UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM 6-K

Report of Foreign Private Issuer Pursuant to

Rule 13a-16 or 15d-16

under the Securities Exchange Act of 1934

For the month of November 2024

Commission

File Number 001-11444

| MAGNA INTERNATIONAL INC. |

| (Exact Name of Registrant as specified in its Charter) |

| |

| 337 Magna Drive, Aurora, Ontario, Canada L4G 7K1 |

| (Address of principal executive office) |

Indicate

by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ¨ Form 40-F

x

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934,

the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

MAGNA INTERNATIONAL INC. |

| |

(Registrant) |

| |

|

| Date: November 1, 2024 |

|

| |

|

| |

By: |

/s/ “Bassem Shakeel” |

| |

|

Bassem

A. Shakeel, |

| |

|

Vice-President, Associate General Counsel and Corporate Secretary |

EXHIBITS

Exhibit 99.1

FINANCIAL REVIEW OF MAGNA INTERNATIONAL INC.

(United States dollars in millions, except per share figures) (Unaudited)

Prepared in accordance with U.S. GAAP

| |

| |

2022 | | |

2023 | | |

2024 | |

| |

Note | |

1st Q | | |

2nd Q | | |

3rd Q | | |

4th Q | | |

TOTAL | | |

1st Q | | |

2nd Q | | |

3rd Q | | |

4th Q | | |

TOTAL | | |

1st Q | | |

2nd Q | | |

3rd Q | | |

TOTAL | |

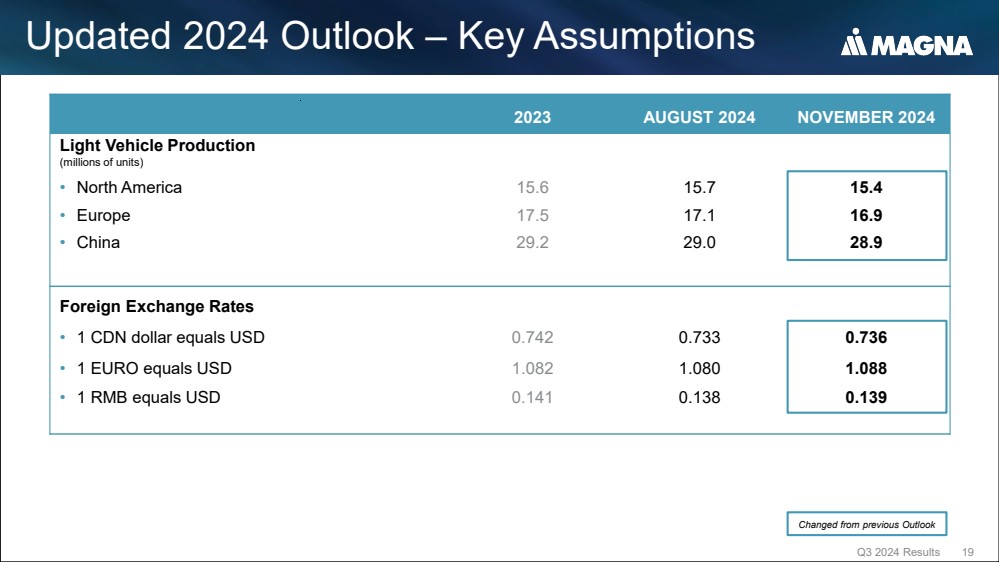

| VEHICLE VOLUME STATISTICS (in millions) | | |

| | |

| | |

| | |

| | |

| |

| North America |

| |

| 3.615 | | |

| 3.551 | | |

| 3.600 | | |

| 3.514 | | |

| 14.280 | | |

| 3.884 | | |

| 4.080 | | |

| 3.930 | | |

| 3.718 | | |

| 15.612 | | |

| 4.019 | | |

| 4.126 | | |

| 3.688 | | |

| 11.833 | |

| Europe |

| |

| 3.962 | | |

| 3.981 | | |

| 3.560 | | |

| 4.168 | | |

| 15.671 | | |

| 4.618 | | |

| 4.637 | | |

| 3.838 | | |

| 4.410 | | |

| 17.503 | | |

| 4.422 | | |

| 4.305 | | |

| 3.761 | | |

| 12.488 | |

| China |

| |

| 6.361 | | |

| 5.485 | | |

| 7.229 | | |

| 7.260 | | |

| 26.335 | | |

| 5.940 | | |

| 6.803 | | |

| 7.628 | | |

| 8.877 | | |

| 29.248 | | |

| 6.455 | | |

| 7.192 | | |

| 7.165 | | |

| 20.812 | |

| Other |

| |

| 6.384 | | |

| 6.145 | | |

| 6.709 | | |

| 6.873 | | |

| 26.111 | | |

| 6.970 | | |

| 6.729 | | |

| 6.998 | | |

| 7.147 | | |

| 27.844 | | |

| 6.591 | | |

| 6.646 | | |

| 6.795 | | |

| 20.032 | |

| Global |

| |

| 20.322 | | |

| 19.162 | | |

| 21.098 | | |

| 21.815 | | |

| 82.397 | | |

| 21.412 | | |

| 22.249 | | |

| 22.394 | | |

| 24.152 | | |

| 90.207 | | |

| 21.487 | | |

| 22.269 | | |

| 21.409 | | |

| 65.165 | |

| Magna Steyr vehicle assembly volumes |

| |

| 0.026 | | |

| 0.032 | | |

| 0.026 | | |

| 0.028 | | |

| 0.112 | | |

| 0.034 | | |

| 0.027 | | |

| 0.023 | | |

| 0.021 | | |

| 0.105 | | |

| 0.022 | | |

| 0.019 | | |

| 0.016 | | |

| 0.057 | |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| AVERAGE FOREIGN

EXCHANGE RATES | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| 1 Canadian dollar equals U.S. dollars |

| |

| 0.790 | | |

| 0.783 | | |

| 0.765 | | |

| 0.737 | | |

| 0.769 | | |

| 0.740 | | |

| 0.745 | | |

| 0.746 | | |

| 0.735 | | |

| 0.742 | | |

| 0.741 | | |

| 0.731 | | |

| 0.733 | | |

| 0.735 | |

| 1 euro equals U.S. dollars |

| |

| 1.123 | | |

| 1.064 | | |

| 1.006 | | |

| 1.019 | | |

| 1.053 | | |

| 1.073 | | |

| 1.089 | | |

| 1.088 | | |

| 1.076 | | |

| 1.082 | | |

| 1.085 | | |

| 1.076 | | |

| 1.099 | | |

| 1.087 | |

| 1 Chinese renminbi equals U.S. dollars |

| |

| 0.158 | | |

| 0.151 | | |

| 0.146 | | |

| 0.140 | | |

| 0.149 | | |

| 0.146 | | |

| 0.143 | | |

| 0.138 | | |

| 0.138 | | |

| 0.141 | | |

| 0.139 | | |

| 0.138 | | |

| 0.140 | | |

| 0.139 | |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| CONSOLIDATED STATEMENTS

OF INCOME (LOSS) | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Sales: |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Body Exteriors & Structures |

| |

| 4,077 | | |

| 3,947 | | |

| 3,976 | | |

| 4,004 | | |

| 16,004 | | |

| 4,439 | | |

| 4,540 | | |

| 4,354 | | |

| 4,178 | | |

| 17,511 | | |

| 4,429 | | |

| 4,465 | | |

| 4,038 | | |

| 12,932 | |

| Power & Vision |

| |

| 3,046 | | |

| 2,888 | | |

| 2,911 | | |

| 3,016 | | |

| 11,861 | | |

| 3,323 | | |

| 3,462 | | |

| 3,745 | | |

| 3,775 | | |

| 14,305 | | |

| 3,842 | | |

| 3,926 | | |

| 3,837 | | |

| 11,605 | |

| Seating Systems |

| |

| 1,376 | | |

| 1,253 | | |

| 1,295 | | |

| 1,345 | | |

| 5,269 | | |

| 1,486 | | |

| 1,603 | | |

| 1,529 | | |

| 1,429 | | |

| 6,047 | | |

| 1,455 | | |

| 1,455 | | |

| 1,379 | | |

| 4,289 | |

| Complete Vehicles |

| |

| 1,275 | | |

| 1,403 | | |

| 1,213 | | |

| 1,330 | | |

| 5,221 | | |

| 1,626 | | |

| 1,526 | | |

| 1,185 | | |

| 1,201 | | |

| 5,538 | | |

| 1,383 | | |

| 1,242 | | |

| 1,159 | | |

| 3,784 | |

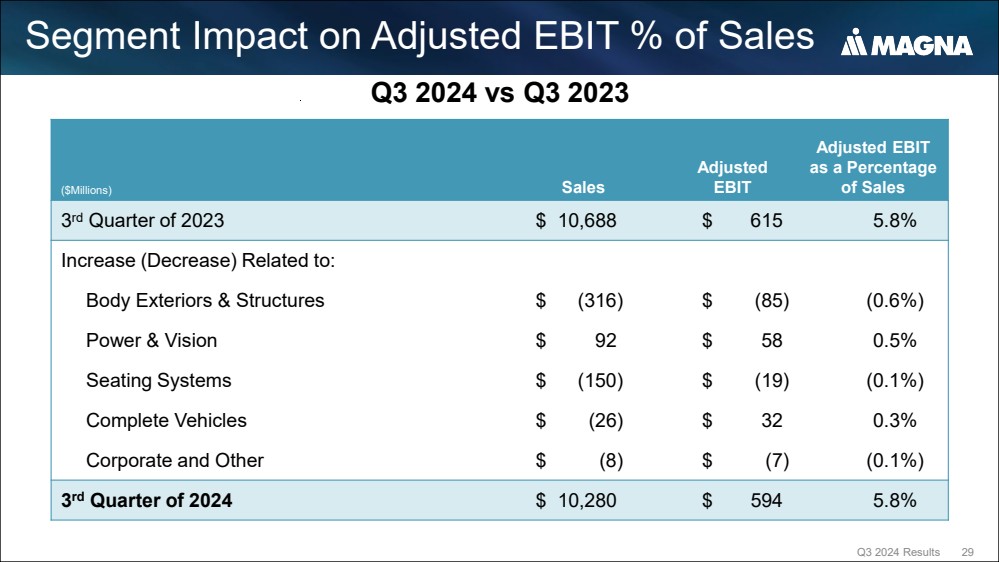

| Corporate & Other |

| |

| (132 | ) | |

| (129 | ) | |

| (127 | ) | |

| (127 | ) | |

| (515 | ) | |

| (201 | ) | |

| (149 | ) | |

| (125 | ) | |

| (129 | ) | |

| (604 | ) | |

| (139 | ) | |

| (130 | ) | |

| (133 | ) | |

| (402 | ) |

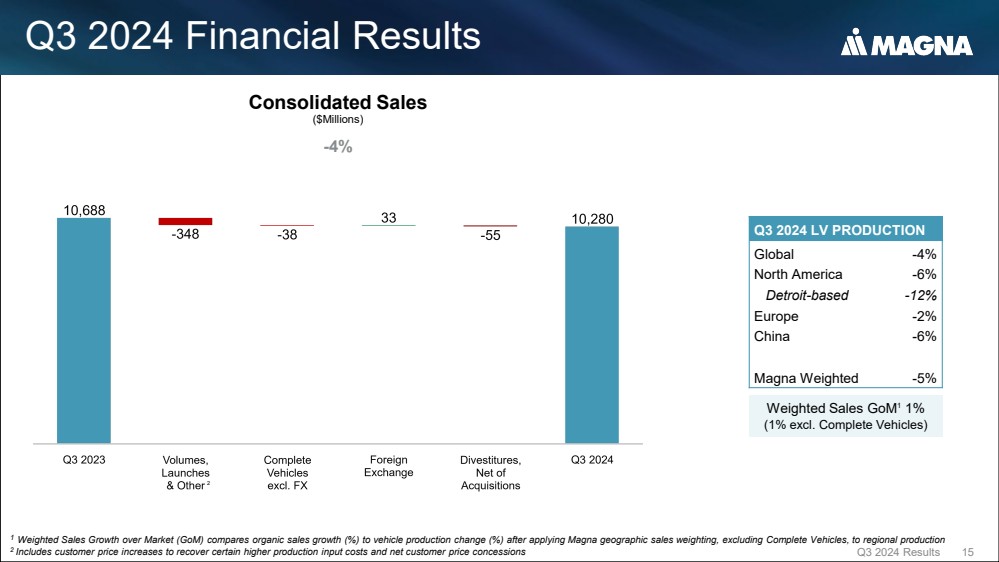

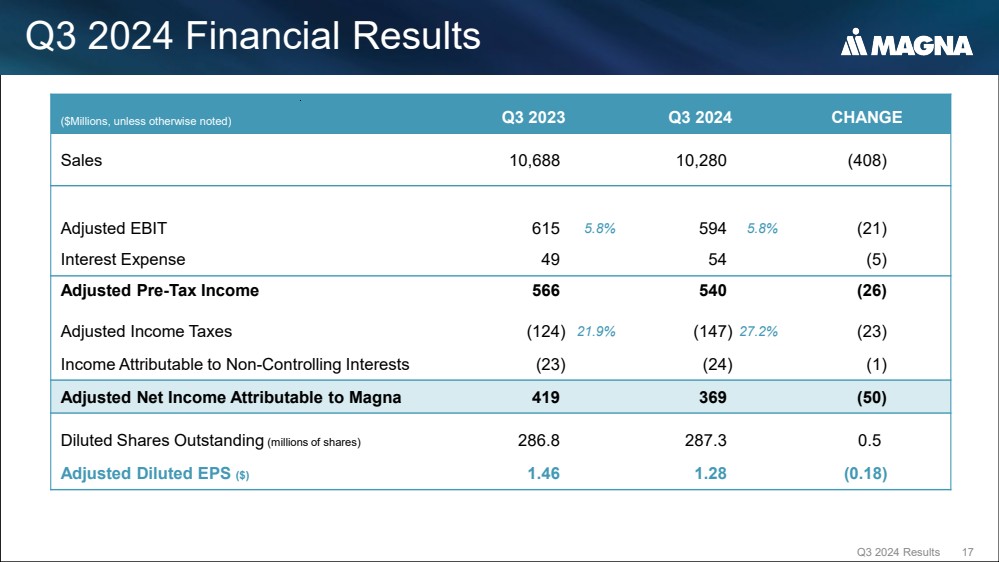

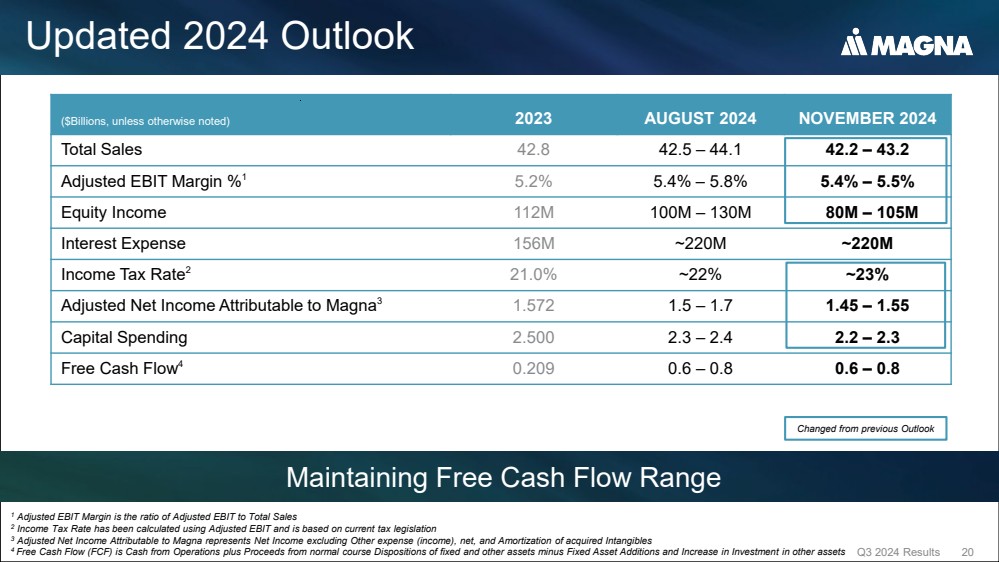

| Sales |

| |

| 9,642 | | |

| 9,362 | | |

| 9,268 | | |

| 9,568 | | |

| 37,840 | | |

| 10,673 | | |

| 10,982 | | |

| 10,688 | | |

| 10,454 | | |

| 42,797 | | |

| 10,970 | | |

| 10,958 | | |

| 10,280 | | |

| 32,208 | |

| Costs and expenses: |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Cost of goods sold |

| |

| 8,400 | | |

| 8,259 | | |

| 8,126 | | |

| 8,403 | | |

| 33,188 | | |

| 9,416 | | |

| 9,544 | | |

| 9,264 | | |

| 8,961 | | |

| 37,185 | | |

| 9,642 | | |

| 9,494 | | |

| 8,828 | | |

| 27,964 | |

| Selling, general and administrative |

| |

| 386 | | |

| 410 | | |

| 387 | | |

| 477 | | |

| 1,660 | | |

| 488 | | |

| 505 | | |

| 491 | | |

| 566 | | |

| 2,050 | | |

| 516 | | |

| 523 | | |

| 487 | | |

| 1,526 | |

| Equity income |

| |

| (20 | ) | |

| (25 | ) | |

| (27 | ) | |

| (17 | ) | |

| (89 | ) | |

| (33 | ) | |

| (36 | ) | |

| (40 | ) | |

| (3 | ) | |

| (112 | ) | |

| (34 | ) | |

| (9 | ) | |

| (13 | ) | |

| (56 | ) |

| Adjusted EBITDA |

| |

| 876 | | |

| 718 | | |

| 782 | | |

| 705 | | |

| 3,081 | | |

| 802 | | |

| 969 | | |

| 973 | | |

| 930 | | |

| 3,674 | | |

| 846 | | |

| 950 | | |

| 978 | | |

| 2,774 | |

| Depreciation |

| |

| 357 | | |

| 348 | | |

| 330 | | |

| 338 | | |

| 1,373 | | |

| 353 | | |

| 353 | | |

| 358 | | |

| 372 | | |

| 1,436 | | |

| 377 | | |

| 373 | | |

| 384 | | |

| 1,134 | |

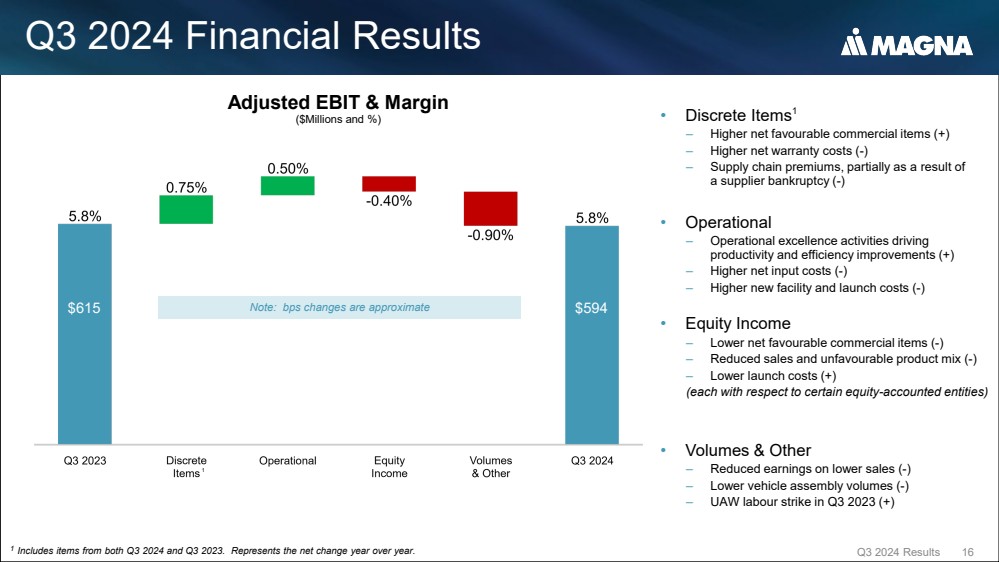

| Adjusted EBIT |

| |

| 519 | | |

| 370 | | |

| 452 | | |

| 367 | | |

| 1,708 | | |

| 449 | | |

| 616 | | |

| 615 | | |

| 558 | | |

| 2,238 | | |

| 469 | | |

| 577 | | |

| 594 | | |

| 1,640 | |

| Amortization of acquired intangible

assets |

| |

| 12 | | |

| 12 | | |

| 11 | | |

| 11 | | |

| 46 | | |

| 12 | | |

| 13 | | |

| 32 | | |

| 31 | | |

| 88 | | |

| 28 | | |

| 28 | | |

| 28 | | |

| 84 | |

| Other expense (income), net |

1 | |

| 61 | | |

| 426 | | |

| 23 | | |

| 193 | | |

| 703 | | |

| 142 | | |

| 86 | | |

| (4 | ) | |

| 164 | | |

| 388 | | |

| 356 | | |

| 68 | | |

| (188 | ) | |

| 236 | |

| Interest expense,

net |

| |

| 26 | | |

| 20 | | |

| 18 | | |

| 17 | | |

| 81 | | |

| 20 | | |

| 34 | | |

| 49 | | |

| 53 | | |

| 156 | | |

| 51 | | |

| 54 | | |

| 54 | | |

| 159 | |

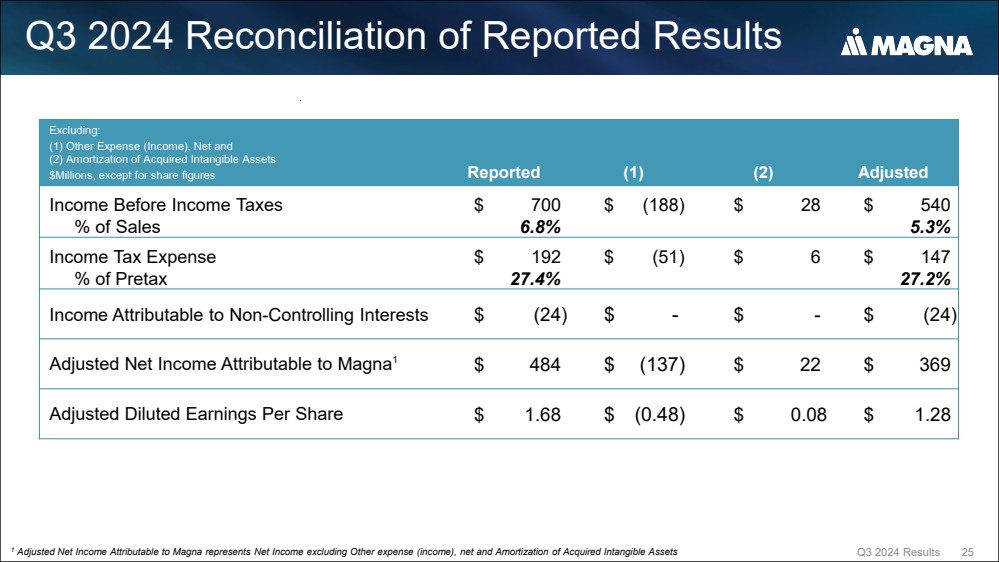

| Income (loss)

from operations before income taxes |

| |

| 420 | | |

| (88 | ) | |

| 400 | | |

| 146 | | |

| 878 | | |

| 275 | | |

| 483 | | |

| 538 | | |

| 310 | | |

| 1,606 | | |

| 34 | | |

| 427 | | |

| 700 | | |

| 1,161 | |

| Income tax expense |

| |

| 41 | | |

| 57 | | |

| 104 | | |

| 35 | | |

| 237 | | |

| 58 | | |

| 129 | | |

| 121 | | |

| 12 | | |

| 320 | | |

| 8 | | |

| 99 | | |

| 192 | | |

| 299 | |

| Net income

(loss) |

| |

| 379 | | |

| (145 | ) | |

| 296 | | |

| 111 | | |

| 641 | | |

| 217 | | |

| 354 | | |

| 417 | | |

| 298 | | |

| 1,286 | | |

| 26 | | |

| 328 | | |

| 508 | | |

| 862 | |

| Income attributable to non-controlling interests |

| |

| (15 | ) | |

| (11 | ) | |

| (7 | ) | |

| (16 | ) | |

| (49 | ) | |

| (8 | ) | |

| (15 | ) | |

| (23 | ) | |

| (27 | ) | |

| (73 | ) | |

| (17 | ) | |

| (15 | ) | |

| (24 | ) | |

| (56 | ) |

| Net income

(loss) attributable to Magna International Inc. |

| |

| 364 | | |

| (156 | ) | |

| 289 | | |

| 95 | | |

| 592 | | |

| 209 | | |

| 339 | | |

| 394 | | |

| 271 | | |

| 1,213 | | |

| 9 | | |

| 313 | | |

| 484 | | |

| 806 | |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Diluted earnings

(loss) per common share |

| |

$ | 1.22 | | |

$ | (0.54 | ) | |

$ | 1.00 | | |

$ | 0.33 | | |

$ | 2.03 | | |

$ | 0.73 | | |

$ | 1.18 | | |

$ | 1.37 | | |

$ | 0.94 | | |

$ | 4.23 | | |

$ | 0.03 | | |

$ | 1.09 | | |

$ | 1.68 | | |

$ | 2.81 | |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Weighted average

number of Common Shares outstanding during the period (in millions): |

| |

| 298.1 | | |

| 291.1 | | |

| 288.5 | | |

| 286.3 | | |

| 291.2 | | |

| 286.6 | | |

| 286.3 | | |

| 286.8 | | |

| 286.6 | | |

| 286.6 | | |

| 287.1 | | |

| 287.3 | | |

| 287.3 | | |

| 287.2 | |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| NON-GAAP MEASURES |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Adjusted EBITDA |

| |

| 876 | | |

| 718 | | |

| 782 | | |

| 705 | | |

| 3,081 | | |

| 802 | | |

| 969 | | |

| 973 | | |

| 930 | | |

| 3,674 | | |

| 846 | | |

| 950 | | |

| 978 | | |

| 2,774 | |

| Adjusted EBIT |

2 | |

| 519 | | |

| 370 | | |

| 452 | | |

| 367 | | |

| 1,708 | | |

| 449 | | |

| 616 | | |

| 615 | | |

| 558 | | |

| 2,238 | | |

| 469 | | |

| 577 | | |

| 594 | | |

| 1,640 | |

| Adjusted net

income attributable to Magna International Inc. |

2 | |

| 393 | | |

| 253 | | |

| 317 | | |

| 270 | | |

| 1,233 | | |

| 329 | | |

| 441 | | |

| 419 | | |

| 383 | | |

| 1,572 | | |

| 311 | | |

| 389 | | |

| 369 | | |

| 1,069 | |

| Adjusted Diluted

earnings per common share |

2 | |

$ | 1.32 | | |

$ | 0.87 | | |

$ | 1.10 | | |

$ | 0.94 | | |

$ | 4.24 | | |

$ | 1.15 | | |

$ | 1.54 | | |

$ | 1.46 | | |

$ | 1.33 | | |

$ | 5.49 | | |

$ | 1.08 | | |

$ | 1.35 | | |

$ | 1.28 | | |

$ | 3.72 | |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| PROFITABILITY RATIOS |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Selling, general and administrative /Sales |

| |

| 4.0 | % | |

| 4.4 | % | |

| 4.2 | % | |

| 5.0 | % | |

| 4.4 | % | |

| 4.6 | % | |

| 4.6 | % | |

| 4.6 | % | |

| 5.4 | % | |

| 4.8 | % | |

| 4.7 | % | |

| 4.8 | % | |

| 4.7 | % | |

| 4.7 | % |

| Adjusted EBIT /Sales |

| |

| 5.4 | % | |

| 4.0 | % | |

| 4.9 | % | |

| 3.8 | % | |

| 4.5 | % | |

| 4.2 | % | |

| 5.6 | % | |

| 5.8 | % | |

| 5.3 | % | |

| 5.2 | % | |

| 4.3 | % | |

| 5.3 | % | |

| 5.8 | % | |

| 5.1 | % |

| Income (loss) from operations before income taxes /Sales |

| |

| 4.4 | % | |

| -0.9 | % | |

| 4.3 | % | |

| 1.5 | % | |

| 2.3 | % | |

| 2.6 | % | |

| 4.4 | % | |

| 5.0 | % | |

| 3.0 | % | |

| 3.8 | % | |

| 0.3 | % | |

| 3.9 | % | |

| 6.8 | % | |

| 3.6 | % |

| Effective tax rate |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Reported |

| |

| 9.8 | % | |

| -64.8 | % | |

| 26.0 | % | |

| 24.0 | % | |

| 27.0 | % | |

| 21.1 | % | |

| 26.7 | % | |

| 22.5 | % | |

| 3.9 | % | |

| 19.9 | % | |

| 23.5 | % | |

| 23.2 | % | |

| 27.4 | % | |

| 25.8 | % |

| Excluding Other

expense (income) and amortization, net of taxes and valuation allowance adjustments |

| |

| 17.2 | % | |

| 24.6 | % | |

| 25.3 | % | |

| 18.3 | % | |

| 21.2 | % | |

| 21.4 | % | |

| 21.6 | % | |

| 21.9 | % | |

| 18.8 | % | |

| 21.0 | % | |

| 21.5 | % | |

| 22.8 | % | |

| 27.2 | % | |

| 24.0 | % |

| Q3 2024 Financial Review of Magna International Inc. | Page 1 of 8 | Prepared as at 10/31/24 |

FINANCIAL

REVIEW OF MAGNA INTERNATIONAL INC.

CONSOLIDATED

BALANCE SHEETS

(United

States dollars in millions) (Unaudited)

| | |

2022 |

| |

2023 | |

2024 | |

| | |

1st

Q | |

2nd

Q | |

|

3rd

Q |

4th

Q |

| |

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q | |

1st

Q | |

2nd

Q | |

3rd

Q | |

| FUNDS

EMPLOYED | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Current

assets: | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Accounts

receivable | |

7,006 | |

6,764 | |

|

7,082 |

|

| 6,791 |

| |

7,959 | |

8,556 | |

8,477 | |

7,881 | |

8,379 | |

8,219 | |

8,377 | |

| Inventories | |

4,258 | |

4,064 | |

|

4,108 |

|

| 4,180 |

| |

4,421 | |

4,664 | |

4,751 | |

4,606 | |

4,511 | |

4,466 | |

4,592 | |

| Prepaid

expenses and other | |

310 | |

262 | |

|

269 |

|

| 320 |

| |

367 | |

455 | |

387 | |

352 | |

399 | |

314 | |

303 | |

| | |

11,574 | |

11,090 | |

|

11,459 |

|

| 11,291 |

| |

12,747 | |

13,675 | |

13,615 | |

12,839 | |

13,289 | |

12,999 | |

13,272 | |

| Current

liabilities: | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Accounts

payable | |

6,845 | |

6,443 | |

|

6,624 |

|

| 6,999 |

| |

7,731 | |

7,984 | |

7,911 | |

7,842 | |

7,855 | |

7,639 | |

7,608 | |

| Accrued

salaries and wages | |

879 | |

766 | |

|

810 |

|

| 850 |

| |

822 | |

858 | |

900 | |

912 | |

883 | |

862 | |

962 | |

| Other

accrued liabilities | |

2,123 | |

2,096 | |

|

1,986 |

|

| 2,118 |

| |

2,526 | |

2,637 | |

2,537 | |

2,626 | |

2,728 | |

2,650 | |

2,642 | |

| Income

taxes payable (receivable) | |

190 | |

136 | |

|

97 |

|

| 93 |

| |

9 | |

(14 | ) |

33 | |

125 | |

132 | |

79 | |

176 | |

| | |

10,037 | |

9,441 | |

|

9,517 |

|

| 10,060 |

| |

11,088 | |

11,465 | |

11,381 | |

11,505 | |

11,598 | |

11,230 | |

11,388 | |

| | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Working

capital | |

1,537 | |

1,649 | |

|

1,942 |

|

| 1,231 |

| |

1,659 | |

2,210 | |

2,234 | |

1,334 | |

1,691 | |

1,769 | |

1,884 | |

| | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Investments | |

1,487 | |

1,375 | |

|

1,323 |

|

| 1,429 |

| |

1,390 | |

1,287 | |

1,311 | |

1,273 | |

1,195 | |

1,161 | |

1,165 | |

| Fixed

assets, net | |

8,090 | |

7,723 | |

|

7,470 |

|

| 8,173 |

| |

8,304 | |

8,646 | |

8,778 | |

9,618 | |

9,545 | |

9,623 | |

9,836 | |

| Goodwill,

other assets and intangible assets | |

3,544 | |

3,353 | |

|

3,280 |

|

| 3,576 |

| |

3,640 | |

4,733 | |

4,726 | |

4,962 | |

4,646 | |

4,709 | |

4,865 | |

| Operating

lease right-of-use assets | |

1,667 | |

1,587 | |

|

1,545 |

|

| 1,595 |

| |

1,638 | |

1,667 | |

1,696 | |

1,744 | |

1,733 | |

1,688 | |

1,780 | |

| Funds

employed | |

16,325 | |

15,687 | |

|

15,560 |

|

| 16,004 |

| |

16,631 | |

18,543 | |

18,745 | |

18,931 | |

18,810 | |

18,950 | |

19,530 | |

| FINANCING | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Straight

debt: | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Cash

and cash equivalents | |

(1,996 | ) |

(1,664 | ) |

|

(1,102 |

) |

| (1,234 |

) | |

(2,429 | ) |

(1,281 | ) |

(1,022 | ) |

(1,198 | ) |

(1,517 | ) |

(999 | ) |

(1,061 | ) |

| Short-term

borrowings | |

- | |

- | |

|

- |

|

| 8 |

| |

4 | |

150 | |

2 | |

511 | |

838 | |

848 | |

828 | |

| Long-term

debt due within one year | |

127 | |

105 | |

|

95 |

|

| 654 |

| |

668 | |

1,426 | |

1,398 | |

819 | |

824 | |

65 | |

65 | |

| Long-term

debt | |

3,501 | |

3,408 | |

|

3,325 |

|

| 2,847 |

| |

4,500 | |

4,159 | |

4,135 | |

4,175 | |

4,549 | |

4,863 | |

4,916 | |

| Current

portion of operating lease liabilities | |

276 | |

270 | |

|

266 |

|

| 276 |

| |

285 | |

303 | |

384 | |

399 | |

306 | |

306 | |

319 | |

| Operating

lease liabilities | |

1,369 | |

1,294 | |

|

1,254 |

|

| 1,288 |

| |

1,318 | |

1,345 | |

1,289 | |

1,319 | |

1,407 | |

1,378 | |

1,458 | |

| | |

3,277 | |

3,413 | |

|

3,838 |

|

| 3,839 |

| |

4,346 | |

6,102 | |

6,186 | |

6,025 | |

6,407 | |

6,461 | |

6,525 | |

| Long-term

employee benefit liabilities | |

686 | |

651 | |

|

617 |

|

| 548 |

| |

563 | |

579 | |

564 | |

591 | |

584 | |

564 | |

571 | |

| Other

long-term liabilities | |

374 | |

390 | |

|

397 |

|

| 461 |

| |

451 | |

448 | |

453 | |

475 | |

471 | |

507 | |

339 | |

| Deferred

tax assets, net | |

(51 | ) |

(111 | ) |

|

(138 |

) |

| (179 |

) | |

(218 | ) |

(242 | ) |

(210 | ) |

(437 | ) |

(576 | ) |

(592 | ) |

(592 | ) |

| | |

1,009 | |

930 | |

|

876 |

|

| 830 |

| |

796 | |

785 | |

807 | |

629 | |

479 | |

479 | |

318 | |

| Shareholders'

equity | |

12,039 | |

11,344 | |

|

10,846 |

|

| 11,335 |

| |

11,489 | |

11,656 | |

11,752 | |

12,277 | |

11,924 | |

12,010 | |

12,687 | |

| | |

16,325 | |

15,687 | |

|

15,560 |

|

| 16,004 |

| |

16,631 | |

18,543 | |

18,745 | |

18,931 | |

18,810 | |

18,950 | |

19,530 | |

| | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| ASSET

UTILIZATION RATIOS | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Days

in accounts receivable | |

65.4 | |

65.0 | |

|

68.8 |

|

| 63.9 |

| |

67.1 | |

70.1 | |

71.4 | |

67.8 | |

68.7 | |

67.5 | |

73.3 | |

| Days

in accounts payable | |

73.3 | |

70.2 | |

|

73.4 |

|

| 75.0 |

| |

73.9 | |

75.3 | |

76.9 | |

78.8 | |

73.3 | |

72.4 | |

77.6 | |

| Inventory

turnover - cost of goods sold | |

7.9 | |

8.1 | |

|

7.9 |

|

| 8.0 |

| |

8.5 | |

8.2 | |

7.8 | |

7.8 | |

8.5 | |

8.5 | |

7.7 | |

| Working

capital turnover | |

25.1 | |

22.7 | |

|

19.1 |

|

| 31.1 |

| |

25.7 | |

19.9 | |

19.1 | |

31.3 | |

25.9 | |

24.8 | |

21.8 | |

| Total

asset turnover | |

2.4 | |

2.4 | |

|

2.4 |

|

| 2.4 |

| |

2.6 | |

2.4 | |

2.3 | |

2.2 | |

2.3 | |

2.3 | |

2.1 | |

| | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| CAPITAL

STRUCTURE | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Straight

debt | |

20.1 | % |

21.8 | % |

|

24.7 |

% |

| 24.0 |

% | |

26.1 | % |

32.9 | % |

33.0 | % |

31.8 | % |

34.1 | % |

34.1 | % |

33.4 | % |

| Long-term employee benefit

liabilities, other long-term liabilities & deferred tax liabilities, net | |

6.2 | % |

5.9 | % |

|

5.6 |

% |

| 5.2 |

% | |

4.8 | % |

4.2 | % |

4.3 | % |

3.3 | % |

2.5 | % |

2.5 | % |

1.6 | % |

| Shareholders'

equity | |

73.7 | % |

72.3 | % |

|

69.7 |

% |

| 70.8 |

% | |

69.1 | % |

62.9 | % |

62.7 | % |

64.9 | % |

63.4 | % |

63.4 | % |

65.0 | % |

| | |

100.0 | % |

100.0 | % |

|

100.0 |

% |

| 100.0 |

% | |

100.0 | % |

100.0 | % |

100.0 | % |

100.0 | % |

100.0 | % |

100.0 | % |

100.0 | % |

| | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Debt

to total capitalization | |

30.5 | % |

30.9 | % |

|

31.3 |

% |

| 30.9 |

% | |

37.1 | % |

38.8 | % |

38.0 | % |

37.0 | % |

39.9 | % |

38.3 | % |

37.4 | % |

| | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| ANNUALIZED

RETURNS | |

| |

| |

|

|

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Adjusted Return on equity

(Adjusted Net income attributable to Magna International Inc. / Average shareholders' equity) | |

13.6 | % |

8.7 | % |

|

11.4 |

% |

| 9.7 |

% | |

11.5 | % |

15.2 | % |

14.3 | % |

12.8 | % |

10.3 | % |

13.0 | % |

12.0 | % |

| Adjusted

Return on Invested Capital (Adjusted Annualized after-tax operating profits / Invested capital) | |

10.6 | % |

7.0 | % |

|

8.6 |

% |

| 7.6 |

% | |

8.7 | % |

11.0 | % |

10.3 | % |

9.6 | % |

7.8 | % |

9.4 | % |

9.0 | % |

| Q3 2024 Financial Review of Magna International Inc. | Page 2 of 8 | Prepared as at 10/31/24 |

FINANCIAL

REVIEW OF MAGNA INTERNATIONAL INC.

CONSOLIDATED

STATEMENTS OF CASH FLOWS

(United

States dollars in millions) (Unaudited)

| | |

| |

2022 | | |

2023 | |

2024 | |

| | |

Note | |

1st

Q | | |

2nd

Q | | |

3rd

Q | | |

4th

Q | |

TOTAL | | |

1st

Q | | |

2nd

Q | | |

3rd

Q | | |

4th

Q | |

TOTAL | |

1st

Q | |

2nd

Q | |

3rd

Q | |

TOTAL | |

| Cash provided from (used for): | |

| |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | |

| |

| |

| |

| |

| |

| |

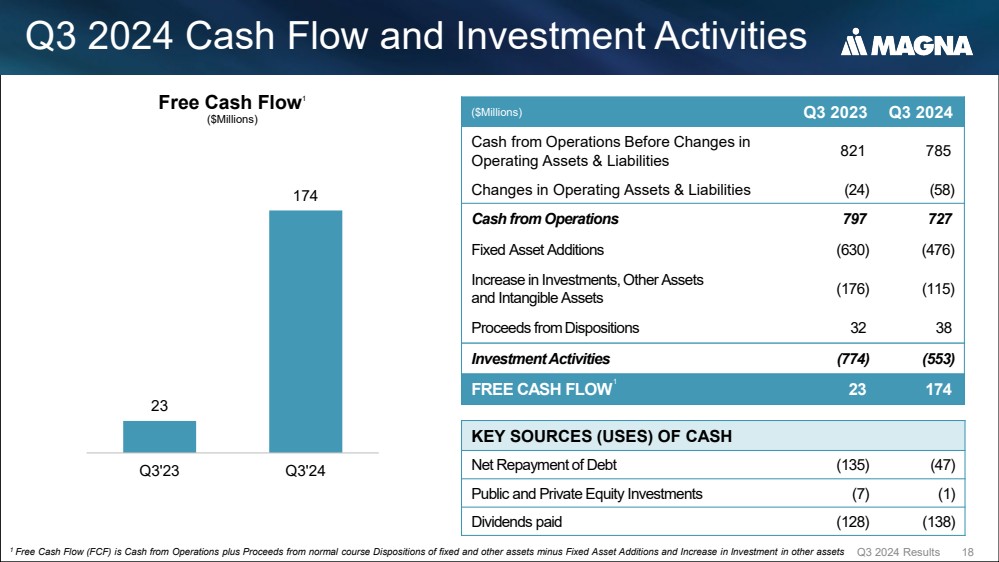

| Operating activities | |

| |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | | |

| |

| |

| |

| |

| |

| |

| Net

income (loss) | |

| |

379 | | |

(145 | ) | |

296 | | |

111 | |

641 | | |

217 | | |

354 | | |

| 417 | | |

298 | |

1,286 | |

26 | |

328 | |

508 | |

862 | |

| Items

not involving current cash flows | |

| |

370 | | |

705 | | |

295 | | |

406 | |

1,776 | | |

351 | | |

525 | | |

| 404 | | |

362 | |

1,642 | |

565 | |

353 | |

277 | |

1,195 | |

| | |

| |

749 | | |

560 | | |

591 | | |

517 | |

2,417 | | |

568 | | |

879 | | |

| 821 | | |

660 | |

2,928 | |

591 | |

681 | |

785 | |

2,057 | |

| Changes

in operating assets and liabilities | |

| |

(569 | ) | |

(139 | ) | |

(353 | ) | |

739 | |

(322 | ) | |

(341 | ) | |

(332 | ) | |

| (24 | ) | |

918 | |

221 | |

(330 | ) |

55 | |

(58 | ) |

(333 | ) |

| | |

| |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | | |

| |

| |

| |

| |

| |

| |

| Cash provided from operating

activities | |

| |

180 | | |

421 | | |

238 | | |

1,256 | |

2,095 | | |

227 | | |

547 | | |

| 797 | | |

1,578 | |

3,149 | |

261 | |

736 | |

727 | |

1,724 | |

| | |

| |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | | |

| |

| |

| |

| |

| |

| |

| Investment activities | |

| |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | | |

| |

| |

| |

| |

| |

| |

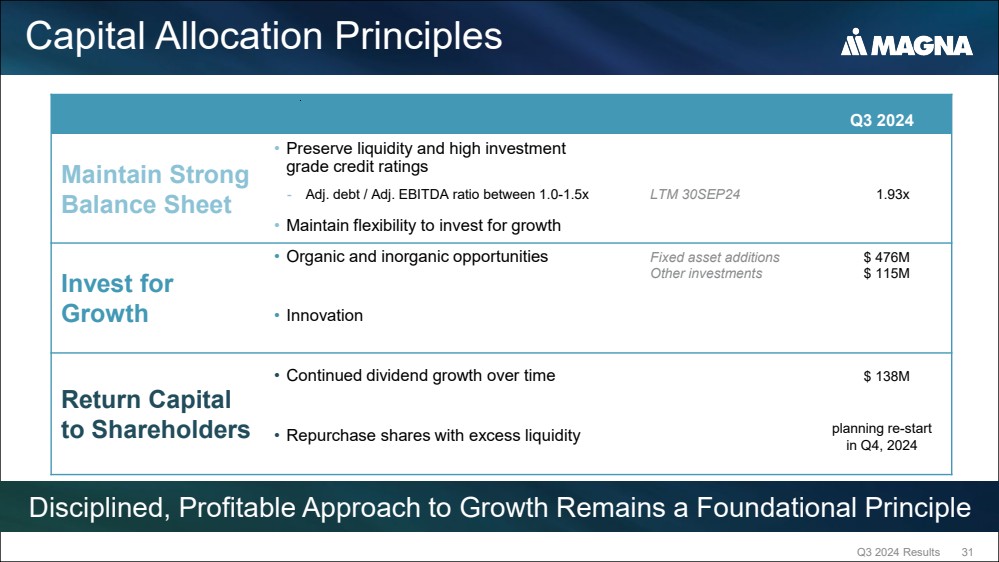

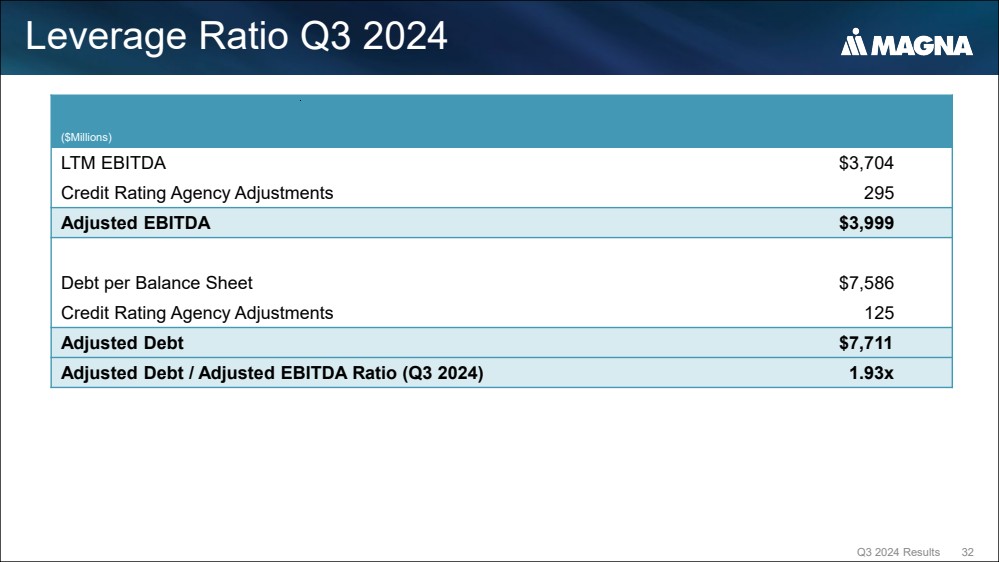

| Fixed

asset additions | |

| |

(238 | ) | |

(329 | ) | |

(364 | ) | |

(750 | ) |

(1,681 | ) | |

(424 | ) | |

(502 | ) | |

| (630 | ) | |

(944 | ) |

(2,500 | ) |

(493 | ) |

(500 | ) |

(476 | ) |

(1,469 | ) |

| Increase

in investments, other assets and intangible assets | |

| |

(64 | ) | |

(80 | ) | |

(125 | ) | |

(186 | ) |

(455 | ) | |

(101 | ) | |

(96 | ) | |

| (176 | ) | |

(189 | ) |

(562 | ) |

(125 | ) |

(170 | ) |

(115 | ) |

(410 | ) |

| Net

cash inflow (outflow) from disposal of facilities | |

1(e),

1(g) | |

6 | | |

- | | |

- | | |

- | |

6 | | |

(25 | ) | |

- | | |

| (23 | ) | |

- | |

(48 | ) |

4 | |

- | |

78 | |

82 | |

| (Decrease)

increase in public and private equity investments | |

| |

(2 | ) | |

(2 | ) | |

(25 | ) | |

- | |

(29 | ) | |

- | | |

(3 | ) | |

| (7 | ) | |

(1 | ) |

(11 | ) |

(23 | ) |

2 | |

(1 | ) |

(22 | ) |

| Proceeds

from disposition | |

| |

23 | | |

40 | | |

41 | | |

20 | |

124 | | |

19 | | |

44 | | |

| 32 | | |

27 | |

122 | |

87 | |

57 | |

38 | |

182 | |

| Business

combinations | |

| |

- | | |

- | | |

- | | |

(3 | ) |

(3 | ) | |

- | | |

(1,475 | ) | |

| - | | |

(29 | ) |

(1,504 | ) |

(30 | ) |

(56 | ) |

- | |

(86 | ) |

| Cash used for investment

activities | |

| |

(275 | ) | |

(371 | ) | |

(473 | ) | |

(919 | ) |

(2,038 | ) | |

(531 | ) | |

(2,032 | ) | |

| (804 | ) | |

(1,136 | ) |

(4,503 | ) |

(580 | ) |

(667 | ) |

(476 | ) |

(1,723 | ) |

| | |

| |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | | |

| |

| |

| |

| |

| |

| |

| Financing

activities | |

| |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | | |

| |

| |

| |

| |

| |

| |

| Net

issues (repayments) of debt | |

| |

(328 | ) | |

(31 | ) | |

(10 | ) | |

(22 | ) |

(391 | ) | |

1,636 | | |

544 | | |

| (135 | ) | |

(119 | ) |

1,926 | |

757 | |

(416 | ) |

(47 | ) |

294 | |

| Common

Shares issued on exercise of stock options | |

| |

4 | | |

- | | |

1 | | |

3 | |

8 | | |

6 | | |

- | | |

| 8 | | |

6 | |

20 | |

30 | |

- | |

- | |

30 | |

| Repurchase of Common

Shares | |

| |

(383 | ) | |

(212 | ) | |

(180 | ) | |

(5 | ) |

(780 | ) | |

(9 | ) | |

(2 | ) | |

| - | | |

(2 | ) |

(13 | ) |

(3 | ) |

(2 | ) |

- | |

(5 | ) |

| Tax

withholdings on vesting of equity awards | |

| |

(14 | ) | |

(1 | ) | |

- | | |

- | |

(15 | ) | |

(9 | ) | |

(1 | ) | |

| - | | |

(1 | ) |

(11 | ) |

(4 | ) |

(1 | ) |

- | |

(5 | ) |

| Contributions

to subsidiaries by non-controlling interests | |

| |

- | | |

5 | | |

- | | |

- | |

5 | | |

- | | |

- | | |

| - | | |

11 | |

11 | |

- | |

- | |

- | |

- | |

| Dividends

paid to non-controlling interests | |

| |

- | | |

(12 | ) | |

(10 | ) | |

(24 | ) |

(46 | ) | |

(7 | ) | |

(24 | ) | |

| (18 | ) | |

(25 | ) |

(74 | ) |

- | |

(26 | ) |

(10 | ) |

(36 | ) |

| Dividends

paid | |

| |

(133 | ) | |

(130 | ) | |

(125 | ) | |

(126 | ) |

(514 | ) | |

(132 | ) | |

(129 | ) | |

| (128 | ) | |

(133 | ) |

(522 | ) |

(134 | ) |

(134 | ) |

(138 | ) |

(406 | ) |

| Cash provided from (used

for) financing activities | |

| |

(854 | ) | |

(381 | ) | |

(324 | ) | |

(174 | ) |

(1,733 | ) | |

1,485 | | |

388 | | |

| (273 | ) | |

(263 | ) |

1,337 | |

646 | |

(579 | ) |

(195 | ) |

(128 | ) |

| Effect of exchange rate

changes on cash and cash equivalents | |

| |

(3 | ) | |

(1 | ) | |

(3 | ) | |

(31 | ) |

(38 | ) | |

14 | | |

(51 | ) | |

| 21 | | |

(3 | ) |

(19 | ) |

(8 | ) |

(8 | ) |

6 | |

(10 | ) |

| | |

| |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | | |

| |

| |

| |

| |

| |

| |

| Net (decrease) increase

in cash and cash equivalents, during the period | |

| |

(952 | ) | |

(332 | ) | |

(562 | ) | |

132 | |

(1,714 | ) | |

1,195 | | |

(1,148 | ) | |

| (259 | ) | |

176 | |

(36 | ) |

319 | |

(518 | ) |

62 | |

(137 | ) |

| | |

| |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | | |

| |

| |

| |

| |

| |

| |

| Cash and cash equivalents,

beginning of period | |

| |

2,948 | | |

1,996 | | |

1,664 | | |

1,102 | |

2,948 | | |

1,234 | | |

2,429 | | |

| 1,281 | | |

1,022 | |

1,234 | |

1,198 | |

1,517 | |

999 | |

1,198 | |

| Cash and cash equivalents,

end of period | |

| |

1,996 | | |

1,664 | | |

1,102 | | |

1,234 | |

1,234 | | |

2,429 | | |

1,281 | | |

| 1,022 | | |

1,198 | |

1,198 | |

1,517 | |

999 | |

1,061 | |

1,061 | |

| Q3 2024 Financial Review of Magna International Inc. | Page 3 of 8 | Prepared as at 10/31/24 |

FINANCIAL

REVIEW OF MAGNA INTERNATIONAL INC.

(United

States dollars in millions, except per share figures) (Unaudited)

This

Analyst should be read in conjunction with the audited consolidated financial statements for the year ended December 31, 2023.

Note

1: OTHER EXPENSE (INCOME), NET

Other

expense (income), net consists of:

| | |

| |

2022 | |

2023 | |

2024 | |

| | |

| |

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q | |

TOTAL | |

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q | |

TOTAL | |

1st

Q | |

2nd

Q | |

3rd

Q | |

TOTAL | |

| Impacts

related to Fisker Inc. [“Fisker”] | |

[a] | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

316 | |

19 | |

(189 | ) |

146 | |

| Restructuring

activities | |

[b] | |

- | |

- | |

- | |

22 | |

22 | |

118 | |

(35 | ) |

(1 | ) |

66 | |

148 | |

38 | |

55 | |

- | |

93 | |

| Investment

revaluations, (gains) losses on sales, and impairments | |

[c] | |

61 | |

50 | |

9 | |

101 | |

221 | |

24 | |

98 | |

(19 | ) |

98 | |

201 | |

2 | |

3 | |

1 | |

6 | |

| Gain

on business combination | |

[d] | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

(9 | ) |

- | |

(9 | ) |

| Impairments

and loss on sale of operations in Russia | |

[e] | |

- | |

376 | |

- | |

- | |

376 | |

- | |

- | |

16 | |

- | |

16 | |

- | |

- | |

- | |

- | |

| Veoneer

AS transaction costs | |

[f] | |

- | |

- | |

- | |

- | |

- | |

- | |

23 | |

- | |

- | |

23 | |

- | |

- | |

- | |

- | |

| Loss

on sale of business | |

[g] | |

- | |

- | |

- | |

58 | |

58 | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

| Impairments | |

[h] | |

- | |

- | |

14 | |

12 | |

26 | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

| | |

| |

61 | |

426 | |

23 | |

193 | |

703 | |

142 | |

86 | |

(4 | ) |

164 | |

388 | |

356 | |

68 | |

(188 | ) |

236 | |

| |

[a] |

Impacts related to Fisker Inc. [“Fisker”] |

During

2024, Fisker filed for Chapter 11 bankruptcy protection in the United States and for similar protection in Austria. In connection with

this, the Company recorded impairment charges on its Fisker related assets during the year, as well as restructuring charges in the first

quarter of 2024. In the course of such bankruptcy proceedings, the Company terminated its manufacturing agreement for the Fisker Ocean

SUV during the third quarter of 2024, as a result of which the Company recognized $196 million of previously deferred revenue related

to its Fisker warrants.

| |

Impairment of Fisker related assets: |

During

the first quarter of 2024, the Company recorded a $261 million impairment charge on its Fisker related assets including production

receivables, inventory, fixed assets and other capitalized expenditures. In connection with purchase obligations and supplier

settlements related to the Fisker program, the Company recorded an additional $19 million of charges in the second quarter of 2024,

and $7 million of charges in the third quarter of 2024. For the nine months ended September 30, 2024, impairment charges totaled

$287 million [$225 million after tax] on the Company's Fisker related assets.

| |

Impairment of Fisker warrants and recognition of related deferred revenue: |

Fisker

issued approximately 19.5 million penny warrants to the Company to purchase common stock in connection with our agreements with Fisker

for platform sharing, engineering and manufacturing of the Fisker Ocean SUV. These warrants vested during 2021 and 2022 based on specified

milestones and were marked to market each quarter. During the first quarter of 2024, Magna recorded a $33 million [$25 million after

tax] impairment charge on these warrants reducing the value of the warrants to nil. When the warrants were issued and the vesting provisions

realized, the Company recorded offsetting amounts to deferred revenue within other accrued liabilities and other long-term liabilities.

Portions of this deferred revenue were recognized in income as performance obligations were satisfied. During the third quarter of 2024,

the agreement for manufacturing of the Fisker Ocean SUV was terminated, and the Company recognized the remaining $196 million of previously

deferred revenue in income. Relevant bankruptcy protection laws had prevented the earlier termination of the agreement and the recognition

of the related deferred revenue by the Company.

In

the first quarter of 2024, the Company recorded additional restructuring charges of $22 million in its Complete Vehicles segment in connection

with its Fisker related assembly operations.

| Q3 2024 Financial Review of Magna International Inc. | Page 4 of 8 | Prepared as at 10/31/24 |

| |

[b] |

Restructuring activities |

| | |

2022 |

|

2023 |

|

2024 |

|

| | |

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q | |

TOTAL | |

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q | |

TOTAL | |

1st

Q | |

2nd

Q | |

3rd

Q | |

TOTAL | |

| Power & Vision | |

- | |

- | |

- | |

22 | |

22 | |

105 | |

(44 | ) |

(1 | ) |

57 | |

117 | |

- | |

55 | |

- | |

55 | |

| Complete Vehicles | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

- | |

26 | |

- | |

- | |

26 | |

| Body Exteriors & Structures | |

- | |

- | |

- | |

- | |

- | |

13 | |

9 | |

- | |

9 | |

31 | |

12 | |

- | |

- | |

12 | |

| | |

- | |

- | |

- | |

22 | |

22 | |

118 | |

(35 | ) |

(1 | ) |

66 | |

148 | |

38 | |

55 | |

- | |

93 | |

During

the second quarter of 2024, the Company recorded $35 million of restructuring charges associated with its acquisition of the Veoneer

Active Safety Business [“Veoneer AS”], and $20 million of restructuring charges related to plant closures in its Power &

Vision Segment. During the second and third quarter of 2023, the Company’s Power & Vision segment recorded a $10 million

and $8 million gain on the sale of a building as a result of restructuring activities, respectively. During the second quarter of 2023,

the Company’s Power & Vision segment reversed $39 million of charges due to a change in the restructuring plans related

to a plant closure.

| |

[c] |

Investment revaluations, (gains) losses on sales, and impairments |

The

Company revalues its public and private equity investments and certain public company warrants every quarter. The gains and losses related

to this revaluation, as well as gain and losses on disposition, are primarily recorded in Corporate. In the second quarter of 2023, the

Company recorded a non-cash impairment charge of $85 million on a private equity investment and related long-term receivables within

Other assets in its Corporate segment. In the fourth quarter of 2023, the Company also recorded a non-cash impairment charge

of $5 million on a private equity investment in its Power & Vision segment.

| |

[d] |

Gain on business combination |

During

the second quarter of 2024, the Company acquired a business in the Body Exteriors & Structures segment for $5 million, resulting

in a bargain purchase gain of $9 million.

| |

[e] |

Impairments and loss on sale of operations in Russia |

As a result of the expected

lack of future cashflows and the continuing uncertainties connected with the Russian economy, during the second quarter of 2022, the

Company recorded a $376 million impairment charge related to its investment in Russia. This included net asset impairments of $173 million

and a $203 million reserve against the related foreign currency translation losses that were included in accumulated other comprehensive

loss. The net asset impairments consisted of $163 million and $10 million in our Body Exteriors & Structures and our Seating

Systems segments, respectively.

During the third quarter of 2023, the Company completed the sale of all of its investments in

Russia resulting in a loss of $16 million including a net cash outflow of $23 million.

| |

[f] |

Veoneer AS transaction costs |

During

2023, the Company incurred $23 million of transaction costs related to the acquisition of the Veoneer Active Safety Business.

| |

[g] |

Loss on sale of business |

During

the fourth quarter of 2022, the Company entered into an agreement to sell a European Power & Vision operation. Under the terms

of the arrangement, the Company was contractually obligated to provide the buyer with up to $42 million of funding, resulting in a loss

of $58 million. During the first quarter of 2023, the Company completed the sale of this operation which resulted in a net cash outflow

of $25 million.

| |

|

2022 | |

2023 | |

2024 | |

| |

|

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q | |

TOTAL | |

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q | |

TOTAL | |

1st

Q | |

2nd

Q | |

3rd

Q | |

TOTAL | |

| Body Exteriors &

Structures |

| - | |

- | |

10 | |

12 | |

22 | |

- | |

- |

| - | |

- | |

- | |

- | |

- | |

- | |

- | |

| Power &

Vision |

| - | |

- | |

4 | |

- | |

4 | |

- | |

- |

| - | |

- | |

- | |

- | |

- | |

- | |

- | |

| |

| - | |

- | |

14 | |

12 | |

26 | |

- | |

- |

| - | |

- | |

- | |

- | |

- | |

- | |

- | |

| Q3 2024 Financial Review of Magna International Inc. | Page 5 of 8 | Prepared as at 10/31/24 |

Note 2: NON-GAAP MEASURES

The

Company presents Adjusted EBIT (Earnings before interest, taxes, Other expense (income), net and amortization of acquired intangible

assets); Adjusted Net Income (Net Income before Other expense (income), net, net of tax excluding significant income tax valuation allowance

adjustments, and amortization of acquired intangible assets); Adjusted Diluted Earnings per Share; Adjusted EBIT as a percentage of sales;

Adjusted Return on Invested Capital; and Adjusted Return on Equity. The Company presents these financial figures because such measures

are widely used by analysts and investors in evaluating the operating performance of the Company. However, such measures do

not have any standardized meaning under U.S. generally accepted accounting principles and may not be comparable to the calculation of

similar measures by other companies.

| |

The following table reconciles Income (loss) from operations before income taxes to Adjusted EBIT: |

| |

2022 |

|

2023 | |

2024 |

|

| |

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q | |

TOTAL | |

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q | |

TOTAL | |

1st

Q | |

2nd

Q | |

3rd

Q | |

TOTAL | |

| Income (loss)

from operations before income taxes |

420 | |

(88 | ) |

400 | |

146 | |

878 | |

275 | |

483 | |

538 | |

310 | |

1,606 | |

34 | |

427 | |

700 | |

1,161 | |

| Exclude: |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Amortization of acquired intangible

assets |

12 | |

12 | |

11 | |

11 | |

46 | |

12 | |

13 | |

32 | |

31 | |

88 | |

28 | |

28 | |

28 | |

84 | |

| Other expense (income), net |

61 | |

426 | |

23 | |

193 | |

703 | |

142 | |

86 | |

(4 | ) |

164 | |

388 | |

356 | |

68 | |

(188 | ) |

236 | |

| Interest expense, net |

26 | |

20 | |

18 | |

17 | |

81 | |

20 | |

34 | |

49 | |

53 | |

156 | |

51 | |

54 | |

54 | |

159 | |

| Adjusted EBIT |

519 | |

370 | |

452 | |

367 | |

1,708 | |

449 | |

616 | |

615 | |

558 | |

2,238 | |

469 | |

577 | |

594 | |

1,640 | |

| |

The following table shows the calculation of Adjusted Return on Invested Capital: |

| |

2022 |

|

|

2023 |

|

|

2024 |

|

| |

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q |

|

|

1st

Q | |

2nd

Q | |

3rd

Q | |

4th

Q |

|

|

1st

Q | |

2nd

Q | |

3rd

Q |

|

| Net income (loss) |

379 | |

(145 | ) |

296 | |

111 |

|

|

217 | |

354 | |

417 | |

298 |

|

|

26 | |

328 | |

508 |

|

| Add

(deduct): |

| |

| |

| |

|

|

|

| |

| |

| |

|

|

|

| |

| |

|

|

| Interest

expense, net |

26 | |

20 | |

18 | |

17 |

|

|

20 | |

34 | |

49 | |

53 |

|

|

51 | |

54 | |

54 |

|

| Amortization

of acquired intangible assets |

12 | |

12 | |

11 | |

11 |

|

|

12 | |

13 | |

32 | |

31 |

|

|

28 | |

28 | |

28 |

|

| Other expense

(income), net |

61 | |

426 | |

23 | |

193 |

|

|

142 | |

86 | |

(4 | ) |

164 |

|

|

356 | |

68 | |

(188 |

) |

| Tax

effect on Interest expense, net, Amortization of acquired intangible assets and Other expense, net |

(19 | ) |

(34 | ) |

(11 | ) |

(32 |

) |

|

(38 | ) |

(4 | ) |

(14 | ) |

(46 |

) |

|

(93 | ) |

(32 | ) |

30 |

|

| Adjustments

to Deferred Tax Valuation Allowances |

(29 | ) |

- | |

- | |

- |

|

|

- | |

- | |

- | |

(47 |

) |

|

- | |

- | |

- |

|

| Adjusted After-tax operating

profits |

430 | |

279 | |

337 | |

300 |

|

|

353 | |

483 | |

480 | |

453 |

|

|

368 | |

446 | |

432 |

|

| |

| |

| |

| |

|

|

|

| |

| |

| |

|

|

|

| |

| |

|

|

| Total Assets |

28,822 | |

27,283 | |

26,667 | |

27,789 |

|

|

30,654 | |

31,837 | |

31,675 | |

32,255 |

|

|

32,678 | |

31,986 | |

32,790 |

|

| Excluding: |

| |

| |

| |

|

|

|

| |

| |

| |

|

|

|

| |

| |

|

|

| Cash and

cash equivalents |

(1,996 | ) |

(1,664 | ) |

(1,102 | ) |

(1,234 |

) |

|

(2,429 | ) |

(1,281 | ) |

(1,022 | ) |

(1,198 |

) |

|

(1,517 | ) |

(999 | ) |

(1,061 |

) |

| Deferred

tax assets |

(464 | ) |

(491 | ) |

(488 | ) |

(491 |

) |

|

(506 | ) |

(535 | ) |

(527 | ) |

(621 |

) |

|

(753 | ) |

(807 | ) |

(811 |

) |

| Less Current Liabilities |

(10,440 | ) |

(9,816 | ) |

(9,878 | ) |

(10,998 |

) |

|

(12,045 | ) |

(13,358 | ) |

(13,165 | ) |

(13,234 |

) |

|

(13,566 | ) |

(12,449 | ) |

(12,600 |

) |

| Excluding: |

| |

| |

| |

|

|

|

| |

| |

| |

|

|

|

| |

| |

|

|

| Short-term

borrowing |

- | |

- | |

- | |

8 |

|

|

4 | |

150 | |

2 | |

511 |

|

|

838 | |

848 | |

828 |

|

| Long-term

debt due within one year |

127 | |

105 | |

95 | |

654 |

|

|

668 | |

1,426 | |

1,398 | |

819 |

|

|

824 | |

65 | |

65 |

|

| Current portion of operating lease

liabilities |

276 | |

270 | |

266 | |

276 |

|

|

285 | |

303 | |

384 | |

399 |

|

|

306 | |

306 | |

319 |

|

| Invested Capital |

16,325 | |

15,687 | |

15,560 | |

16,004 |

|

|

16,631 | |

18,542 | |

18,745 | |

18,931 |

|

|

18,810 | |

18,950 | |

19,530 |

|

| |

| |

| |

| |

|

|

|

| |

| |

| |

|

|

|

| |

| |

|

|

| Adjusted

After-tax operating profits |

430 | |

279 | |

337 | |

300 |

|

|

353 | |

483 | |

480 | |

453 |

|

|

368 | |

446 | |

432 |

|

| Average Invested Capital |

16,185 | |

16,006 | |

15,624 | |

15,782 |

|

|

16,318 | |

17,587 | |

18,644 | |

18,838 |

|

|

18,871 | |

18,880 | |

19,240 |

|

| Adjusted Return on Invested

Capital |

10.6 | % |

7.0 | % |

8.6 | % |

7.6 |

% |

|

8.7 | % |

11.0 | % |

10.3 | % |

9.6 |

% |

|

7.8 | % |

9.4 | % |

9.0 |

% |

| Q3 2024 Financial Review of Magna International Inc. | Page 6 of 8 | Prepared as at 10/31/24 |

Note

2: NON-GAAP MEASURES (Continued)

The

following table shows the calculation of Adjusted Return on Equity:

| | |

2022 | | |

2023 | | |

2024 | |

| | |

1st

Q | | |

2nd

Q | | |

3rd

Q | | |

4th

Q | | |

1st

Q | | |

2nd

Q | | |

3rd

Q | | |

4th

Q | | |

1st

Q | | |

2nd

Q | | |

3rd

Q | |

| Net income (loss)

attributable to Magna International Inc. | |

| 364 | | |

| (156 | ) | |

| 289 | | |

| 95 | | |

| 209 | | |

| 339 | | |

| 394 | | |

| 271 | | |

| 9 | | |

| 313 | | |

| 484 | |

| Add (deduct): | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Amortization

of acquired intangible assets | |

| 12 | | |

| 12 | | |

| 11 | | |

| 11 | | |

| 12 | | |

| 13 | | |

| 32 | | |

| 31 | | |

| 28 | | |

| 28 | | |

| 28 | |

| Other expense

(income), net | |

| 61 | | |

| 426 | | |

| 23 | | |

| 193 | | |

| 142 | | |

| 86 | | |

| (4 | ) | |

| 164 | | |

| 356 | | |

| 68 | | |

| (188 | ) |

| Tax

effect on Amortization of acquired intangible assets and Other expense, net | |

| (15 | ) | |

| (29 | ) | |

| (6 | ) | |

| (29 | ) | |

| (34 | ) | |

| 3 | | |

| (3 | ) | |

| (36 | ) | |

| (82 | ) | |

| (20 | ) | |

| 45 | |

| Adjustments

to Deferred Tax Valuation Allowances | |

| (29 | ) | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (47 | ) | |

| - | | |

| - | | |

| - | |

| Adjusted

Net income (loss) attributable to Magna International Inc. | |

| 393 | | |

| 253 | | |

| 317 | | |

| 270 | | |

| 329 | | |

| 441 | | |

| 419 | | |

| 383 | | |

| 311 | | |

| 389 | | |

| 369 | |

| Average Shareholder's

Equity | |

| 11,599 | | |

| 11,692 | | |

| 11,095 | | |

| 11,091 | | |

| 11,412 | | |

| 11,573 | | |

| 11,704 | | |

| 12,015 | | |

| 12,101 | | |

| 11,967 | | |

| 12,349 | |

| Adjusted

Return on Equity | |

| 13.6 | % | |

| 8.7 | % | |

| 11.4 | % | |

| 9.7 | % | |

| 11.5 | % | |

| 15.2 | % | |

| 14.3 | % | |

| 12.8 | % | |

| 10.3 | % | |

| 13.0 | % | |

| 12.0 | % |

The following table reconciles Net income (loss) attributable to Magna International Inc. to Adjusted

net income attributable to Magna International Inc.:

| | |

2022 |

|

|

2023 | | |

2024 | |

| | |

1st Q | | |

2nd Q | | |

3rd Q | | |

4th Q | | |

TOTAL | | |

1st Q | | |

2nd Q | | |

3rd Q | | |

4th Q | | |

TOTAL | | |

1st Q | | |

2nd Q | | |

3rd Q | | |

TOTAL | |

| Net income (loss) attributable to Magna International

Inc. | |

| 364 | | |

| (156 | ) | |

| 289 | | |

| 95 | | |

| 592 | | |

| 209 | | |

| 339 | | |

| 394 | | |

| 271 | | |

| 1,213 | | |

| 9 | | |

| 313 | | |

| 484 | | |

| 806 | |

| Exclude: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Amortization of acquired intangible assets | |

| 10 | | |

| 10 | | |

| 9 | | |

| 9 | | |

| 38 | | |

| 10 | | |

| 11 | | |

| 25 | | |

| 25 | | |

| 71 | | |

| 22 | | |

| 23 | | |

| 22 | | |

| 67 | |

| Impacts related to Fisker Inc. [“Fisker”] | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 247 | | |

| 15 | | |

| (140 | ) | |

| 122 | |

| Investment revaluations, (gains) losses

on sales, and impairments | |

| 48 | | |

| 38 | | |

| 7 | | |

| 75 | | |

| 168 | | |

| 18 | | |

| 95 | | |

| (14 | ) | |

| 74 | | |

| 173 | | |

| 1 | | |

| 2 | | |

| 3 | | |

| 6 | |

| Restructuring activities | |

| - | | |

| - | | |

| - | | |

| 22 | | |

| 22 | | |

| 92 | | |

| (26 | ) | |

| (2 | ) | |

| 60 | | |

| 124 | | |

| 32 | | |

| 45 | | |

| - | | |

| 77 | |

| Gain on business combination | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (9 | ) | |

| - | | |

| (9 | ) |

| Impairments and loss on sale of operations

in Russia | |

| - | | |

| 361 | | |

| - | | |

| - | | |

| 361 | | |

| - | | |

| - | | |

| 16 | | |

| - | | |

| 16 | | |

| - | | |

| - | | |

| - | | |

| - | |

| Veoneer AS transaction costs | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 22 | | |

| - | | |

| - | | |

| 22 | | |

| - | | |

| - | | |

| - | | |

| - | |

| Impairments | |

| - | | |

| - | | |

| 12 | | |

| 12 | | |

| 24 | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | |

| Net losses on the sale of business | |

| - | | |

| - | | |

| - | | |

| 57 | | |

| 57 | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | |

| Adjustments to Deferred

Tax Valuation Allowance | [i] |

| (29 | ) | |

| - | | |

| - | | |

| - | | |

| (29 | ) | |

| - | | |

| - | | |

| - | | |

| (47 | ) | |

| (47 | ) | |

| - | | |

| - | | |

| - | | |

| - | |

| Adjusted net income attributable

to Magna International Inc. | |

| 393 | | |

| 253 | | |

| 317 | | |

| 270 | | |

| 1,233 | | |

| 329 | | |

| 441 | | |

| 419 | | |

| 383 | | |

| 1,572 | | |

| 311 | | |

| 389 | | |

| 369 | | |

| 1,069 | |

The following table reconciles diluted earnings (loss) per common share to Adjusted diluted earnings

per common share:

| | |

2022 |

|

|

2023 | | |

2024 | |

| | |

1st Q | | |

2nd Q | | |

3rd Q | | |

4th Q | | |

TOTAL | | |

1st Q | | |

2nd Q | | |

3rd Q | | |

4th Q | | |

TOTAL | | |

1st Q | | |

2nd Q | | |

3rd Q | | |

TOTAL | |

| Diluted earnings (loss) per common share | |

$ | 1.22 | | |

$ | (0.54 | ) | |

$ | 1.00 | | |

$ | 0.33 | | |

$ | 2.03 | | |

$ | 0.73 | | |

$ | 1.18 | | |

$ | 1.37 | | |

$ | 0.95 | | |

$ | 4.23 | | |

$ | 0.03 | | |

| 1.09 | | |

| 1.68 | | |

$ | 2.81 | |

| Exclude: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Amortization of acquired intangible assets | |

| 0.04 | | |

| 0.03 | | |

| 0.03 | | |

| 0.03 | | |

| 0.13 | | |

| 0.04 | | |

| 0.04 | | |

| 0.09 | | |

| 0.09 | | |

| 0.25 | | |

| 0.08 | | |

| 0.08 | | |

| 0.08 | | |

| 0.23 | |

| Impacts related to Fisker Inc. [“Fisker”] | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 0.86 | | |

| 0.05 | | |

| (0.49 | ) | |

| 0.42 | |

| Investment revaluations, (gains) losses

on sales, and impairments | |

| 0.16 | | |

| 0.13 | | |

| 0.03 | | |

| 0.26 | | |

| 0.58 | | |

| 0.07 | | |

| 0.33 | | |

| (0.06 | ) | |

| 0.25 | | |

| 0.60 | | |

| - | | |

| 0.01 | | |

| 0.01 | | |

| 0.02 | |

| Restructuring activities | |

| - | | |

| - | | |

| - | | |

| 0.08 | | |

| 0.08 | | |

| 0.31 | | |

| (0.09 | ) | |

| - | | |

| 0.20 | | |

| 0.43 | | |

| 0.11 | | |

| 0.15 | | |

| - | | |

| 0.27 | |

| Gain on business combination | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (0.03 | ) | |

| - | | |

| (0.03 | ) |

| Impairments and loss on sale of operations

in Russia | |

| - | | |

| 1.24 | | |

| - | | |

| - | | |

| 1.24 | | |

| - | | |

| - | | |

| 0.06 | | |

| - | | |

| 0.06 | | |

| - | | |

| - | | |

| - | | |

| - | |

| Veoneer AS transaction costs | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 0.08 | | |

| - | | |

| - | | |

| 0.08 | | |

| - | | |

| - | | |

| - | | |

| - | |

| Impairments | |

| - | | |

| - | | |

| 0.04 | | |

| 0.04 | | |

| 0.08 | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | |

| Net losses on the sale of business | |

| - | | |

| - | | |

| - | | |

| 0.20 | | |

| 0.20 | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | |

| Adjustments to Deferred Tax Valuation

Allowance | [i] |

| (0.10 | ) | |

| - | | |

| - | | |

| - | | |

| (0.10 | ) | |

| - | | |

| - | | |

| - | | |

| (0.16 | ) | |

| (0.16 | ) | |

| - | | |

| - | | |

| - | | |

| - | |

| Adjusted diluted earnings per common share | |

$ | 1.32 | | |

$ | 0.87 | | |

$ | 1.10 | | |

$ | 0.94 | | |

$ | 4.24 | | |

$ | 1.15 | | |

$ | 1.54 | | |

$ | 1.46 | | |

$ | 1.33 | | |

$ | 5.49 | | |

$ | 1.08 | | |

$ | 1.35 | | |

$ | 1.28 | | |

$ | 3.72 | |

[i] Adjustments to Deferred Tax Valuation Allowance

The Company records quarterly adjustments to the valuation allowance against its deferred tax assets in

continents like North America, Europe, Asia, and South America. The net effect of these adjustments is a reduction to income tax expense.

| Q3 2024 Financial Review of Magna International Inc. | Page 7 of 8 | Prepared as at 10/31/24 |

Note

3: SEGMENTED INFORMATION

| |

2022 | | |

2023 | | |

2024 | |

| |

1st

Q | | |

2nd

Q | | |

3rd

Q | | |

4th

Q | | |

TOTAL | | |

1st

Q | | |

2nd

Q | | |

3rd

Q | | |

4th

Q | | |

TOTAL | | |

1st

Q | | |

2nd

Q | | |

3rd

Q | | |

TOTAL | |

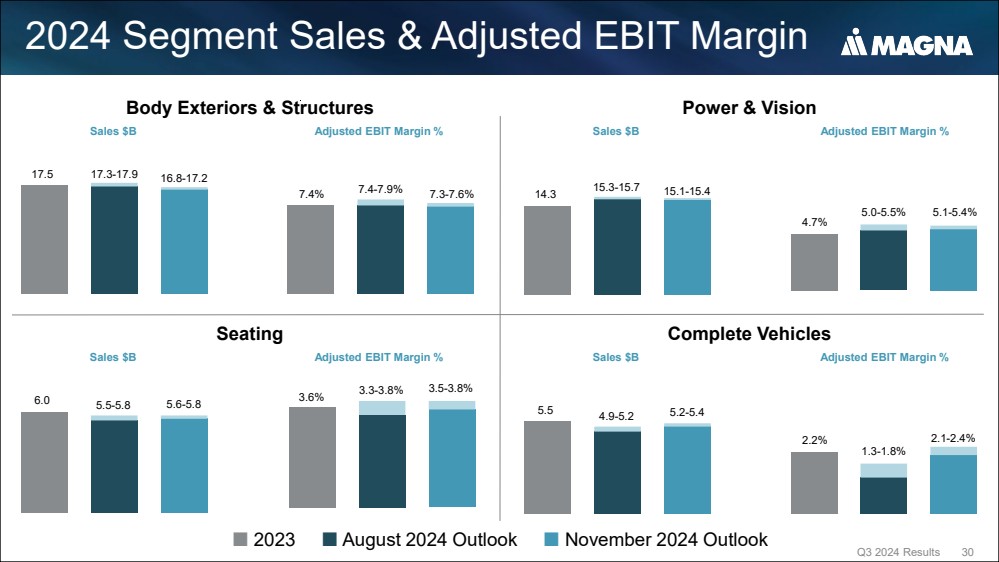

| Body Exteriors &

Structures |

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Sales |

| 4,077 | | |

3,947 | | |

3,976 | | |

4,004 | | |

16,004 | | |

4,439 | | |

4,540 | | |

4,354 | | |

4,178 | | |

17,511 | | |

4,429 | | |

4,465 | | |

4,038 | | |

12,932 | |

| Adjusted

EBIT |

| 231 | | |

194 | | |

227 | | |

200 | | |

852 | | |

272 | | |

394 | | |

358 | | |

280 | | |

1,304 | | |

298 | | |

341 | | |

273 | | |

912 | |

| Adjusted

EBIT as a percentage of sales |

| 5.7 | % | |

4.9 | % | |

5.7 | % | |

5.0 | % | |

5.3 | % | |

6.1 | % | |

8.7 | % | |

8.2 | % | |

6.7 | % | |

7.4 | % | |

6.7 | % | |

7.6 | % | |

6.8 | % | |

7.1 | % |

| |

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Power & Vision |

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Sales |

| 3,046 | | |

2,888 | | |

2,911 | | |

3,016 | | |

11,861 | | |

3,323 | | |

3,462 | | |

3,745 | | |

3,775 | | |

14,305 | | |

3,842 | | |

3,926 | | |

3,837 | | |

11,605 | |

| Adjusted

EBIT |

| 163 | | |

99 | | |

124 | | |

116 | | |

502 | | |

92 | | |

124 | | |

221 | | |

231 | | |

668 | | |

98 | | |

198 | | |

279 | | |

575 | |

| Adjusted

EBIT as a percentage of sales |

| 5.4 | % | |

3.4 | % | |

4.3 | % | |

3.8 | % | |

4.2 | % | |

2.8 | % | |

3.6 | % | |

5.9 | % | |

6.1 | % | |

4.7 | % | |

2.6 | % | |

5.0 | % | |

7.3 | % | |

5.0 | % |

| |

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Seating Systems |

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Sales |

| 1,376 | | |

1,253 | | |

1,295 | | |

1,345 | | |

5,269 | | |

1,486 | | |

1,603 | | |

1,529 | | |

1,429 | | |

6,047 | | |

1,455 | | |

1,455 | | |

1,379 | | |

4,289 | |

| Adjusted

EBIT |

| 50 | | |

3 | | |

37 | | |

14 | | |

104 | | |

37 | | |

67 | | |

70 | | |

44 | | |

218 | | |

52 | | |

53 | | |

51 | | |

156 | |

| Adjusted

EBIT as a percentage of sales |

| 3.6 | % | |

0.2 | % | |

2.9 | % | |

1.0 | % | |

2.0 | % | |

2.5 | % | |

4.2 | % | |

4.6 | % | |

3.1 | % | |

3.6 | % | |

3.6 | % | |

3.6 | % | |

3.7 | % | |

3.6 | % |

| |

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Complete Vehicles |

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Sales |

| 1,275 | | |

1,403 | | |

1,213 | | |

1,330 | | |

5,221 | | |

1,626 | | |

1,526 | | |

1,185 | | |

1,201 | | |

5,538 | | |

1,383 | | |

1,242 | | |

1,159 | | |

3,784 | |

| Adjusted

EBIT |

| 50 | | |

63 | | |

65 | | |

57 | | |

235 | | |

52 | | |

34 | | |

(5 | ) | |

43 | | |

124 | | |

27 | | |

20 | | |

27 | | |

74 | |

| Adjusted

EBIT as a percentage of sales |

| 3.9 | % | |

4.5 | % | |

5.4 | % | |

4.3 | % | |

4.5 | % | |

3.2 | % | |

2.2 | % | |

-0.4 | % | |

3.6 | % | |

2.2 | % | |

2.0 | % | |

1.6 | % | |

2.3 | % | |

2.0 | % |

| |

| | | |

| | |