on its evaluation of the probability

of default that exists at NHC. The amount of the credit loss reserve represents the entire receivable amount and interest incurred as

of June 30, 2024. The provision for credit loss reserve is recorded within selling, general and administrative expenses in the consolidated

statement of operations for the three and six months ended June 30, 2024. In conjunction with the Infrastructure Improvement Agreement,

the Company retains certain approval rights relating to the uses and designs of the site to ensure the uses and designs are aligned with

the Company's planned master development. If such uses result in a dispute with the developer of the site, development of the site could

be delayed. The 14.9 acre site is intended to be used for a critical access hospital, skilled nursing facility, assisted living facility,

and independent living facility.

On June 3, 2024, KLMC entered into a property

sale agreement (“PVM Sales Agreement”) with an unrelated third party for the sale of several parcels of land, aggregating

approximately 241 acres (the “PVM land parcels”) within Pu’ukoli’i Village Mauka located near the Kaanapali resort

area, north of Lahaina, Hawaii. Pursuant to the PVM Sales Agreement, the base sales price for the PVM land parcels is $29,900, and

the closing of the sale of the PVM land parcels is subject to a due diligence period of one hundred days, subject to a one-time extension.

In addition, the developer has the right to terminate the PVM Sales Agreement on or before the expiration of the due diligence period.

Accordingly, there can be no assurance the sale of the PVM land parcels will be completed under the existing or any other terms of the

PVM Sales Agreement, if at all.

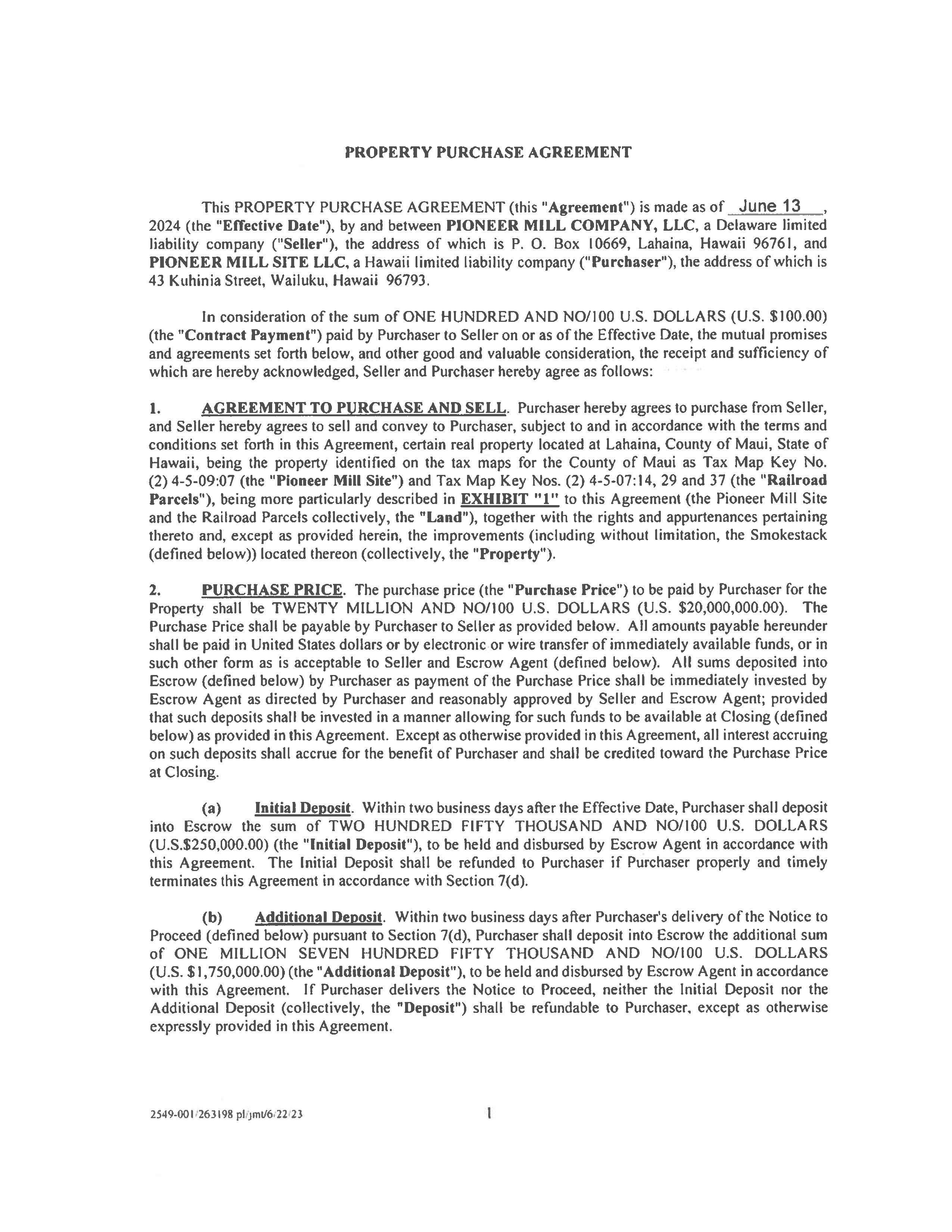

On June 13, 2024, Pioneer Mill

Company, LLC. (“PMC”), entered into a property sale agreement (“PMC Sales Agreement”) with an unrelated third

party for the sale of four parcels of land, aggregating approximately 20 acres (the “PMS land parcels”) located in Lahaina,

Hawaii. Pursuant to the PMC Sales Agreement, the sales price for the PMS land parcels is $20,000, and the closing of the sale of the PMS

land parcels is subject to the due diligence period. The developer has the right to terminate the PMC Sales Agreement depending on various

factors. As the PMC Sales Agreement is subject to certain conditions, there can be no assurance that the sale of the PMS land parcels

will be completed under the existing or any other terms of the PMC Sales Agreement, if at all.

(3) Retirement Plan Investments

Prior to June 1, 2022,

the Company participated in a defined benefit pension plan (the “Pension Plan”) that covered substantially all of its eligible

employees. The Pension Plan was sponsored and maintained by Kaanapali Land in conjunction with other plans providing benefits to employees

of Kaanapali Land and its affiliates.

Pacific Trail Holdings LLC, the

manager of the Company, adopted a plan to freeze the benefit accruals under and close participation in the Pension Plan and terminate

the Pension Plan on June 1, 2022. Effective February 7, 2022, the fair value hierarchy Level 1 and Level 2 plan asset investments were

reallocated to a money market fund. Benefit accruals were frozen on March 31, 2022. The Company paid lump sum benefits totaling approximately

$420 to Pension Plan participants during October 2022, thereby settling all benefit Pension Plan liabilities. The remaining assets of

the terminated Pension Plan of approximately $14,500 reverted to the Company on September 15, 2023.

On September 8, 2023, the Company

transferred $5,000 which was approximately 25% of the Pension Plan assets to a qualified replacement plan (“QRP”). The Company’s

contribution to the QRP enabled the Company to reduce the excise tax due as a result of the Pension Plan termination from 50% to 20% of

the amount reverted to the Company. The Company paid the 20% excise tax of approximately $2,900 in October 2023. In accordance with U.S.

GAAP, the amount transferred to the QRP is reflected as Retirement plan investments on the Company’s consolidated balance sheet

as of June 30, 2024. Such assets are considered to be a fair value hierarchy Level 1 investment, and are maintained in a suspense

account within the QRP pending allocation to plan participants. The assets will be allocated to the participants in the QRP who were participants

in the terminated Pension Plan and the employees of certain affiliates, all of which have some degree of common ownership with the Company

and were concluded as eligible participants per the Employee Retirement Income Security Act (“ERISA”) requirements for QRPs.

Such allocations are planned to be allocated ratably over a period not to exceed seven years to comply with regulatory requirements. On

February 26, 2024, approximately $1,019 was allocated to the participants in the QRP. Approximately $182 was allocated to participants

in the terminated Pension Plan and is reflected in general and administrative expenses in the consolidated statement of operations for

the six months ended June 30, 2024 and approximately $837 was allocated to employees of affiliated companies and is reflected as

a distribution from accumulated earnings on the consolidated balance sheet as of June 30, 2024.

The Company maintains a nonqualified

deferred compensation arrangement (the "Rabbi Trust") which provides certain former directors of Amfac Hawaii, LLC (now known

as KLC Land Company, LLC, a direct subsidiary of Kaanapali Land through which the Company conducts substantially all of its operations)

and their spouses with pension benefits. The deferred compensation liability of $244 is included in Other liabilities in the Company's

condensed consolidated balance sheet as of June 30, 2024.

(4) Income Taxes

The Company's taxes for 2020

and more recent years remain open to examinations by tax authorities, subject to possible utilization of loss carryforwards from earlier

years. Notwithstanding the foregoing, all net operating losses (“NOL”) generated and not yet utilized are subject to adjustment

by the Internal Revenue Service (“IRS”). The Company believes adequate provisions for income tax have been recorded for all

years, although there can be no assurance that such provisions will be adequate. To the extent that there is a shortfall, any such shortfall

for which the Company is liable could adversely and materially affect the Company’s results of operations.

The Tax Cuts and Jobs Act of 2017

is a comprehensive tax reform bill containing a number of other provisions that either currently or in the future could impact the Company,

particularly the effect of certain limitations effective for the tax year 2018 and forward (prior losses remain subject to the prior 20

year carryforward period) on the use of federal NOL carryforwards, which will generally be limited to being used to offset 80% of future

annual taxable income.

(5) Transactions with Affiliates

An affiliated insurance agency,

JMB Insurance Agency, Inc., which has some degree of common ownership with the Company, earns insurance brokerage commissions in connection

with providing the placement of insurance coverage for certain of the properties and operations of the Company. Commissions paid for the

three and six months ended June 30, 2024 were $25 and $25, respectively, and $23 and $23 for the three and six months ended June 30,

2023, respectively.

The Company reimburses its affiliates

for general overhead expense and for direct expenses incurred on its behalf, including salaries and salary-related expenses incurred in

connection with the management of the Company's operations. Generally, the entity that employs the person providing the services receives

the reimbursement. Substantially all of such reimbursable amounts were incurred by JMB Realty Corporation or its affiliates, 900FMS, LLC,

900Work, LLC, and JMB Financial Advisors, LLC, all of which have some degree of common ownership with the Company. The total costs recorded

in cost of sales and selling, general and administrative expenses in the consolidated statement of operations for the three and six months

ended June 30, 2024 and 2023 were $356 and $302, respectively, and $654 and $565, respectively, all of which was paid as of June 30,

2024.

The Company maintains a suspense

account within the QRP pending allocation to the employees of certain affiliates, all of which have some degree of common ownership with

the Company and were concluded as eligible participants per ERISA requirements for QRPs. The total allocation of $837, which occurred

during the first quarter of 2024, was recorded as a reduction in accumulated earnings in the consolidated balance sheet as of June 30,

2024. Reference is made to Footnote 3 for discussion regarding the QRP.

(6) Commitments and Contingencies

Material legal proceedings

of the Company are described below. Unless otherwise noted, the parties adverse to the Company in the legal proceedings described below

have not made a claim for damages in a liquidated amount and/or the Company believes that it would be speculative to attempt to determine

the Company's exposure relative thereto, and as a consequence believes that an estimate of the range of potential loss cannot be made.

A subsidiary of the Company, D/C

Distribution Corporation (“D/C”) was substantially without assets and was unable to obtain additional sources of capital to

satisfy its liabilities, and therefore filed with the United States Bankruptcy Court, Northern District of Illinois, its voluntary petition

for liquidation under Chapter 7 of Title 11, United States Bankruptcy Code in July 2007, Case No. 07-12776. Such filing was not expected

to have a material adverse effect on the Company as D/C was substantially without assets at the time of the filing. Kaanapali Land filed

claims in the D/C bankruptcy that aggregated approximately $26,800, relating to both secured and unsecured intercompany debts owed by

D/C to Kaanapali Land.

At the time of the filing of the

bankruptcy petition, Kaanapali Land, as successor by merger to other entities, and D/C had been named as defendants in personal injury

actions allegedly based on exposure to asbestos. While there were relatively few cases that name Kaanapali Land, there were a substantial

number of cases that were pending against D/C on the U.S. mainland (primarily in California). Cases against Kaanapali Land (hereafter,

“Kaanapali Land asbestos cases”) were allegedly based on its prior business operations in Hawaii and cases against D/C were

allegedly based on sale of asbestos-containing products by D/C's prior distribution business operations primarily in California. Each

entity defending these cases believes that it has meritorious defenses against these actions, but can give no assurances as to the ultimate

outcome of these cases. The defense of these cases had a material adverse effect on the financial condition of D/C as it has been forced

to file a voluntary petition for liquidation as discussed above. Kaanapali Land does not believe that it has liability, directly or indirectly,

for D/C's obligations in those cases. Kaanapali Land does not presently believe that the cases in which it is named will result in any

material liability to Kaanapali Land; however, there can be no assurance in that regard.

On January 21, 2020, certain asbestos

claimants filed a Stay Relief Motion (“motion to lift stay”) in connection with the D/C proceeding. The motion to lift stay

sought the entry of an order, among other things, modifying the automatic stay in the D/C bankruptcy to permit those claimants to prosecute

various lawsuits in state courts against D/C and to recover on any judgment or settlement solely from any available insurance coverage.

Various oppositions to the motion to lift stay were filed, and the matter was heard and taken under advisement in April 2020. On July 21,

2020, the bankruptcy court issued an order granting the motion to lift stay to permit the movants to pursue their claims and to recover

any judgment or settlement from and to the extent of any available insurance coverage of D/C only.

Certain asbestos-related proofs

claims in the bankruptcy case were withdrawn in connection with the closing of the case. A court hearing was held on March 29, 2023

in which the court awarded the trustee’s compensation and expenses and therefore D/C no longer has any assets. On June 6, 2023,

the bankruptcy trustee filed a final account and application to close the D/C bankruptcy and on June 14, 2023, the D/C bankruptcy

court closed the case and the trustee was discharged. Due to the closing of the case, the Company derecognized a related contingent liability.

The derecognition of the contingent liability is included as a reduction of selling, general and administrative expenses and resulted

in a credit in expenses on the Company’s consolidated statement of operations for the three and six months ended June 30, 2023.

However, personal injury claimants may in the future assert asbestos-related claims against D/C.

The Company has received notice

from Hawaii’s Department of Land and Natural Resources (“DLNR”) that DLNR on a periodic basis would inspect all significant

dams and reservoirs in Hawaii, including those maintained by the Company on Maui in connection with its agricultural operations. A series

of such inspections have taken place over the period from 2006 through the most recent inspections that occurred in July 2024. To date,

the DLNR has cited certain deficiencies concerning two of the Company’s reservoirs relating to dam and reservoir safety standards

established by the State of Hawaii. These deficiencies include, among other things, vegetative overgrowth, erosion of slopes, uncertainty

of inflow control, spillway capacity, and freeboard, and uncertainty of structural stability under certain loading and seismic conditions.

The Company does not expect that additional deficiencies will be cited as a result of the most recent inspection. The Company has taken

certain corrective actions, including lowering the reservoir operating level, as well as updating plans to address emergency events and

basic operations and maintenance. In 2018, the Company contracted with an engineering firm to develop plans to address certain DLNR cited

deficiencies on one of the Company’s reservoirs. Remediation plans for addressing all deficiencies have been submitted to DLNR.

In 2012, the State of Hawaii issued new Hawaii Administrative Rules

for Dams and Reservoirs which require dam owners to

obtain from DLNR Certificates of Impoundment (“permits”) to operate and maintain dams or reservoirs. Obtaining such permits

requires owners to completely resolve all cited deficiencies. Therefore, the process may involve further analysis of dam and reservoir

safety requirements, which will involve continuing engagement with specialized engineering consultants, and ultimately could result in

significant and costly improvements which may be material to the Company.

The DLNR categorizes the

reservoirs as "high hazard" under State of Hawaii administrative rules and state statutes concerning dam and reservoir safety.

This classification, which bears upon government oversight and reporting requirements, may increase the cost of managing and maintaining

these reservoirs materially. The Company does not believe that this classification is warranted for either of the reservoirs and has initiated

a dialogue with DLNR in that regard. In April 2008, the Company received further correspondence from DLNR that included the assessment

by their consultants of the potential losses that result from the failure of these reservoirs. In April 2009, the Company filed a written

response to DLNR to correct certain factual errors in its report and to request further analysis on whether such "high hazard"

classifications are warranted. It is unlikely that the “high hazard” designation will be changed.

On August 5, 2024, NHC served

KLMC with a Demand for Arbitration administrated by Dispute Prevention and Resolution, Inc., relating to the Infrastructure Improvement

Agreement and NHC’s development of the site. NHC alleges, among other things, that KLMC wrongfully caused significant delays, increased

costs and related damages to NHC with respect to NHC’s planning and construction of the infrastructure improvements required of

NHC under the Infrastructure Improvement Agreement (as subsequently amended). NHC seeks judgment for declaratory relief that the Infrastructure

Improvement Agreement between NHC and KLMC is void; in the alternative, for reformation of the Infrastructure Improvement Agreement;

for award of damages in an amount to be proven at arbitration; for attorneys’ fees and costs; for prejudgment and post-judgment

interest on any monetary award; and for such other and further relief as the arbitrator deems appropriate. KLMC is in the early stages

of assessing the complaint and intends to vigorously defend. However, there can be no assurance that the eventual outcome of the arbitration

will not result in any material liability or have a material impact on business and financial results for KLMC.

Other than as described above,

the Company is not involved in any material pending legal proceedings, other than ordinary routine litigation incidental to its business.

The Company and/or certain of its affiliates have been named as defendants in several pending lawsuits. While it is impossible to predict

the outcome of such routine litigation that is now pending (or threatened) and for which the potential liability is not covered by insurance,

the Company is of the opinion that the ultimate liability from any of this litigation will not materially adversely affect the Company's

consolidated results of operations or its financial condition.

The Company often seeks insurance

recoveries under its policies for costs incurred or expected to be incurred for losses or claims under which the policies might apply.

As a result of the Lahaina wildfire, in October 2023, the Company received an initial, unallocated advance payment of $1,000 from its

insurance carrier. In June 2024, the Company also received an insurance payment of $4,882, which is recorded within insurance proceeds

in the consolidated statement of operations for the three and six months ended June 30, 2024. Reference is made to Note 1, Property,

for further discussion regarding the Lahaina wildfire.

KLMC is a party to an agreement

with the State of Hawaii for the development of the Lahaina Bypass Highway. Approximately 2.4 miles of this two lane state highway have

been completed. Construction to extend the southern terminus was completed mid-2018. The northern portion of the Lahaina Bypass Highway,

which extends to KLMC’s lands, is in the early stage of planning. Under certain circumstances, which have not yet occurred, KLMC

remains committed for approximately $1,100 of various future costs relating to the planning and design of the uncompleted portion of the

Lahaina Bypass Highway. Under certain conditions, which have not yet been met, KLMC has agreed to contribute an amount not exceeding $6,700

toward construction costs. Any such amount contributed would be reduced by the value of KLMC’s land actually contributed to the

State for the Lahaina Bypass Highway.

These potential commitments have

not been reflected in the accompanying condensed consolidated financial statements. While the completion of the Lahaina Bypass Highway

would add value to KLMC’s lands north of the town of Lahaina, there can be no assurance that it will be completed or when any future

phases will be undertaken.

(7) Calculation of Net Income (Loss)

Per Share

The following tables set

forth the computation of net income (loss) per share - basic and diluted:

| |

Three Months Ended

June 30, |

|

Six Months Ended

June 30, |

| |

(Amounts in thousands, except per share amounts) |

| |

2024 |

|

2023 |

|

2024 |

|

2023 |

| Numerator: |

|

|

|

|

|

|

|

|

|

|

|

| Net income |

$ |

2,033 |

|

$ |

3,725 |

|

$ |

999 |

|

$ |

3,389 |

| |

|

|

|

|

|

|

|

|

|

|

|

| Denominator: |

|

|

|

|

|

|

|

|

|

|

|

|

Number of weighted

average shares outstanding |

|

|

|

|

|

|

|

|

|

|

|

| - basic and diluted |

|

1,845 |

|

|

1,845 |

|

|

1,845 |

|

|

1,845 |

| |

|

|

|

|

|

|

|

|

|

|

|

| Net income per share |

|

|

|

|

|

|

|

|

|

|

|

| - basic and diluted |

$ |

1.10 |

|

$ |

2.02 |

|

$ |

0.54 |

|

$ |

1.84 |

(8) Business Segment Information

As described in Note 1, the

Company operates in two business segments. Total revenues and operating profit by business segment are presented in the tables below.

Total revenues by business

segment includes primarily (i) sales, all of which are to unaffiliated customers, and (ii) interest income that is earned from outside

sources on assets which are included in the individual industry segment's identifiable assets.

Operating income (loss) is

comprised of total revenue less cost of sales and operating expenses. In computing operating income (loss), none of the following items

have been added or deducted: general corporate revenues and expenses, interest expense and income taxes.

| |

Three Months Ended

June 30,

(in thousands) |

|

Six Months Ended

June 30,

(in thousands) |

| |

2024 |

|

2023 |

|

2024 |

|

2023 |

| Revenues: |

|

|

|

|

|

|

|

|

|

|

|

| Property |

$ |

62 |

|

$ |

107 |

|

$ |

116 |

|

$ |

299 |

| Agriculture |

|

33 |

|

|

1,050 |

|

|

162 |

|

|

2,064 |

| Corporate |

|

328 |

|

|

416 |

|

|

686 |

|

|

705 |

| |

$ |

423 |

|

$ |

1,573 |

|

$ |

964 |

|

$ |

3,068 |

| |

|

|

|

|

|

|

|

|

|

|

|

| Operating income (loss): |

|

|

|

|

|

|

|

|

|

|

|

| Property |

$ |

(1,449) |

|

$ |

(381) |

|

$ |

(1,997) |

|

$ |

(761) |

| Agriculture |

|

(645) |

|

|

215 |

|

|

(1,255) |

|

|

363 |

| Operating income (loss) |

|

(1,140) |

|

|

(166) |

|

|

(2,298) |

|

|

(398) |

| |

|

|

|

|

|

|

|

|

|

|

|

| Corporate |

|

(975) |

|

|

5,200 |

|

|

(1,291) |

|

|

4,978 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

Operating income (loss)

before other income

and income taxes |

$ |

(3,069) |

|

$ |

5,034 |

|

$ |

(4,543) |

|

$ |

4,580 |

The Company’s Property

segment consists primarily of revenue received from land sales and lease and licensing agreements.

The Company’s Agriculture

segment consists primarily of coffee operations and licensing agreements.

The Company’s Corporate

segment consists primarily of interest earned on investments.

The Company is exploring

alternative agricultural operations, but there can be no assurance that replacement operations at any level will result.

(9) Subsequent Events

On August 5, 2024, NHC served

KLMC with a Demand for Arbitration. See Note 2 for further discussion of arbitration.

Item 2. Management’s

Discussion and Analysis of Financial Condition and Results

of Operation

General

Unless the context indicates

otherwise, references in this report to “Kaanapali Land” mean Kaanapali Land, LLC, and references to the “Company”

mean Kaanapali Land and all of its subsidiaries and its predecessors.

In addition to historical

information, this report contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995.

These statements are based on management's current expectations about its businesses and the markets in which the Company operates. These

statements include expectations concerning, among other things, the Company’s land development plans, strategy and initiatives,

the expected outcome of the legal proceedings, and the impact of macroeconomic conditions. Such forward-looking statements are not guarantees

of future performance and involve known and unknown risks, uncertainties or other factors which may cause actual results, performance

or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by

such forward-looking statements. Actual operating results may be affected by various factors including, without limitation, natural events,

including the Lahaina wildfire discussed below, the effect of geopolitical, economic and market conditions in Hawaii and globally, including

continued increases in the rate of inflation, changes to fiscal and monetary policy, heightened interest rates and currency fluctuations,

pressure on the global banking system, competitive market conditions, uncertainties and costs related to the imposition of conditions

on receipt of governmental approvals and costs of material and labor, actual versus projected timing of events, and the factors described

in Part I, Item 1A of the Company’s Annual Report on Form 10-K for the year ended December 31, 2023 (the “2023 Form 10-K”),

this report and any other periodic reports the Company files with the U.S. Securities and Exchange Commission (the “SEC), all of

which may cause such actual results to differ materially from what is expressed or forecast in this report.

Lahaina Wildfire

Beginning on August 8, 2023,

a wildfire occurred due east of historic Lahaina town in Maui. The fire spread rapidly due to extreme wind conditions caused in part by

Hurricane Dora which traveled 800 miles offshore west of Maui. The fires caused multiple fatalities, widespread damage to Lahaina town

and the surrounding area including the Company’s 19-acre Pioneer Mill site. The Company’s offices and coffee mill were located

on the site as well as various other structures, including a building which was leased to an unrelated third party and used to operate

a coffee store. The Company also utilized portions of the property for short term license agreements with third parties that generated

income for the Company. Although no employees were injured in the fire, the Company’s offices and coffee store building were destroyed.

Additionally, most of the personal property of the licensees and the coffee mill was destroyed. The widespread destruction is likely to

cause disruptions in the Company’s development plans. The damage to the coffee mill has disrupted operations and prevented the Company

from processing and selling the 2023 year coffee crop. It is also likely that the fires and devastation caused thereby will adversely

affect the long-term Maui economy and businesses operated on Maui. Clean up of Lahaina town, including the Pioneer Mill Site, has commenced

by U.S. Army Corps of Engineers (“USACE”) contractors. Access to the property remains restricted, and such restrictions are

expected to continue while the clean-up of Lahaina town continues, estimated by USACE to be completed in the first quarter of 2025. The

Company has initiated claims with its insurance carriers, and in October 2023, the Company received an initial, unallocated advance payment

of $1 million and in June 2024, the Company received approximately $4.9 million from its insurance carrier. Although the Company currently

expects that the Company’s insurance coverage will compensate the Company for the majority of its losses incurred in connection

with the fire and related devastation, including the costs of its structures and

equipment lost in the fire, the loss in revenue

from the lack of coffee sales, and the loss of income from the licensees, there can be no assurances the Company will be fully compensated

for such losses. The Company could experience losses in excess of our insured limits, and further, claims for certain losses could be

denied or subject to deductibles or exclusions under our insurance policies. The Company has relocated its offices to temporary office

facilities located on its lands in Kaanapali and is in the planning stages of relocating its coffee mill to its farm in Kaanapali. Recovery

efforts continue.

Inflation

High rates of inflation adversely

affect real estate development generally because of their impact on interest rates. High interest rates not only increase the cost of

borrowed funds to the Company, but can also have a significant effect on the affordability of permanent mortgage financing to prospective

purchasers. However, high rates of inflation may permit the Company to increase the prices that it charges in connection with land sales,

subject to a slowdown in sales and increase in home construction costs and to general economic conditions affecting the real estate industry

and local market factors.

Water Use Permits

By letters dated October

28, 2022, the State of Hawaii Commission on Water Resource Management (“CWRM”) officially designated all six Aquifer System

Areas of the Lahaina Aquifer Sector, Maui, as Ground Water Management Areas, as of August 6, 2022. CWRM notified the Company that by August

5, 2023, the Company would need to apply for ground and surface water use permits to continue the Company’s use of certain wells

that are integral to the Company’s entire operations. The Company has submitted such applications for permits. In response to the

Company’s applications for permits, the Company received letters dated July 19, 2024 from CWRM requesting additional information

for both of the Company’s ground water and surface water applications. Such responses are due within 30 days of the date of the

letters. The Company is currently preparing its responses to the letters. The permits, when or if granted and subject to various conditions,

would preserve the Company’s existing water uses as of August 6, 2022. The Company cannot provide any assurances that CWRM

will approve such permit applications for the amounts of water the Company seeks or impose conditions on such use that might affect the

Company’s operations. If CWRM should fail to approve the Company’s water requests or impose onerous conditions on its use,

CWRM’s actions could delay the Company’s development in substantial and material respects and affect the Company’s operations

and finances. Further, in the event permits adequate to the Company’s plans are not received timely or at all, there could be negative

impacts on the west Maui real estate market as a whole and on the development and sale of the Company’s lands on the Island of Maui,

thereby materially and adversely affecting the Company’s operations, land sales, land values, results, and financial position.

By letter dated March 13,

2023, CWRM provided the Company a notice of alleged water violation covering the metering and monitoring of certain designated areas with

the Honokowai aquifer and hydrologic unit, as well as certain waste conditions CWRM allegedly observed on prior investigations of those

certain areas. The Company has engaged with CWRM to address the alleged violations and to seek clarification of the issues. While the

Company does not believe that such issues, when and if addressed by the Company will prove material in cost, there can be no assurances

of same.

Pension Plan

Pacific Trail Holdings LLC,

the manager of the Company, adopted a plan to freeze the benefit accruals under and close participation in the Company’s former

Pension Plan (the “Pension Plan”) and terminated the Pension Plan on or about June 1, 2022. The Company paid lump sum benefits

totaling approximately $0.42 million to Pension Plan participants during October 2022, thereby settling all Pension Plan liabilities.

The remaining assets of the terminated Pension Plan of approximately $14.5 million reverted to the Company on September 15, 2023.

The Company transferred $5 million,

which was approximately 25% of the Pension Plan assets to a qualified replacement plan (“QRP”). The Company’s contribution

to the QRP enabled the Company to reduce the excise tax due as a result of the Pension Plan termination from 50% to 20% of the amount

reverted to the Company. Such assets are maintained in a suspense account within the QRP pending allocation to plan participants. The

assets will be allocated to the participants in the QRP who were participants in the terminated Pension Plan and the employees of certain

affiliates of the Company and were concluded as eligible participants per the Employee Retirement Income Security Act (“ERISA”)

required for QRPs. Such allocations are planned to be allocated ratably over a period not to exceed seven years to comply with regulatory

requirements. On February 26, 2024, approximately $1 million was allocated to the participants in the QRP.

The Company paid the 20%

excise tax of approximately $2.9 million in October 2023. The funds freed up cash to better prepare the Company for tightening credit

markets and are available for, among other things, working capital requirements, including future operating expenses, the Company’s

obligations for engineering, planning, regulatory and development costs, drainage and utilities, and potential environmental remediation

costs on existing properties.

Land Development

In September 2014, Kaanapali

Land Management Corp. (“KLMC”), pursuant to a property and option purchase agreement (“Purchase Agreement”) with

Newport Hospital Corporation (“NHC”), sold a parcel of approximately 14.9 acres in West Maui. The Purchase Agreement included

an Infrastructure Improvement Agreement (as subsequently amended) which commits KLMC to fund up to $0.6 million, depending on various

factors, for off-site roadway, sewer and electrical improvements that will also provide service to other KLMC properties. KLMC may, at

its discretion, design, construct, install, and complete all or portions of the off-site road, sewer and/or electrical improvements, in

which case the developer shall pay to KLMC the total costs thereof, less the KLMC committed amount. In relation to such sewer line improvement,

KLMC entered into a contract for $1.1 million to install the sewer line. KLMC has paid $1.1 million on the contract which has been recorded

as a receivable, less KLMC’s sewer line commitment of $0.2 million. In accordance with the Infrastructure Improvement Agreement,

the receivable accrues interest of 6.5% and is secured by the 14.9 acre property. Due to the receipt of a Demand for Arbitration, discussed

below, as of June 30, 2024, the Company recorded a $1 million credit loss reserve on its receivable with NHC based on its evaluation

of the probability of default that exists at NHC. The amount of the credit loss reserve represents the entire receivable amount and interest

incurred as of June 30, 2024. In conjunction with the Infrastructure Improvement Agreement, the Company retains certain approval rights

relating to the uses and designs of the site to ensure the uses and designs are aligned with the Company’s planned master development.

If such uses result in a dispute with the developer of the site, development of the site could be delayed. The 14.9 acre site is intended

to be used for a critical access hospital, skilled nursing facility, assisted living facility, and independent living facility.

On August 5, 2024, NHC served

KLMC with a Demand for Arbitration, administrated by Dispute Prevention and Resolution, Inc., relating to the Infrastructure Improvement

Agreement and NHC’s development of the site. NHC alleges, among other things, that KLMC wrongfully caused significant delays, increased

costs and related damages to NHC with respect to NHC’s planning and construction of the infrastructure improvements required of

NHC under the Infrastructure Improvement Agreement (as subsequently amended). NHC seeks judgment for declaratory relief that the Infrastructure

Improvement Agreement between NHC and KLMC is void; in the alternative, for reformation of the Infrastructure Improvement Agreement; for

award of damages in an amount to be proven at arbitration; for attorneys’ fees and costs; for prejudgment and post-judgment interest

on any monetary award; and for such other and further relief as the arbitrator deems appropriate. KLMC is in the early stages of assessing

the complaint and intends to vigorously defend. However, there can be no assurance that the eventual outcome of the arbitration will not

result in any material liability or a material impact on business and financial results for KLMC.

On June 3, 2024, KLMC entered into a property

sale agreement (“PVM Sales Agreement”) with an unrelated third party for the sale of several parcels of land, aggregating

approximately 241 acres (the “PVM land parcels”) within Pu’ukoli’i Village Mauka located near the Kaanapali resort

area, north of Lahaina, Hawaii. Pursuant to the PVM Sales Agreement, the base sales price for the PVM land parcels is $29.9 million,

and the closing of the sale of the PVM land parcels is subject to the due diligence period of one hundred days, subject to a one-time

extension. In addition, the developer has the right to terminate the PVM Sales Agreement on or before the expiration of the due diligence

period. Accordingly, there can be no assurance the sale of the PVM land parcels will be completed under the existing or any other terms

of the PVM Sales Agreement, if at all.