Filed

Pursuant to Rule 424(b)(5)

Registration

No. 333-262181

PROSPECTUS

SUPPLEMENT

(To

Prospectus dated July 1, 2022 and

Prospectus

Supplement dated July 17, 2023)

TAOPING

INC.

80,000

Ordinary Shares

Pursuant

to this prospectus supplement, the accompanying prospectus supplement and the accompanying base prospectus, we are offering 80,000 ordinary

shares to SHANJING CAPITAL GROUP CO., LTD (the “Investor”) at a price of approximately $4.626 per share, pursuant to our

previously announced Standby Equity Purchase Agreement with the Investor dated July 17, 2023 (the “SEPA”). The total purchase

price and proceeds we will receive from the sale of the shares is $370,080. These shares are being issued as part of the commitment by

Investor to purchase from time to time, at our option, up to $1,000,000 of our ordinary shares pursuant to the SEPA, as described in

Prospectus Supplement dated July 17, 2023. We expect to issue the shares to Investor on or about August 3, 2023.

In

addition to our issuance of the shares to the Investor pursuant to the SEPA, this prospectus supplement, the accompanying prospectus

supplement and the accompanying prospectus also cover the sale of these shares by the Investor to the public. Though we have been advised

by the Investor, and the Investor represents in the SEPA, that the Investor is purchasing the shares for its own account, for investment

purposes in which it takes investment risk (including, without limitation, the risk of loss), and without any view or intention to distribute

such shares in violation of the Securities Act of 1933, as amended (the “Securities Act”) or any other applicable securities

laws, the Securities and Exchange Commission (the “SEC”) may take the position that the Investor may be deemed an “underwriter”

within the meaning of Section 2(a)(11) of the Securities Act and any profits on the sales of shares of our ordinary shares by the Investor

and any discounts, commissions or concessions received by the Investor are deemed to be underwriting discounts and commissions under

the Securities Act. For additional information on the methods of sale that may be used by the Investor, see the section entitled “Plan

of Distribution” on page S-6 of the accompanying prospectus supplement.

Our

ordinary shares are listed on the Nasdaq Capital Market under the symbol “TAOP.” Effective at the market opening on August

1, 2023, the Company implemented a one-for-ten reverse stock split of its issued and outstanding ordinary shares where every ten ordinary

shares outstanding were automatically combined and converted into one issued and outstanding ordinary share. Any fractional shares resulting

from the reverse stock split were rounded up to the nearest whole share. The reverse stock split was intended to increase the per share

trading price of the Company’s ordinary shares to satisfy the $1.00 minimum bid price requirement for continued listing on the

NASDAQ Stock Market. Immediately following the reverse stock split, the Company had approximately 1,864,554 ordinary shares outstanding.

On August 1, 2023, the closing price of our ordinary

shares was $4.90 per share. The aggregate market value of our outstanding ordinary shares held by non-affiliates is $9,349,694, based

on 1,864,554 ordinary shares outstanding as of the date of this prospectus supplement, of which 1,236,732 are held by non-affiliates,

and $7.56, which was closing price of the ordinary shares on June 22, 2023. Pursuant to General Instruction I.B.5 of Form F-3, in no

event will the aggregate market value of securities sold by us or on our behalf pursuant to General Instruction I.B.5 of Form F-3 during

the 12 calendar month period immediately prior to, and including, the date of any such sale exceed one-third of the aggregate market

value of our ordinary shares held by non-affiliates, calculated in accordance with General Instruction I.B.5 of Form F-3. During the

12 calendar month period that ends on and includes the date hereof, we have not sold securities pursuant to General Instruction I.B.5

of Form F-3.

Investing

in our securities involves a high degree of risk. Before buying any securities, you should review carefully the risks and uncertainties

described under the heading “Risk Factors” beginning on page S-4 of the accompanying prospectus supplement and in the documents

incorporated by reference into this prospectus supplement, the accompanying prospectus supplement and the accompanying prospectus.

Neither

the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined

if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The

date of this prospectus supplement is August 1, 2023

TABLE

OF CONTENTS

PROSPECTUS

SUPPLEMENT

PROSPECTUS

SUPPLEMENT DATED JULY 17, 2023

PROSPECTUS

You

should rely only on the information contained in this prospectus supplement, the accompanying prospectus supplement and the accompanying

prospectus. Neither we nor the Investor have not authorized anyone else to provide you with additional or different information. We are

offering to sell, and seeking offers to buy the securities only in jurisdictions where offers and sales are permitted. You should not

assume that the information in this prospectus supplement, the accompanying prospectus supplement or the accompanying prospectus is accurate

as of any date other than the date on the front of those documents or that any document incorporated by reference is accurate as of any

date other than its filing date.

No

action is being taken in any jurisdiction outside the United States to permit a public offering of the securities or possession or distribution

of this prospectus supplement, the accompanying prospectus supplement or the accompanying prospectus in that jurisdiction. Persons who

come into possession of this prospectus supplement, the accompanying prospectus supplement or the accompanying prospectus in jurisdictions

outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution

of this prospectus supplement, the accompanying prospectus supplement and the accompanying prospectus applicable to that jurisdiction.

THE

OFFERING

| Securities

Offered |

|

80,000

ordinary shares of Taoping Inc. |

| |

|

|

| Purchaser |

|

SHANJING

CAPITAL GROUP CO., LTD pursuant to the Standby Equity Purchase Agreement dated July 17, 2023 |

| |

|

|

| Purchase

price |

|

Approximately

$4.626 per share |

| |

|

|

| Proceeds |

|

$370,080 |

| |

|

|

| Use

of Proceeds |

|

We

intend to use the net proceeds, if any, from this offering for working capital and general corporate purposes. Our management will

have broad discretion in the application of net proceeds, if any. See “Use of Proceeds” in the accompanying prospectus

supplement. |

| |

|

|

| Symbol

for our ordinary shares on Nasdaq |

|

“TAOP”

|

| |

|

|

| Resale |

|

This

prospectus supplement, the accompanying prospectus supplement and the accompanying prospectus also cover the resale of shares by

the Investor to the public. See “Plan of Distribution” in the accompanying prospectus supplement. |

Filed

Pursuant to Rule 424(b)(2)

Registration

No. 333-262181

PROSPECTUS

SUPPLEMENT

(To

Prospectus dated July 1, 2022)

TAOPING

INC.

Up

to $1,000,000 of Ordinary Shares

43,394

Ordinary Shares

Taoping

Inc. (the “Company”) entered into a Standby Equity Purchase Agreement with SHANJING CAPITAL GROUP CO., LTD (the “Investor”)

on July 17, 2023 (the “SEPA”). Pursuant to the SEPA, the Company shall have the right, but not the obligation, to sell to

the Investor up to $1,000,000 of the Company’s ordinary shares, no par value (the “Advance Shares”), offered by this

prospectus supplement and the accompanying prospectus at the Company’s request any time during the commitment period commencing

on July 17, 2023 and terminating on the earliest of (i) the first day of the month following the 24-month anniversary of the date of

the SEPA and (ii) the date on which the Investor shall have made payment of advances requested pursuant to the SEPA for the Company’s

ordinary shares equal to the commitment amount of $1,000,000 (the “Commitment Period”). The Advance Shares would be purchased

at 85.0% of the Market Price (as defined below), provided that in no event shall such purchase price be less than $0.20 per share (the

“Floor Price”), and would be subject to certain limitations, including that the Investor could not purchase any shares that

would result in it owning more than 4.99% of the Company’s outstanding ordinary shares. As defined in the SEPA, “Market Price”

means the number obtained when the aggregate value of the Company’s ordinary shares (each trading day closing price times the number

of shares traded in such trading day) traded on the Nasdaq Stock Market during the five (5) trading days immediately preceding the date

set forth in any notice requesting an advance, is divided by the total number of ordinary shares traded during such five (5) trading

days’ period.

In

connection with the execution of the SEPA, the Company agreed to issue an aggregate of 43,394 ordinary shares of the Company (the “Commitment

Fee Shares”) to the Investor as consideration for its irrevocable commitment to purchase the Advance Shares upon the terms and

subject to the satisfaction of the conditions set forth in the SEPA.

This

prospectus supplement and the accompanying prospectus also cover the sale of these shares by the Investor to the public. Though we have

been advised by the Investor, and the Investor represents in the SEPA, that the Investor is purchasing the shares for its own account,

for investment purposes in which it takes investment risk (including, without limitation, the risk of loss), and without any view or

intention to distribute such shares in violation of the Securities Act of 1933, as amended (the “Securities Act”) or any

other applicable securities laws, the Securities and Exchange Commission (the “SEC”) may take the position that the Investor

may be deemed an “underwriter” within the meaning of Section 2(a)(11) of the Securities Act and any profits on the sales

of shares of our ordinary shares by the Investor and any discounts, commissions or concessions received by the Investor are deemed to

be underwriting discounts and commissions under the Securities Act. For additional information on the methods of sale that may be used

by the Investor, see the section entitled “Plan of Distribution” on page S-6.

Our

ordinary shares are listed on the Nasdaq Capital Market under the symbol “TAOP.” On July 14, 2023, the closing price of our

ordinary shares was $0.565 per share. The aggregate market value of our outstanding ordinary shares held by non-affiliates

is $8,988,665, based on 18,167,973 ordinary shares outstanding as of the date of this prospectus supplement, of which 11,889,769

are held by non-affiliates, and $0.756, which was closing price of the ordinary shares on June 22, 2023. Pursuant to General Instruction

I.B.5 of Form F-3, in no event will the aggregate market value of securities sold by us or on our behalf pursuant to General Instruction

I.B.5 of Form F-3 during the 12 calendar month period immediately prior to, and including, the date of any such sale exceed one-third

of the aggregate market value of our ordinary shares held by non-affiliates, calculated in accordance with General Instruction

I.B.5 of Form F-3. During the 12 calendar month period that ends on and includes the date hereof, we have not sold securities pursuant

to General Instruction I.B.5 of Form F-3.

Investing

in our securities involves a high degree of risk. Before buying any securities, you should review carefully the risks and uncertainties

described under the heading “Risk Factors” beginning on page S-4 of this prospectus supplement and in the documents incorporated

by reference into this prospectus supplement and the accompanying prospectus.

Neither

the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined

if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The

date of this prospectus supplement is July 17, 2023

TABLE

OF CONTENTS

You

should rely only on the information contained in this prospectus supplement and the accompanying prospectus. We have not authorized anyone

else to provide you with additional or different information. We are offering to sell, and seeking offers to buy the securities only

in jurisdictions where offers and sales are permitted. You should not assume that the information in this prospectus supplement or the

accompanying prospectus is accurate as of any date other than the date on the front of those documents or that any document incorporated

by reference is accurate as of any date other than its filing date.

No

action is being taken in any jurisdiction outside the United States to permit a public offering of the securities or possession or distribution

of this prospectus supplement or the accompanying prospectus in that jurisdiction. Persons who come into possession of this prospectus

supplement or the accompanying prospectus in jurisdictions outside the United States are required to inform themselves about and to observe

any restrictions as to this offering and the distribution of this prospectus supplement and the accompanying prospectus applicable to

that jurisdiction.

ABOUT

THIS PROSPECTUS SUPPLEMENT

This

prospectus supplement and the accompanying prospectus are part of a “shelf” registration statement on F-3 (File No. 333-262181)

that we initially filed with the SEC on January 14, 2022, and which was declared effective on July 1, 2022. Under this shelf registration

process, we may, from time to time, sell any combination of the securities described in the accompanying prospectus in one or more offerings

up to a total dollar amount of $100,000,000.

This

document contains two parts. The first part consists of this prospectus supplement, which describes the specific terms of this offering

and the securities offered. The second part, the accompanying prospectus which is dated July 1, 2022, provides more general information,

some of which may not apply to this offering. If the description of the offering varies between this prospectus supplement and the accompanying

prospectus, you should rely on the information in this prospectus supplement.

Before

purchasing any of our ordinary shares, you should carefully read both this prospectus supplement and the accompanying prospectus, together

with the additional information described under the heading “Where You Can Find More Information.”

FORWARD-LOOKING

INFORMATION

This

prospectus supplement contains “forward-looking statements” that involve substantial risks and uncertainties. All statements

other than statements of historical facts contained in this prospectus supplement, including statements regarding our future results

of operations and financial position, strategy and plans, and our expectations for future operations, are forward-looking statements

within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange

Act. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,”

“can,” “continue,” “could,” “estimates,” “expects,” “intends,”

“may,” “plans,” “potential,” “predicts,” “should,” or “will”

or the negative of these terms or other comparable terminology. Our actual results may differ materially or perhaps significantly from

those discussed herein, or implied by, these forward-looking statements.

Any

forward looking statements contained in this prospectus supplement, accompanying prospectus and the documents that we have filed with

the SEC that are incorporated by reference in this prospectus supplement are only estimates or predictions of future events based on

information currently available to our management and management’s current beliefs about the potential outcome of future events.

Whether these future events will occur as management anticipates, whether we will achieve our business objectives, and whether our revenues,

operating results, or financial condition will improve in future periods are subject to numerous risks. There are a number of important

factors that could cause actual results to differ materially from the results anticipated by these forward-looking statements. These

important factors include those that we discuss under the heading “Risk Factors” and in other sections of our Annual Report

on Form 20-F for the fiscal year ended December 31, 2022, as well as in our other SEC filings that are incorporated by reference into

this prospectus supplement and the accompanying prospectus. You should read these factors and the other cautionary statements made in

this prospectus supplement, the accompanying prospectus and in the documents we incorporate by reference into this prospectus supplement

and the accompanying prospectus as being applicable to all related forward-looking statements wherever they appear in this prospectus

supplement or the documents we incorporate by reference into this prospectus supplement and the accompanying prospectus. If one or more

of these factors materialize, or if any underlying assumptions prove incorrect, our actual results, performance or achievements may vary

materially from any future results, performance or achievements expressed or implied by these forward-looking statements. We undertake

no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise,

except as required by law.

PROSPECTUS

SUPPLEMENT SUMMARY

This

summary highlights certain information contained elsewhere, or incorporated by reference, in this prospectus supplement and the accompanying

prospectus. As a result, this summary is not complete and does not contain all of the information that you should consider before investing

in our ordinary shares. You should read the following summary in conjunction with the more detailed information contained in this prospectus

supplement, the accompanying prospectus and the documents incorporated by reference, which are described under “Where You Can Find

More Information” in this prospectus supplement. This prospectus supplement and the accompanying prospectus contain or incorporate

forward-looking statements. Forward-looking statements should be read with the cautionary statements and important factors included under

“Risk Factors” and “Forward-Looking Information” in this prospectus supplement as well as the “Risk Factors”

sections in our Annual Report on Form 20-F for the year ended December 31, 2022 and in other reports that we file with the SEC from time

to time. In this prospectus supplement, except as otherwise indicated or as the context otherwise requires, “the Company,”

“we,” “our” and “us” refer to Taoping Inc. and its subsidiaries.

TAOPING

INC.

Company

Overview

Executive

Offices of the Company currently are located in Shenzhen, China.

We

are a leading provider of cloud-app technologies for Smart City IoT platforms, digital advertising delivery, and other internet-based

information distribution systems in China. Our Internet ecosystem enables all participants of the new media community to efficiently

promote branding, disseminate information, and exchange resources. In addition, we provide a broad portfolio of software and hardware

with fully integrated solutions, including Information Technology infrastructure, Internet-enabled display technologies, and IoT platforms

to customers in government, education, residential community management, media, transportation, and other private sectors.

Prior

to 2014, we generated the majority of our revenues through selling our products and services mostly to the public service entities to

help them improve their operational efficiency and service quality. Our representative customers included the China Ministry of Public

Security, provincial bureaus of public security, fire departments, traffic bureaus, police stations, human resource departments, urban

planning boards, civic administrations, land resource administrations, mapping and surveying bureaus, and the Shenzhen General Station

of Immigration Frontier Inspection.

Since

2014, we have expanded and diversified our customer base into the private sector as well. Our customers in the private sector include,

among others, elevator maintenance companies, residential community management, advertising agencies, auto dealerships, and educational

institutes. Our new corporate mission is to make publicity accessible and affordable for businesses of all sizes.

Previously,

we generated revenues primarily from sales of hardware products, software products, system integration services, and related maintenance

and support services. In 2015, with the introduction of our cloud-based software as a service (SaaS) offering, we started to generate

additional recurring monthly revenues from SaaS fees. In 2019 and 2020, only a very small portion of our revenue was generated from SaaS.

The revenue from SaaS has increased in the following years with the nationwide roll-out of our cloud-based ad display terminal network.

In

May 2017, we completed our transformation to a provider of CAT and IoT technology based digital advertising distribution network and

new media resource sharing platform, and offered an end-to-end digital advertising solution enabling customers to efficiently and cost-effectively

direct advertisements to specific interactive ad display terminals in the out-of-home advertising market across China. In 2017, we became

profitable as a result of a successful transition of our business model. We continued to improve our financial position in 2018. However,

due to the unfavorable macro-economic environment and the slowdown of the out-of-home advertising market in China, we had net loss of

approximately $7.1 million, $9.9 million and $18.3 million respectively in 2022, 2021, and 2020. Going forward, we intend to continue

to execute our business plan and build a nationwide cloud-based ad terminal network by penetrating into more cities throughout China,

which is expected to generate recurring service revenue for the Company, in addition to equipment sales.

On

June 9, 2021, the Company consummated an acquisition of 100% of the equity interest of Taoping New Media Co., Ltd (“TNM”),

a leading media operator in China’s out-of-home digital advertising industry. Mr. Jianghuai Lin, the Chairman, CEO and a principal

shareholder of the Company, owned approximately 51% of TNM. TNM focuses on digital life scenes and mainly is engaged in selling out-of-home

advertising time slots on its networked smart digital advertising display terminals with artificial intelligence and big data technologies.

The acquisition of TNM was intended to enhance the Company’s presence in the new media and advertising sectors.

In

September 2021, the Company and the Company’s wholly owned subsidiary, Information Security Technology (China) Co., Ltd. (“IST”)

entered into an equity transfer agreement with Mr. Jianghuai Lin, the sole shareholder of iASPEC. Upon closing of the equity transfer,

the Company’s previous variable interest entity structure was dissolved and iASPEC became a wholly owned indirect subsidiary of

the Company.

In

2021, the Company ventured into blockchain related business through the launch of cryptocurrency mining operations and established new

subsidiaries in Hong Kong to diversity revenue streams, following a decline in its Traditional Information Technology (TIT) business

segment. In December 2022, the Company entered into a series of contracts with certain third parties to sell its cryptocurrency mining

and related equipment for a total sale price of approximately $1.08 million. The Company also terminated the leases for both the office

facility and the storage rooms, which were previously used to house most of its mining machines for its cryptocurrency mining operations,

and laid off relevant employees. As a result, the Company had ceased its cryptocurrency mining business by December 31, 2022.

We

report financial and operational information in the following three segments:

| |

(1) |

Cloud-based

Technology (CBT) segment — It includes the Company’s cloud-based products, high-end data storage servers and related

services sold to private sectors including new media, healthcare, education and residential community management, and among other

industries and applications. In this segment, the Company generates revenues from the sales of hardware and software total solutions

with proprietary software and content as well as from designing and developing software products specifically customized for private

sector customers’ needs for a fixed price. The Company includes the revenue and cost of revenue of high-end data storage servers

in the CBT segment. Advertising services are included in the CBT segment, after the Company consummated the acquisition of TNM. Advertisements

are delivered to the ads display terminals and vehicular ads display terminals through the Company’s cloud-based new media

sharing platform. Incorporation of advertising services complements the Company’s out-of-home advertising business strategy. |

| |

|

|

| |

(2) |

Blockchain

Technology (BT) segment — The BT segment is the Company’s newly formed business sector. Cryptocurrency mining is the

first initiative implemented in the BT segment. However, due to the decreased output and the highly volatile cryptocurrency market,

the Company had ceased the operation of the BT segment by December 2022.

|

| |

(3) |

Traditional Information

Technology (TIT) segment —The TIT segment includes the Company’s project-based technology products and services sold

to the public sector. The solutions the Company has sold primarily include Geographic Information Systems (GIS), Digital Public Security

Technology (DPST), and Digital Hospital Information Systems (DHIS). In this segment, the Company generates revenues from sales of

hardware and system integration services. As a result of the business transformation, the TIT segment was gradually phased out in

2021. |

Corporate

Information

Taoping

Inc. was incorporated in the British Virgin Islands, or BVI, under the BVI Act on June 18, 2012. The address of our principal place of

business is 21st Floor, Everbright Bank Building, Zhuzilin, Futian District, Shenzhen 518040 Guangdong China. Our telephone

number is 86-755-83708333. Taoping’s registered agent in the BVI is Maples Corporate Services (BVI) Limited of Kingston Chambers,

PO Box 173, Road Town, Tortola, British Virgin Islands.

The

Offering

| Ordinary Shares Offered by the Company |

|

Ordinary shares having an aggregate offering price

of up to $1,000,000, and 43,394 ordinary shares as Commitment Fee Shares |

| |

|

|

| Ordinary Shares Outstanding

Immediately Before the Offering* |

|

18,167,973 shares as of July 17, 2023 |

| |

|

|

| Manner of Offering |

|

See “Plan of Distribution” beginning

on page S-6. |

| |

|

|

| Market for the Ordinary Shares |

|

Our ordinary shares are

traded on the Nasdaq Capital Market under the symbol “TAOP.” |

| |

|

|

| Use of Proceeds |

|

We intend to use the net

proceeds from this offering for working capital and other general corporate purposes. See “Use of Proceeds” on page S-5

of this prospectus supplement. |

| |

|

|

| Risk Factors |

|

Investing in our securities

involves a high degree of risk. For a discussion of factors you should consider carefully before deciding to invest in our securities,

see “Risk Factors” beginning on page S-4 of this prospectus supplement and on page 8 of the accompanying prospectus and

other information included or incorporated by reference in this prospectus supplement and the accompanying prospectus. |

| |

|

|

| Transfer Agent and Registrar |

|

TranShare Corporation |

The

number of our ordinary shares outstanding immediately before this offering excludes:

| |

● |

333,348

ordinary shares issuable upon the vesting of restricted share units outstanding as of July 17, 2023; and |

| |

● |

1,749,288 ordinary shares

available for future issuance under our equity incentive plan as of July 17, 2023. |

RISK

FACTORS

Any

investment in our securities involves a high degree of risk. You should consider carefully the risks described below as well as the risks

described in the section captioned “Risk Factors” in our annual report on Form 20-F for the year ended December 31, 2022,

and as updated by any document that we subsequently file with the SEC that is incorporated by reference in this prospectus supplement

or the accompanying prospectus, together with other information in this prospectus supplement, the accompanying prospectus and the information

and documents incorporated by reference in this prospectus supplement and the accompanying prospectus before you make a decision to invest

in our securities. If any of such risks actually occur, our business, operating results, prospects or financial condition could be materially

and adversely affected. This could cause the trading price of our ordinary shares to decline and you may lose all or part of your investment.

The risks described below are not the only ones that we face. Additional risks not presently known to us or that we currently deem immaterial

may also affect our business operations. The risks discussed below also include forward-looking statements and our actual results may

differ substantially from those discussed in these forward-looking statements. See “Forward-Looking Information.”

RISKS

RELATED TO THIS OFFERING

We

will have broad discretion as to the use of the proceeds from this offering, and we may not use the proceeds effectively.

We

have considerable discretion in the application of the net proceeds of this offering. You will not have the opportunity, as part of your

investment decision, to assess whether the net proceeds are being used in a manner agreeable to you. You must rely on our judgment regarding

the application of the net proceeds of this offering. The net proceeds may be used for corporate purposes that do not improve our profitability

or increase the price of our shares. The net proceeds may also be placed in investments that do not produce income or that lose value.

The failure to use such funds by us effectively could have a material adverse effect on our business, financial condition, operating

results and cash flow.

A

large number of shares may be sold in the market following this offering, which may depress the market price of our ordinary shares.

The

ordinary shares sold in the offering will be freely tradable without restriction or further registration under the Securities Act. As

a result, a substantial number of our ordinary shares may be sold in the public market following this offering. If there are significantly

more ordinary shares offered for sale than buyers are willing to purchase, then the market price of our ordinary shares may decline to

a market price at which buyers are willing to purchase the offered ordinary shares and sellers remain willing to sell the ordinary shares.

USE

OF PROCEEDS

The

amount of proceeds from this offering will depend upon the number of our ordinary shares sold and the price at which they are sold. There

can be no assurance that we will be able to sell any shares under or fully utilize the SEPA as a source of financing. We intend to use

the net proceeds, if any, from this offering for working capital and general corporate purposes.

As

of the date of this prospectus supplement, we cannot specify with certainty all of the particular uses for the net proceeds we will have

upon completion of this offering. Accordingly, our management will have broad discretion in the application of net proceeds, if any.

This

prospectus also relates to our ordinary shares that may be offered and sold from time to time by the Investor. All of the ordinary shares

offered by the Investor pursuant to this prospectus will be sold by the Investor for its own account. We will not receive any of the

proceeds from these sales.

Pending

the uses described above, we plan to invest the net proceeds from this offering in cash or cash equivalents.

PLAN

OF DISTRIBUTION

On

July 17, 2023, the Company entered into the SEPA with the Investor. Pursuant to the SEPA, the Company shall have the right, but not the

obligation, to sell to the Investor up to $1,000,000 of its ordinary shares upon the Company’s written request during the twenty-four

months following execution of the SEPA, or the Commitment Period. At any time during the Commitment Period, the Company may require the

Investor to purchase its ordinary shares by delivering an advance notice (the “Advance Notice”). The shares would be purchased

pursuant to the SEPA at 85.0% of the Market Price and would be subject to certain limitations, including that the Investor could not

purchase any shares that would result in it owning more than 4.99% of our ordinary shares.

Delivery

of the shares against payment therefor in respect of each Advance Notice shall be settled promptly following each sale pursuant to the

SEPA. In connection with any Advance Notice, if any portion of an advance would cause the Investor’s beneficial ownership of our

then outstanding ordinary shares to exceed 4.99%, then such portion shall automatically be deemed to be withdrawn by us (with no further

action required by us) and modified to reduce the amount of the advance requested by an amount equal to such withdrawn portion. We may

terminate the SEPA upon five trading days’ prior notice to the Investor, provided that there are no Advance Notices outstanding

and we have paid to the Investor all amounts then due.

In

addition to the issuance of our ordinary shares to the Investor pursuant to the SEPA, this prospectus supplement also covers the resale

of those shares from time to time by the Investor to the public. Though we have been advised by the Investor, and the Investor

represents in the SEPA, that the Investor is purchasing the shares for its own account, for investment purposes in which it takes investment

risk (including, without limitation, the risk of loss), and without any view or intention to distribute such shares in violation of the

Securities Act or any other applicable securities laws, the SEC may take the position that the Investor may be deemed an “underwriter”

within the meaning of Section 2(a)(11) of the Securities Act. We have agreed in the SEPA to provide customary indemnification to the

Investor. It is possible that our shares may be sold by the Investor in one or more of the following manners:

| |

● |

ordinary brokerage transactions and transactions in

which the broker solicits purchasers; |

| |

|

|

| |

● |

a block trade in which the broker or dealer so engaged

will attempt to sell the shares as agent, but may position and resell a portion of the block as principal to facilitate the transaction; |

| |

|

|

| |

● |

to a broker-dealer as principal and resale by the broker-dealer

for its account; or |

| |

|

|

| |

● |

a combination of any such methods of sale. |

The

Investor has agreed that, during the term of the SEPA, neither the Investor nor its affiliates will engage in any short sales or hedging

transactions with respect to our ordinary shares, provided that upon receipt of an advance notice, the Investor may sell shares that

it is obligated to purchase under such advance notice prior to taking possession of such shares.

The

Investor will be subject to liability under the federal securities laws and must comply with the requirements of the Exchange Act, including

without limitation, Rule 10b-5 and Regulation M under the Exchange Act. These rules and regulations may limit the timing of purchases

and sales of our ordinary shares by the Investor. Under these rules and regulations, The Investor:

| |

● |

may not engage

in any stabilization activity in connection with our securities; |

| |

|

|

| |

● |

must furnish

each broker which offers shares of our ordinary shares covered by the prospectus supplement and accompanying prospectus that are

a part of our registration statement with the number of copies of such prospectus supplement and accompanying prospectus which are

required by each broker; and |

| |

|

|

| |

● |

may not bid

for or purchase any of our securities or attempt to induce any person to purchase any of our securities other than as permitted under

the Exchange Act. |

These

restrictions may affect the marketability of the shares by the Investor.

Transfer

Agent and Registrar

The

transfer agent and registrar for our ordinary shares is TranShare Corporation, 17755 US Highway 19 N, Suite 140, Clearwater, FL 33764,

and its telephone number is (303) 662-1112.

Listing

Our

ordinary shares are traded on the Nasdaq Capital Market under the symbol “TAOP.”

LEGAL

MATTERS

The

validity of the issuance of the ordinary shares offered hereby will be passed upon for us by Maples and Calder. Certain other

legal matters will be passed upon for us by Bevilacqua PLLC. Bevilacqua PLLC may rely upon Maples and Calder with respect to matters

of the laws of the Cayman Islands.

EXPERTS

The

consolidated financial statements of Taoping Inc. as of December 31, 2020 and for the year ended December 31, 2020 appearing in Taoping

Inc.’s Annual Report on Form 20-F for the year ended December 31, 2022 and incorporated by reference in this prospectus supplement

and the accompanying prospectus, have been audited by UHY LLP, an independent registered public accounting firm, as set forth in their

report thereon dated April 30, 2021. Such financial statements are incorporated herein by reference in reliance upon such report given

on the authority of said firm as experts in auditing and accounting.

The

consolidated financial statements of Taoping Inc. as of December 31, 2022 and 2021 and for the years ended December 31,

2022 and 2021 appearing in Taoping Inc.’s Annual Report on Form 20-F for the year ended December 31, 2022 and incorporated by reference

in this prospectus supplement and the accompanying prospectus, have been audited by PKF Littlejohn LLP, an independent registered public

accounting firm, as set forth in their report thereon dated April 25, 2023. Such financial statements are incorporated herein by reference

in reliance upon such report given on the authority of said firm as experts in auditing and accounting.

INCORPORATION

OF CERTAIN INFORMATION BY REFERENCE

The

SEC allows us to “incorporate by reference” the information we file with it into this prospectus supplement. This means that

we can disclose important information about us and our financial condition to you by referring you to another document filed separately

with the SEC instead of having to repeat the information in this prospectus supplement. The information incorporated by reference is

considered to be part of this prospectus supplement and later information that we file with the SEC will automatically update and supersede

this information. We incorporate by reference into this prospectus supplement the information contained in the documents listed below

and any future filings made by us with the SEC under Section 13(a), 13(c) or 15(d) of the Exchange Act, except for information “furnished”

to the SEC which is not deemed filed and not incorporated by reference into this prospectus (unless otherwise indicated below), until

the termination of the offering of securities described in the applicable prospectus supplement:

| |

● |

the

Company’s Annual Report on Form 20-F for the fiscal year ended December 31, 2022, filed with the SEC on April 25, 2023; |

| |

|

|

| |

● |

The

description of the Company’s ordinary shares contained in the Form

8-K12B, filed with the SEC on October 31, 2012, and any further amendment or report filed hereafter for the purpose of updating

such description; and |

| |

|

|

| |

● |

all subsequent reports

on Form 20-F and any report on Form 6-K that so indicates it (or any applicable portions thereof) is being incorporated by reference

that we file with or furnish to the SEC on or after the date hereof and until the termination or completion of this offering. |

You

may obtain any of the documents incorporated by reference in this prospectus supplement from the SEC at the SEC’s website at http://www.sec.gov.

WHERE

YOU CAN FIND MORE INFORMATION

We

have filed with the SEC a registration statement on Form F-3 (File No. 333-262181) under the Securities Act with respect to the securities

offered by this prospectus supplement. This prospectus supplement and the accompanying prospectus, which constitute a part of our registration

statement on Form F-3, omit some information contained in the registration statement in accordance with SEC rules and regulations. You

should review the information and exhibits in the registration statement for further information on us and the securities we are offering.

Statements in this prospectus supplement and the accompanying prospectus concerning any document we filed as an exhibit to the registration

statement or that we otherwise filed with the SEC are not intended to be comprehensive and are qualified by reference to these filings.

You should review the complete document to evaluate these statements.

The

SEC maintains an Internet site that contains reports, information statements and other information regarding issuers, such as us, that

file electronically with the SEC (http://www.sec.gov).

Additionally,

we make these filings available, free of charge, on our website at www.taop.com as soon as reasonably practicable after we electronically

file such materials with, or furnish them to, the SEC. The information on our website, other than these filings, is not, and should not

be, considered part of this prospectus supplement and is not incorporated by reference into this document.

PRELIMINARY

PROSPECTUS

TAOPING

INC.

$100,000,000

Ordinary

Shares

Debt

Securities

Warrants

Rights

Units

Taoping

Inc., a British Virgin Islands Business Company, may offer, issue and sell from time to time ordinary shares, no par value (the “Ordinary

Shares”), debt securities, warrants, rights or units up to $100,000,000 or its equivalent in any other currency, currency units,

or composite currency or currencies in one or more issuances. Throughout this prospectus, unless the context indicates otherwise, references

to “Taoping” or “the Company” refer to Taoping Inc., a holding company and references to “we,” “us,”

“our” or “our company” are to Taoping and its consolidated subsidiaries.

Taoping

may sell any combination of these securities in one or more offerings. This prospectus describes some of the general terms that may apply

to these securities and the general manner in which they may be offered. The specific terms of any securities to be offered, and the

specific manner in which they may be offered, will be described in a supplement to this prospectus or incorporated into this prospectus

by reference. You should read this prospectus and any supplement carefully before you invest. Each prospectus supplement will indicate

if the securities offered thereby will be listed or quoted on a securities exchange or quotation system.

The

information contained or incorporated in this prospectus or in any prospectus supplement is accurate only as of the date of this prospectus,

or such prospectus supplement, as applicable, regardless of the time of delivery of this prospectus or any sale of our securities.

The

Ordinary Shares are listed on the NASDAQ Capital Market under the symbol “TAOP.” On June 8, 2022, the closing sale price

of the Ordinary Share was $1.31. As of June 8, 2022, the aggregate market value of outstanding

Ordinary Shares held by non-affiliates was approximately $16.15 million based on 15,590,789

outstanding Ordinary Shares, of which approximately 10,767,875 Ordinary Shares were held by non-affiliates, and the last sale price of

Ordinary Shares as reported by the Nasdaq Capital Market of $1.5002 per share on June

3, 2022, which was the highest closing price of Ordinary Shares reported on the NASDAQ Capital Market within the last 60 days

prior to the date of this filing. Taoping has offered approximately $4.98 million of Ordinary Shares pursuant to General Instruction

I.B.5 of Form F-3 during the prior 12 calendar month period that ends on, and includes, the date of this prospectus.

Taoping

may offer securities through underwriting syndicates managed or co-managed by one or more underwriters, through agents, or directly to

purchasers. The prospectus supplement for each offering of securities will describe the plan of distribution for that offering. For general

information about the distribution of securities offered, please see “Plan of Distribution” in this prospectus.

Investing

in Taoping’s securities involves a high degree of risk. You are urged to carefully consider the risk factors beginning on page

8 of this prospectus, in any accompanying prospectus supplement and in any related free writing prospectus, and in the documents incorporated

by reference into this prospectus, any accompanying prospectus supplement and any related free writing prospectus before making any decision

to invest in the securities.

Investors

purchasing securities in this offering are purchasing securities of Taoping, the British Virgin Islands holding company rather than securities

of Taoping’s subsidiaries that have substantive business operations in China and other countries.

Taoping

is not an operating company but rather a holding company incorporated in the British Virgin Islands. Because Taoping has no business

operations of its own, we conduct our business through Taoping’s operating subsidiaries, primarily in Hong Kong, mainland China

and Kazakhstan. This structure involves unique risks to investors and you may never directly hold equity interests in Taoping’s

operating entities. You are specifically cautioned that there are significant legal and operational risks associated with being based

in or having the majority of operations in China, including that changes in the legal, political and economic policies of the Chinese

government, the relations between China and the United States, or Chinese or United States regulations may materially and adversely affect

our business, financial condition, results of operations and the market price of Taoping’s securities. Moreover, the Chinese government

may exercise significant oversight and discretion over the conduct of our business and may intervene in or influence our operations at

any time, which could result in a material change in our operations and/or the value of the securities being registered for sale or could

significantly limit or completely hinder Taoping’s ability to offer or continue to offer securities to investors and cause the

value of such securities to significantly decline or be worthless. For a detailed description of risks related to the holding

corporate structure, see “Risk Factors — Risks Related to Doing Business in China — There are uncertainties

regarding the interpretation and enforcement of PRC laws, rules and regulations” on page 9.

Specifically,

the government of China (which is also referred to as “PRC”) recently initiated a series of regulatory actions and made a

number of public statements on the regulation of business operations in China, including cracking down on illegal activities in the securities

market, enhancing supervision over China-based companies listed overseas using a variable interest entity structure, adopting new measures

to extend the scope of cybersecurity reviews, and expanding efforts in anti-monopoly enforcement. We do not believe that our subsidiaries

in Hong Kong or mainland China are directly subject to these regulatory actions or statements, as we have not carried out any monopolistic

behavior and our business does not involve the collection of personal information or implicate national security. We also have dissolved

the variable interest entity structure in 2021 as our business does not involve any type of restricted industry. However, since these

statements and regulatory actions by the PRC government are newly published and detailed official guidance and related implementation

rules have not been issued or taken effect, uncertainties exist as to how soon the regulatory bodies in China will finalize implementation

measures, and the impacts the modified or new laws and regulations will have on our daily business operation, the ability to accept foreign

investments and list securities on an U.S. or other foreign exchange. For a detailed description of various risks related to doing

business in China, see “Risk Factors — Risks Related to Doing Business in China” beginning on page 8.

In

addition, pursuant to the Holding Foreign Companies Accountable Act (the “HFCA Act”) enacted in 2020, if the auditor of a

U.S. listed company’s financial statements is not subject to Public Company Accounting Oversight Board (the “PCAOB”)

inspections for three consecutive “non-inspection” years, the Securities and Exchange Commission (the “SEC”)

is required to prohibit the securities of such issuer from being traded on a U.S. national securities exchange, such as NYSE and Nasdaq,

or in U.S. over-the-counter markets. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies

Accountable Act, which, if enacted into law, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from

trading on U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive “non-inspection” years

instead of three. The PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate

completely registered public accounting firms headquartered in mainland China and Hong Kong because of a position taken by one or more

authorities in such jurisdictions. In addition, the PCAOB’s report identified specific registered public accounting firms which

are subject to these determinations. Our current registered public accounting firm, PKF Littlejohn LLP (“PKF”), or our former

registered public accounting firm, UHY LLP, is not headquartered in mainland China or Hong Kong and was not identified

in this report as a firm subject to the PCAOB’s determination. They both are subject to full inspection by the PCAOB and the PCAOB

is able to inspect the audit workpapers of our China subsidiaries, as such workpapers are electronic files possessed by our registered

public accounting firms. However, if the PCAOB determines in the future that it cannot inspect or fully investigate our auditor at such

future time, trading in Taoping’s securities would be prohibited under the HFCA Act. See “Risk Factor—Risks

Related to Doing Business in China— The increased regulatory scrutiny focusing on U.S.-listed companies with significant operations

in China in the U.S. could add uncertainties to our business operations, share price and reputation. Although our former auditor, UHY

LLP, and current auditor, PKF, are both subject to inspection by the PCAOB, trading in our securities may be prohibited under the Holding

Foreign Companies Accountable Act if the PCAOB subsequently determines our audit work is performed by auditors that the PCAOB is unable

to inspect or investigate completely, and as a result, U.S. national securities exchanges, such as the Nasdaq, may determine to delist

Taoping’s securities. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable

Act, which, if enacted, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on any U.S.

stock exchanges if its auditor is not subject to the PCAOB inspections for two consecutive years instead of three.” on page

14.

Cash

is transferred through our organization in the following manner:

| |

● |

Our equity structure is

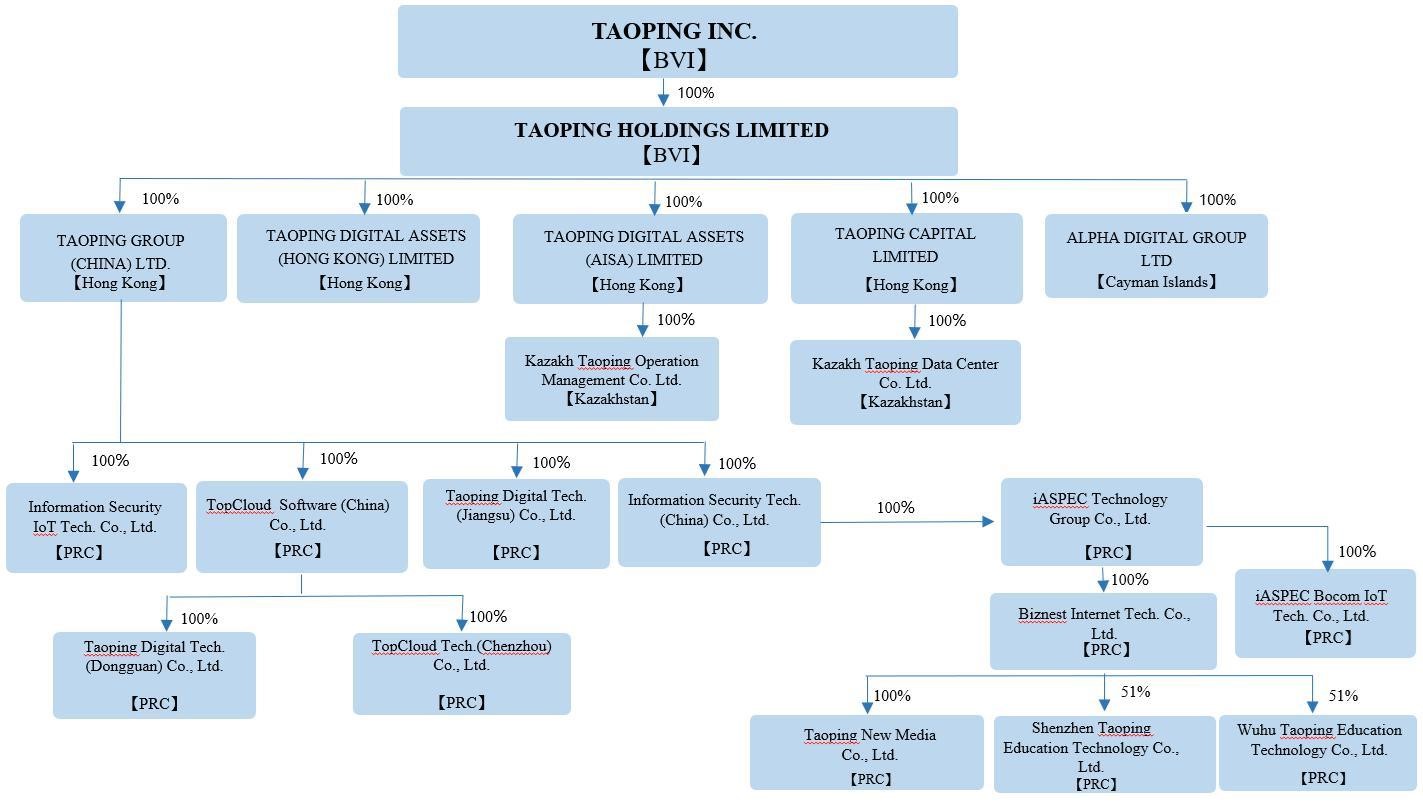

a direct holding structure, that is, Taoping, the British Virgin Islands entity listed in the U.S., controls its operating subsidiaries

in Hong Kong, mainland China and Kazakhstan, through Taoping Holdings Limited, a British Virgin Islands subsidiary of Taoping (“Taoping

Holdings”). See “Prospectus Summary—Corporate Structure” on page 4 for more details. |

| |

|

|

| |

● |

As of the date of this

prospectus, neither Taoping nor any of its subsidiaries have paid dividends or made distributions to U.S. investors. |

| |

|

|

| |

● |

Within our direct holding

structure, the cross-border transfer of funds from Taoping to its Chinese subsidiaries is legal and compliant with the laws and regulations

of China. Taoping is permitted to provide funding to its subsidiaries in Hong Kong, mainland China and Kazakhstan in the form of

shareholder loans or capital contributions, subject to satisfaction of applicable government registration, approval and filing requirements

of the respective jurisdiction. There are no quantity limits on Taoping’s ability to make capital contributions to its subsidiaries

in mainland China under the PRC regulations. However, the subsidiaries in mainland China may only procure shareholder loans from

Taoping Group (China) Ltd., a Hong Kong subsidiary that owns all subsidiaries in mainland China (“Taoping Group”), to

the extent of the difference between their respective registered capital and total investment amount as recorded in the Chinese Foreign

Investment Comprehensive Management Information System. In the event that proceeds are received by Taoping from selling its securities

being offered hereby, the funds can be directly transferred to Taoping Group and then transferred to its subordinate entities. Historically

cash proceeds raised from overseas financing activities were transferred by Taoping to our Chinese subsidiaries via capital contribution

or shareholder loans, as the case may be. |

| |

|

|

| |

● |

As a holding company, Taoping

relies on dividends and other distributions on equity paid by its operating subsidiaries in Hong Kong, mainland China and Kazakhstan

for cash requirements, including the funds necessary to pay dividends and other cash distributions to its shareholders or to any

service expenses it may incur. To make transfers, transfers, dividends or distributions to Toping, our operating subsidiaries in

mainland China will need first transfer funds to Taoping Group in accordance with applicable laws and regulations of Hong Kong and

mainland China and then to Taoping through Taoping Holdings. Taoping will then distribute dividends to its shareholders in proportion

to their respective shareholding, regardless of whether the shareholders are U.S. investors or investors in other countries or regions.

As of the date of this prospectus, none of our subsidiaries has made any transfers, dividends or other distributions to Taoping,

the holding company. We intend to retain most, if not all, of our available funds and any future earnings after this offering

to the development and growth of our business and do not expect to pay dividends in the foreseeable future. |

| |

|

|

| |

● |

The ability of our subsidiaries

in mainland China to distribute dividends is based upon their distributable earnings. Current PRC regulations permit these subsidiaries

to pay dividends to their respective shareholders only out of their accumulated profits, if any, determined in accordance with PRC

accounting standards and regulations. In addition, each of our subsidiaries in mainland China is required to set aside at least 10%

of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital.

These reserves are not distributable as cash dividends. In addition, if any of our operating subsidiaries incurs debt on its own

behalf in the future, the instruments governing such debt may restrict its ability to pay dividends to Taoping. Other than above,

current PRC laws and regulations do not prohibit or limit using cash generated from one subsidiary to fund another subsidiary’s

operations. Our subsidiaries in mainland China have historically from time to time funded other subsidiaries’ operations. Other

than complying with the applicable PRC laws and regulations, we currently do not have our own cash management policy and procedures

that dictate how funds are transferred. |

For

more information, see the section entitled “Incorporation of Certain Information by Reference” below regarding information

of our audited consolidated financial statements for the years ended December 31, 2021, 2020 and 2019 appearing in our most recent annual

report on Form 20-F.

Neither

the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed

upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The

date of this prospectus is , 2022

TABLE

OF CONTENTS

ABOUT

THIS PROSPECTUS

This

prospectus is part of a registration statement that we filed with the Securities and Exchange Commission, or the SEC, using a “shelf”

registration process. Under this shelf registration process, Taoping may sell its securities described in this prospectus in one or more

offerings up to a total dollar amount of $100,000,000 (or its equivalent in foreign or composite currencies).

This

prospectus provides you with a general description of the securities that may be offered. Each time Taoping offers its securities, we

will provide you with a supplement to this prospectus that will describe the specific amounts, prices and terms of the securities being

offered. The prospectus supplement may also add, update or change information contained in this prospectus. This prospectus, together

with applicable prospectus supplements and the documents incorporated by reference in this prospectus and any prospectus supplements,

includes all material information relating to this offering. Please read carefully both this prospectus and any prospectus supplement

together with additional information described below under “Where You Can Find More Information.”

You

should rely only on the information contained in or incorporated by reference in this prospectus and any applicable prospectus supplement.

We have not authorized anyone to provide you with different or additional information. If anyone provides you with different or inconsistent

information, you should not rely on it. We take no responsibility for, and can provide no assurance as to the reliability of, any other

information that others may give you. The information contained in this prospectus is accurate only as of the date of this prospectus,

regardless of the time of delivery of this prospectus or any sale of securities described in this prospectus. This prospectus is not

an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale

is not permitted.

You

should not assume that the information contained in this prospectus and the accompanying prospectus supplement is accurate on any date

subsequent to the date set forth on the front of the document or that any information that we have incorporated by reference is correct

on any date subsequent to the date of the document incorporated by reference. Our business, financial condition, results of operations

and prospects may have changed since those dates.

PROSPECTUS

SUMMARY

This

summary highlights selected information that is presented in greater detail elsewhere, or incorporated by reference, in this prospectus.

It does not contain all of the information that may be important to you and your investment decision. Before investing in the securities

that Taoping is offering under this prospectus, you should carefully read this entire prospectus, including the matters set forth under

the section of this prospectus captioned “Risk Factors” and the financial statements and related notes and other information

that we incorporate by reference herein, including, but not limited to, our Annual Report on Form 20-F and our other SEC reports.

Company

Overview

We

are a leading provider of integrated cloud-based platform, resource sharing functionality, and big data solutions to the Chinese new

media, education residential community management, and elevator IoT industries. Our Internet ecosystem enables all participants of the

new media community to efficiently promote brands, disseminate information, and share resources. In addition, we provide a broad portfolio

of software, hardware and fully integrated solutions, including information technology infrastructure and Internet-enabled display technologies

to customers in government, education, healthcare, media, transportation, and other private sectors. We also engage in cryptocurrency

mining and blockchain related business operations as a part of business transformation.

The

outbreak of COVID-19 has negatively impacted our business. Starting from January 2020, to prevent the spread of COVID-19, the Chinese

government has taken strict quarantine measures, such as nationwide lockdowns, transportation restrictions, public gathering prohibitions

and temporary closures of non-essential businesses, which had put economic activities in a suspension mode until late March 2020. Although

the COVID-19 pandemic was largely contained in China since early 2020 and businesses have gradually resumed to normal operations, China’s

out-of-home advertising market was adversely impacted. In addition, imported infection cases and regional outbreaks of infection persisted

throughout 2021.

On

June 9, 2021, we consummated an acquisition of 100% equity interest of Taoping New Media Co., Ltd. (“TNM”) that focuses on

digital advertising in the out-of-home advertising market. By synergizing our cloud-based new media resource sharing platform and technology

with TNM’s advertising customers, including Taoping Alliance members, we expect to have more prominent presence in the out-of-home

advertising market and improve our business profitability.

In

early 2021, we launched blockchain related new business in cryptocurrency mining operations and established subsidiaries in Hong Kong

to supplement its diminished Traditional Information Technology (TIT) business segment as a part of new business transformation. With

multiple cloud data centers deployed overseas, currently in Hong Kong, we continue to improve computing power and create value for the

encrypted digital currency industry.

In

September 2021, we relocated our global corporate headquarters from Shenzhen, China to Hong Kong as part of the implementation of our

global growth strategy. As a result, the executive offices of the Company are now located at Unit

3102, 31/F, Citicorp Centre, 18 Whitefield Road, Hong Kong. Our offices in Shenzhen, China currently serve as our regional headquarters

in mainland China.

In

September 2021, we dissolved the variable interest entity (the “VIE”) structure by exercising the purchase option under the

purchase option agreement dated July 1, 2007 entered into by and among iASPEC Technology Group Co., Ltd. (“iASPEC”), iASPEC’s

shareholders and Information Security Technology (China) Co., Ltd., a wholly owned PRC subsidiary of Taoping (“IST”), to

purchase all of the equity interests in iASPEC at an aggregate exercise price of $1,800,000. On September 18, 2021, Taoping and IST also

entered into an equity transfer agreement with iASPEC and iASPEC’s then sole shareholder, Mr. Jianghuai Lin (“Mr. Lin”),

the chief executive officer and chairman of Taoping, under which Mr. Lin agreed to sell and transfer to IST all of the equity interests

in and any and all rights and benefits relating thereto of iASPEC in exchange for 612,245 unregistered Ordinary Shares of Taoping, as

determined by dividing $1,800,000 by the volume-weighted average closing price of Ordinary Shares for the consecutive five (5) trading

days immediately prior to September 18, 2021. The parties thereafter completed the applicable PRC governmental registration(s) to effectuate

the transfer of the equity interests.

For

the year ended December 31, 2021, our total revenue was $24.8 million, of which approximately $0.2 million was from related parties,

compared to total revenue of $11.0 million for the year ended December 31, 2020, an increase of $13.8 million, or 124.6%. The revenue

increase was mainly contributed by products and software sales totaling $5.8 million, advertising from TNM of $2.6 million, and cryptocurrency

mining of $5.5 million.

Corporate

Information

Taoping

was incorporated in the British Virgin Islands under the BVI Business Companies Act (as amended) (the “BVI Act”) on June

18, 2012. Our principal executive offices are located at Unit 3102, 31/F, Citicorp Centre, 18 Whitefield Road, Hong Kong. The telephone

number at our executive offices is 852-36117837.

Taoping’s

registered agent in the British Virgin Islands is Maples Corporate Services (BVI) Limited of Kingston Chambers, PO Box 173, Road Town,

Tortola, British Virgin Islands. Taoping’s agent for service of process in the United States is Cogency Global Inc., located at

122 East 42nd Street, 18th Floor, New York, NY 10168.

Our

website can be found at http://www.taop.com. Information on our website is not incorporated by reference into this prospectus, any prospectus

supplement or into any information incorporated herein by reference. You should not consider information on our website to be part of

this prospectus, prospectus supplement, any free writing prospectus or any information incorporated by reference herein.

Corporate

Structure

The

following diagram illustrates our current corporate structure.

Summary

of Risk Factors

There

are a number of risks that you should consider and understand before making an investment decision regarding the securities being offered

under this prospectus. You should carefully consider all of the information set forth in this prospectus and, in particular, the specific

factors set forth in the section titled “Risk Factors” below. These risks include, but are not limited to:

| |

● |

As of the date of this

prospectus, we believe that we are not required to obtain any approval or prior permission for Taoping to offer its securities to

foreign investors from the China Securities Regulatory Commission (the “CSRC”) or any other Chinese regulatory authority

under the Chinese laws and regulations currently in effect. As of the date of this prospectus, neither Taoping nor any of its subsidiaries

has been informed by the CSRC, Cybersecurity Administration of China (the “CAC”) or any other Chinese regulatory authority

of any requirements, approvals or permissions that we should obtain prior to this offering. Neither Taoping nor any of its subsidiaries

has obtained the approval or clearance from either the CSRC or any other Chinese regulatory authority for the offering that we may

make under this prospectus and any applicable prospectus supplement. However, there remains significant uncertainty as to the enactment,

interpretation and implementation of regulatory requirements related to overseas securities offerings and other capital markets activities.

The PRC regulatory agencies, including the CSRC or the CAC, may not reach the same conclusion as us. If we do not receive or maintain

the approvals, or we inadvertently conclude that such approvals are not required but the CSRC or other PRC regulatory body subsequently

determines that we need to obtain the approval for this offering or if the CSRC or any other PRC government authorities promulgates

any interpretation or implements rules subsequently that would require us to obtain CSRC or other governmental approvals for this

offering, the Company may not be able to proceed with this offering, face adverse actions or sanctions by the CSRC or any other PRC

regulatory agencies. In any such event, these regulatory agencies may impose fines and penalties on our operations in China, limit

our operating privileges in China, delay or restrict the repatriation of the proceeds from this offering into the PRC or take other

actions that could have a material adverse effect on our business, financial condition, the value of the securities that we are registering,

as well as Taoping’s ability to offer or continue to offer securities to investors or cause such securities to significantly

decline in value or become worthless. The risks arising from the legal system in China include risks and uncertainties regarding

the enforcement of laws and that rules and regulations in China can change quickly with little, if any, advance notice. As a result,

there can be no assurance that we will not be subject to such requirements, approvals or permissions in the future. For additional

information, see “Risk Factors—Risks Relating to Doing Business in China—Our business is subject to complex

and evolving laws and regulations regarding privacy and data protection. Compliance with China’s new Data Security Law, Cybersecurity

Review Measures, Personal Information Protection Law, Regulations on Network Data Security (draft for public comments), as well as

additional laws, regulations and guidelines that the Chinese government promulgates in the future may entail significant expenses

and could materially affect our business” on page 10 and “Risk Factors—Risks Relating to Doing Business in

China — The approval of the CSRC or other Chinese regulatory agencies may be required in connection with our future overseas

capital-raising activities under Chinese law” on page 12. |

| |

● |

There are significant legal and operational risks associated with having significant business operations in China, including that changes in the legal, political and economic policies of the Chinese government, the relations between China and the United States, or Chinese or United States regulations may materially and adversely affect our business, financial condition, results of operations and the value of the securities that we are registering. Any such changes may take place quickly and with very little notice and as a result, could significantly limit or completely hinder Taoping’s ability to offer or continue to offer its securities to investors, and could cause the value of Taoping’s securities to significantly decline or become worthless. Recent statements made and regulatory actions undertaken by China’s government, such as those related to data security or anti-monopoly concerns and any other future laws and regulations may require us to incur significant expenses and could materially affect our ability to conduct our business or accept foreign investments. For additional information, see “Risk Factors—Risks Relating to Doing Business in China— Changes in U.S. and Chinese regulations or in relations between the United States and China may adversely impact our business, our operating results, our ability to raise capital and the value of the securities that we are registering. Any such changes may take place quickly and with very little notice” on page 9 and “Risk Factors—Risks Relating to Doing Business in China— Our business is subject to complex and evolving laws and regulations regarding privacy and data protection. Compliance with China’s new Data Security Law, Cybersecurity Review Measures, Personal Information Protection Law, Regulations on Network Data Security (draft for public comments), as well as additional laws, regulations and guidelines that the Chinese government promulgates in the future may entail significant expenses and could materially affect our business” on page 10. |

| |

|

|

| |

● |